Here’s why Citi says crypto prices have been weak recently

Introduction & Market Context

Microchip Technology Inc (NASDAQ:MCHP) presented its fiscal first quarter 2026 results on November 6, 2025, highlighting sequential growth and margin expansion despite year-over-year revenue declines. The semiconductor manufacturer, known for its embedded control solutions, emphasized its strategic positioning across diverse markets and its consistent focus on shareholder value creation.

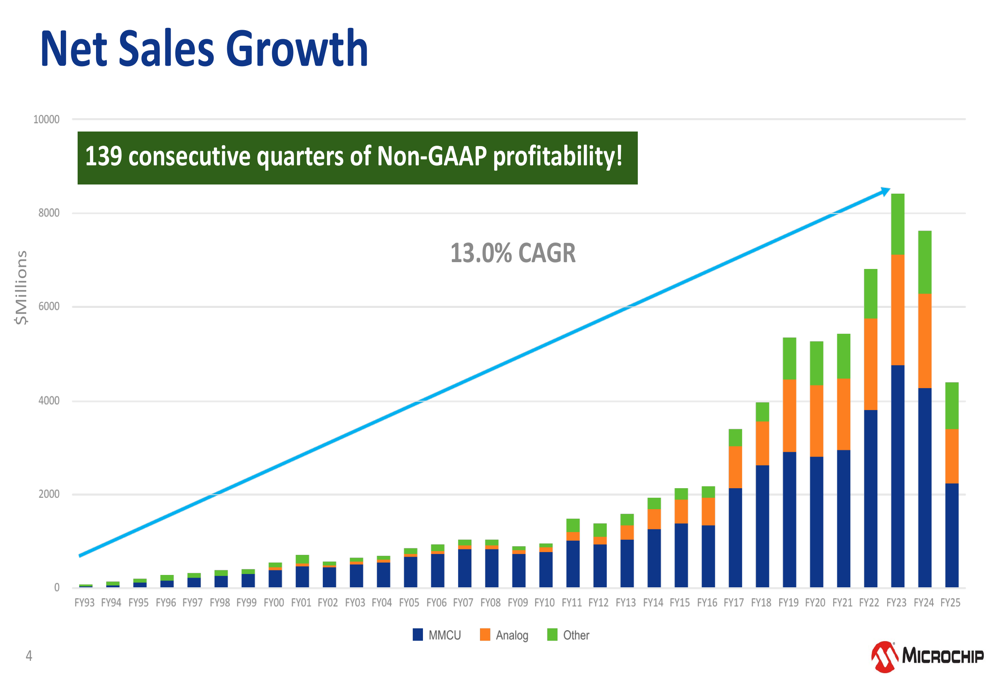

The company has maintained a long-term growth trajectory with a 13.0% CAGR in net sales from fiscal 1993 through fiscal 2025, positioning itself as a leading provider of smart, connected, and secure embedded solutions.

As shown in the following chart of historical net sales growth, Microchip has demonstrated consistent expansion over multiple decades, with particularly accelerated growth beginning around FY15:

