Street Calls of the Week

Introduction & Market Context

Mr. Cooper Group Inc. (NASDAQ:COOP) presented its second quarter 2025 earnings results on July 23, showing strong performance across key business segments. The mortgage servicing and origination company reported significant growth in its servicing portfolio and a substantial increase in origination volumes compared to the prior year.

The company’s stock responded positively to the results, trading up 6.49% in premarket at $180.10, building on yesterday’s close of $169.12. This represents a substantial recovery from the company’s disappointing first quarter, when it missed analyst expectations with an EPS of $1.35 versus the forecasted $2.98.

Quarterly Performance Highlights

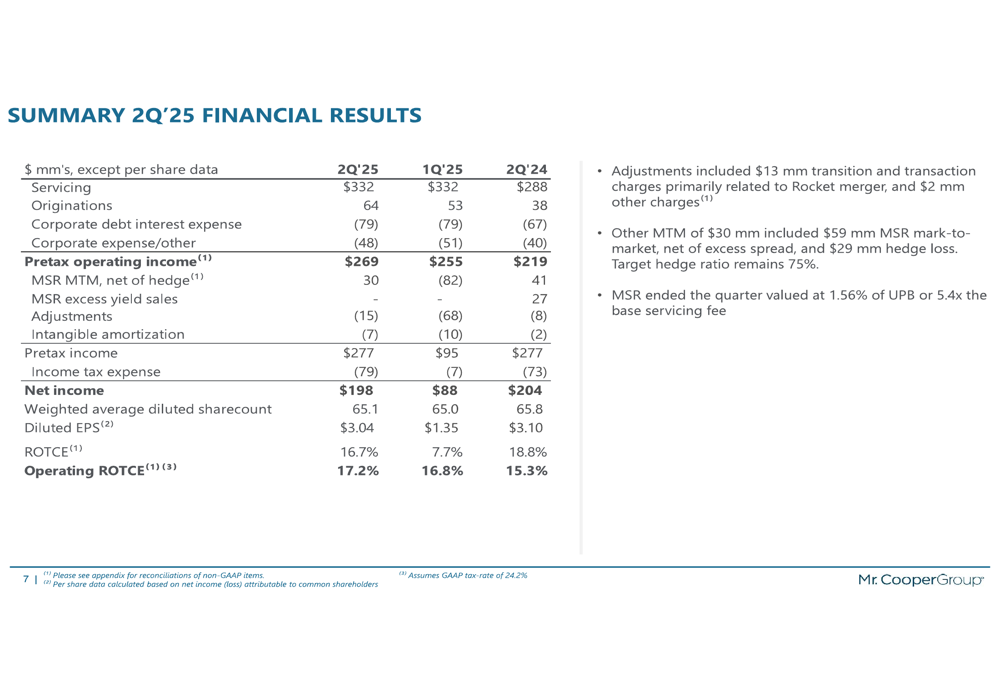

Mr. Cooper reported net income of $198 million for the second quarter of 2025, with pretax operating income reaching $269 million. The company achieved a return on tangible common equity (ROTCE) of 16.7%, including other mark-to-market adjustments of $30 million, while operating ROTCE came in at 17.2%.

As shown in the following comprehensive financial summary:

The company’s performance demonstrates continued improvement from the previous quarter, when it reported net income of $88 million and pretax operating earnings of $255 million. The Q2 results reflect the company’s ability to capitalize on its growing servicing portfolio and increased origination volumes.

