Robinhood shares gain on Q2 beat, as user and crypto growth accelerate

Introduction & Market Context

MSCI Inc (NYSE:MSCI) released its first quarter 2025 earnings presentation on April 22, 2025, showcasing solid growth across its key business segments. The financial data and analytics provider reported a 9.7% year-over-year increase in operating revenues, reaching $745.8 million, while delivering double-digit growth in operating income and adjusted earnings per share.

Despite the strong results, MSCI’s stock was down 1.5% in trading following the announcement, with the share price at $533.48, well below its 52-week high of $642.45. This follows a pattern seen in the previous quarter when the stock fell 5.45% despite beating earnings expectations, suggesting investors may be setting higher expectations for the company’s performance.

Quarterly Performance Highlights

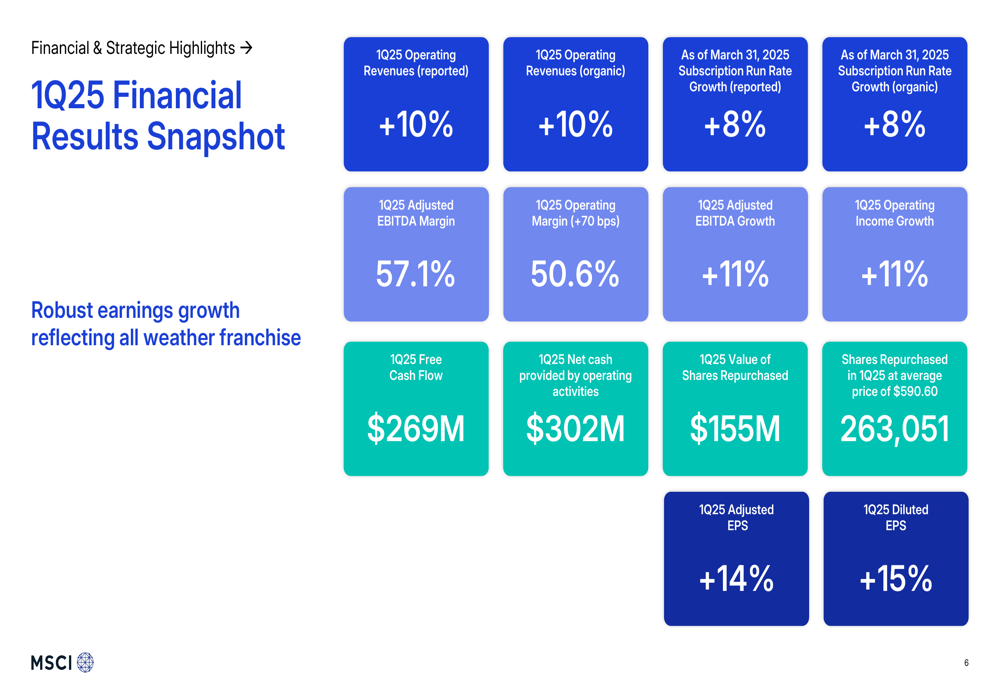

MSCI delivered robust financial results in Q1 2025, demonstrating the resilience of its diversified business model. The company reported operating revenues of $745.8 million, up 9.7% year-over-year, with organic growth of 10%. Operating income increased by 11.1% to $377 million, while net income grew 12.8% to $288.6 million.

