TSX runs higher on rate cut expectations

Introduction & Market Context

Mistras Group Inc (NYSE:MG) presented its second quarter 2025 earnings results on August 7, 2025, revealing significant improvements in profitability metrics despite a slight revenue decline. The asset protection and testing services provider saw its stock climb 7.4% in regular trading to $8.56, with an additional 4.89% gain in pre-market trading, signaling positive investor reception following a challenging first quarter.

The company’s Q2 performance marks a substantial recovery from its disappointing Q1 2025 results, when it reported a net loss of $0.01 per share and missed revenue expectations by a significant margin. This turnaround suggests Mistras’s strategic initiatives and diversification efforts are beginning to yield results.

Quarterly Performance Highlights

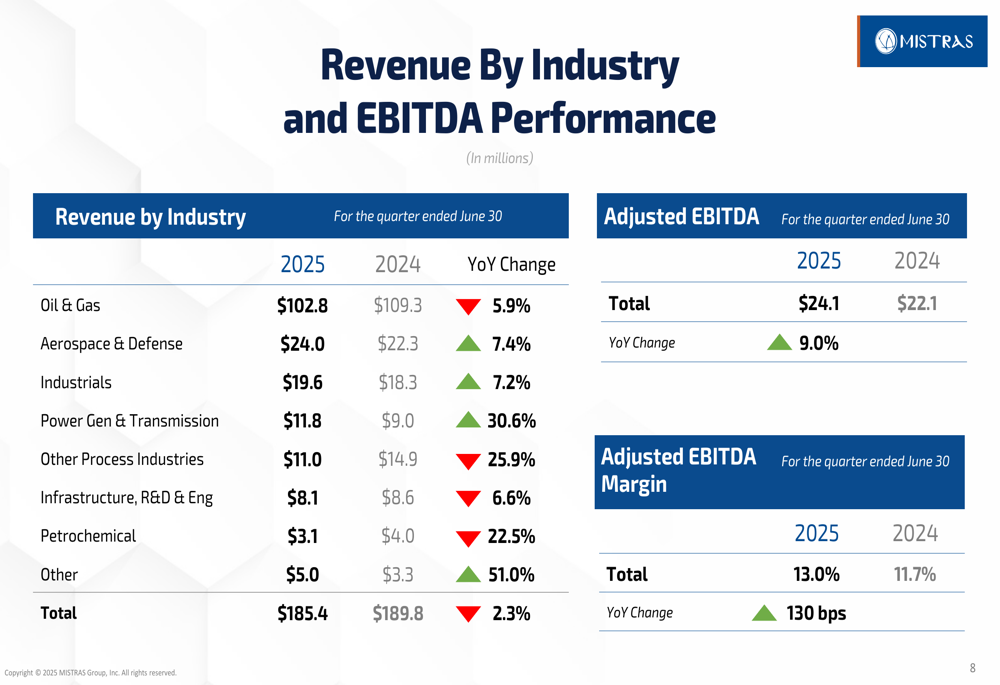

Mistras reported Q2 2025 revenue of $185.4 million, representing a modest 2.3% decrease from $189.8 million in the same period last year. However, the company achieved notable improvements in profitability metrics, with Adjusted EBITDA increasing 9.0% to $24.1 million and Adjusted EBITDA margin expanding by 130 basis points to 13.0%.

As shown in the following comprehensive revenue breakdown by industry segment:

While traditional Oil & Gas revenue declined by 5.9% to $102.8 million, several growth sectors demonstrated strong performance. Power Generation (HM:PGV) & Transmission showed the most impressive growth at 30.6%, while Aerospace & Defense and Industrials grew by 7.4% and 7.2% respectively. These results validate the company’s diversification strategy away from its traditional oil and gas focus.

