US stock futures muted as rate cut bets wane ahead of Jackson Hole

Introduction & Market Context

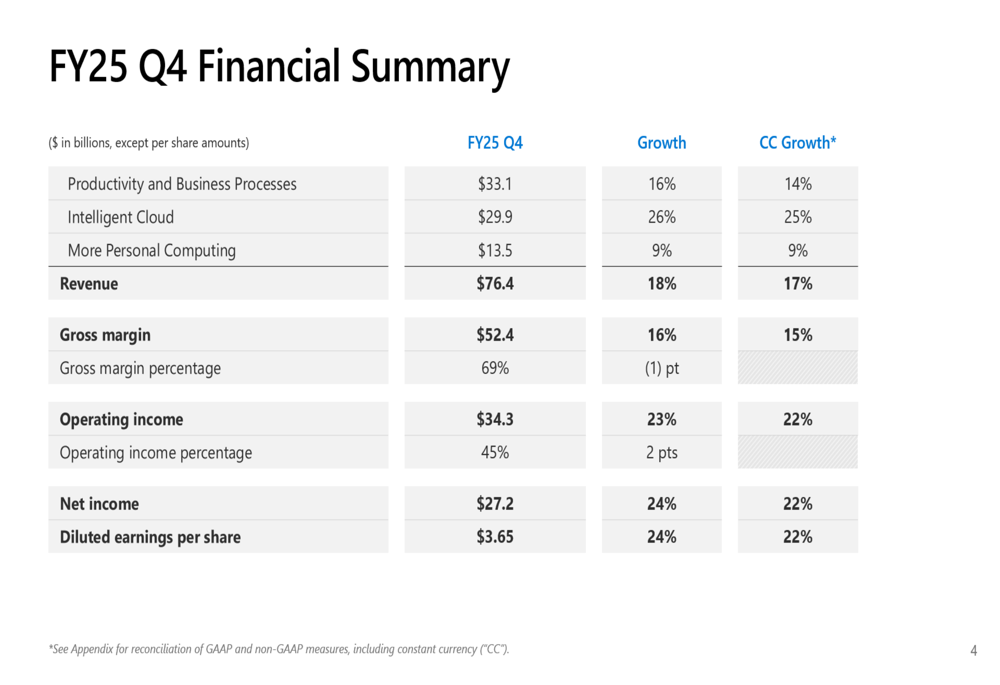

Microsoft Corporation (NASDAQ:MSFT) delivered impressive fourth-quarter fiscal year 2025 results on July 30, 2025, showcasing robust growth across all business segments. The tech giant reported total revenue of $76.4 billion, representing an 18% year-over-year increase (17% in constant currency), significantly outpacing the previous quarter’s performance. The strong results reflect Microsoft’s continued dominance in cloud computing and successful AI integration across its product portfolio.

Following the earnings announcement, Microsoft shares edged up 0.47% in after-hours trading to $515, building on a 0.29% gain during regular trading hours. The stock remains near its 52-week high of $518.29, demonstrating continued investor confidence in the company’s growth trajectory.

Quarterly Performance Highlights

Microsoft reported substantial growth in key financial metrics for Q4 FY25. Operating income reached $34.3 billion, up 23% year-over-year (22% in constant currency), while net income grew 24% to $27.2 billion. Diluted earnings per share increased 24% to $3.65, continuing the strong performance seen in previous quarters.

As shown in the following comprehensive financial summary:

Microsoft Cloud revenue was a particular standout, reaching $46.7 billion with 27% year-over-year growth (25% in constant currency). This represents a significant acceleration from the 20-22% growth rate reported in Q1 FY25, indicating strengthening momentum in Microsoft’s cloud business.

