Gold prices rebound as risk-off mood grips markets; US payroll data awaited

Introduction & Market Context

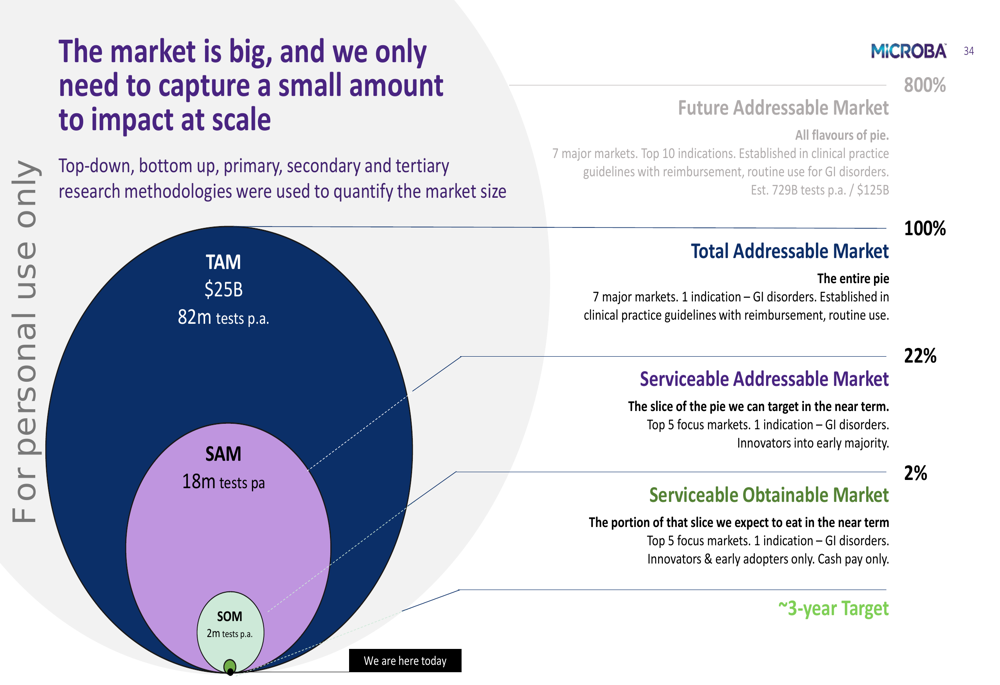

Microba Life Sciences Ltd (ASX:MAP) reported its Q1 FY26 results on October 28, 2025, highlighting significant growth in its core diagnostic products despite an overall flat revenue performance. The company is executing a strategic transition away from legacy products toward its high-growth microbiome diagnostic tests, positioning itself in what it identifies as a $25 billion market opportunity for patients with unresolved gastrointestinal disease.

The microbiome diagnostics company reported total revenue of $3.6 million, down 1% compared to the prior comparable period (PCP), while its stock price has reached a 52-week low of $0.08, reflecting ongoing market skepticism despite the company’s growth in core segments.

