Asia FX dithers as dollar steadies before Powell speech; yen muted after CPI data

Introduction & Market Context

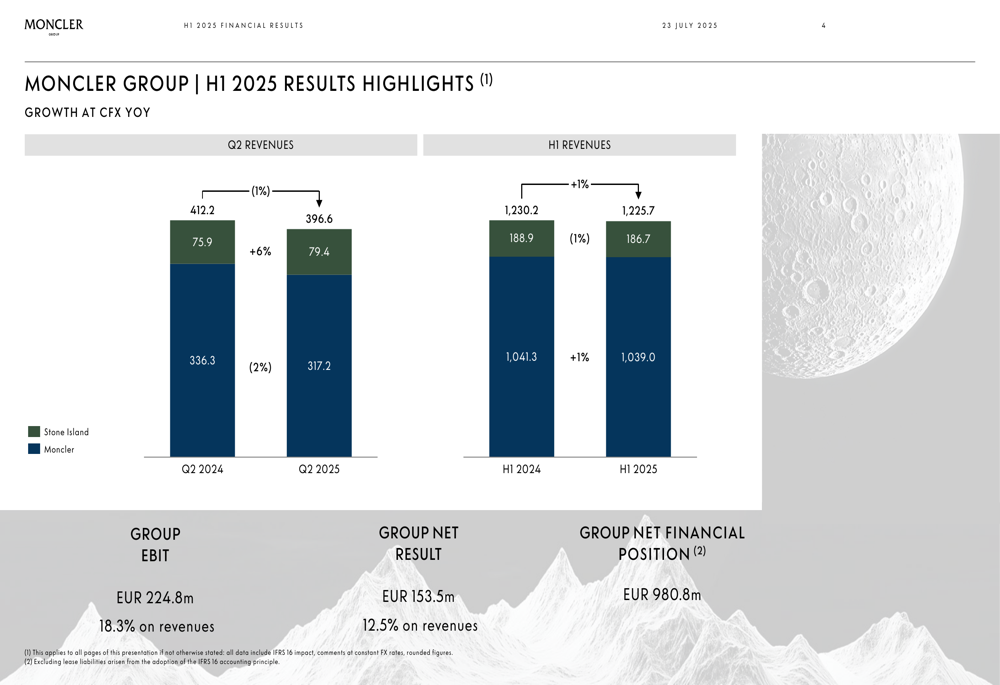

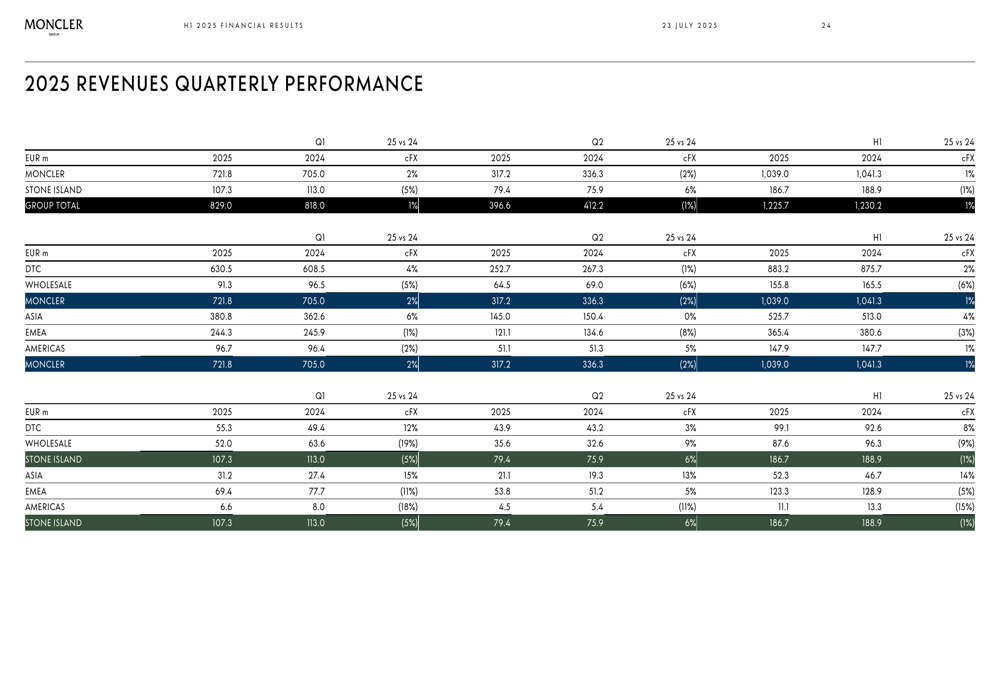

Moncler SpA (BIT:MONC) released its H1 2025 financial results on July 23, 2025, revealing a modest 1% year-over-year revenue growth at constant exchange rates, reaching €1,039.0 million. However, the luxury outerwear maker experienced a 2% revenue decline in Q2, signaling a slowdown from the positive momentum seen in the first quarter. The stock closed at €50.08, up 1.2% on the day of the announcement, but remains significantly below its 52-week high of €70.48.

