Gold prices hit 4-month high on Fed easing hopes, tariff uncertainty

Motorola Solutions (NYSE:MSI) presented its second-quarter 2025 earnings results on August 7, showing solid growth across all technology segments and announcing a significant acquisition that has prompted the company to raise its full-year outlook.

Quarterly Performance Highlights

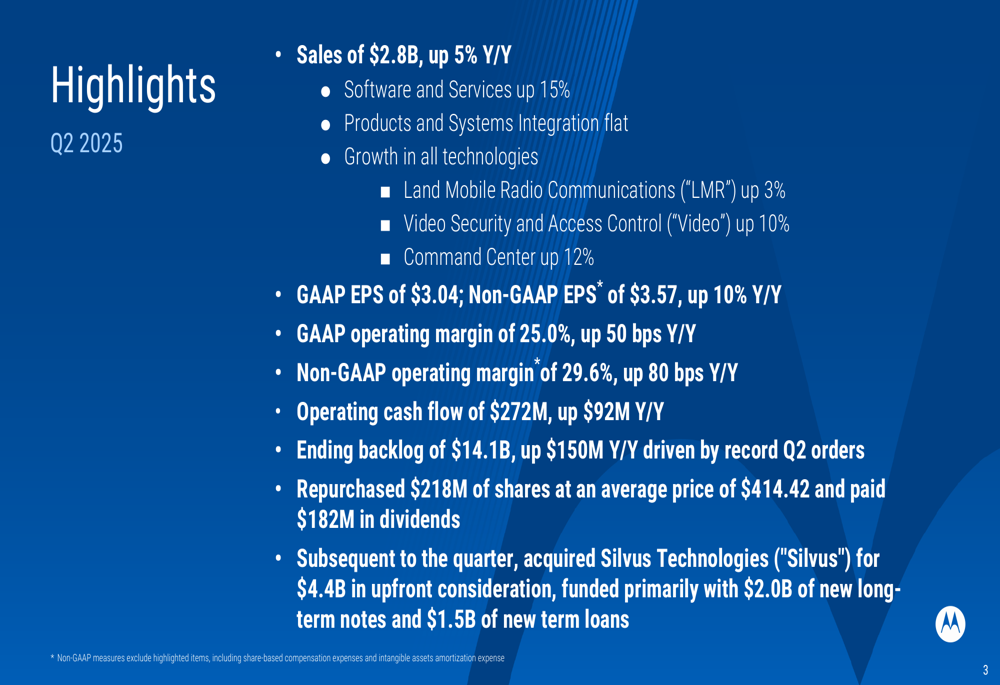

Motorola reported Q2 2025 sales of $2.8 billion, representing a 5% year-over-year increase. The growth was primarily driven by the Software (ETR:SOWGn) and Services segment, which surged 15%, while Products and Systems Integration remained flat compared to the prior year.

The company delivered GAAP earnings per share of $3.04 and non-GAAP EPS of $3.57, the latter marking a 10% increase from Q2 2024. Operating margins also improved, with GAAP operating margin rising 50 basis points to 25.0% and non-GAAP operating margin increasing 80 basis points to 29.6%.

