Dubai Holding and Palantir create joint venture Aither for AI transformation

Moderna Inc (NASDAQ:MRNA) presented its second quarter 2025 financial results on August 1, revealing a significant revenue decline while highlighting recent FDA approvals and progress in its diversified pipeline. Despite the challenging financial performance, the company’s stock surged 12.06% following the presentation, reflecting investor confidence in Moderna’s strategic direction and cost-cutting initiatives.

Introduction & Market Context

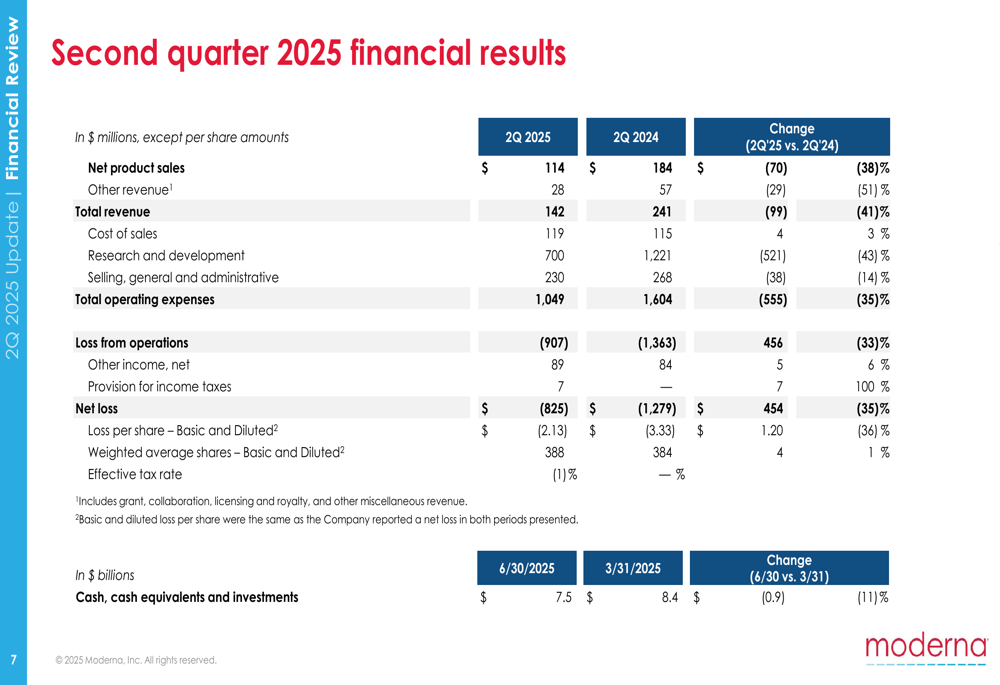

Moderna reported Q2 2025 revenue of $142 million, a 41% decrease from the $241 million recorded in the same period last year. The decline primarily reflects reduced demand for COVID-19 vaccines, which have been the company’s main revenue driver since the pandemic. Despite this setback, Moderna maintained a strong cash position of $7.5 billion, down 11% from $8.4 billion at the end of Q1 2025.

The company’s stock performance, which has traded between $23.15 and $56.70 over the past 52 weeks, suggests investors are focusing more on Moderna’s pipeline progress and cost-reduction efforts than on current revenue challenges.

Quarterly Performance Highlights

Moderna’s Q2 2025 financial results show a company in transition, with significant revenue declines offset by aggressive cost-cutting measures. Net product sales fell 38% year-over-year to $114 million, while other revenue decreased 51% to $28 million.

As shown in the following comprehensive financial table:

The company reported a net loss of $0.8 billion for the quarter. However, Moderna has made substantial progress in reducing its operating expenses, which decreased by 35% ($555 million) compared to Q2 2024. Research and development expenses saw the most significant reduction, falling 43% to $700 million, while selling, general, and administrative expenses decreased 14% to $230 million.

Pipeline and Product Approvals

A key highlight of Moderna’s presentation was the recent FDA approvals for three products, expanding the company’s commercial portfolio beyond its original COVID-19 vaccine:

1. MNEXSPIKE (COVID-19 vaccine) for adults 65 and older, and high-risk individuals aged 12-64

2. MRESVIA (RSV Vaccine) with expanded approval to high-risk individuals aged 18-59

3. Spikevax (COVID-19 Vaccine) with expanded approval to high-risk children aged 6 months to 11 years

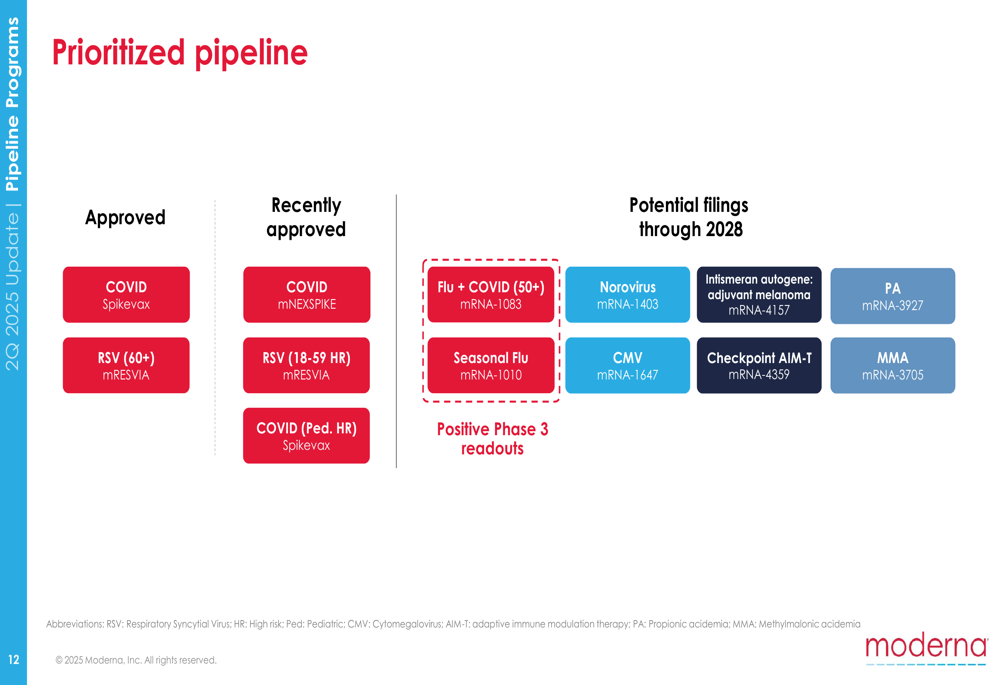

The company’s prioritized pipeline shows a strategic shift toward a more diversified portfolio of vaccines and therapeutics, as illustrated in this comprehensive pipeline overview:

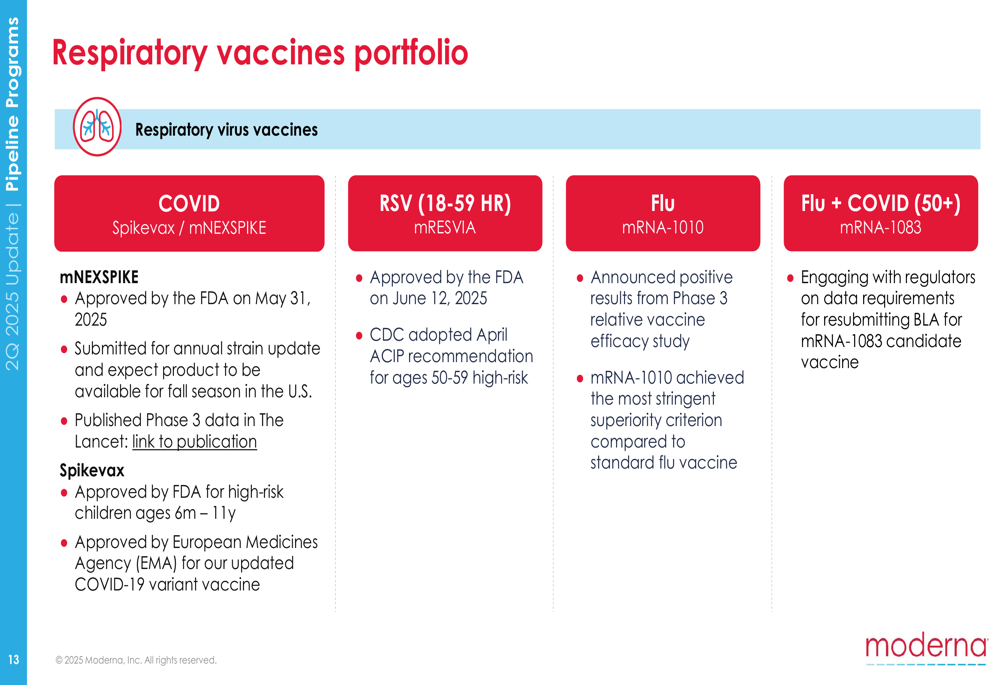

Moderna also announced positive Phase 3 data for its flu vaccine (mRNA-1010), demonstrating superior relative vaccine efficacy of 26.6% compared to a licensed standard-dose seasonal influenza vaccine in adults aged 50 years and older. This represents a significant milestone in the company’s efforts to expand beyond COVID-19 vaccines.