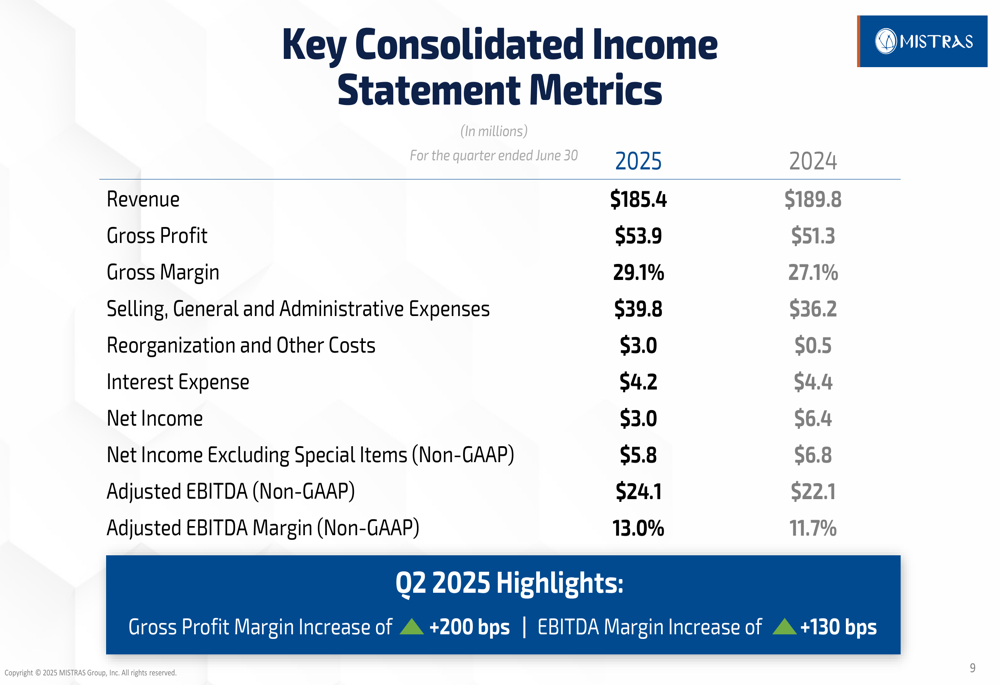

The company’s consolidated income statement reveals significant margin improvements despite the revenue decline:

Gross profit increased to $53.9 million from $51.3 million in Q2 2024, with gross margin expanding by 200 basis points to 29.1%. However, net income decreased to $3.0 million from $6.4 million in the prior year, primarily due to higher selling, general and administrative expenses and increased reorganization costs.

Strategic Initiatives

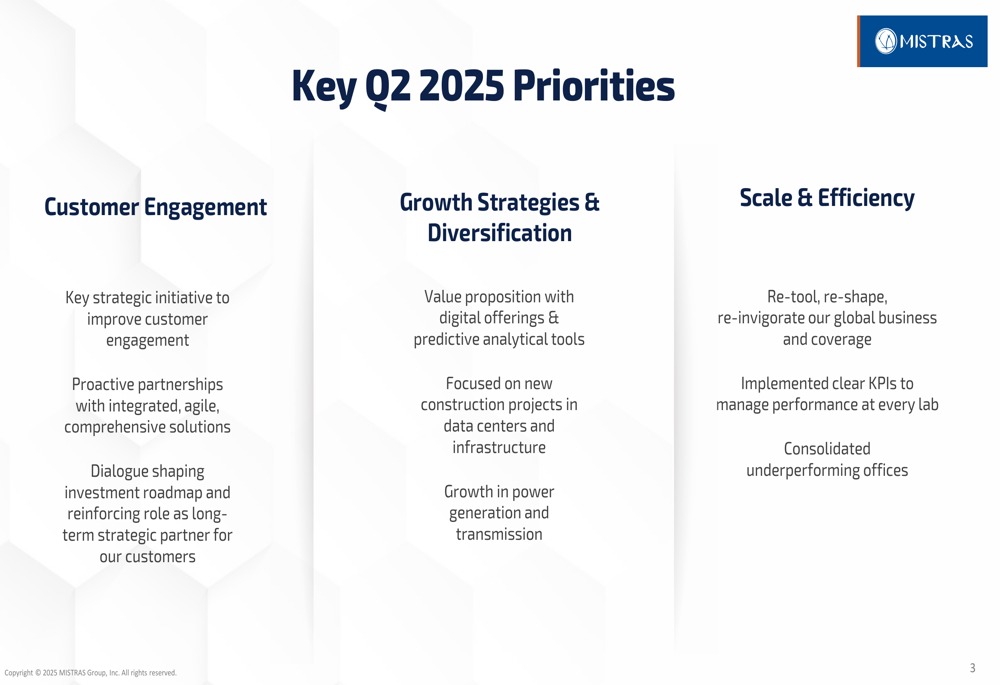

Mistras outlined three key strategic priorities for Q2 2025, focusing on customer engagement, growth strategies, and operational efficiency:

The company is actively diversifying its end markets to reduce dependency on oil and gas, targeting high-margin projects in data centers, infrastructure, power generation, and re-shoring manufacturing:

A significant component of Mistras’s strategy involves leveraging data analytics and digital solutions to create higher-value offerings. The company is developing data-driven asset protection solutions through Digital Twins, which provide predictive maintenance capabilities and enhance customer value:

The company is also strengthening its position in the aerospace and defense sector through an integrated testing platform. This initiative involves centralizing manufacturing capabilities and developing long-term partnerships with major industry players:

Detailed Financial Analysis

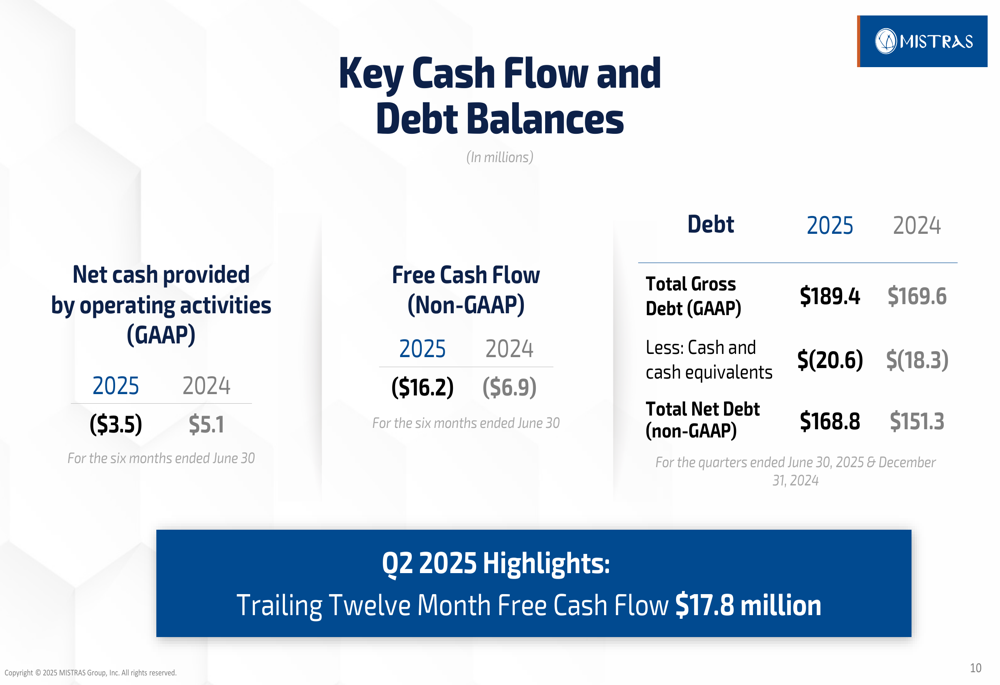

Despite improved operational performance, Mistras faces challenges with cash flow and debt management. The company reported negative free cash flow of $16.2 million for the six months ended June 30, 2025, compared to negative $6.9 million in the same period last year:

Total (EPA:TTEF) net debt increased to $168.8 million from $151.3 million in 2024. However, the company highlighted a trailing twelve-month free cash flow of $17.8 million, suggesting potential improvement in the second half of the year.

Selling, general and administrative expenses increased to $39.8 million from $36.2 million in Q2 2024, and reorganization costs rose to $3.0 million from $0.5 million, reflecting ongoing efforts to restructure operations and consolidate underperforming offices.

Forward-Looking Statements

Mistras’s strategic outlook positions the company as a leader in asset protection and testing, with a focus on four key areas:

The company’s emphasis on data solutions and digital offerings aligns with industry trends toward predictive maintenance and condition-based monitoring. By diversifying its end markets and focusing on high-margin segments, Mistras aims to reduce its traditional dependence on oil and gas while capitalizing on growth opportunities in aerospace, power generation, and infrastructure.

The significant improvement from Q1 2025’s disappointing results suggests the company’s strategic initiatives are gaining traction. The positive stock movement indicates investor confidence in Mistras’s ability to continue its margin expansion and strategic transformation, despite ongoing challenges in certain market segments.

While cash flow and debt metrics present concerns, the improved profitability and operational efficiency demonstrated in Q2 2025 provide a foundation for potential financial strengthening in future quarters. The company’s focus on consolidating underperforming offices and implementing key performance indicators across its global operations should continue to support margin improvement initiatives.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.