Servicing Business Performance

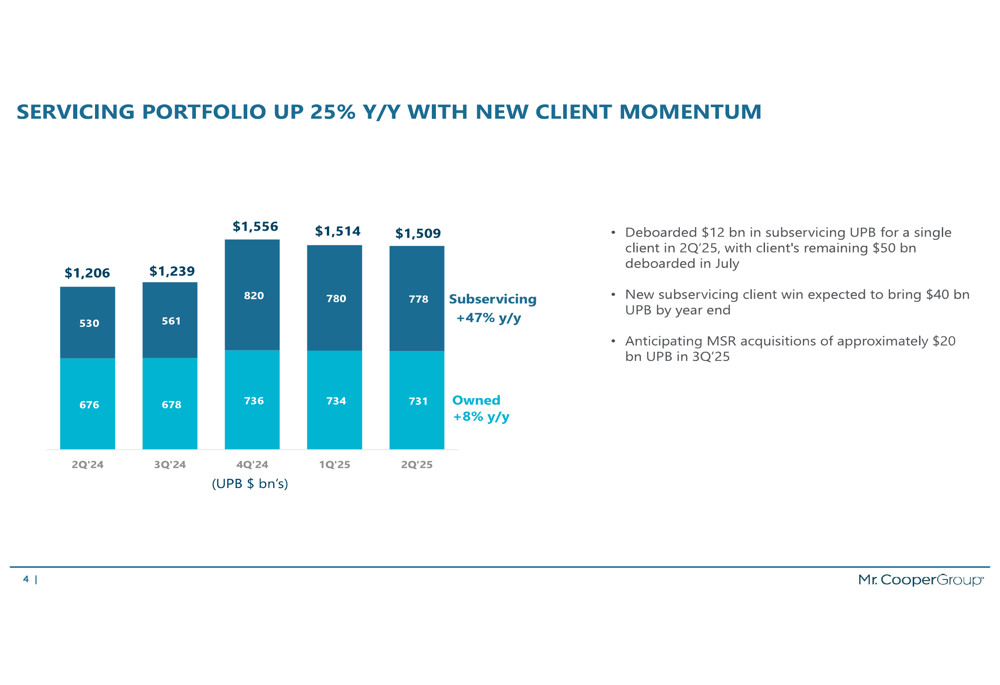

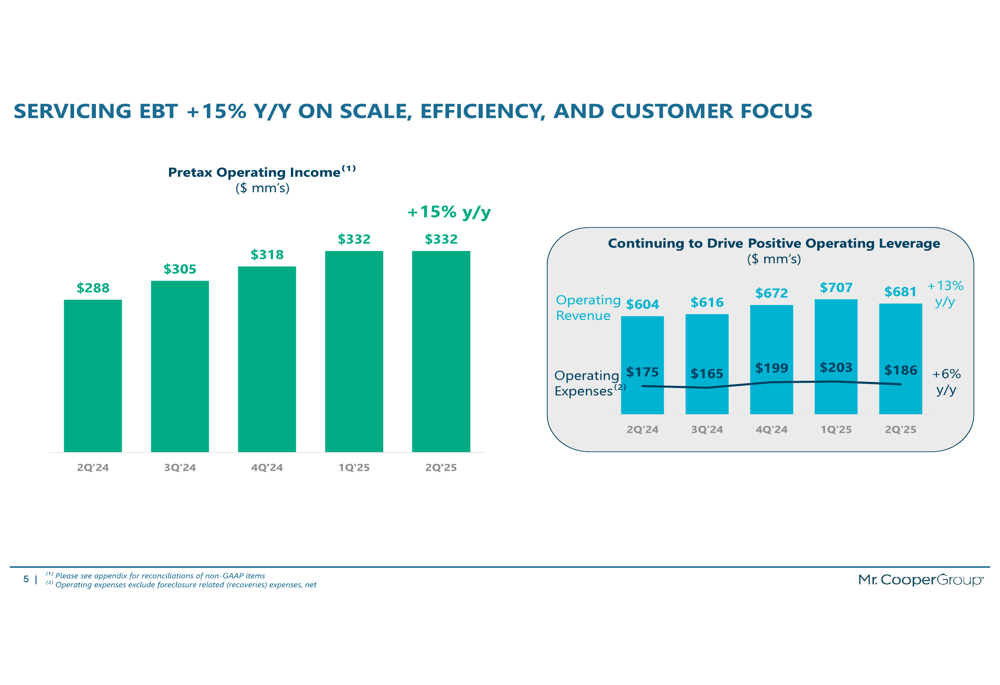

Mr. Cooper’s servicing business continued to be the primary driver of profitability, generating $332 million in pretax operating income. The company’s total servicing portfolio grew by an impressive 25% year-over-year to $1.5 trillion in unpaid principal balance (UPB).

The following chart illustrates this substantial growth trajectory:

The servicing portfolio growth was primarily driven by a 47% year-over-year increase in subservicing UPB, while owned MSRs grew by 8%. Despite deboarding $12 billion in subservicing UPB for a single client in Q2, with the client’s remaining $50 billion deboarded in July, the company announced a new subservicing client win expected to bring $40 billion UPB by year-end. Additionally, Mr. Cooper anticipates MSR acquisitions of approximately $20 billion UPB in the third quarter.

The servicing segment’s profitability has shown consistent improvement, with pretax operating income growing 15% year-over-year:

The company has successfully achieved positive operating leverage in its servicing business, with operating revenue increasing by 13% year-over-year to $681 million, while operating expenses grew at a slower rate of 6% to $186 million.

