Gold prices fall as geopolitical tensions ease; U.S. CPI looms

Introduction & Market Context

MSA Safety (NYSE:MSA), a global leader in safety equipment, presented its second quarter 2025 earnings results on August 5, 2025, revealing a mixed performance characterized by modest revenue growth but declining profitability metrics. The company reported a 3% increase in net sales while navigating challenges from tariffs and inflation that pressured margins. Despite these headwinds, MSA’s stock rose 1.54% following the presentation, closing at $180.18.

The company’s presentation highlighted its continued focus on worker safety across diverse end markets including energy, utilities, HVAC-R, water treatment, food retail, and industrial sectors. With a market capitalization of approximately $6.1 billion, MSA Safety maintains its position as a premium provider of safety solutions with a strong emphasis on detection technology, fire service equipment, and industrial personal protective equipment (PPE).

Quarterly Performance Highlights

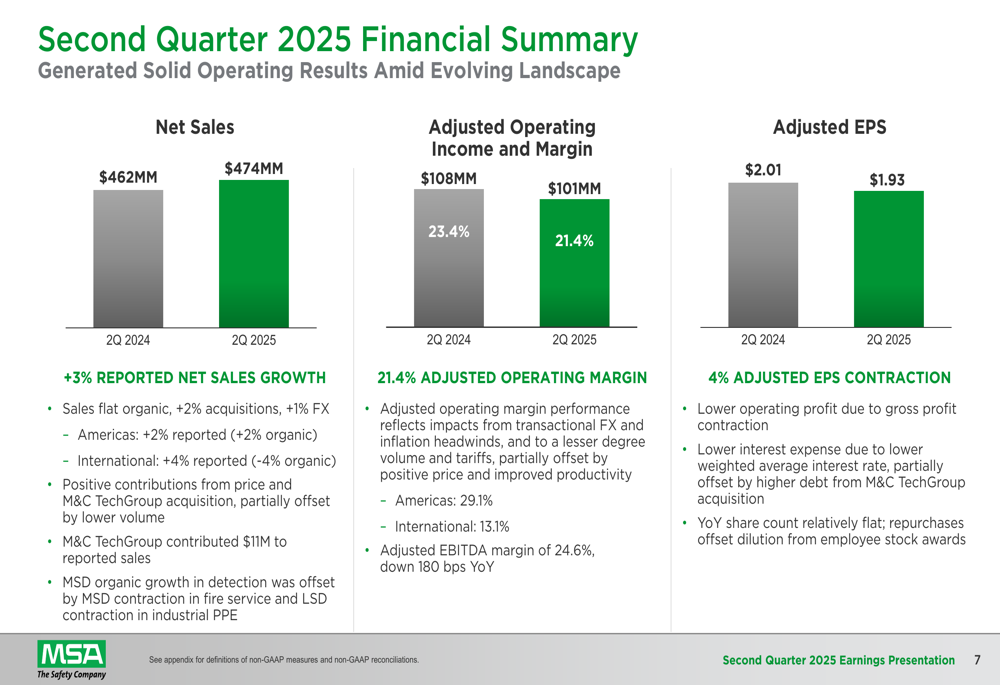

MSA Safety generated $474 million in net sales for Q2 2025, representing a 3% increase on a reported basis compared to the same period last year. However, organic sales remained flat year-over-year, with acquisition contributions (+2%) and favorable currency translation (+1%) accounting for the reported growth. The Americas segment grew 2% both on a reported and organic basis, while the International segment showed 4% reported growth but declined 4% organically.

As shown in the following financial summary chart:

Profitability metrics declined across the board, with adjusted operating income falling 6% to $101 million and adjusted operating margin contracting 200 basis points to 21.4%. Adjusted earnings per share decreased 4% to $1.93. Management attributed these declines primarily to transactional foreign exchange impacts and inflation headwinds affecting gross margins.

