TSX drop after Canadian index edges higher in prior session

Introduction & Market Context

Mitek Systems , Inc. (NASDAQ:MITK) released its Q3 FY2025 financial results on August 7, 2025, highlighting continued progress in its strategic shift toward SaaS-based offerings and identity verification solutions. The company, which specializes in digital identity verification and mobile deposit technologies, operates in a substantial $47 billion total addressable market spanning identity verification, biometrics, and check deposit/fraud prevention.

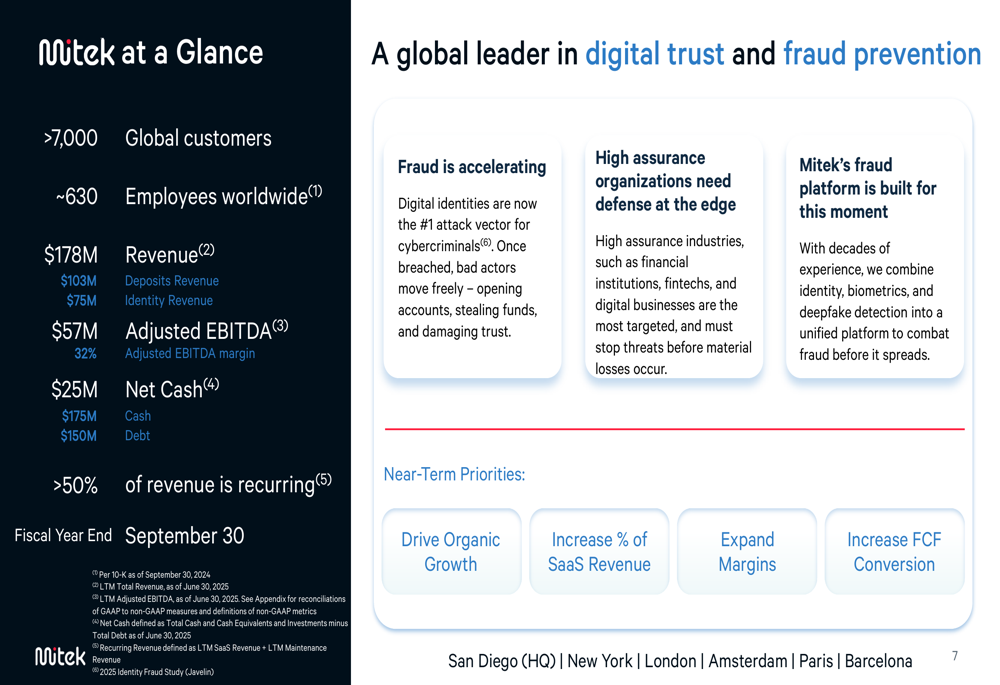

As shown in the following snapshot of Mitek’s business fundamentals:

Mitek serves over 7,000 global customers with approximately 630 employees worldwide. The company’s revenue mix is split between Deposits ($103M) and Identity ($75M), with an adjusted EBITDA of $57M representing a 32% margin. With $175M in cash against $150M in debt, Mitek has achieved a net cash position of $25M, a significant improvement from its debt position a year ago.