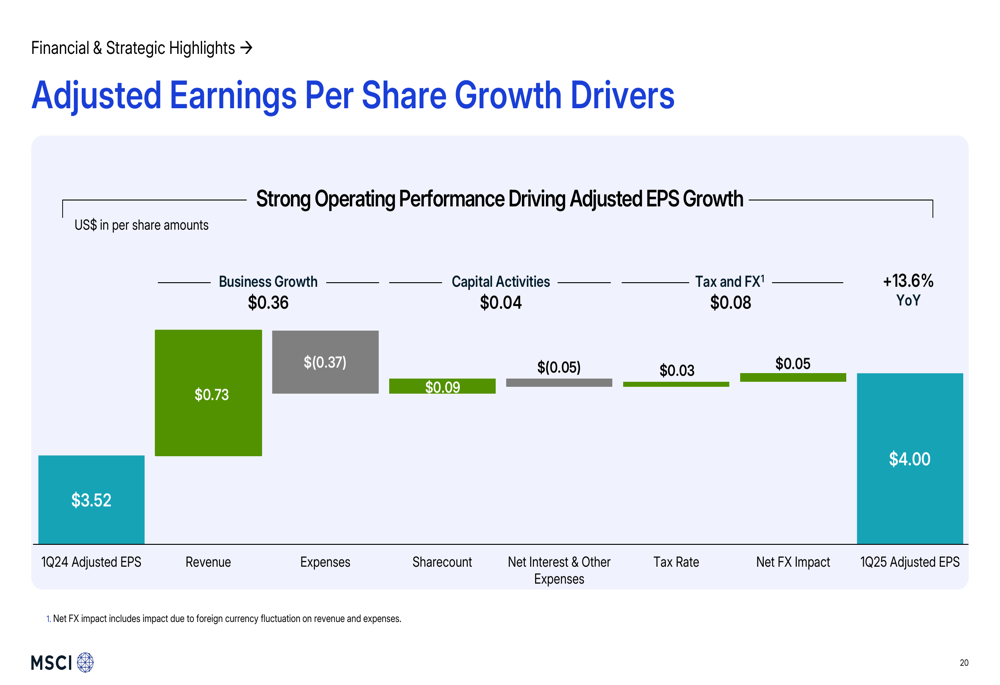

As shown in the following financial results snapshot, the company achieved significant growth across key metrics, including a 13.6% increase in adjusted EPS to $4.00 and an 11% rise in adjusted EBITDA to $425.6 million:

The company’s adjusted EBITDA margin expanded to 57.1%, up from 56.4% in the same period last year, while operating margin improved to 50.6% from 49.9%. MSCI generated $269 million in free cash flow and returned $155 million to shareholders through share repurchases, buying back 263,051 shares at an average price of $590.60.

Strategic Initiatives

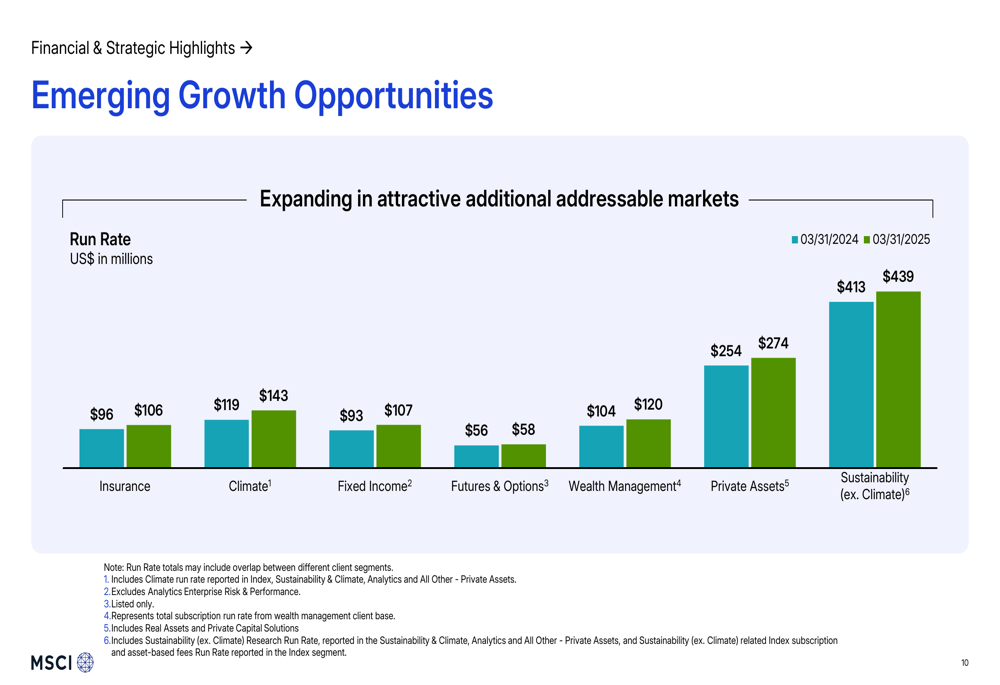

MSCI continues to expand beyond its core index business into high-growth areas, with particular focus on climate analytics, fixed income, and wealth management solutions. The company’s strategic investments in these emerging opportunities are showing promising results, as illustrated in the following chart:

Climate-related run rate grew by 20% year-over-year to $143 million, while fixed income increased by 15% to $107 million. The wealth management segment saw 15% growth to $120 million, and private assets expanded by 8% to $274 million. These emerging areas represent significant growth vectors for MSCI as it diversifies its revenue streams.

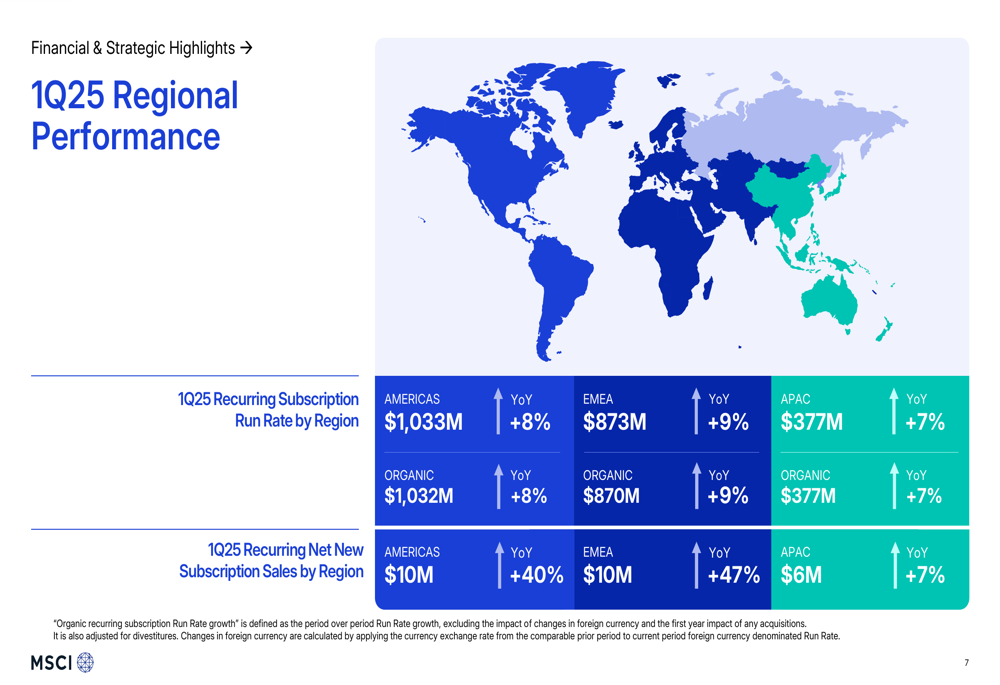

The company’s global footprint continues to strengthen, with balanced growth across all major regions. As shown in the regional performance breakdown, MSCI achieved solid subscription run rate growth in the Americas (+8%), EMEA (+9%), and APAC (+7%):