Quarterly Performance Highlights

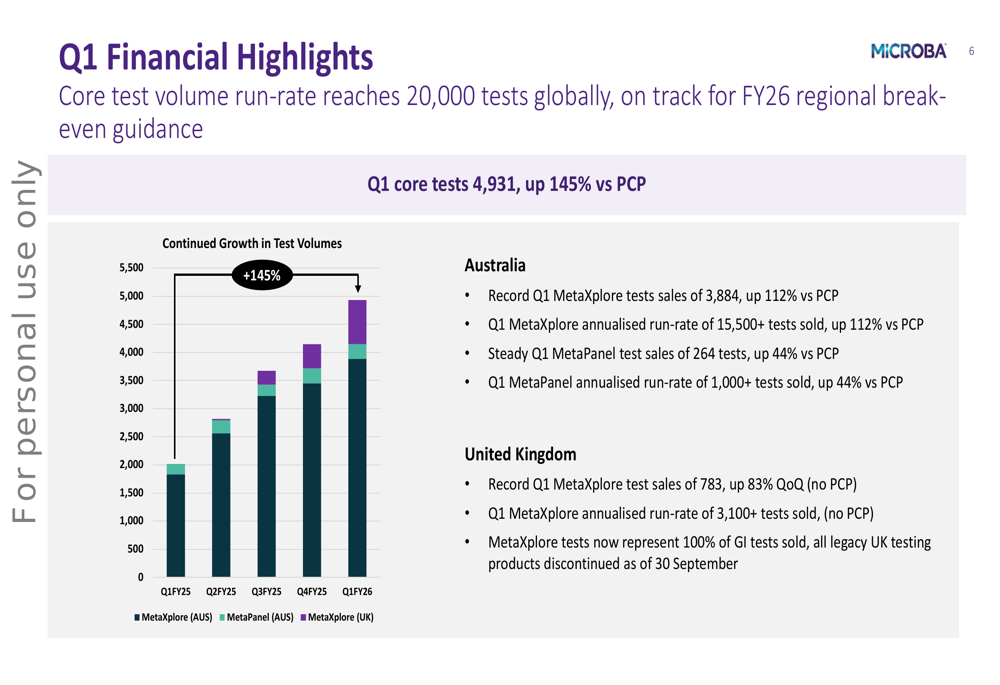

Microba’s Q1 FY26 results demonstrate strong momentum in its core test volume, which grew 145% year-over-year to 4,931 tests. The company’s core test volume run-rate has now reached 20,000 tests globally, putting it on track to achieve its FY26 regional break-even guidance.

As shown in the following chart detailing core test volume growth across markets:

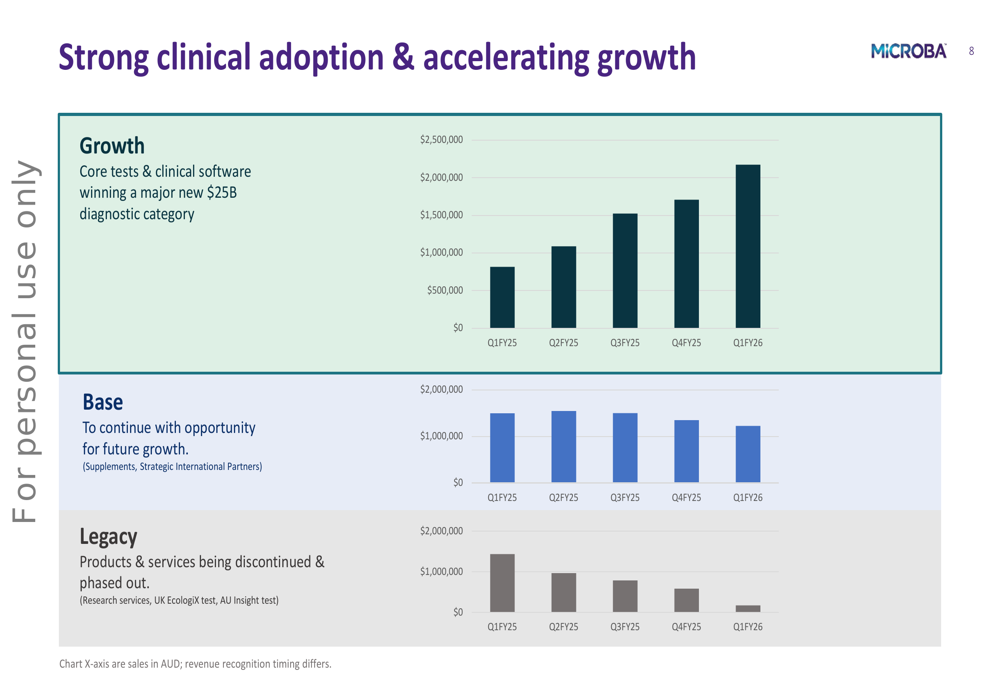

Revenue performance showed a mixed picture across product categories. While growth product revenue increased by 151% to $1.9 million compared to PCP, base product revenue declined by 15% to $1.3 million, and legacy product revenue fell by 73% to $0.4 million. The company noted that this revenue pattern aligns with its strategic discontinuation of legacy products.

The following chart illustrates the revenue breakdown across growth, base, and legacy categories:

Microba has implemented disciplined cost management measures, reducing operating expenditure by more than 26% in Q1 FY26 compared to Q4 FY25 (excluding one-off and restructuring items). The company ended the quarter with a cash balance of $13.89 million as of September 30, 2025.