Quarterly Performance Highlights

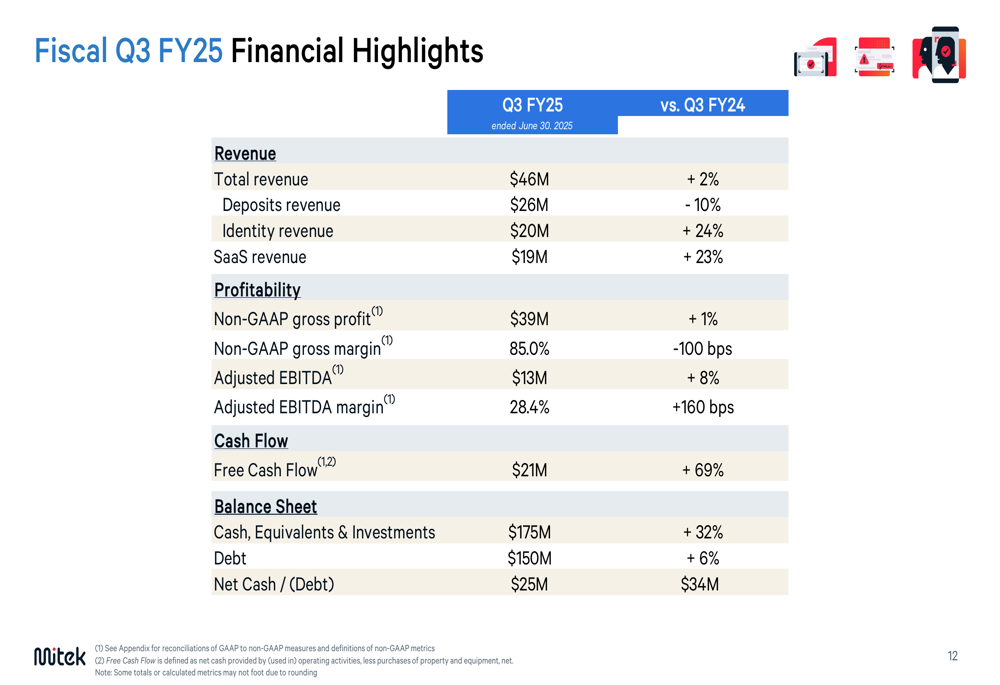

Mitek reported Q3 FY25 total revenue of $46 million, representing a modest 2% year-over-year increase. However, this headline figure masks significant divergence between business segments, with Identity revenue surging 24% while Deposits revenue declined 10%. The company’s strategic focus on SaaS offerings continues to gain traction, with SaaS revenue growing 23% year-over-year to $19 million, now constituting 41% of last twelve months (LTM) revenue.

The following chart details Mitek’s Q3 FY25 financial performance:

Despite the modest overall revenue growth, Mitek demonstrated improved profitability with adjusted EBITDA of $13 million, up 8% year-over-year, representing a margin of 28.4% (an improvement of 160 basis points). Free cash flow showed remarkable growth, increasing 69% to $21 million. The company maintained strong gross margins at 85%, though this represented a slight 100 basis point contraction from the previous year.