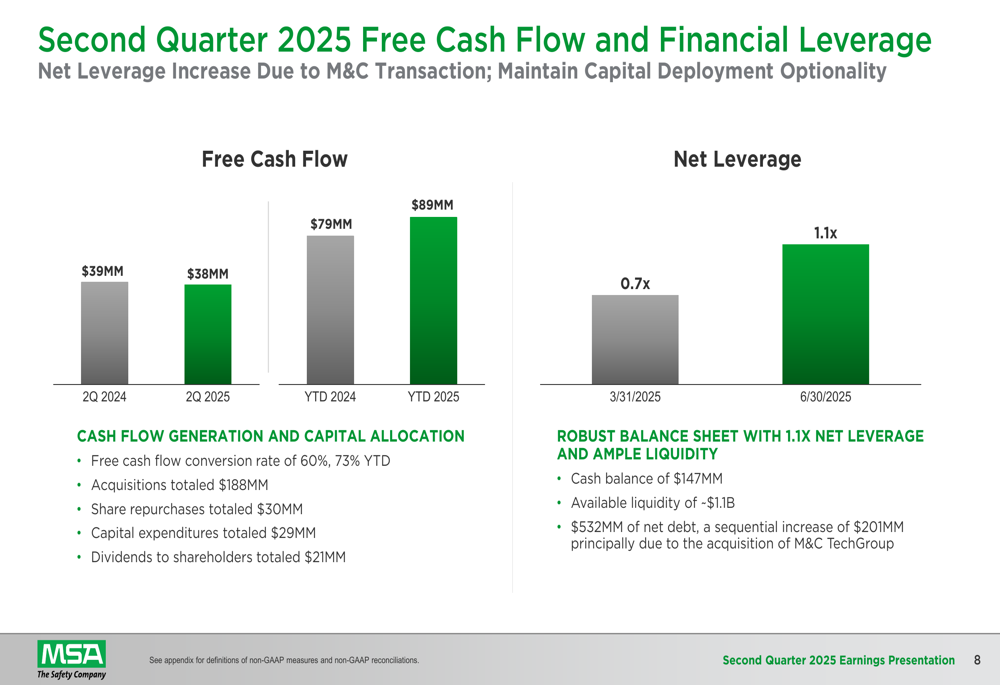

Free cash flow remained relatively stable at $38 million for the quarter with a 60% conversion rate, compared to $39 million in Q2 2024. Year-to-date free cash flow improved to $89 million, up from $79 million in the prior year period.

The company’s financial position remains solid despite increased leverage from recent acquisition activity. Net leverage increased to 1.1x from 0.7x at the end of the first quarter, primarily due to the M&C TechGroup acquisition. MSA maintains substantial liquidity of approximately $1.1 billion with a cash balance of $147 million.

Strategic Initiatives

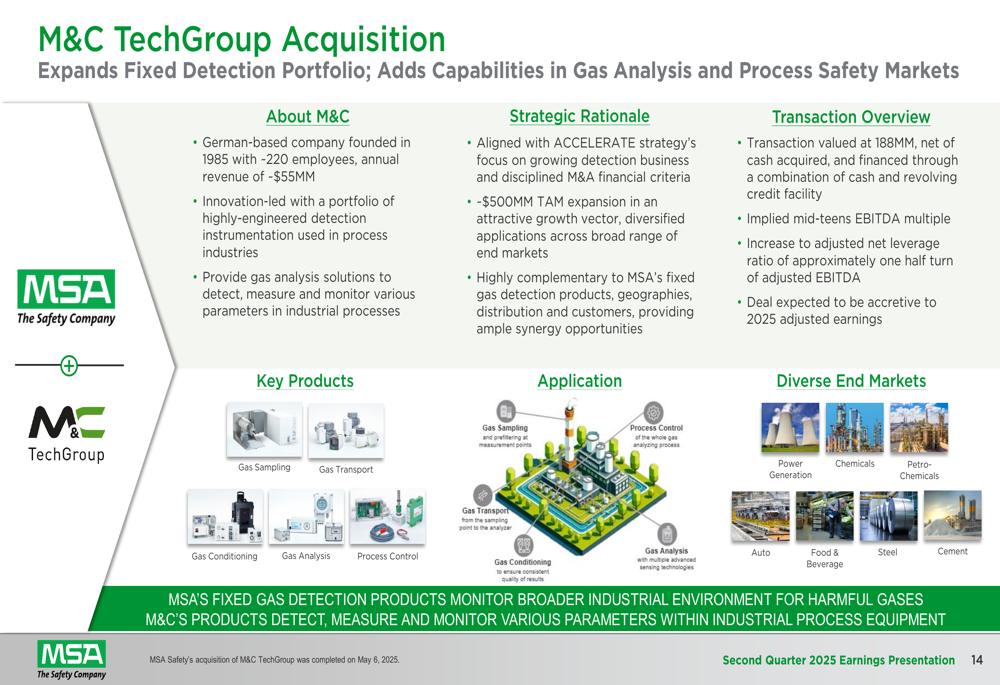

The most significant strategic development in the quarter was MSA’s acquisition of M&C TechGroup, a German-based company specializing in gas analysis solutions. The $188 million transaction (net of cash acquired) expands MSA’s fixed detection total addressable market by approximately $500 million and aligns with the company’s ACCELERATE strategy focused on growing its detection business.