Strategic Initiatives

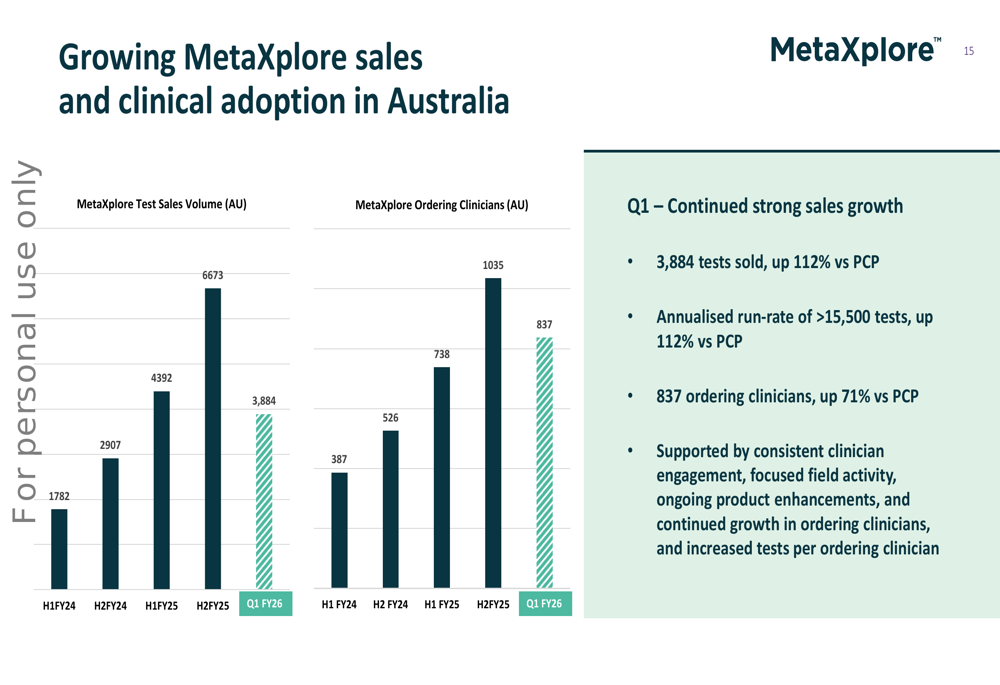

Microba is focusing on expanding its market presence in Australia and the United Kingdom, with both regions showing strong growth in test volumes. In Australia, MetaXplore test sales reached 3,884 in Q1, up 112% versus PCP, with an annualized run-rate exceeding 15,500 tests. The number of ordering clinicians grew 71% to 837.

The following chart demonstrates the growth trajectory in Australia:

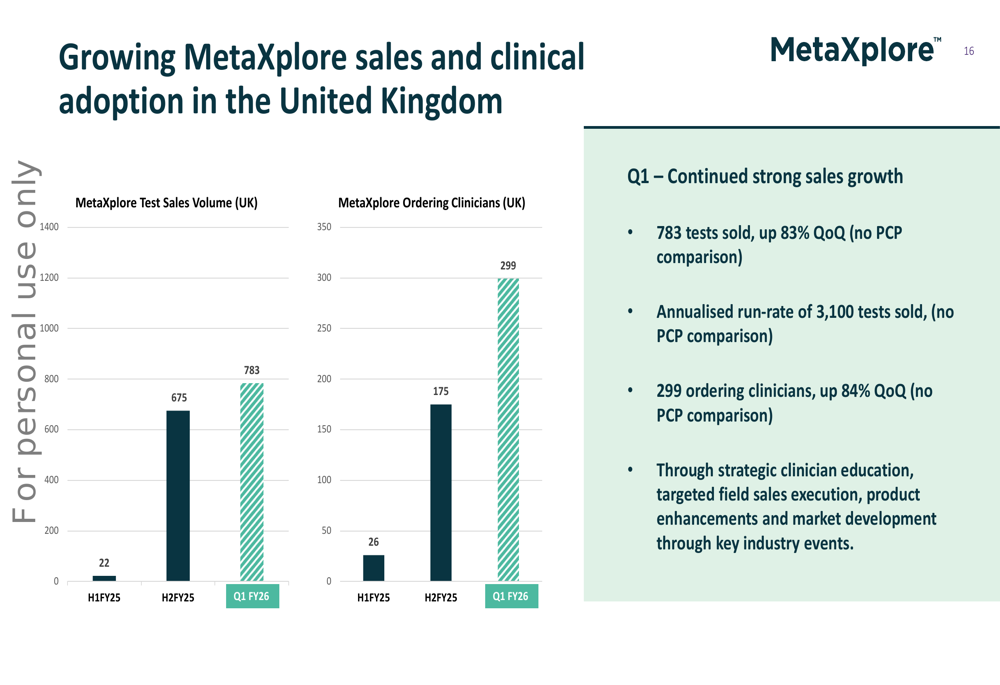

In the United Kingdom, MetaXplore test sales reached 783 in Q1, up 83% quarter-over-quarter, with an annualized run-rate of over 3,100 tests. The UK market has seen ordering clinicians increase by 84% to 299.