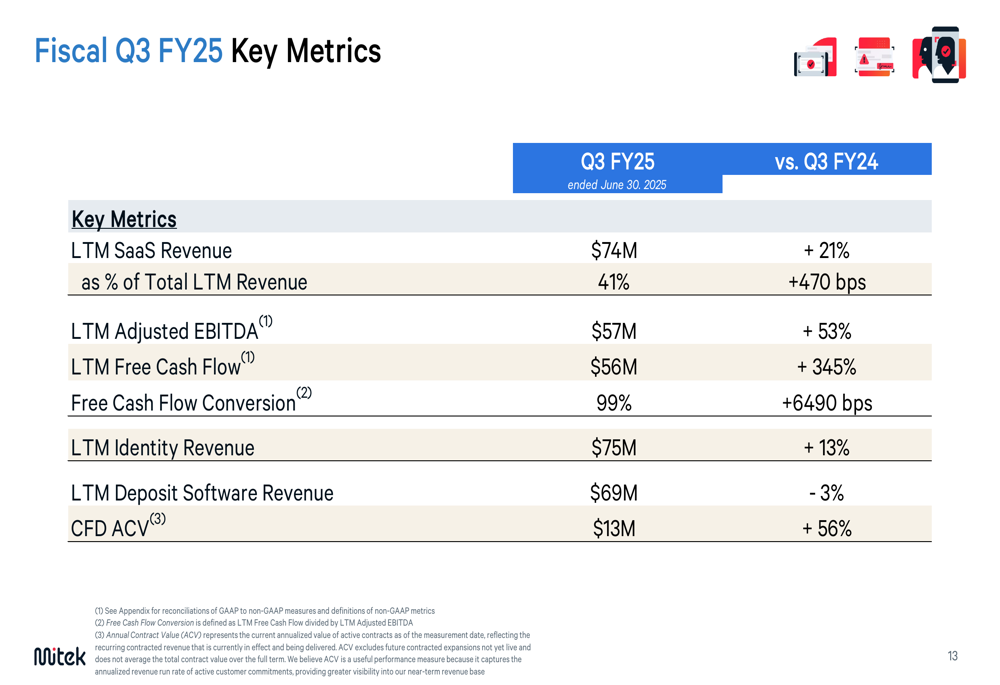

Additional key performance metrics show promising trends across Mitek’s business:

The LTM SaaS revenue reached $74 million, growing 21% year-over-year and now representing 41% of total LTM revenue (up 470 basis points). The company’s Check Fraud Defender (CFD) solution showed particularly strong momentum with annual contract value (ACV) of $13 million, up 56% year-over-year.

Segment Analysis: Identity Growth Offsetting Deposits Decline

Mitek’s performance continues to be characterized by the diverging trajectories of its two core business segments. The Identity segment, which includes verification, authentication, and synthetic fraud detection solutions, posted impressive 24% year-over-year growth to $20 million in Q3 FY25.

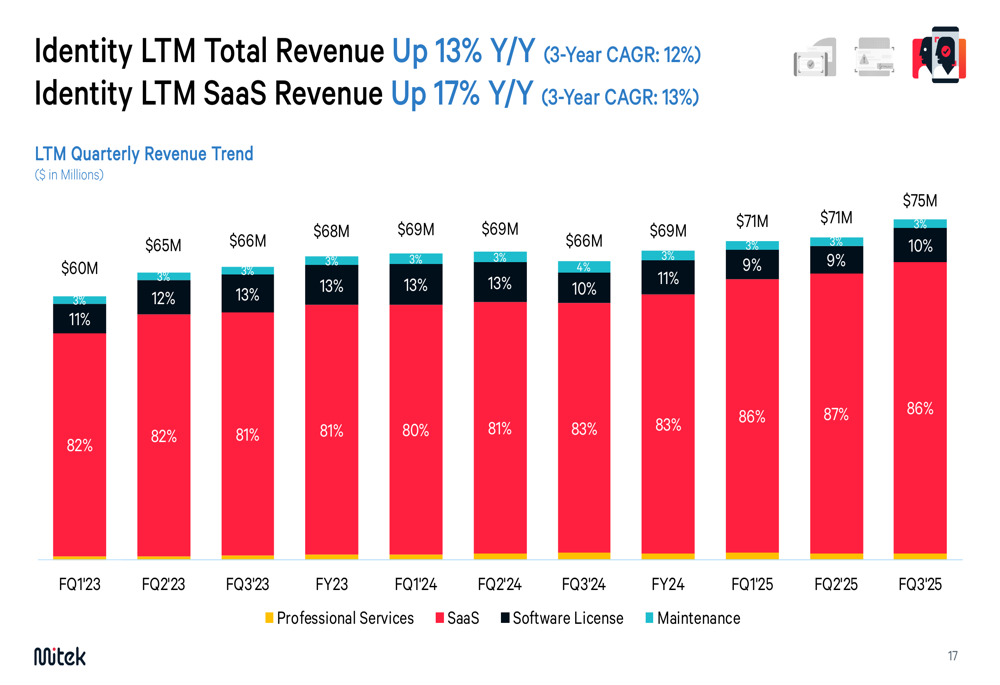

The following chart illustrates the Identity segment’s revenue trend:

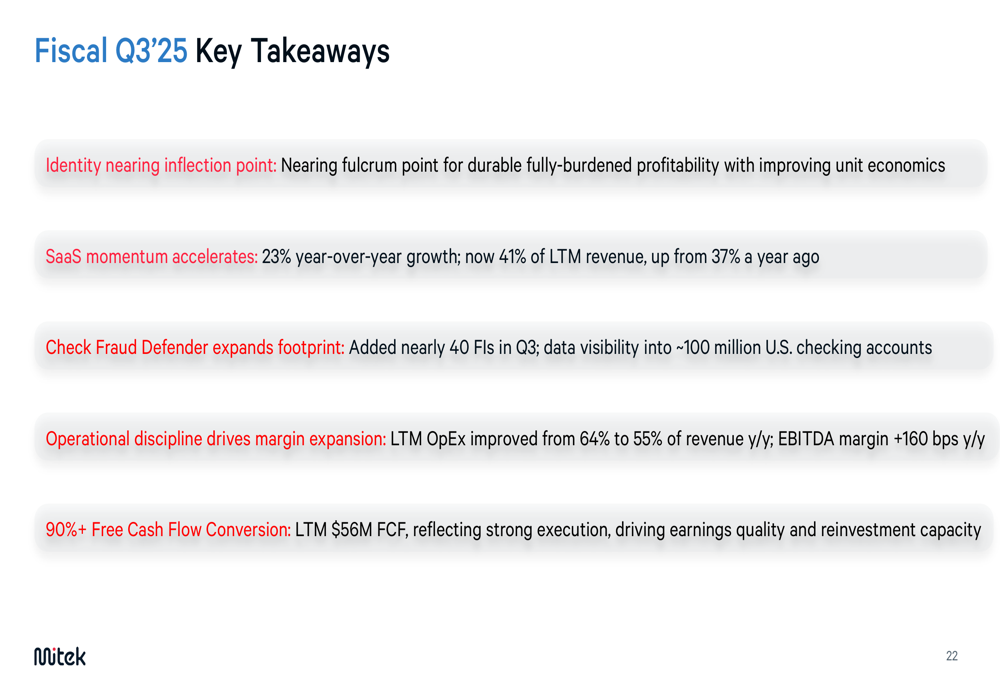

Identity LTM revenue reached $75 million, growing at 13% year-over-year with a three-year CAGR of 12%. Notably, SaaS revenue now constitutes 86% of the Identity segment, positioning it well for recurring revenue growth. The Identity business is approaching what management described as "the fulcrum point for durable fully-burdened profitability with improving unit economics."

In contrast, the Deposits segment, which includes Mobile Check Deposit and Check Fraud Prevention solutions, experienced a 10% year-over-year decline to $26 million in Q3 FY25. However, the segment is showing promising signs in its transition toward SaaS-based offerings, with Deposits LTM SaaS revenue growing 56% year-over-year.