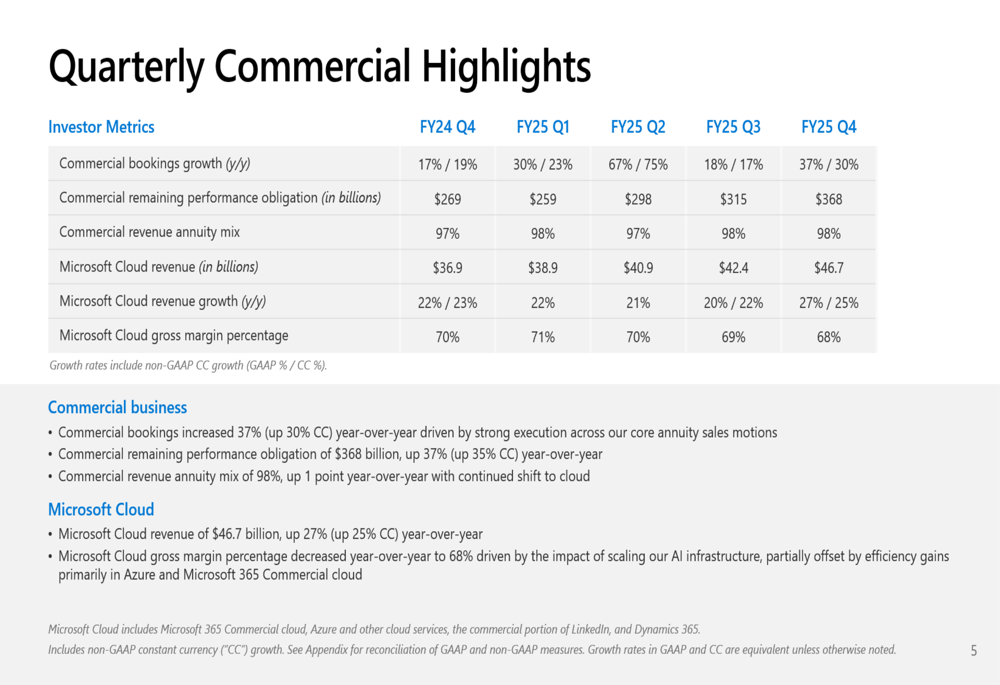

Commercial bookings increased 37% (30% in constant currency), while commercial remaining performance obligation reached $368 billion, up 37% year-over-year. These metrics highlight the robust demand for Microsoft’s enterprise offerings and provide visibility into future revenue streams.

The following chart illustrates the consistent growth in Microsoft’s commercial metrics:

Detailed Financial Analysis by Segment

Productivity and Business Processes

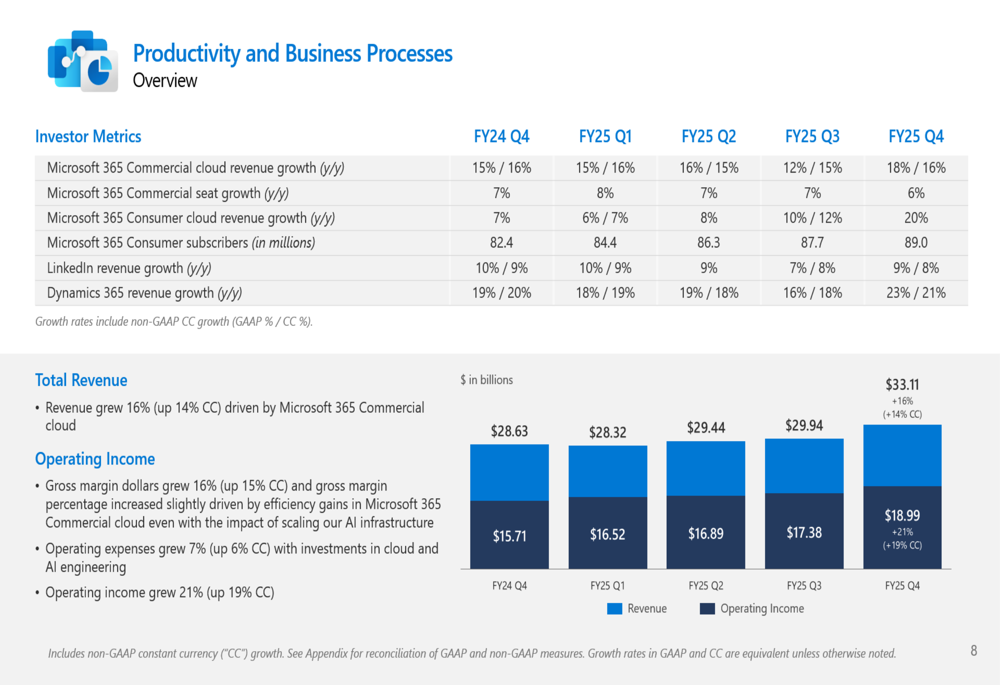

The Productivity and Business Processes segment generated $33.1 billion in revenue, a 16% increase year-over-year (14% in constant currency). Operating income for this segment grew 21% to $19 billion, demonstrating improved operational efficiency.

Microsoft 365 Commercial products and cloud services revenue increased 16% (15% in constant currency), with seat growth of 6%. Microsoft 365 Consumer subscribers reached 89 million, up from 87.7 million in the previous quarter, with revenue growing 21%. LinkedIn continued its steady performance with 9% revenue growth (8% in constant currency).

The following chart details the performance metrics for this segment:

Intelligent Cloud

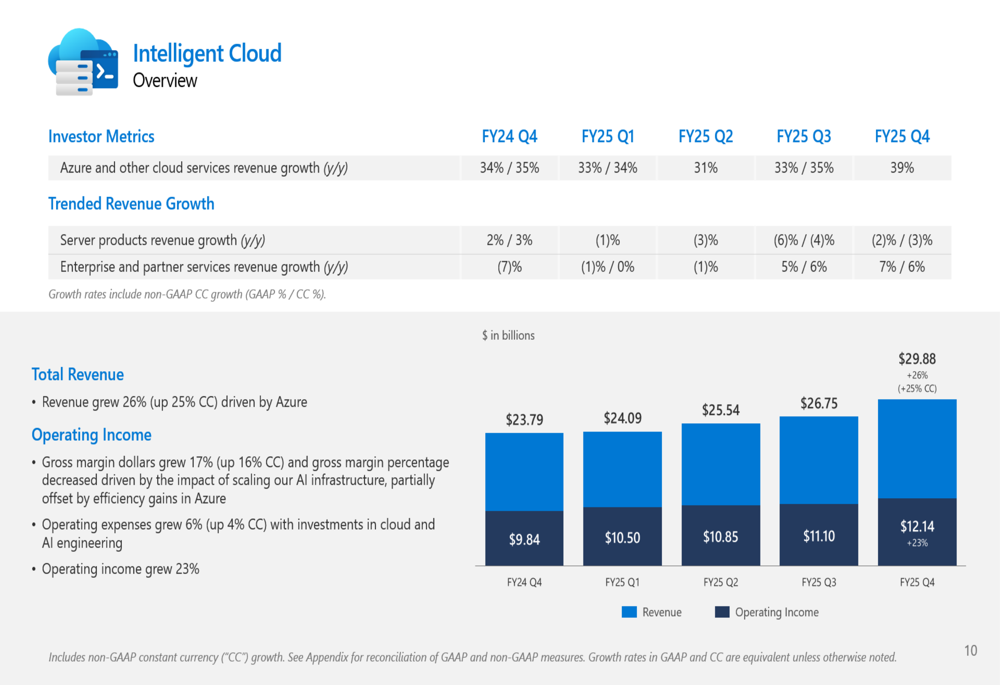

The Intelligent Cloud segment delivered the strongest performance among Microsoft’s business units, with revenue increasing 26% to $29.9 billion (25% in constant currency). Operating income rose 23% to $12.1 billion.