Quarterly Performance Highlights

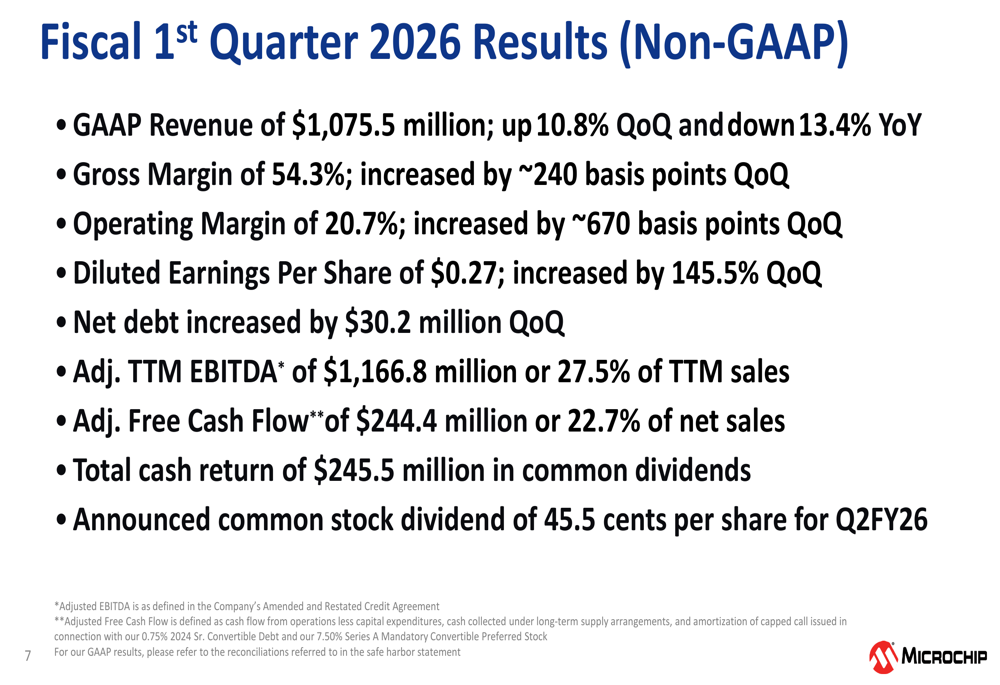

For the first quarter of fiscal 2026, Microchip reported GAAP revenue of $1,075.5 million, representing a 10.8% sequential increase but a 13.4% year-over-year decline. The company achieved significant margin expansion with gross margins reaching 54.3%, an improvement of approximately 240 basis points quarter-over-quarter.

Operating margins showed even more dramatic improvement, climbing to 20.7%, a sequential increase of approximately 670 basis points. This margin expansion helped drive diluted earnings per share to $0.27, a substantial 145.5% increase from the previous quarter.

The following slide details Microchip’s Q1 FY2026 financial performance:

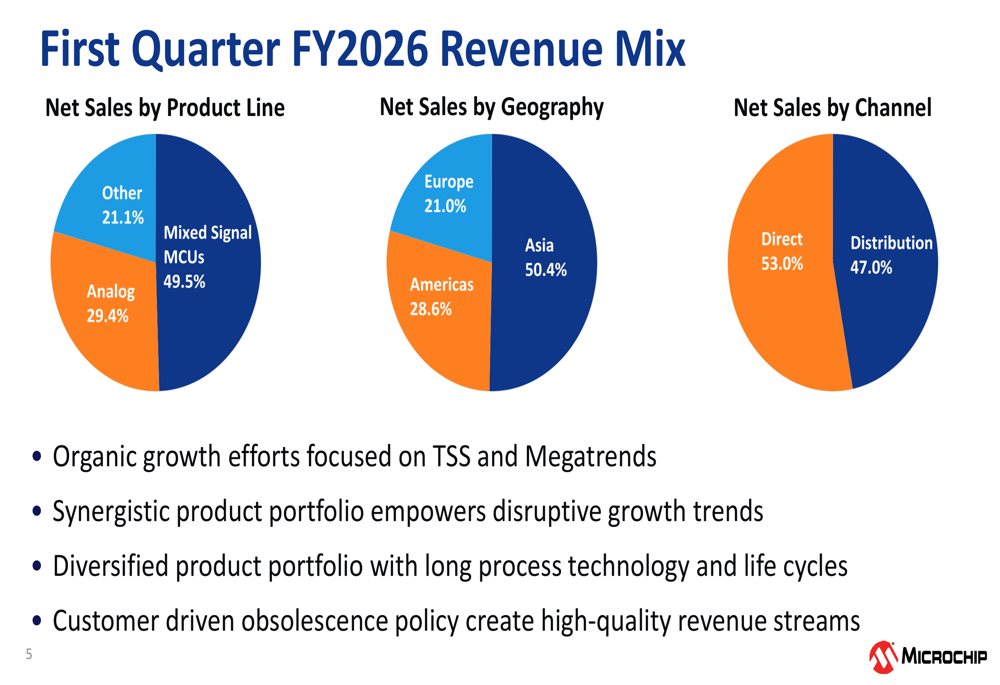

Microchip’s revenue mix for Q1 FY2026 shows a diversified portfolio across product lines, geographies, and sales channels. Mixed Signal MCUs represent nearly half of the company’s revenue at 49.5%, followed by Analog at 29.4%, and Other products at 21.1%. Geographically, Asia continues to be the largest market at 50.4%, with the Americas and Europe contributing 28.6% and 21.0%, respectively.

The company’s revenue distribution is illustrated in the following pie charts:

Strategic Initiatives and Market Focus

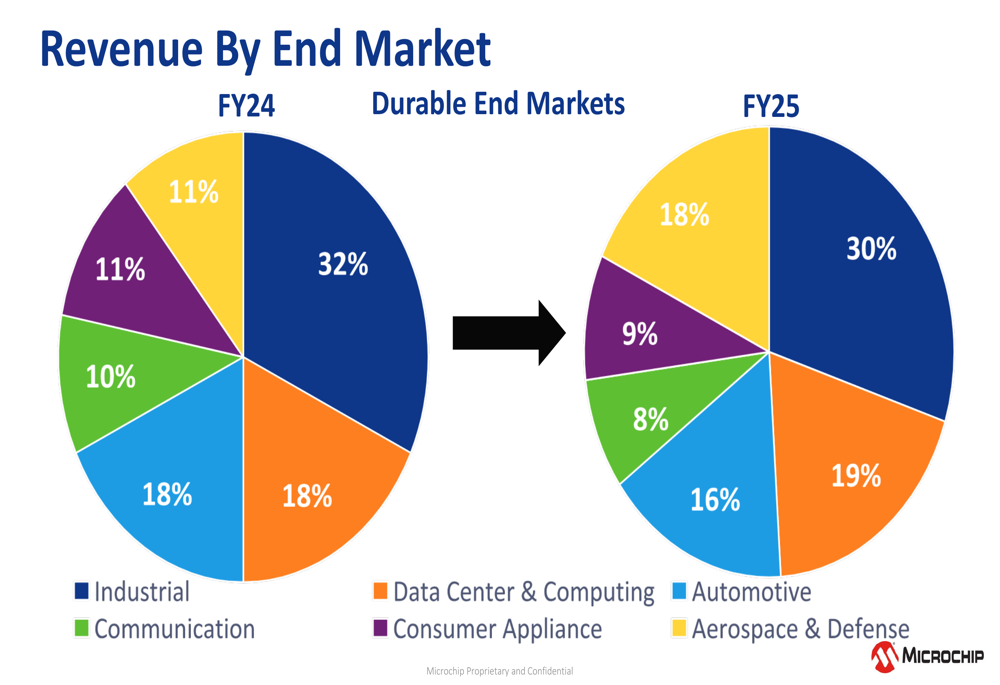

A notable strategic shift in Microchip’s business is the growing importance of the automotive sector. From fiscal 2024 to fiscal 2025, automotive’s contribution to revenue increased from 11% to 18%, representing one of the most significant changes in the company’s end market mix. Meanwhile, the industrial sector remains the largest contributor at 30%, though slightly down from 32% in the previous fiscal year.