Detailed Financial Analysis

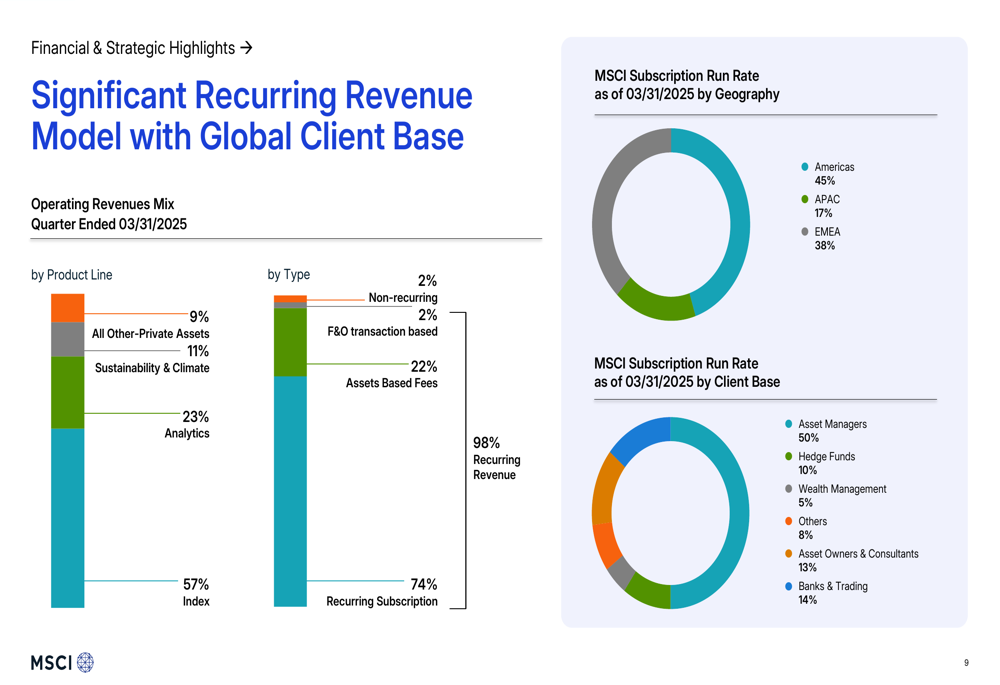

MSCI’s business model remains heavily weighted toward recurring subscription revenues, which account for 74% of total operating revenues. Asset-based fees contribute 22%, while futures & options and non-recurring revenues each represent 2% of the total. This high proportion of recurring revenue provides stability and predictability to MSCI’s financial performance.

The following chart illustrates MSCI’s revenue mix by product line and type, along with the geographic and client distribution of its subscription run rate:

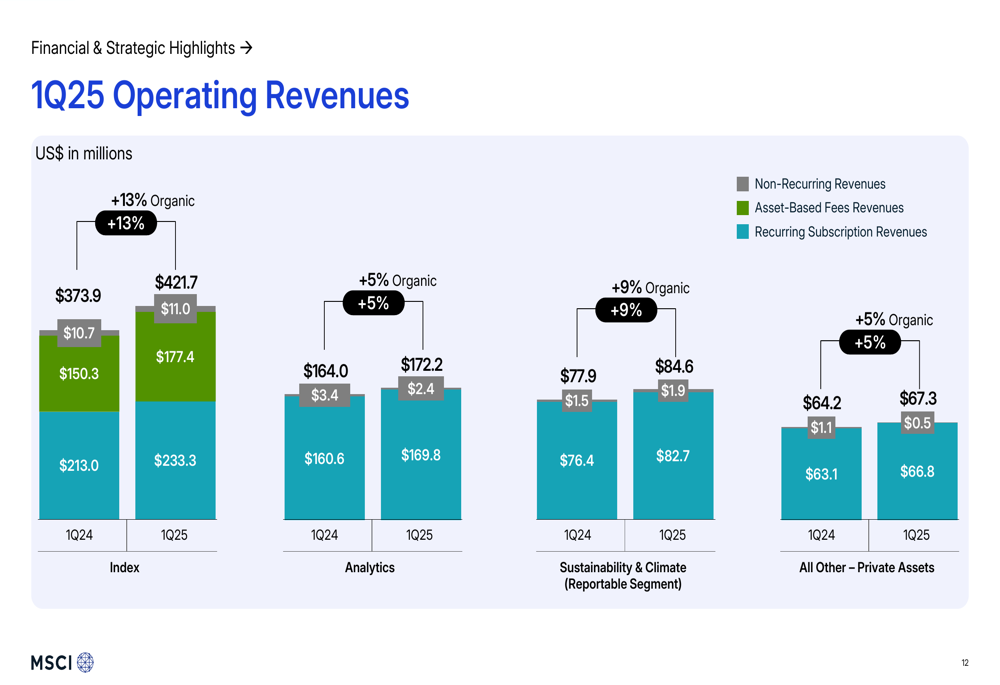

Breaking down performance by segment, the Index business remains MSCI’s largest revenue contributor at 57% of total operating revenues. The segment delivered 10% organic growth in subscription run rate, reaching $1.65 billion. Analytics, representing 23% of revenues, grew its subscription run rate by 7% to $708 million, while Sustainability & Climate (11% of revenues) increased by 10% to $352 million.