Chairman and CEO Remo Ruffini acknowledged the challenging environment in his opening statement, emphasizing the need for vigilance and agility: "In a world that continues to be unpredictable and complex, companies need to be vigilant and agile... We will continue to operate with consistency and resilience, guided by a clear vision and awareness, to turn external challenges into opportunities."

Quarterly Performance Highlights

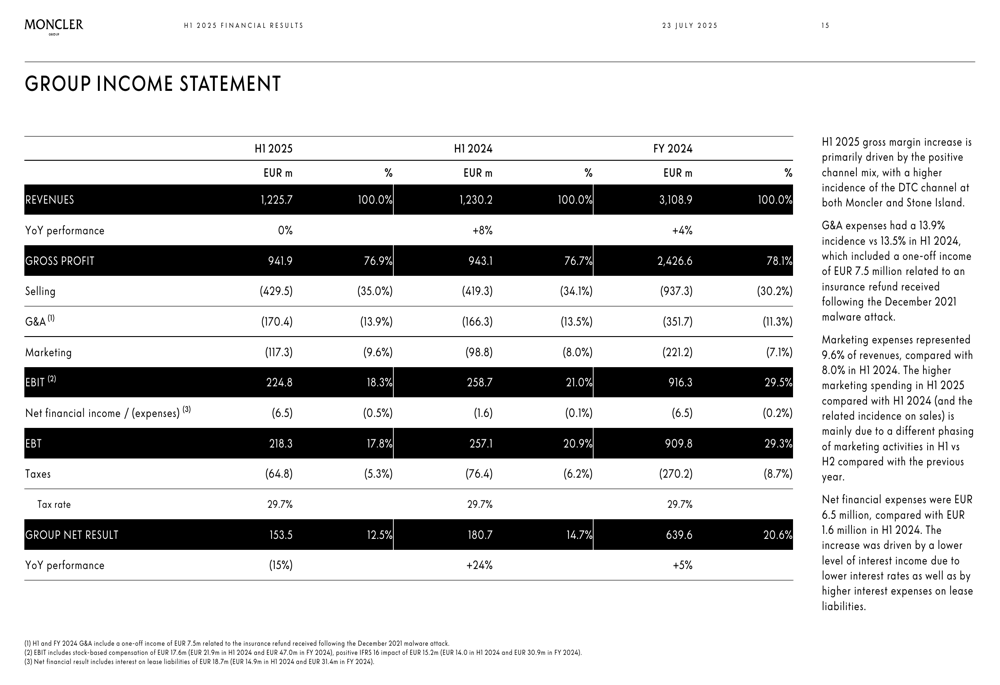

The Moncler Group reported H1 2025 revenues of €1,039.0 million, a slight increase of 1% at constant exchange rates compared to H1 2024. However, Q2 revenues declined by 2% to €396.6 million, indicating a slowdown from the first quarter. The group maintained strong profitability with EBIT reaching €224.8 million (18.3% of revenues) and net income of €153.5 million (12.5% of revenues).

As shown in the following chart of the group’s H1 2025 financial highlights:

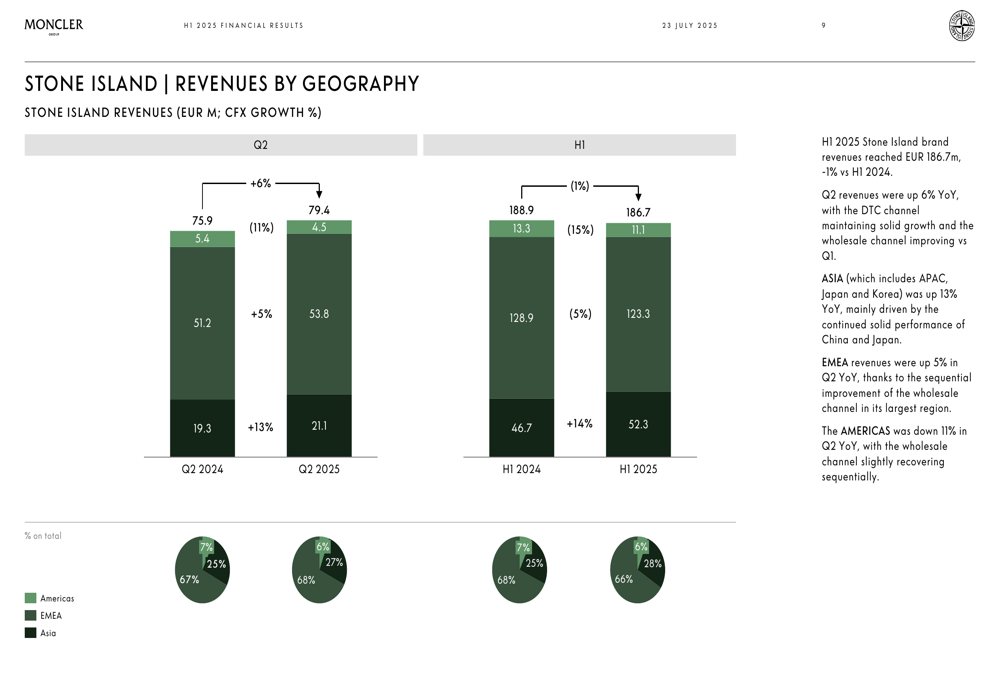

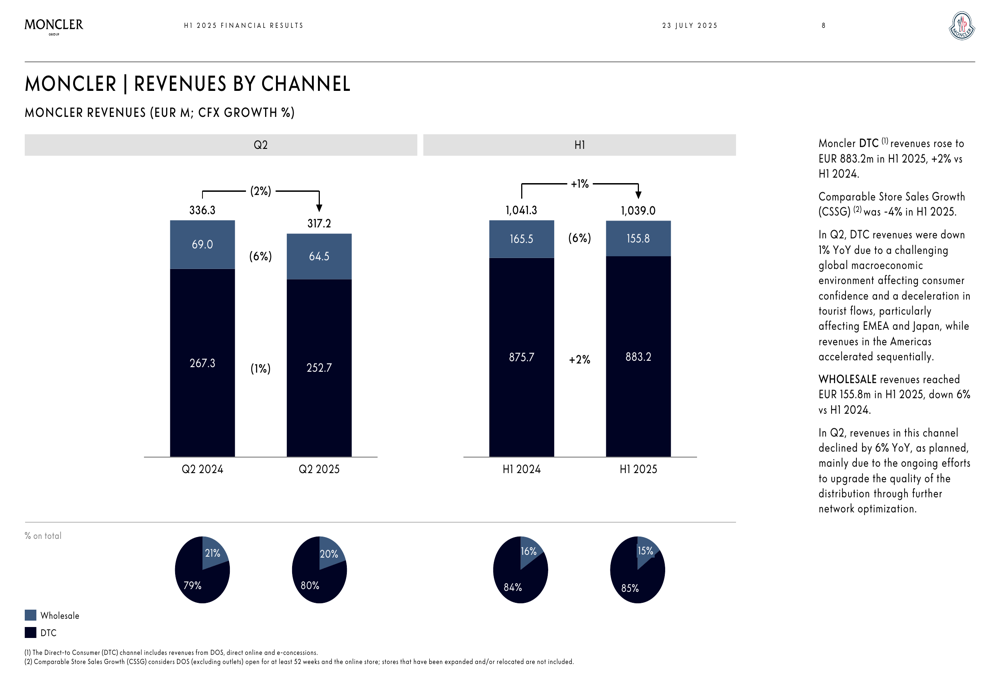

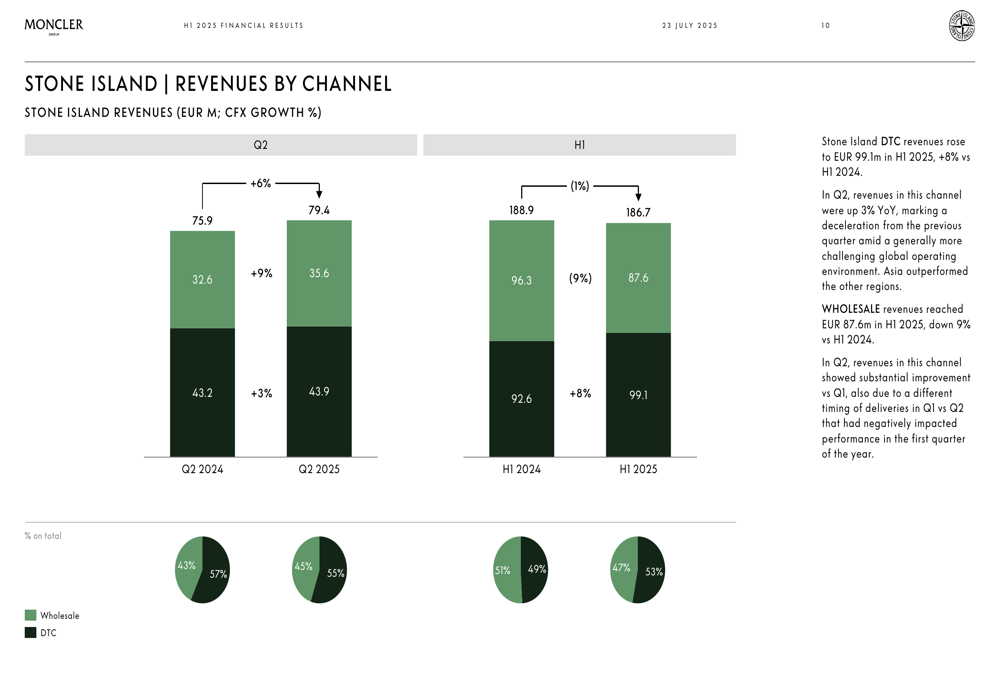

Breaking down performance by brand, Moncler’s flagship brand showed resilience with a 1% revenue increase in H1, despite a 2% decline in Q2. Stone Island delivered mixed results with a 6% revenue increase in Q2 to €79.4 million, but a 1% decline for the half-year period to €186.7 million.

The group’s income statement reveals stable gross margins at 76.9%, demonstrating the company’s continued pricing power in the luxury segment:

Geographic and Channel Analysis

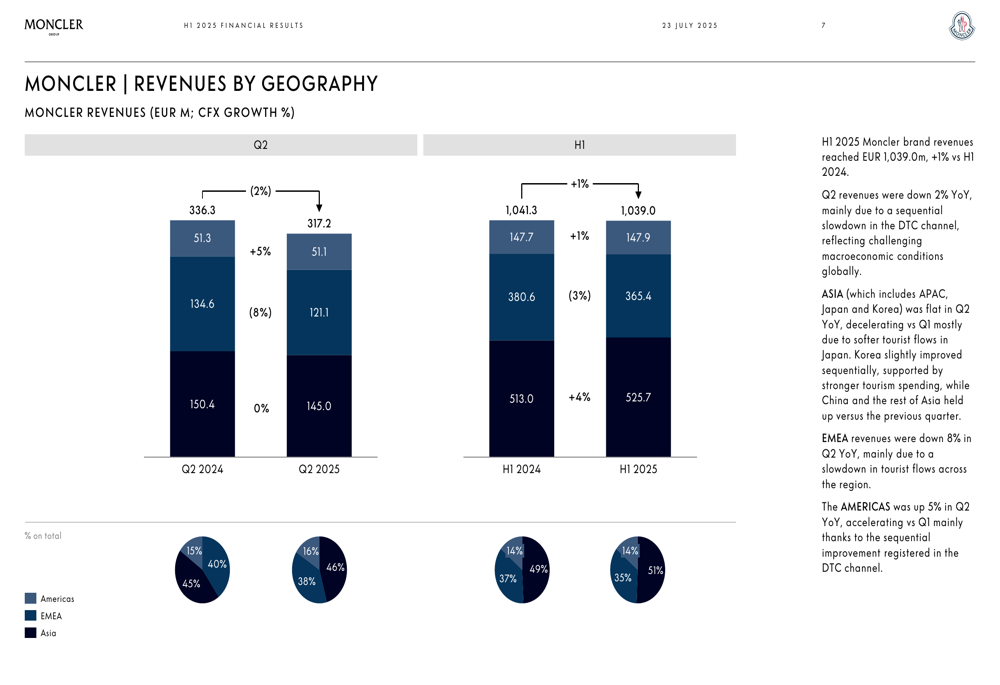

Moncler’s geographic performance continued to show significant regional divergence. Asia remained the growth engine for both brands, with Moncler reporting a 6% increase in H1 and Stone Island delivering an impressive 14% growth in the region. Conversely, EMEA (Europe, Middle East, and Africa) showed weakness with Moncler declining 3% and Stone Island falling 5% in H1. The Americas presented a mixed picture, with Moncler growing 4% while Stone Island experienced a substantial 15% decline.