The following comparison illustrates this strategic shift in end markets:

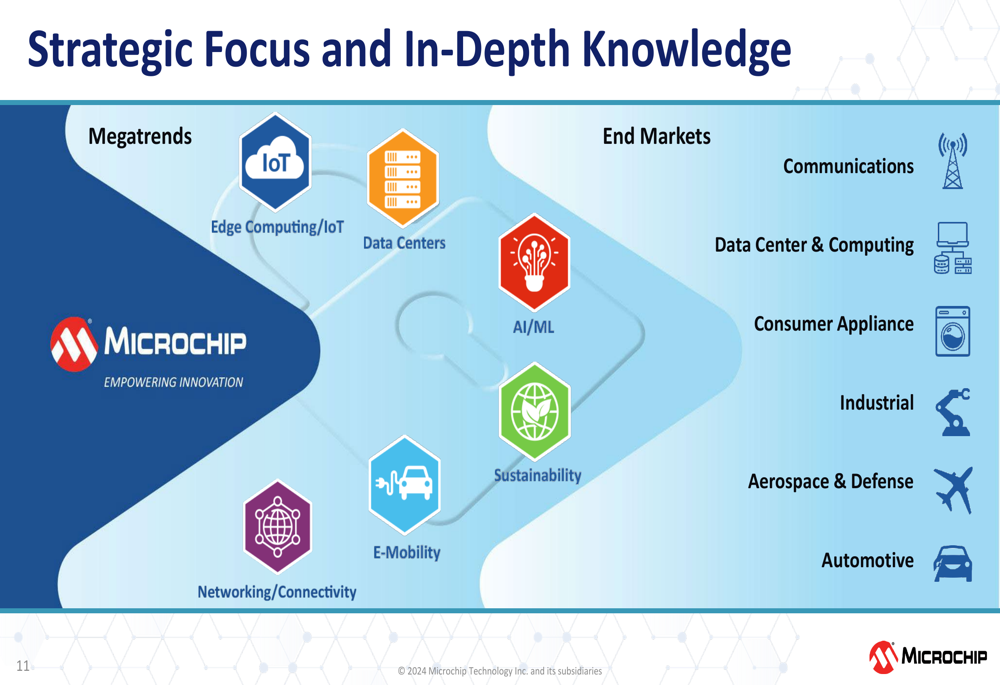

Microchip continues to focus on megatrends including IoT, Edge Computing, Data Centers, AI/ML, E-Mobility, and Networking/Connectivity. The company’s strategic focus spans multiple end markets including Communications, Data Center & Computing, Consumer Appliance, Industrial, Aerospace & Defense, and Automotive.

The company’s strategic focus across megatrends and end markets is visualized here:

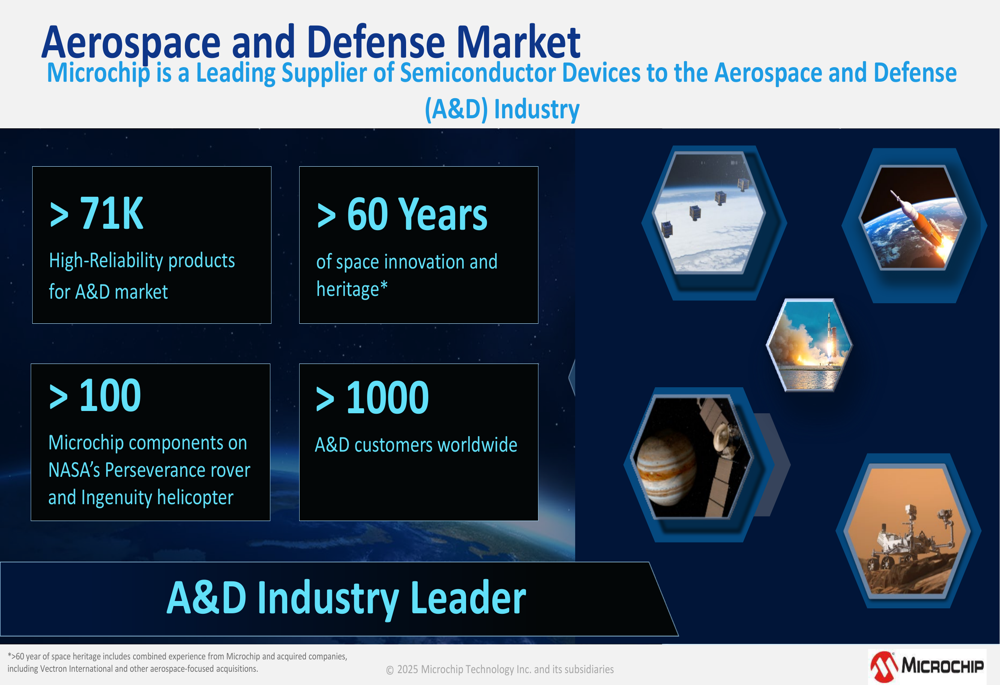

Microchip highlighted its strong position in the Aerospace and Defense (A&D) market, where it offers over 71,000 high-reliability products and serves more than 1,000 A&D customers worldwide. The company emphasized its 60+ years of space innovation heritage, including having more than 100 components on NASA’s Perseverance rover and Ingenuity helicopter.

The following slide showcases Microchip’s leadership in the A&D sector:

Capital Allocation and Shareholder Returns

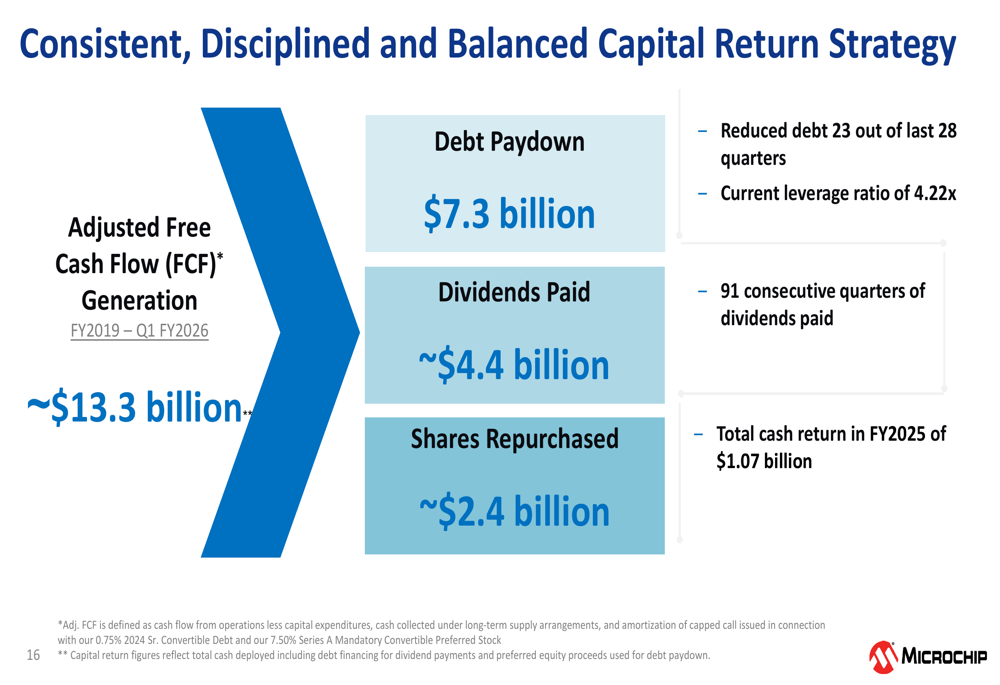

Microchip emphasized its disciplined approach to capital allocation, having generated approximately $13.3 billion in adjusted free cash flow from fiscal 2019 through Q1 fiscal 2026. The company has allocated this cash flow to debt reduction ($7.3 billion), dividend payments ($4.4 billion), and share repurchases ($2.4 billion).

The company has reduced debt in 23 out of the last 28 quarters and maintained a current leverage ratio of 4.22x. Microchip has paid dividends for 91 consecutive quarters, with total cash return to shareholders in fiscal 2025 reaching $1.07 billion.