Azure and other cloud services revenue growth accelerated to 39%, a significant improvement from the 33-35% range seen in previous quarters. This acceleration highlights Microsoft’s strengthening position in the cloud infrastructure market and successful execution of its AI integration strategy. Server products revenue declined slightly by 2-3%, reflecting the ongoing shift from on-premises solutions to cloud services.

The following overview illustrates the Intelligent Cloud segment’s performance:

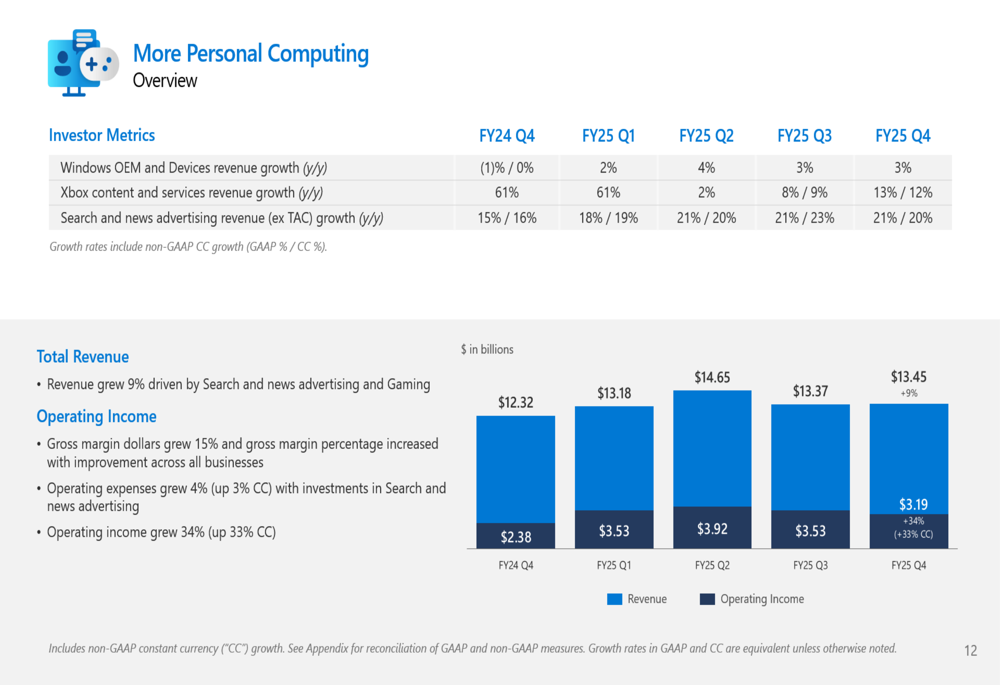

More Personal Computing

The More Personal Computing segment reported revenue of $13.5 billion, up 9% year-over-year. Operating income showed impressive growth of 34% to $3.2 billion, indicating substantial margin improvement in this segment.

Xbox content and services revenue increased 13% (12% in constant currency), showing continued momentum in Microsoft’s gaming business. Search and news advertising revenue excluding traffic acquisition costs grew 21% (20% in constant currency), maintaining the strong performance seen in previous quarters. Windows OEM and Devices revenue increased by a modest 3%.

The segment’s performance is detailed in the following chart:

Strategic Initiatives and Financial Health

Microsoft returned $9.4 billion to shareholders during the quarter, including $6.2 billion in dividends and $3.2 billion in share repurchases. The company’s effective tax rate for the quarter was 17%.