The following geographic breakdown illustrates Moncler’s regional performance:

Stone Island’s geographic revenue distribution shows an even heavier reliance on the Asian market:

Both brands continued their strategic shift toward direct-to-consumer (DTC) channels. Moncler’s DTC revenues grew 2% in H1, now representing 84% of total brand revenues, while wholesale declined 6%. Stone Island’s DTC channel grew 8%, now accounting for 49% of brand revenues, while its wholesale channel contracted by 9%.

The channel performance for Moncler is illustrated in this breakdown:

Stone Island’s channel evolution is shown here:

Strategic Initiatives

During Q2, Moncler continued to strengthen its brand positioning through high-profile initiatives, including its debut at the Met Gala and collaborations with Mercedes-Benz (OTC:MBGAF) by NIGO and artist Donald Glover. Stone Island focused on cultural initiatives and collaborations, including a partnership with New Balance.

The group continued its retail expansion, operating 287 retail stores and 54 wholesale stores as of June 30, 2025. New store openings included locations in South Coast Plaza, Sydney Westfield, and Hangzhou, reinforcing the company’s commitment to enhancing its direct retail presence.

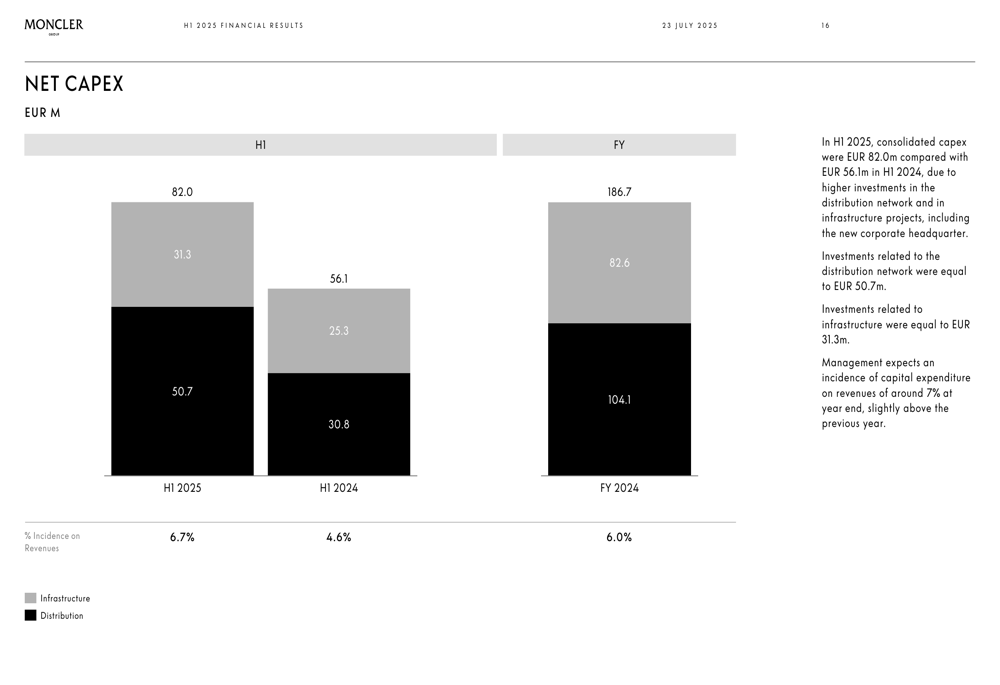

The company’s capital expenditure reached €82.0 million in H1 2025, with €50.7 million dedicated to the distribution network and €31.3 million to infrastructure projects:

Financial Position & Outlook

Moncler Group maintained a strong financial position with a positive net financial position of €980.8 million as of June 30, 2025. Working capital increased slightly to €283.7 million, representing 9.1% of revenues compared to 8.5% in the previous year.

The company’s net financial position is illustrated in this chart:

Looking ahead, management remains cautious about market conditions while emphasizing the importance of brand strength and operational flexibility. This approach aligns with comments made during the Q1 earnings call, where the company projected mid-single-digit growth in its direct-to-consumer channel for 2025 and highlighted its ability to adjust production by around 10% to maintain flexibility in the supply chain.

The detailed quarterly revenue breakdown provides insight into the company’s performance trajectory:

While Moncler continues to demonstrate resilience in a challenging luxury market, the Q2 slowdown and regional disparities highlight the ongoing challenges facing the sector. The company’s strong balance sheet and strategic focus on direct-to-consumer channels position it to navigate these challenges, but investors will be watching closely for signs of recovery in the European and American markets in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.