This balanced capital return strategy is illustrated in the following slide:

Forward-Looking Statements

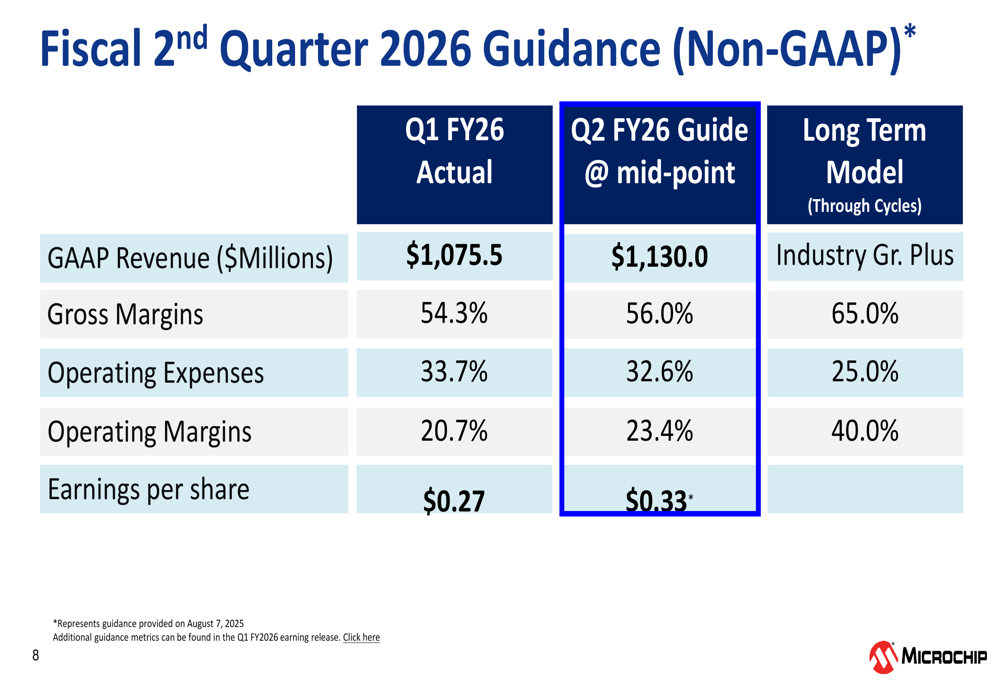

For the second quarter of fiscal 2026, Microchip provided guidance for GAAP revenue of $1,130.0 million, gross margins of 56.0%, operating margins of 23.4%, and earnings per share of $0.33. These projections represented continued sequential improvement in both revenue and profitability.

The company’s long-term model targets industry-leading growth, with gross margins of 65.0%, operating expenses of 25.0%, and operating margins of 40.0%.

The guidance and long-term targets are detailed in the following table:

Actual Q2 Performance vs. Guidance

Microchip’s actual Q2 fiscal 2026 results, released after this presentation, showed that the company exceeded its guidance. Non-GAAP earnings per share came in at $0.35, surpassing the forecasted $0.33 by 6.1%. Revenue reached $1.14 billion, slightly above the guided $1.13 billion, representing a 6% sequential increase from Q1.

The company achieved gross margins of 56.7%, exceeding its guidance of 56.0%. Operational improvements included a significant reduction in inventory, which decreased by $73.8 million, with inventory days dropping from 266 to 199.

Despite these positive results, Microchip’s stock fell by 2.34% to $60.26 in after-hours trading following the earnings announcement, reflecting broader market volatility rather than company-specific concerns. The stock remains below its 52-week high of $77.20, though well above its 52-week low of $34.13.

Looking ahead, Microchip has provided a cautious outlook for Q3 fiscal 2026, with net sales guidance of $1.129 billion (plus or minus $20 million), suggesting a potential slight sequential decline. However, the company anticipates stronger performance in subsequent quarters, driven by reduced inventory write-offs and improved factory utilization as it continues to progress toward its long-term margin targets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.