The respiratory vaccines portfolio, which includes COVID, RSV, flu, and combination vaccines, remains a core focus:

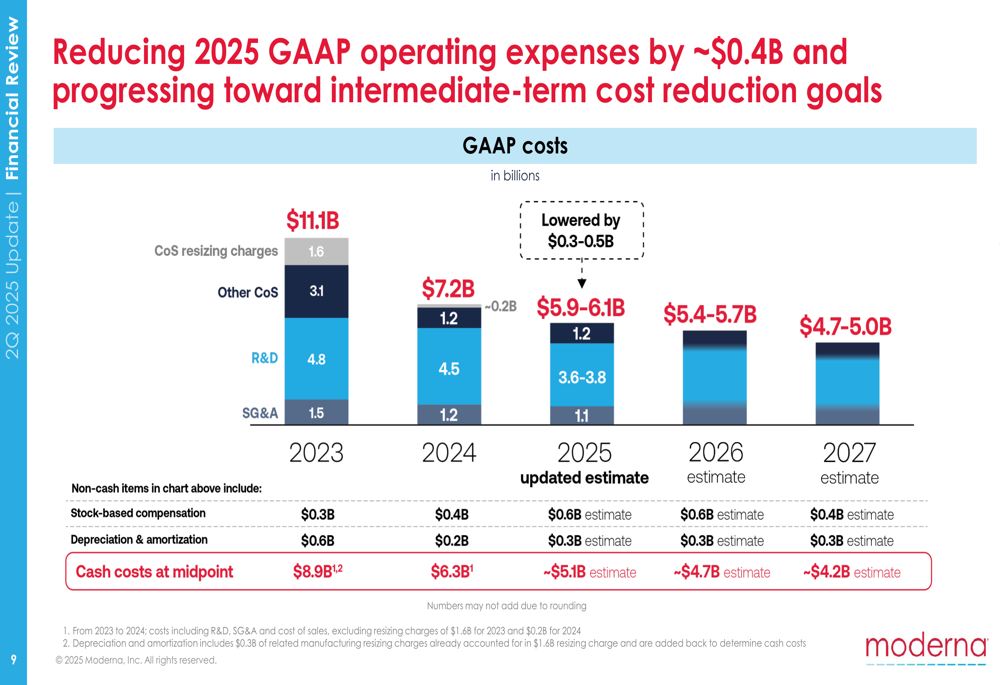

Cost Reduction Strategy

Moderna has implemented an aggressive cost-cutting strategy to adapt to the post-pandemic market environment. The company aims to reduce GAAP operating expenses from $11.1 billion in 2023 to between $4.7-5.0 billion by 2027, with the ultimate goal of achieving cash breakeven in 2028.

The following chart illustrates Moderna’s progress and targets for cost reduction:

The primary drivers for these cost reductions include the completion of Phase 3 clinical trials, manufacturing efficiencies, procurement savings, and workforce restructuring. Moderna has already achieved a fourth consecutive quarter of double-digit year-over-year declines in combined R&D and SG&A expenses.