Operational Efficiency & Cash Flow Improvements

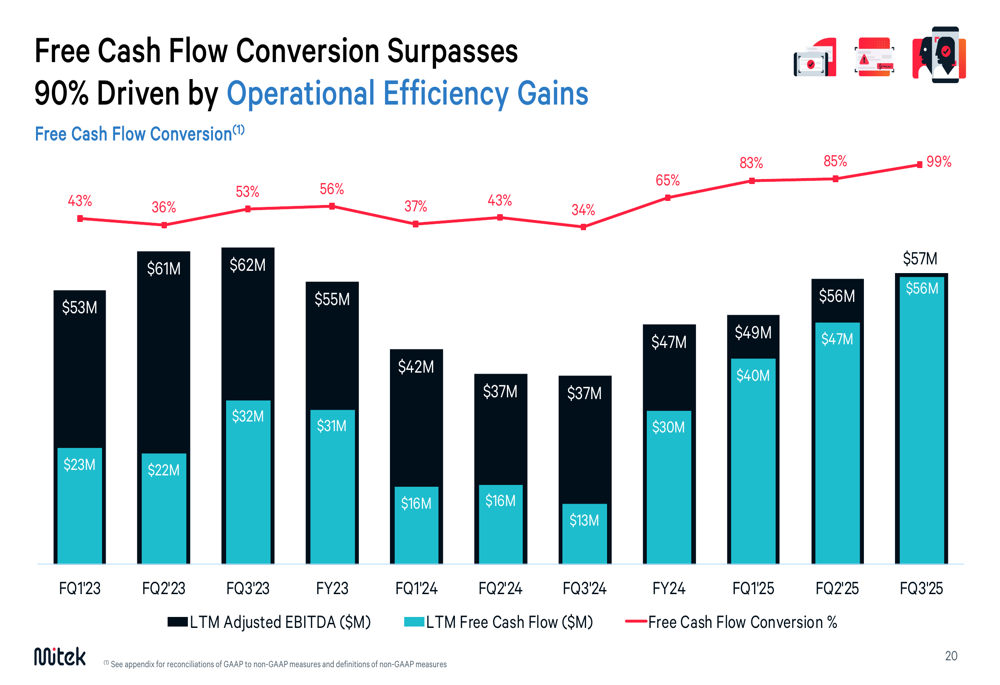

One of the most impressive aspects of Mitek’s Q3 FY25 performance was the dramatic improvement in operational efficiency and cash flow generation. The company has significantly enhanced its free cash flow conversion, which measures the percentage of adjusted EBITDA converted to free cash flow.

As illustrated in the following chart, this metric has improved dramatically:

Free cash flow conversion reached 99% in Q3 FY25, compared to just 34% in Q3 FY24, representing a remarkable improvement of 6,490 basis points. This transformation reflects Mitek’s focus on operational discipline, with LTM operating expenses improving from 64% to 55% of revenue year-over-year.

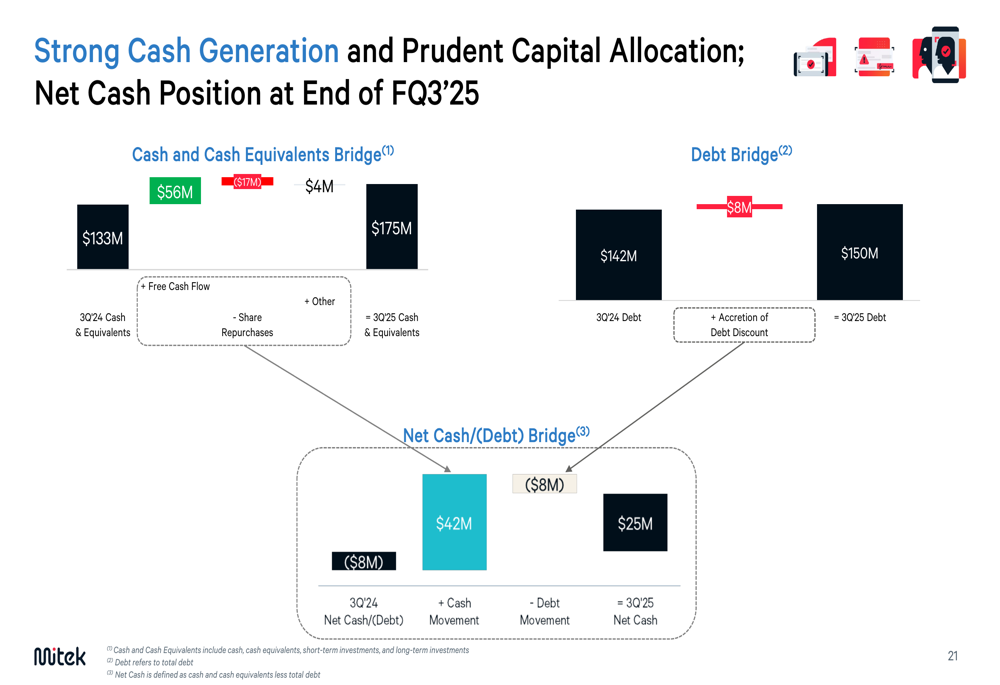

The company’s improved cash generation has strengthened its balance sheet, resulting in a shift from a net debt position to a net cash position:

Cash and cash equivalents increased from $133 million in Q3 FY24 to $175 million in Q3 FY25, while debt increased modestly from $142 million to $150 million. This resulted in a net cash position of $25 million, compared to a net debt position of $8 million a year earlier.