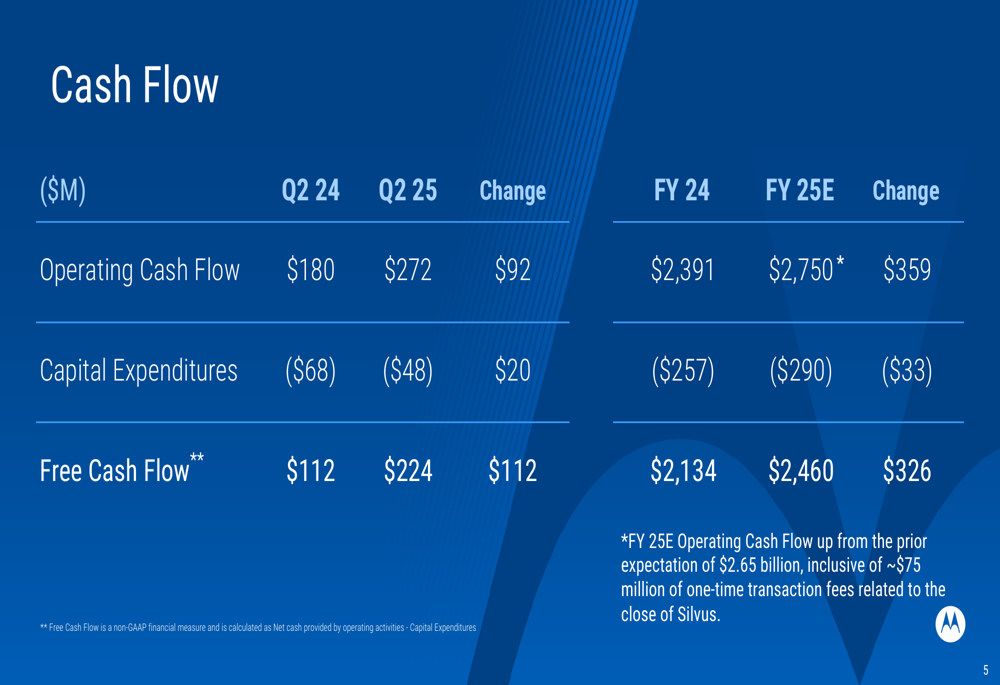

Cash flow performance showed significant improvement, with operating cash flow of $272 million, up $92 million year-over-year. Free cash flow more than doubled to $224 million compared to $112 million in Q2 2024. The company has raised its full-year 2025 operating cash flow expectation from the previous guidance.

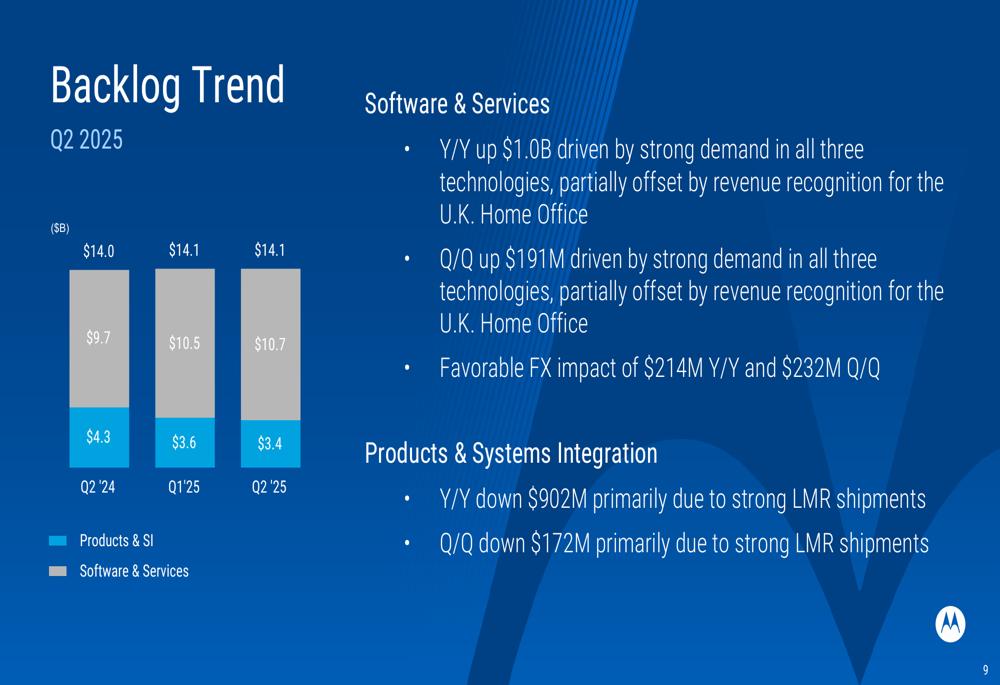

Motorola’s backlog reached $14.1 billion, representing a $150 million increase year-over-year, driven by record Q2 orders. The Software & Services backlog grew by $1.0 billion year-over-year to $10.7 billion, while the Products & Systems Integration backlog decreased by $902 million to $3.4 billion, primarily due to strong LMR (Land Mobile Radio) shipments.