M&C TechGroup, founded in 1985, employs approximately 220 people and generates annual revenue of around $55 million. The acquisition was financed through a combination of cash and revolving credit facility at a mid-teens EBITDA multiple. Management expects the transaction to be accretive to 2025 adjusted earnings.

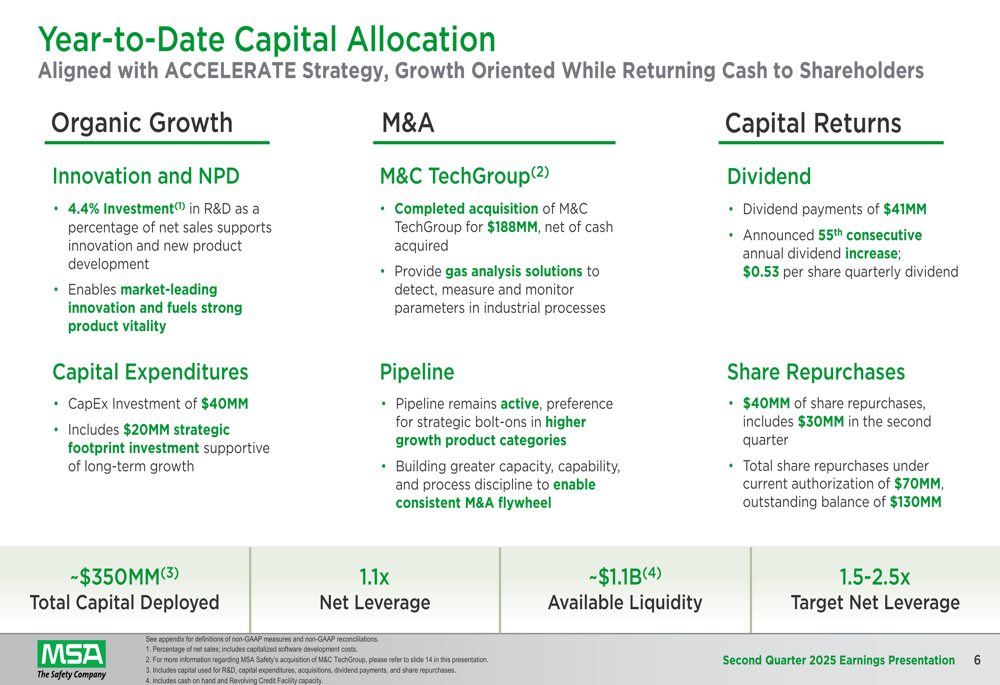

Beyond acquisitions, MSA continued to invest in organic growth initiatives, with R&D investment representing 4.4% of net sales. The company also allocated $40 million to capital expenditures year-to-date, including a $20 million strategic footprint investment to support long-term growth.

MSA’s capital allocation strategy remains balanced, with $41 million in dividend payments (marking the 55th consecutive annual increase) and $40 million in share repurchases during the first half of 2025. The company announced a quarterly dividend of $0.53 per share, continuing its long track record of returning capital to shareholders.