Financial Outlook & Guidance

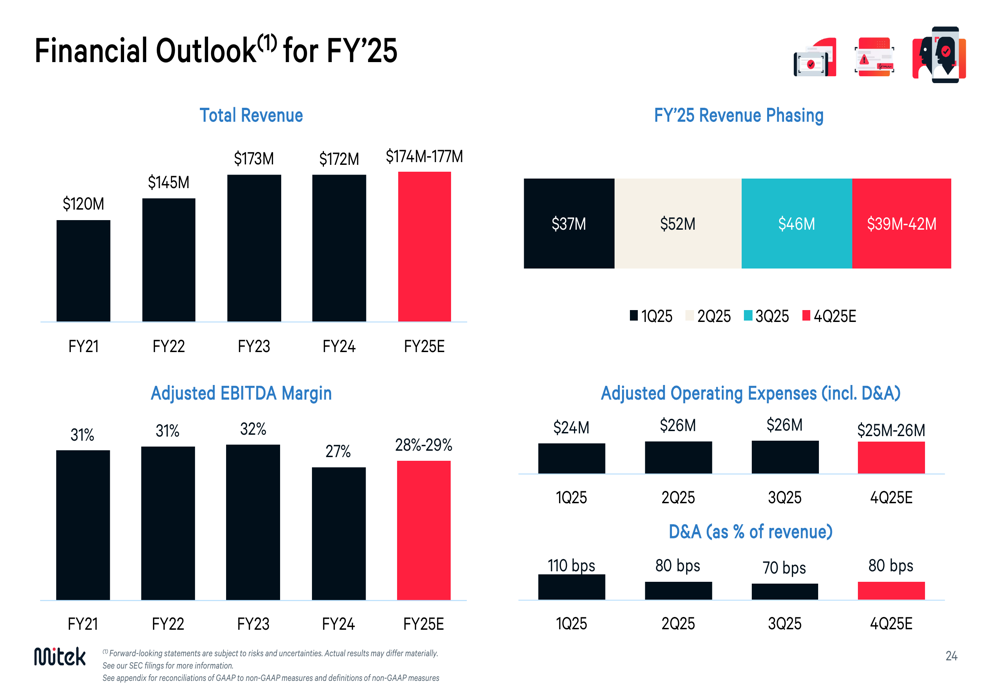

Looking ahead, Mitek provided financial guidance for the full fiscal year 2025:

The company expects total revenue of $174-177 million for FY25, with quarterly phasing of $37 million in Q1, $52 million in Q2, $46 million in Q3, and $39-42 million projected for Q4. Adjusted EBITDA margin is expected to be 28-29% for the full year.

This guidance suggests Q4 revenue will be lower than Q3, potentially indicating some seasonality or conservatism in the company’s projections. The adjusted operating expenses (including D&A) are expected to be $25-26 million in Q4, consistent with Q3 levels.

Strategic Initiatives

Mitek highlighted several key strategic initiatives and takeaways from the quarter:

The company emphasized that its Identity business is nearing an inflection point for "durable fully-burdened profitability with improving unit economics." SaaS momentum continues to accelerate, now representing 41% of LTM revenue, up from 37% a year ago.

Check Fraud Defender is expanding its footprint, with nearly 40 financial institutions added in Q3, providing data visibility into approximately 100 million U.S. checking accounts. This expansion strengthens Mitek’s position in the check fraud prevention market, which remains a significant concern for financial institutions despite the broader digital transformation in banking.

Operational discipline has driven margin expansion, with LTM operating expenses improving from 64% to 55% of revenue year-over-year, contributing to the 160 basis point improvement in EBITDA margin. The resulting free cash flow conversion exceeding 90% provides Mitek with substantial reinvestment capacity to fuel future growth.

Mitek’s strategic focus on combating evolving digital fraud through its comprehensive platform positions the company well in an environment where AI-powered threats continue to proliferate. As digital transactions become increasingly prevalent, the company’s solutions addressing identity verification, mobile deposit, and fraud prevention address critical market needs.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.