Segment Performance Analysis

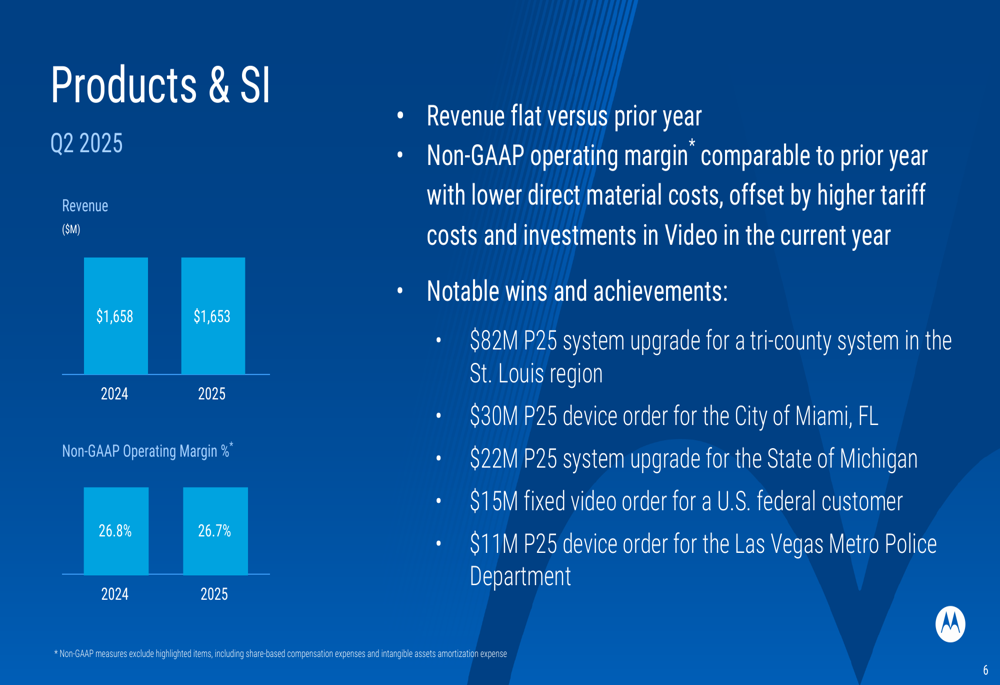

The Products & Systems Integration segment reported flat revenue of $1.65 billion compared to the prior year, with non-GAAP operating margin holding steady at 26.7% versus 26.8% in Q2 2024. The company cited lower direct material costs offset by higher tariff costs and investments in Video as factors affecting the margin.

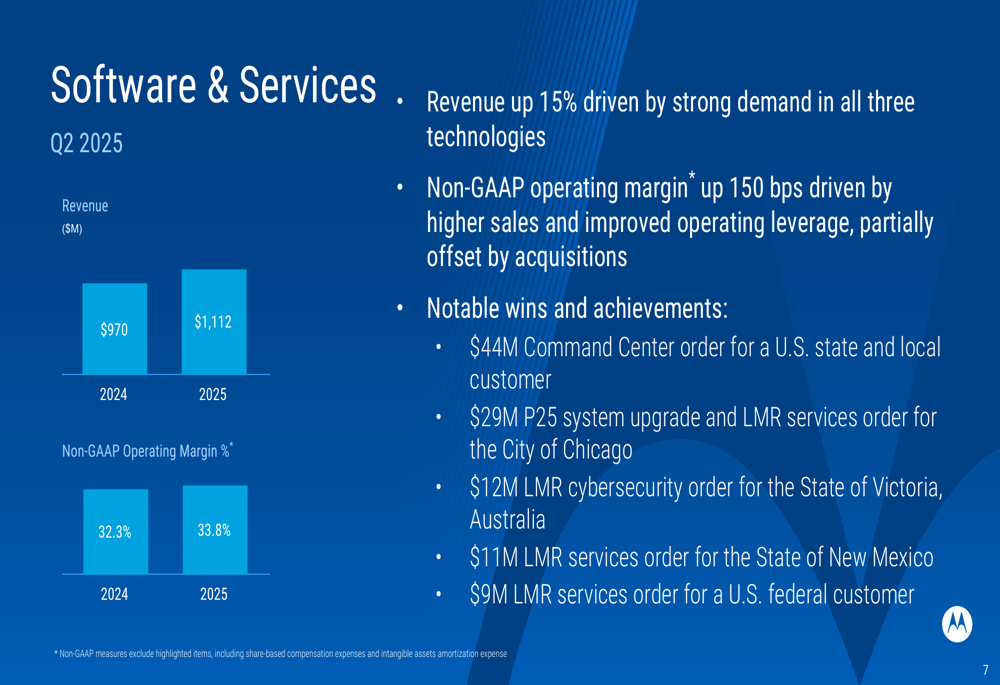

In contrast, the Software & Services segment demonstrated robust performance with revenue increasing 15% to $1.11 billion. This segment also saw non-GAAP operating margin expand by 150 basis points to 33.8%, driven by higher sales and improved operating leverage, partially offset by acquisitions.