As illustrated in this chart of UK market performance:

The company has introduced new product features to enhance adoption, including "Practitioner Pays," which allows healthcare practitioners to order and pay for MetaXplore tests directly on behalf of patients, and "Admin Accounts," designed to ease administrative workload in busy, multi-practitioner clinics.

Additionally, Microba announced an upcoming brand consolidation in November, which will bring Co-Biome, Invivo Testing, and the MetaXplore range under the Microba brand to drive operational efficiencies and increase marketing effectiveness.

Forward-Looking Statements

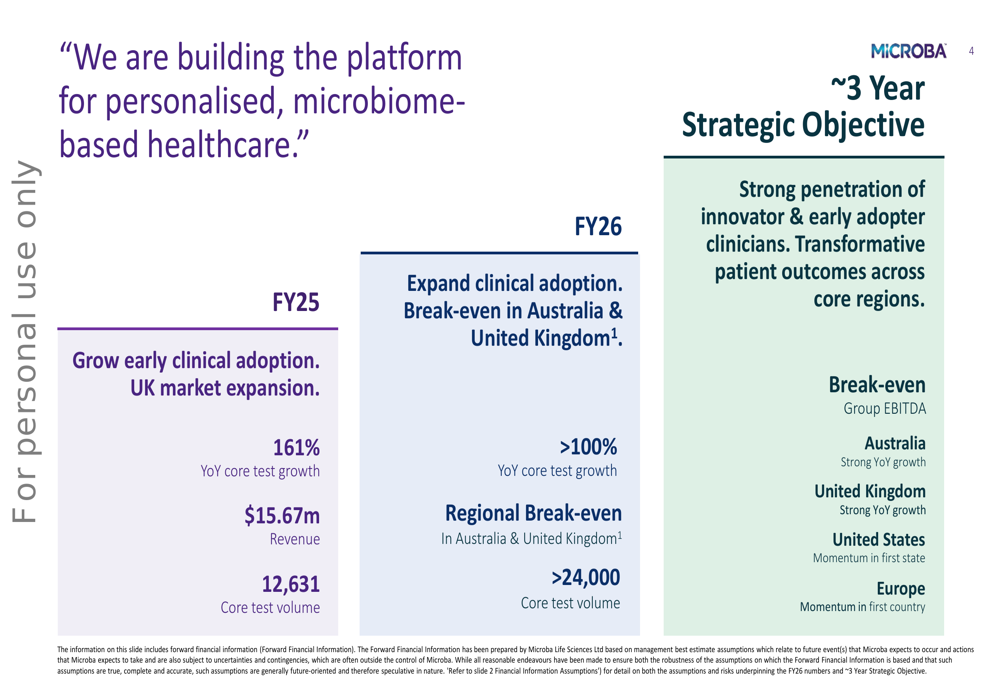

Microba has outlined clear strategic objectives for FY26, targeting regional break-even in Australia and the United Kingdom with over 24,000 core test volume. The company’s three-year strategic objective includes achieving strong penetration of innovator and early adopter clinicians, delivering transformative patient outcomes across core regions, and reaching group EBITDA break-even.

As shown in this strategic roadmap:

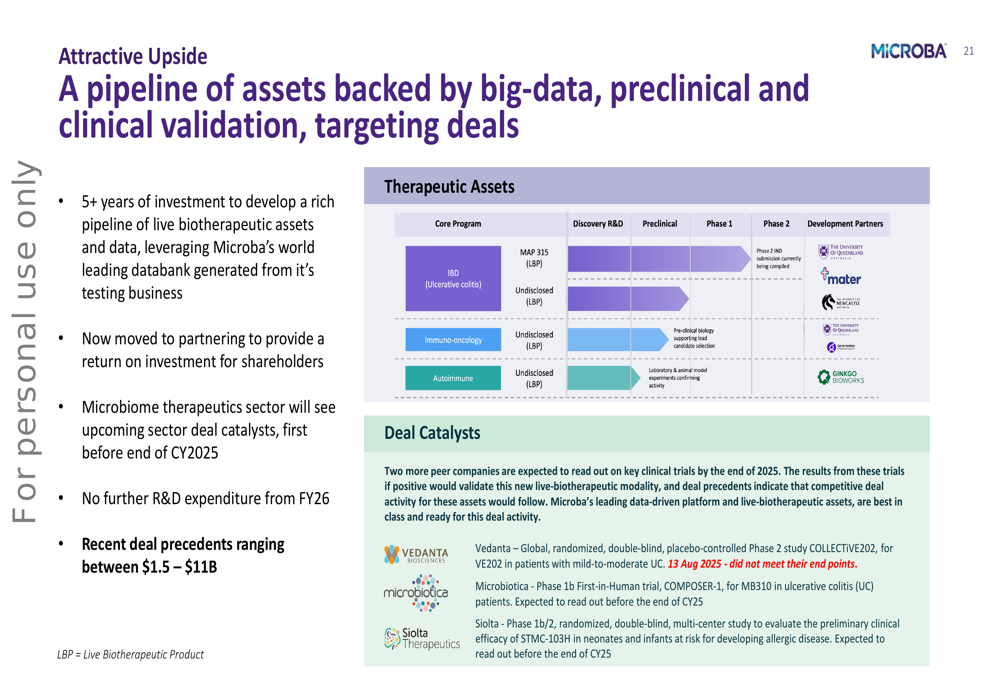

On the therapeutics front, Microba has transitioned from R&D to a partnering focus, with no further R&D expenditure planned from FY26. The company has highlighted upcoming sector deal catalysts expected before the end of CY2025, with recent deal precedents in the sector ranging between $1.5 billion and $11 billion.

The company’s therapeutics pipeline is illustrated here:

Competitive Industry Position

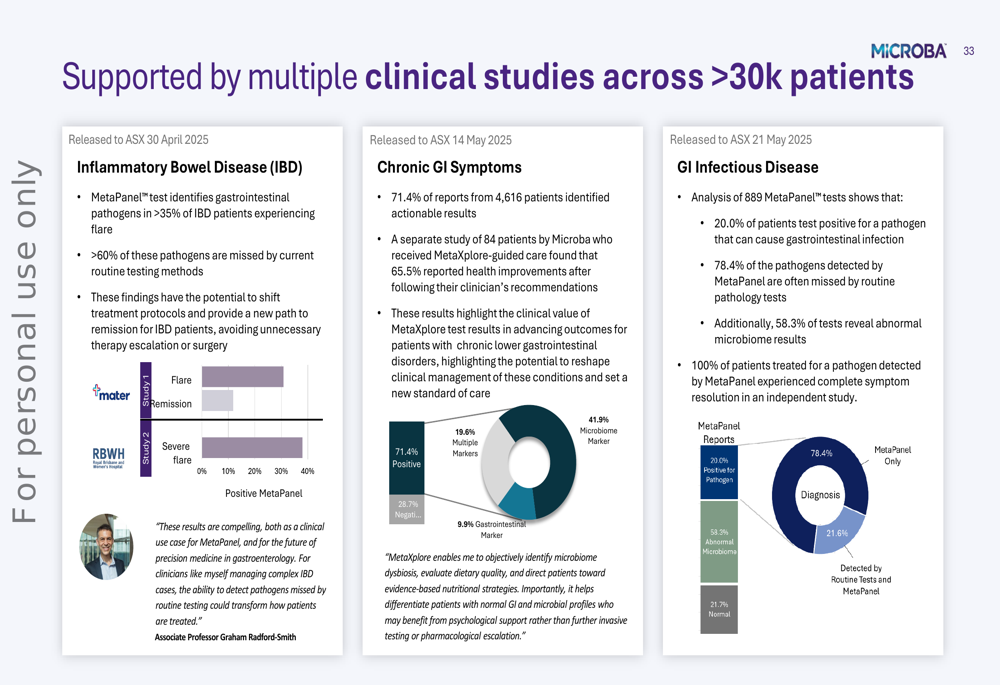

Microba positions itself at the forefront of the microbiome diagnostics and therapeutics market, which it estimates as a $1.4 trillion healthcare opportunity. The company’s diagnostic tests have shown promising clinical results, with studies indicating that 71.4% of reports from 4,616 patients identified actionable results, and 65.5% of patients reported health improvements after following their clinician’s recommendations based on MetaXplore-guided care.

The following slide demonstrates the clinical evidence supporting Microba’s products:

The company’s market opportunity assessment shows a progression from its current serviceable obtainable market to a much larger total addressable market as adoption increases:

Despite the promising growth in core test volumes and the large market opportunity, Microba faces challenges in transitioning away from legacy products while achieving regional break-even targets. The stock’s performance, currently at a 52-week low, suggests investors remain cautious about the company’s path to profitability despite the significant growth in its core diagnostic products.

With major shareholders including Sonic Healthcare (19.14%), Perennial (13.47%), and Thorney Investment Group (6.86%), Microba has established strategic partnerships with global diagnostic leaders Sonic Healthcare and SYNLAB, which could support its market expansion efforts as it progresses through the adoption curve from innovators to early adopters and eventually the early majority.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.