Two 59%+ winners, four above 25% in Aug – How this AI model keeps picking winners

Introduction & Market Context

Mohawk Industries (NYSE:MHK), the world’s largest flooring company, presented its Q2 2025 results on July 25, showcasing operational resilience in a challenging market environment. The company’s stock responded positively, rising 4.22% to close at $116, with aftermarket trading pushing shares up an additional 3.27% to $119.79.

The presentation highlighted Mohawk’s global scale and comprehensive product portfolio, emphasizing its position as an industry leader with $10.8 billion in 2024 net sales, approximately 41,900 employees, manufacturing operations in 19 countries, and product distribution in roughly 180 countries worldwide.

As shown in the following breakdown of Mohawk’s global presence and sales distribution:

Quarterly Performance Highlights

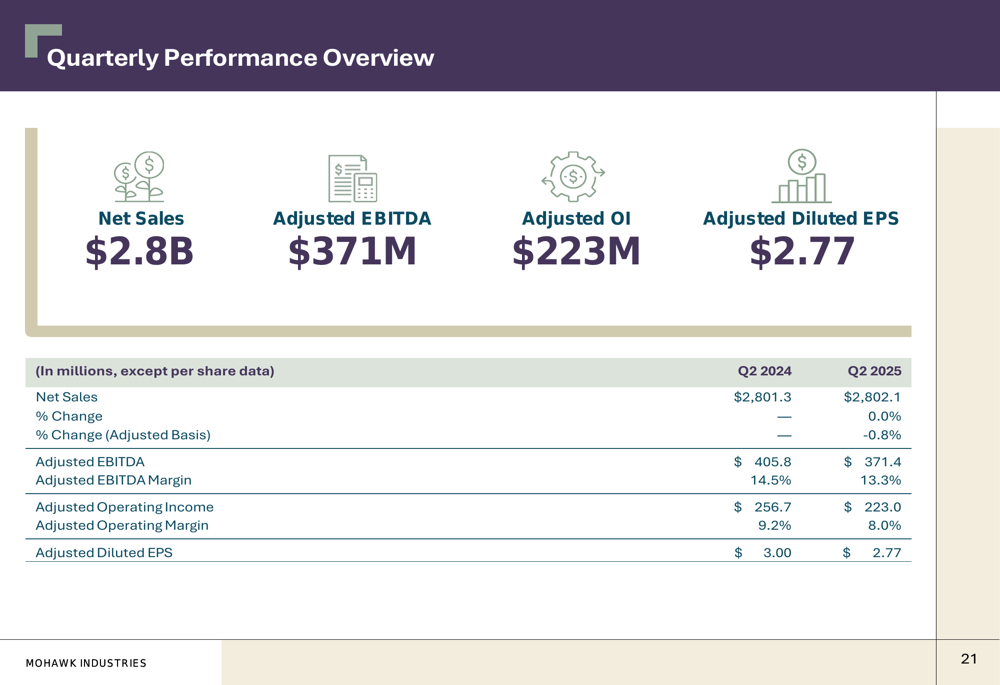

Mohawk reported essentially flat Q2 2025 sales of $2.8 billion compared to the year-ago period, while profitability metrics showed pressure. Adjusted EBITDA declined to $371.4 million from $405.8 million in Q2 2024, with adjusted EBITDA margin contracting from 14.5% to 13.3%. Adjusted operating income fell to $223 million from $256.7 million, resulting in adjusted operating margin compression from 9.2% to 8.0%. Adjusted diluted EPS came in at $2.77, down from $3.00 in the prior-year quarter but exceeding the company’s previous guidance of $2.52-$2.62.

The following chart details Mohawk’s Q2 2025 financial performance:

Despite the margin pressure, Mohawk generated approximately $126 million in free cash flow during the quarter. The company continued its shareholder return program, repurchasing approximately 393,000 shares for $42 million and announcing a new $500 million share repurchase program. Management also lowered its 2025 capital expenditure projection to approximately $500 million.

The company’s Q2 performance reflected the impact of operational improvements, cost containment actions, and market development initiatives, as illustrated in this overview:

Segment Performance Analysis

Mohawk’s Global Ceramic segment reported Q2 2025 sales of $1.12 billion, a slight increase from $1.12 billion in Q2 2024. However, adjusted operating income declined to $90.3 million from $94.8 million, with adjusted operating margin contracting to 8.1% from 8.5%. The segment benefited from favorable pricing and product mix, productivity gains, and higher sales of premium products, partially offset by higher input costs.

The Flooring Rest of World segment posted sales of $734.4 million, up from $727.2 million in Q2 2024. However, adjusted operating income declined significantly to $76.4 million from $91.4 million, with adjusted operating margin falling to 10.4% from 12.6%. The segment was positively impacted by productivity gains but faced headwinds from competitive industry pricing.