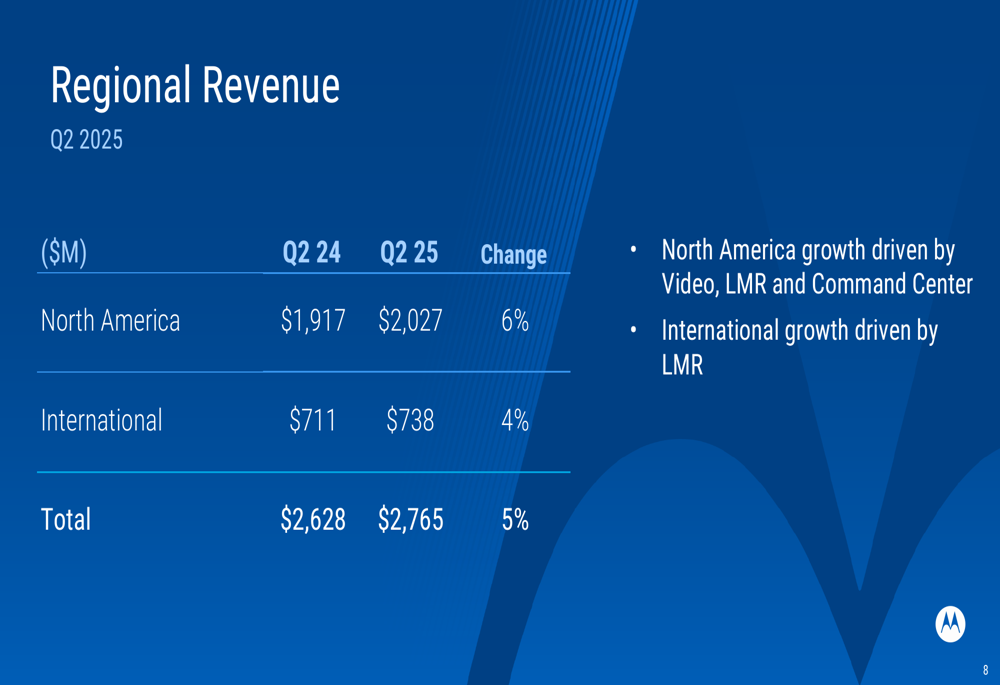

From a regional perspective, North America continued to lead growth with revenue of $2.03 billion, up 6% year-over-year, driven by Video, LMR, and Command Center solutions. International revenue grew 4% to $738 million, primarily due to strength in LMR technology.

Strategic Acquisition of Silvus Technologies

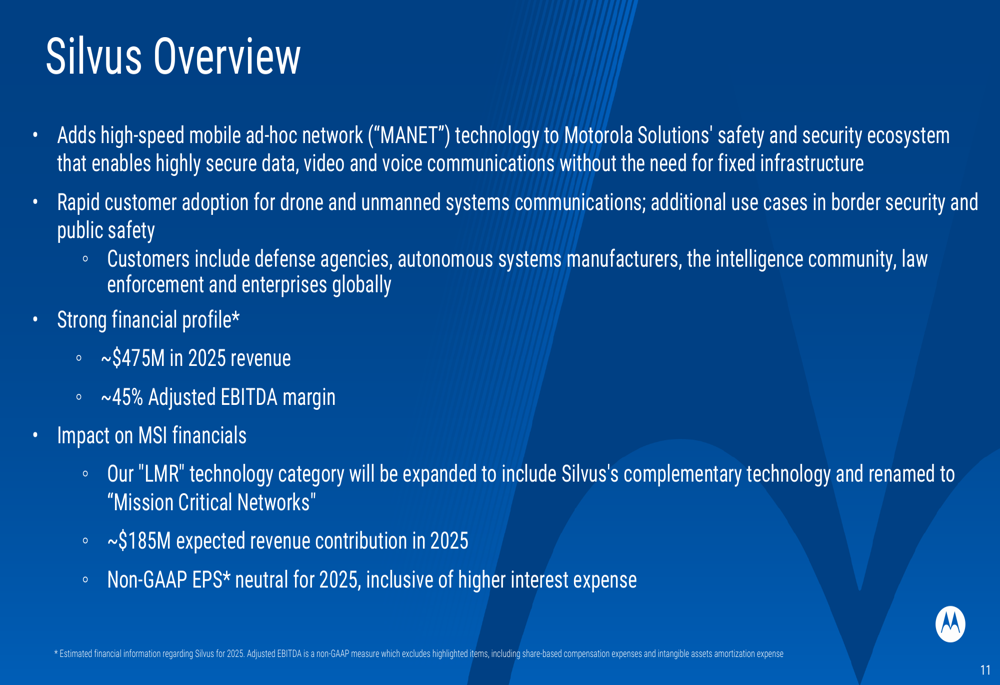

A significant development in the quarter was Motorola’s acquisition of Silvus Technologies for $4.4 billion, funded primarily with $2.0 billion of new long-term notes and $1.5 billion of new term loans. This acquisition adds high-speed mobile ad-hoc network (MANET) technology to Motorola’s safety and security ecosystem.