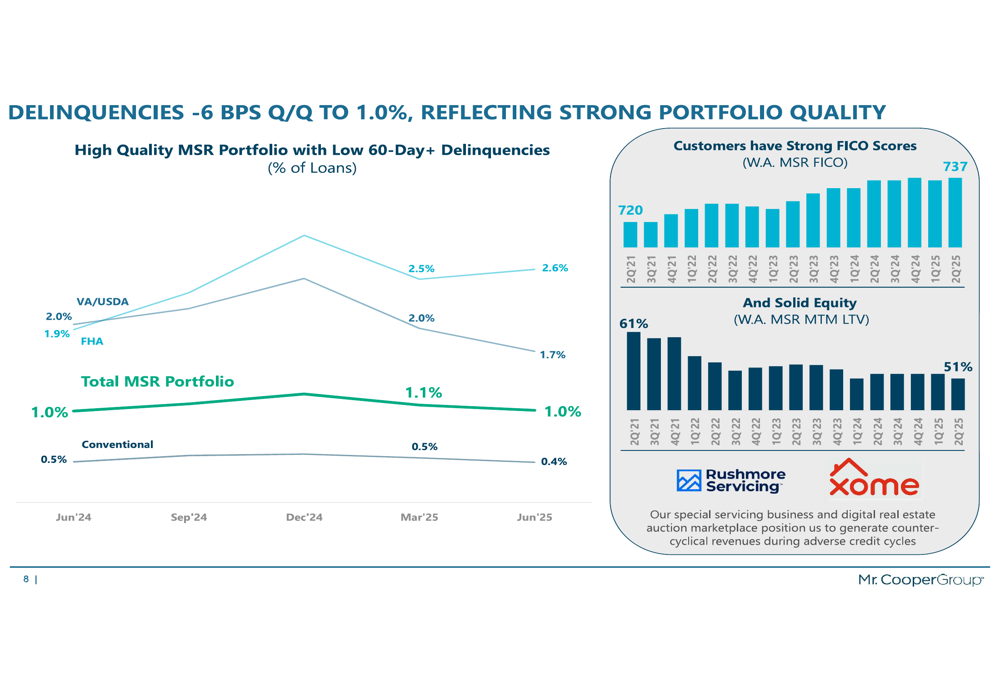

Portfolio quality remains strong, with 60-day+ delinquencies decreasing by 6 basis points quarter-over-quarter to just 1.0%. The weighted average FICO score across the MSR portfolio stands at a healthy 737, with solid equity metrics at 51%.

Originations Business Performance

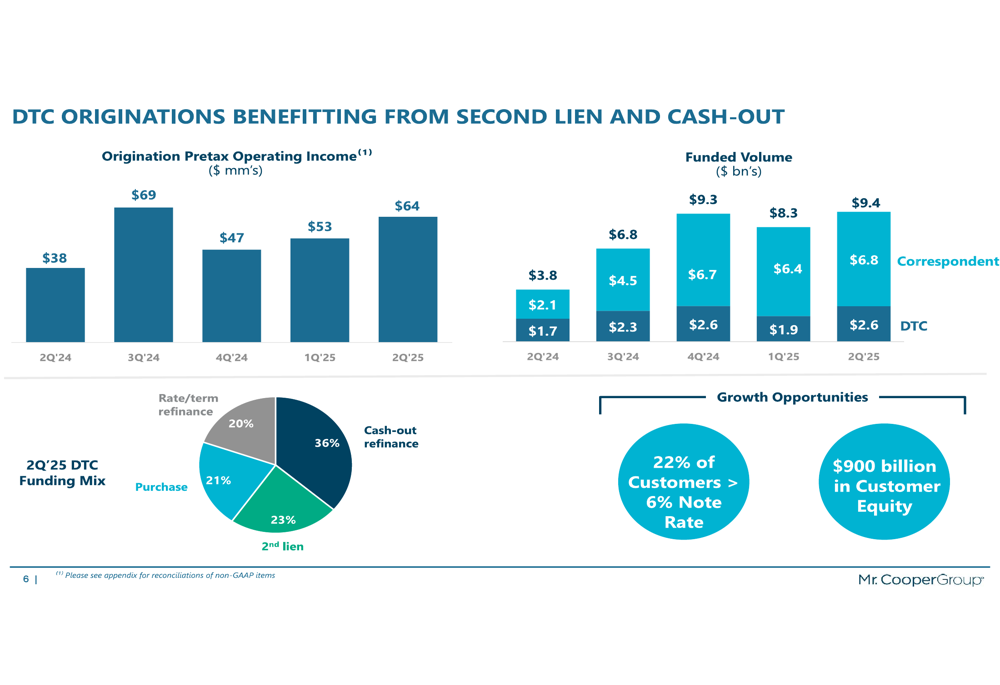

Mr. Cooper’s originations segment delivered $64 million in pretax operating income on funded volume of $9.4 billion, more than doubling the $3.8 billion funded in Q2 2024. The direct-to-consumer (DTC) channel continues to be a significant focus for the company.