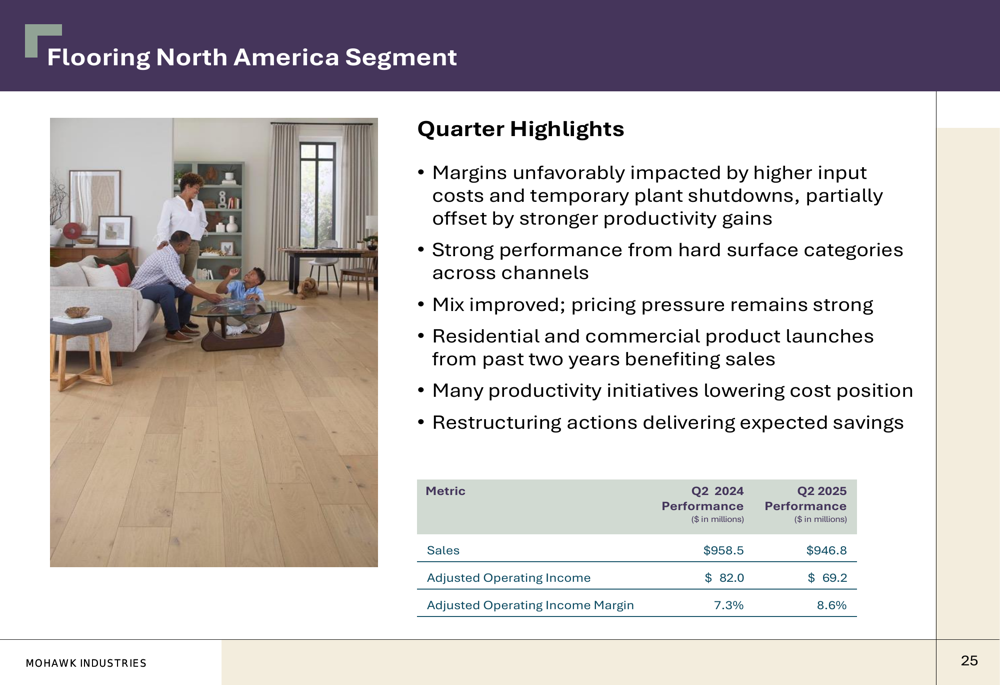

The Flooring North America segment recorded sales of $946.8 million, down from $958.5 million in Q2 2024. Adjusted operating income decreased to $69.2 million from $82.0 million, with adjusted operating margin declining to 7.3% from 8.6%. The segment was unfavorably impacted by higher input costs and temporary plant shutdowns, partially offset by stronger productivity gains and improved mix.

Strategic Initiatives and Competitive Positioning

Mohawk’s presentation emphasized several strategic advantages that position the company to navigate current market conditions and capitalize on future opportunities. These include long-term building trends, geographic reach, operational excellence, product innovation, and a strong financial position.

The company highlighted its leadership across multiple flooring categories in key regional markets, with differentiated products aligned with local preferences:

Mohawk also showcased its commitment to product innovation, featuring recent category innovations that provide competitive advantages through differentiation:

The company’s operational excellence initiatives focus on maximizing productivity, with restructuring actions expected to deliver approximately $100 million in savings in 2025. Mohawk emphasized its vertical integration, which optimizes process controls and ensures product quality and business agility.

Forward-Looking Statements

Looking ahead, Mohawk provided Q3 2025 adjusted EPS guidance of $2.56 to $2.66. Management noted that evolving tariffs are adding economic uncertainty, and the company has initiated price adjustments and supply chain optimization to counter the impact of initial tariff rates.

Market conditions remain soft due to inflation and cautious consumer outlook, with commercial continuing to outperform residential. Higher input costs are expected to continue, peaking in Q3. The company’s restructuring actions are on track to lower costs by approximately $100 million in 2025.

For the long term, Mohawk emphasized that its domestic U.S. manufacturing provides advantages against import-driven competition. The company noted that the industry historically rebounded by more than 10% annually in years following the trough of the Great Recession, and while the timing of an inflection point is unpredictable, industry volumes are expected to return to historical levels, supported by significant future demand from the housing deficit and aging homes across regions.

As shown in the company’s near-term outlook:

Mohawk maintains a strong financial position with a net debt to adjusted EBITDA ratio of 1.1x as of the end of 2024, down from 1.5x in 2023. The company’s total liquidity stood at $1.6 billion as of December 31, 2024, providing ample flexibility to navigate market challenges and pursue strategic opportunities.

Despite current headwinds, Mohawk’s management remains confident in the company’s ability to leverage its scale, geographic diversification, operational excellence, and product innovation to drive long-term value creation as market conditions improve.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.