Forward-Looking Statements

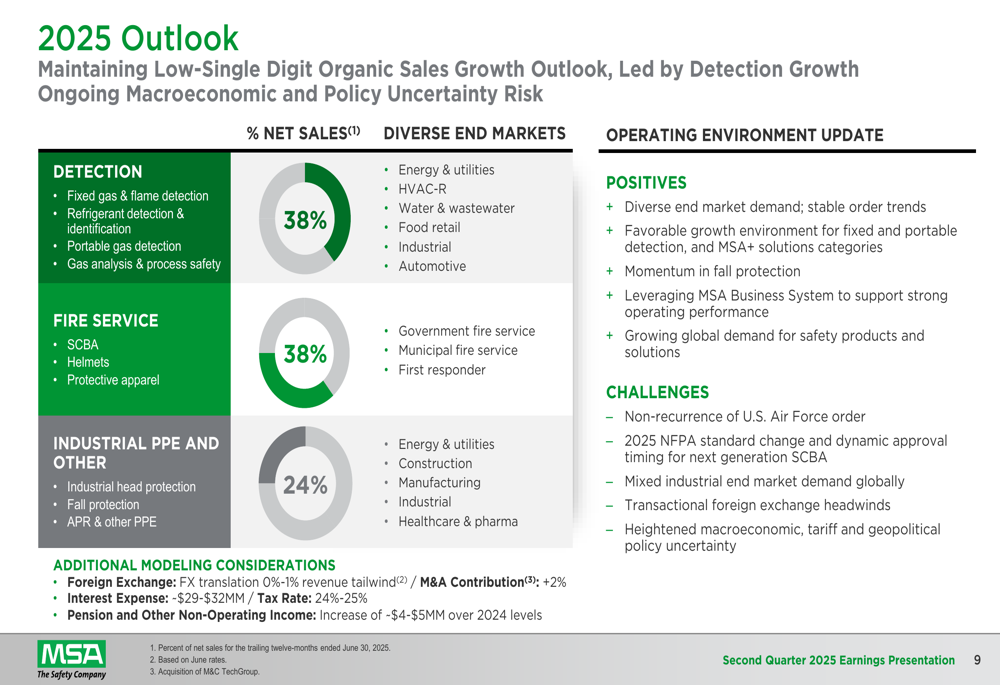

Looking ahead, MSA Safety maintained its outlook for low-single digit organic sales growth in 2025, led by continued strength in the detection segment. Management acknowledged ongoing macroeconomic uncertainty, tariff impacts, and geopolitical challenges but expressed confidence in the company’s diverse end markets and strategic positioning.

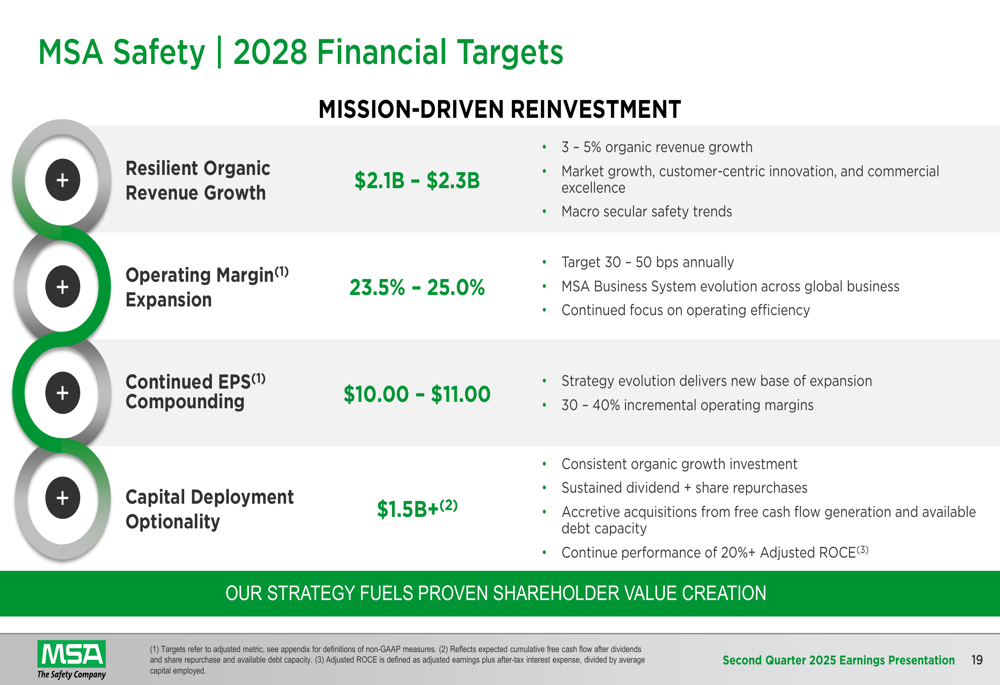

The company continues to target its previously announced 2028 financial goals, including revenue of $2.1-$2.3 billion, operating margins of 23.5-25.0%, and adjusted earnings per share of $10.00-$11.00. Management emphasized that achieving these targets would represent significant growth from current levels and provide substantial capital deployment optionality exceeding $1.5 billion.

Market Reaction & Analyst Perspectives

Despite the mixed quarterly results, MSA Safety’s stock rose 1.54% following the earnings presentation, suggesting investors may have anticipated worse outcomes or were encouraged by the company’s strategic direction and maintained outlook. The stock has been performing well in 2025, approaching its 52-week high of $187.41.

This reaction aligns with the company’s performance in the first quarter, when MSA exceeded analyst expectations with earnings per share of $1.68 and revenue of $421 million. While second-quarter profitability declined year-over-year, the company’s strategic acquisition and ongoing pricing actions to counter tariff impacts appear to have resonated positively with investors.

MSA’s focus on worker safety continues to be a cornerstone of its market positioning, with the company highlighting its protection of over 40 million workers globally in its recently published 2024 Impact Report. This mission-driven approach, combined with its diversified product portfolio and end markets, positions MSA to navigate the current challenging environment while pursuing long-term growth opportunities in high-margin segments like detection and fall protection.

The company’s ability to maintain its dividend increase streak for 55 consecutive years further underscores its financial resilience and commitment to shareholder returns, even amid temporary margin pressures and increased investments in strategic growth initiatives.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.