Silvus Technologies enables secure data, video, and voice communications without fixed infrastructure, with applications in drone and unmanned systems communications, border security, and public safety. The company has a strong financial profile with projected 2025 revenue of approximately $475 million and an adjusted EBITDA margin of around 45%.

Financial Outlook and Guidance

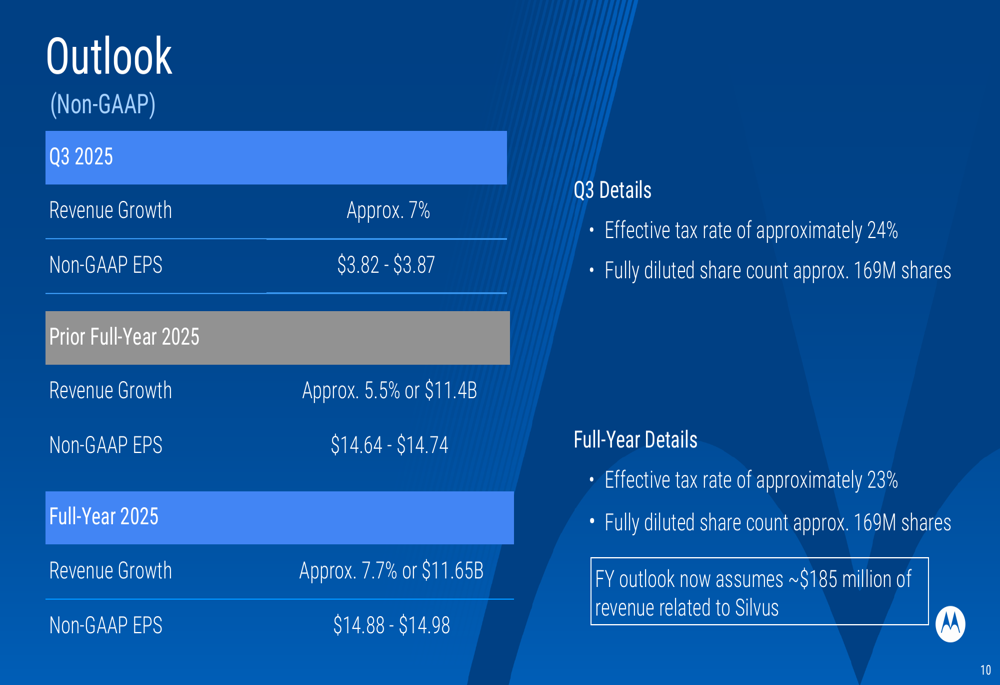

Following the strong Q2 results and the Silvus acquisition, Motorola has raised its full-year 2025 guidance. The company now expects revenue growth of approximately 7.7% to $11.65 billion, up from the previous forecast of 5.5% growth to $11.4 billion. This updated outlook includes approximately $185 million of revenue related to Silvus.

Non-GAAP EPS guidance has also been increased to a range of $14.88 to $14.98, compared to the previous range of $14.64 to $14.74. For the third quarter of 2025, Motorola anticipates revenue growth of approximately 7% and non-GAAP EPS between $3.82 and $3.87.

Conclusion

Motorola Solutions’ Q2 2025 results demonstrate continued momentum across its business segments, particularly in Software and Services. The acquisition of Silvus Technologies represents a strategic expansion of the company’s capabilities, prompting management to rename its LMR category to "Mission Critical Networks" to encompass this complementary technology.

The raised full-year guidance reflects management’s confidence in sustained growth, supported by a strong backlog and the integration of Silvus. With improving margins and robust cash flow generation, Motorola appears well-positioned to continue its positive trajectory through the remainder of 2025.

The company’s stock closed at $445.10 on August 7, 2025, up 0.67% for the day, suggesting a positive market reception to the earnings results and strategic developments.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.