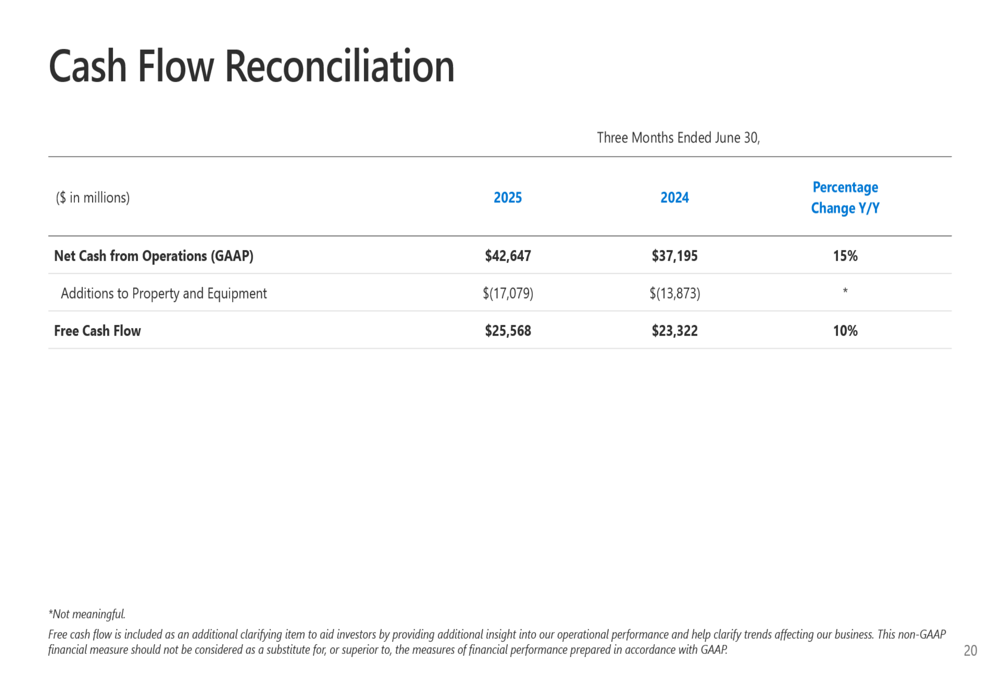

Capital expenditures reached $24.2 billion, up 27% year-over-year, reflecting Microsoft’s continued investment in cloud infrastructure and AI capabilities. Despite these significant investments, the company generated $42.6 billion in cash flow from operations (up 15%) and $25.6 billion in free cash flow (up 10%), demonstrating Microsoft’s ability to fund growth initiatives while maintaining strong cash generation.

The following reconciliation provides insight into Microsoft’s cash flow performance:

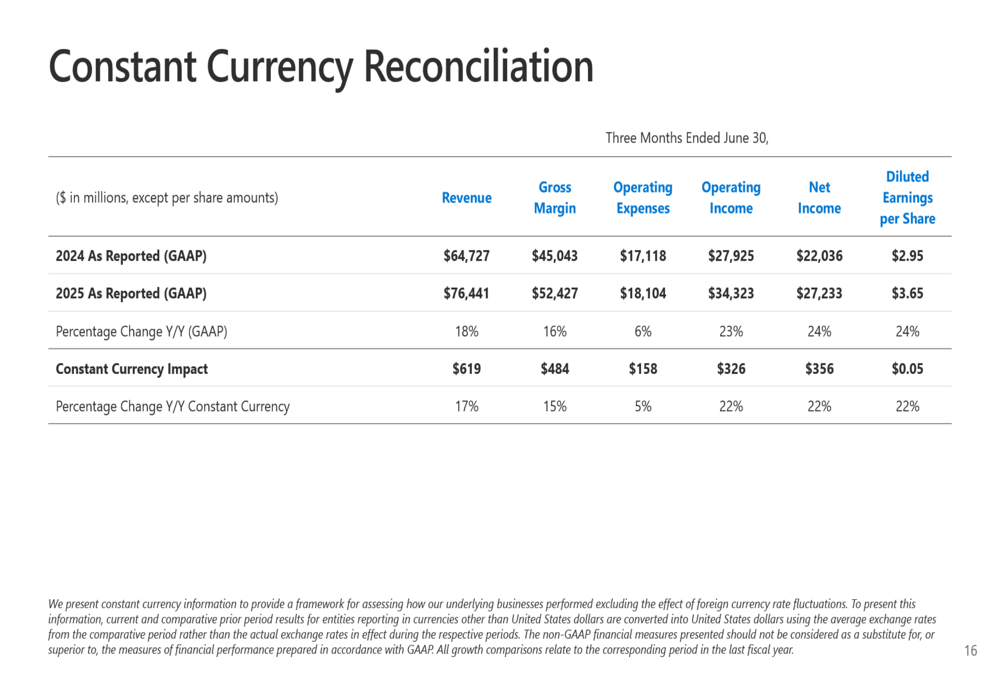

Microsoft’s constant currency reconciliation across segments shows the company’s ability to deliver strong growth despite currency fluctuations:

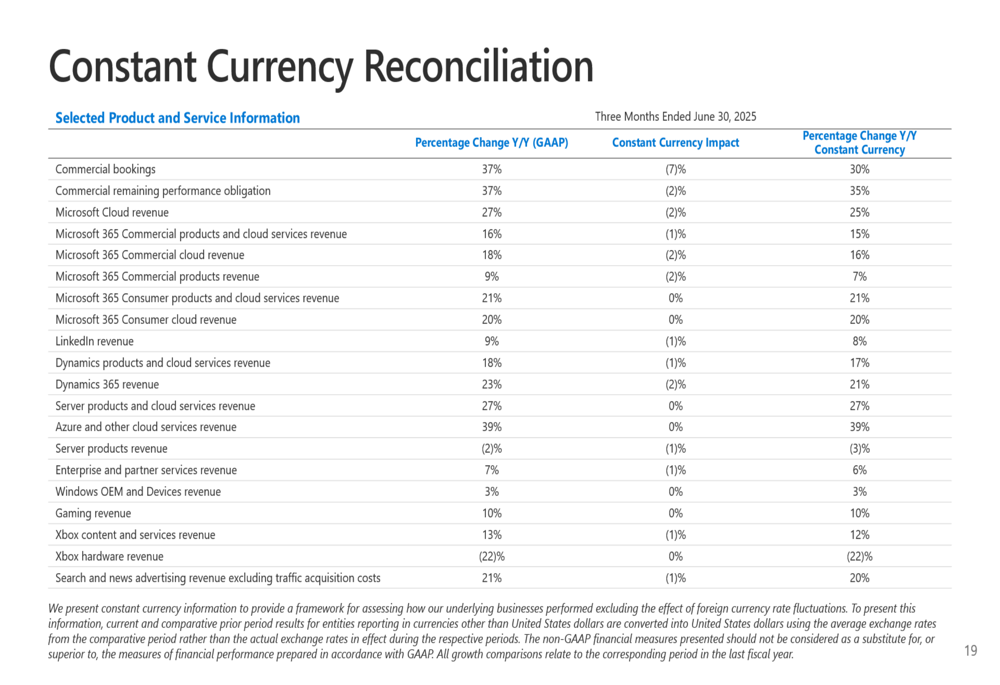

The detailed product and service performance metrics further highlight Microsoft’s strength across its diverse portfolio:

Market Reaction and Outlook

Microsoft’s Q4 FY25 results continue the momentum seen in previous quarters, with cloud and AI services driving significant growth. The acceleration in Azure revenue growth to 39% is particularly noteworthy, as it indicates Microsoft’s strengthening competitive position in the cloud infrastructure market.

The company’s substantial investments in capital expenditures signal confidence in future demand for cloud and AI services. With commercial remaining performance obligation reaching $368 billion, Microsoft has considerable visibility into future revenue streams, providing a solid foundation for continued growth.

While Microsoft faces challenges, including increased competition in the cloud space and potential macroeconomic headwinds, the company’s diversified business model and strong execution position it well to navigate these challenges. The consistent performance across all business segments demonstrates Microsoft’s ability to drive growth through innovation and strategic investments in high-growth areas like cloud computing and artificial intelligence.

As Microsoft continues to integrate AI capabilities across its product portfolio and expand its cloud infrastructure, the company appears well-positioned to maintain its growth trajectory in fiscal year 2026.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.