The following chart provides a detailed view of operating revenues by segment:

The drivers behind MSCI’s 13.6% adjusted EPS growth provide insight into the company’s operational efficiency. As shown in the following breakdown, business growth contributed $0.36 to the EPS increase, while capital activities added $0.04 and tax and FX benefits provided $0.08, partially offset by $0.37 in increased expenses:

Forward-Looking Statements

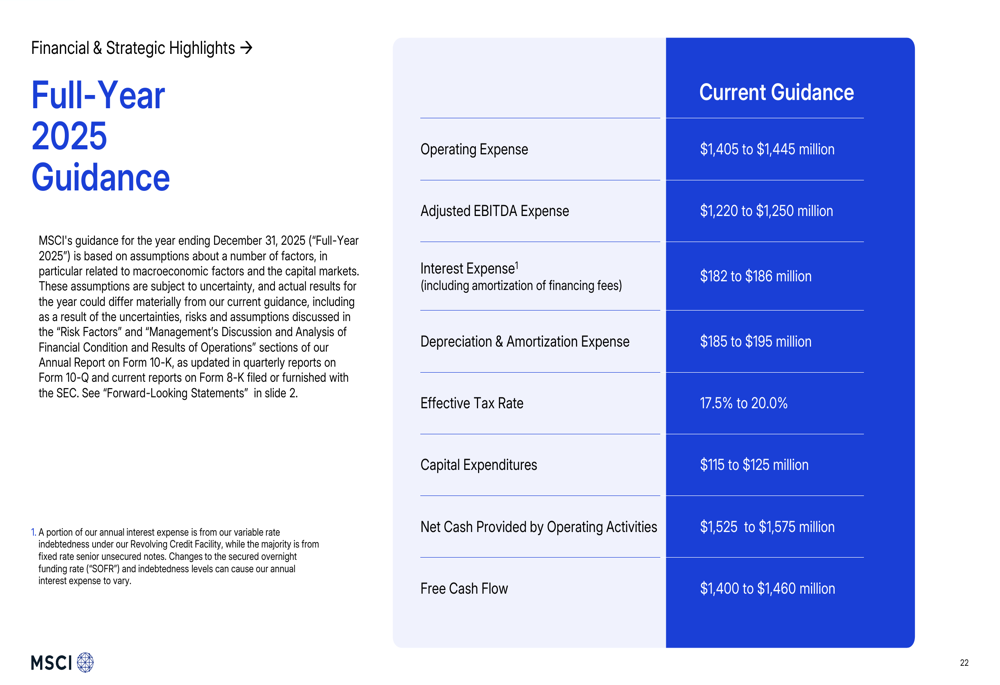

Looking ahead, MSCI provided guidance for full-year 2025, projecting operating expenses between $1,405 million and $1,445 million, and adjusted EBITDA expenses between $1,220 million and $1,250 million. The company expects to generate net cash from operating activities of $1,525 million to $1,575 million and free cash flow of $1,400 million to $1,460 million.

The detailed guidance for 2025 is outlined in the following slide:

Beyond 2025, MSCI has set ambitious long-term targets, aiming for low double-digit revenue growth and high 50s adjusted EBITDA margins. The company expects its Index segment to deliver high single-digit to low double-digit revenue growth, while Analytics is targeted for mid to high single-digit growth.

The company’s long-term strategic vision is summarized in the following targets:

MSCI’s strong balance sheet provides flexibility for future investments and shareholder returns. As of March 31, 2025, the company had $361 million in cash and $4,547 million in total debt, resulting in a net debt to LTM adjusted EBITDA ratio of 2.4x. This financial position supports MSCI’s capital allocation strategy, which includes strategic investments, share repurchases, and dividend payments.

In Q1 2025, MSCI returned $295.1 million to shareholders through share repurchases of $155.4 million and quarterly dividends of $139.7 million, demonstrating its commitment to delivering shareholder value while investing in future growth opportunities.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.