The following chart shows the consistent growth in origination volumes and profitability:

The DTC funding mix for Q2 2025 was well-diversified, with cash-out refinances representing the largest portion at 36%, followed by second liens at 23%, purchase mortgages at 21%, and rate/term refinances at 20%. This balanced approach helps the company maintain origination volumes across different interest rate environments.

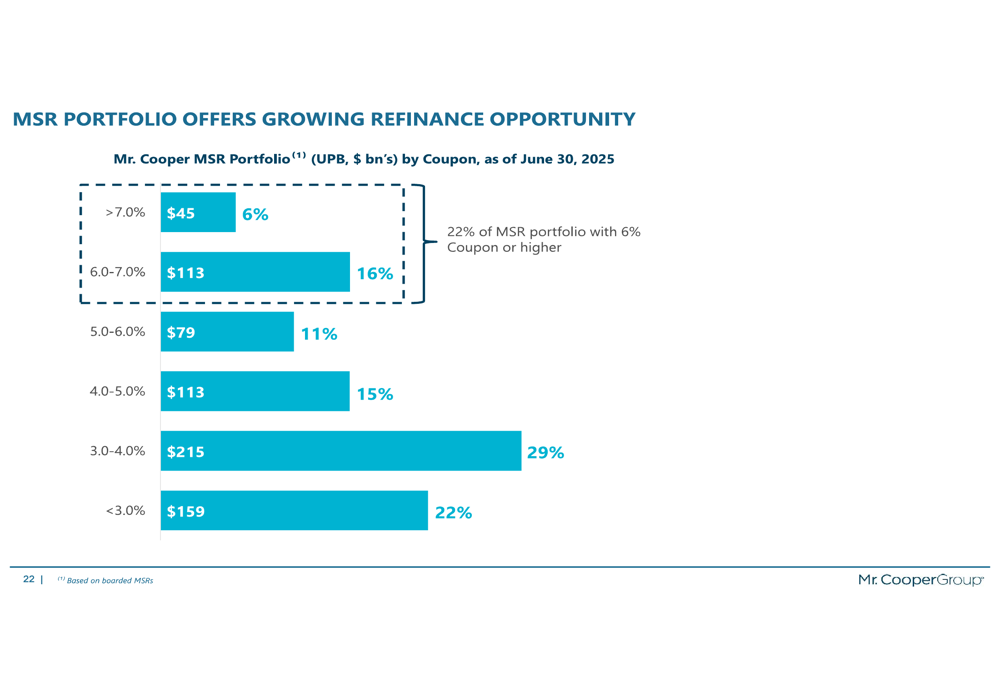

The company highlighted significant growth opportunities, noting that 22% of its customers have mortgage rates above 6%, representing a substantial refinance opportunity as rates potentially moderate. Additionally, Mr. Cooper identified $900 billion in customer equity that could be tapped through cash-out refinances and second liens.

Strategic Initiatives & Outlook

Following the quarter’s end, Mr. Cooper launched an MSR Fund with an initial $200 million commitment, representing a strategic move to expand its investment capabilities in the mortgage servicing rights market. This initiative aligns with the company’s core competencies and provides additional avenues for growth.

The company also highlighted its workplace culture achievements, being recognized by Great Place to Work as one of the Best Workplaces in Texas. This recognition is particularly notable given the competitive labor market in the financial services industry.