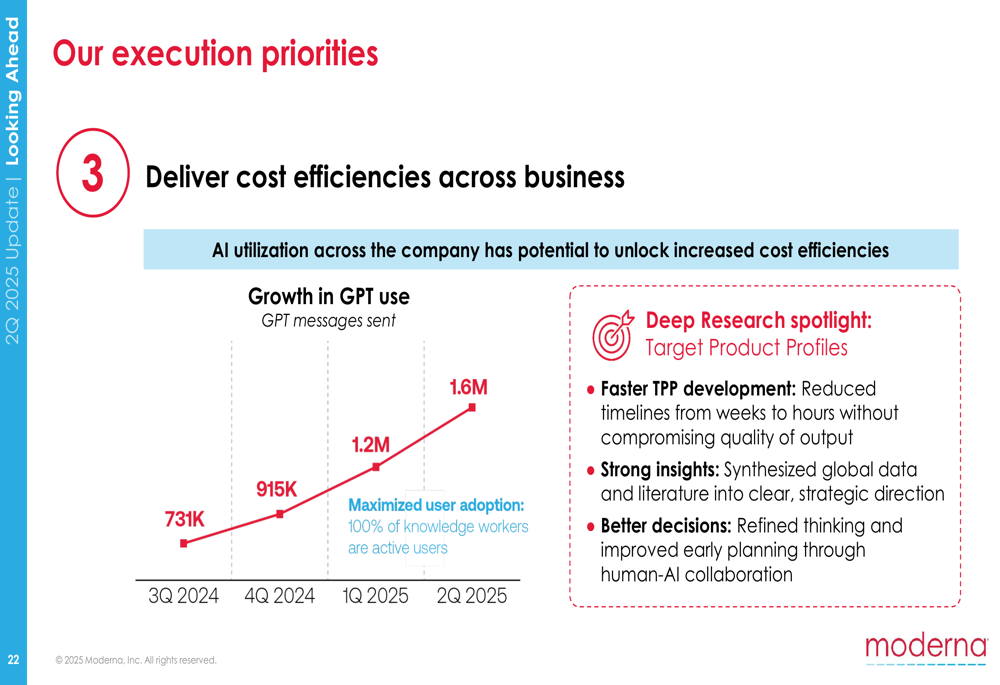

Additionally, the company is leveraging artificial intelligence to drive further efficiencies across the organization:

Forward-Looking Statements

Moderna updated its 2025 financial framework, projecting total revenue between $1.5-$2.2 billion, down from the previous high-end estimate of $2.5 billion. The company also lowered its R&D expense projection to $3.6-$3.8 billion from $4.1 billion, and reduced expected capital expenditures to $0.3 billion from $0.4 billion.

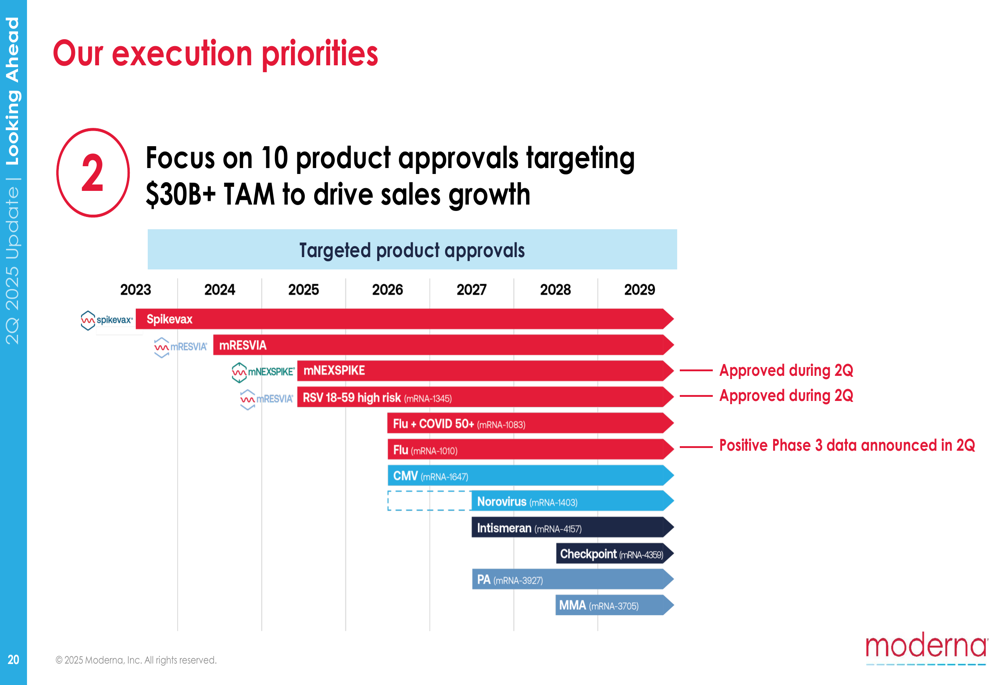

The company’s execution priorities focus on three key areas:

1. Driving use of its approved vaccines (Spikevax, mNEXSPIKE, and mRESVIA)

2. Focusing on 10 product approvals to drive sales growth

3. Delivering cost efficiency across the business

Moderna’s product approval timeline shows an ambitious roadmap for future growth:

CEO Stéphane Bancel emphasized the company’s commitment to streamlining operations while delivering on its pipeline promises. "We remain confident in our ability to further streamline our operation structure for the remaining of 2025 to 2027," Bancel stated during the earnings call.

With a clear strategy focused on pipeline advancement, cost reduction, and strategic prioritization, Moderna appears to be navigating its post-pandemic transition with a disciplined approach that has resonated with investors despite current revenue challenges. The company’s ability to execute on both its pipeline milestones and cost-cutting targets will be crucial for its long-term success in the evolving vaccine and therapeutics market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.