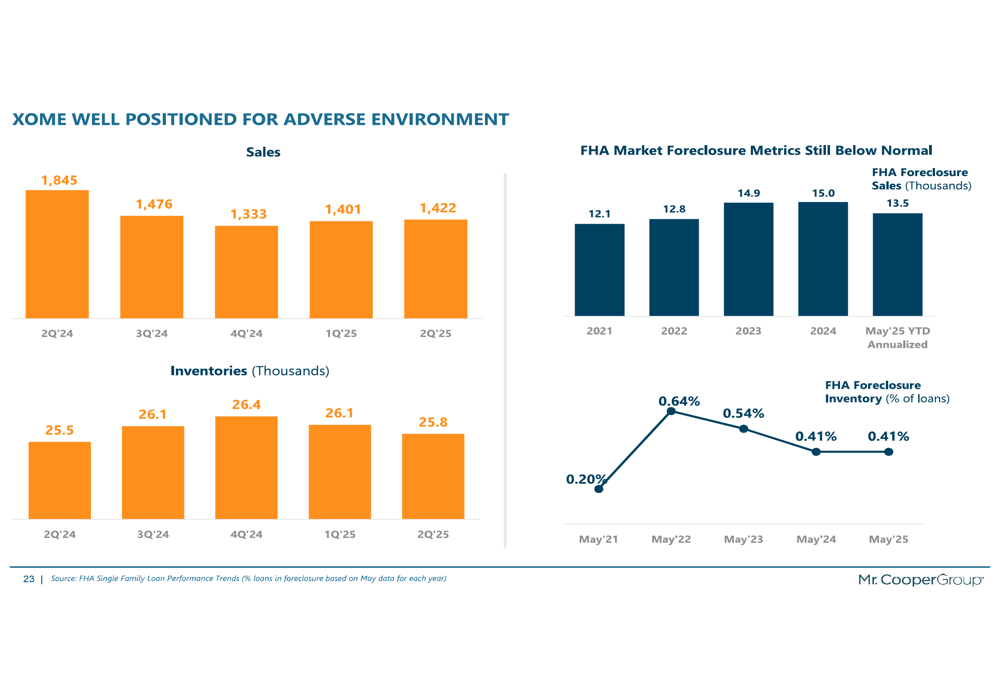

For Xome, the company’s real estate services platform, Mr. Cooper indicated it is well-positioned for an adverse environment, with inventory levels and foreclosure metrics still below historical averages but showing signs of normalization.

Financial Position & Capital Management

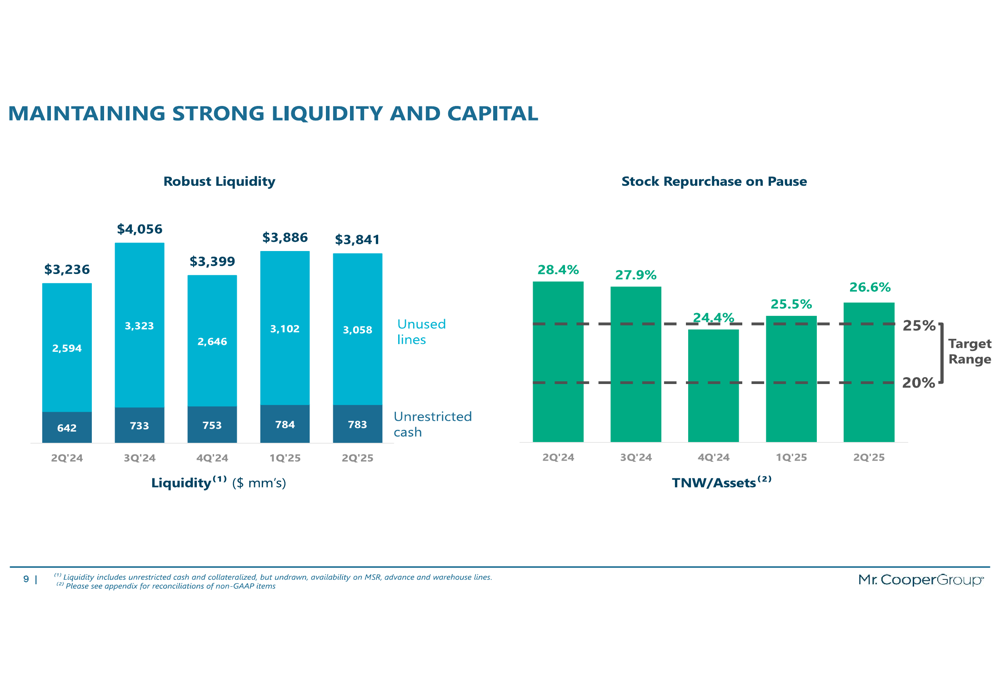

Mr. Cooper maintained a strong financial position with $3.8 billion in liquidity as of Q2 2025, consisting of unrestricted cash and unused lines of credit. The company’s tangible net worth to assets ratio stood at 26.6%, down from 28.4% a year ago but still representing a robust capital position.

The company noted that stock repurchases remain on pause, suggesting a conservative approach to capital management in the current environment. This differs from the context provided in the Q1 earnings report, which mentioned a pending transaction with Rocket Mortgage expected to close by Q4 2025, though this transaction was not specifically addressed in the Q2 presentation materials.

Tangible book value per share reached $75.90, providing a solid foundation for shareholder value. The company’s balance sheet remains strong with total assets of $18,499 million and total stockholders’ equity of $5,099 million as of the end of Q2 2025.

Overall, Mr. Cooper’s Q2 2025 results demonstrate a significant improvement from its Q1 performance, with strong growth in its core servicing business, doubled origination volumes, and strategic initiatives positioning the company for continued success in the evolving mortgage market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.