CrowdStrike partners with Salesforce to secure AI agents and applications

Mueller Water Products, Inc. (NYSE:MWA) delivered record financial results in its third quarter of fiscal 2025, according to the company’s earnings presentation released on August 5, 2025. The water infrastructure solutions provider reported strong growth across key metrics and raised its full-year guidance, despite facing tariff headwinds.

Quarterly Performance Highlights

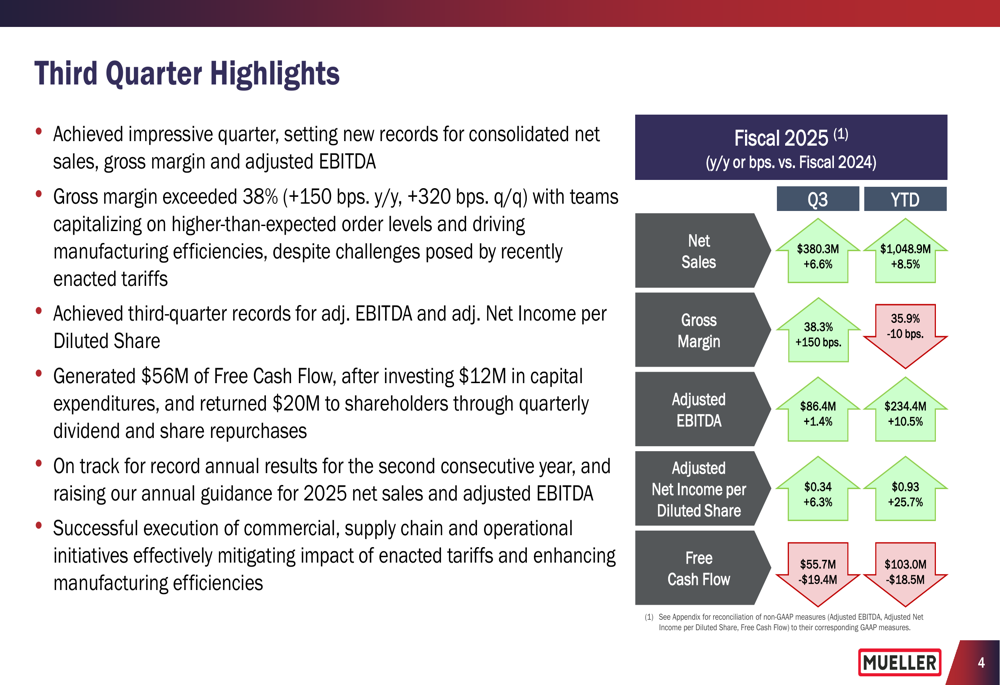

Mueller Water Products achieved record consolidated net sales of $380.3 million in Q3 FY2025, representing a 6.6% increase compared to the same period last year. The company also posted record gross margin of 38.3%, up 150 basis points year-over-year and 320 basis points sequentially from Q2.

As shown in the following quarterly results summary:

Adjusted EBITDA reached $86.4 million, a 1.4% increase year-over-year, while adjusted net income per diluted share grew 6.3% to $0.34. The company generated $55.7 million in free cash flow after $12 million in capital expenditures and returned $20 million to shareholders.

"We delivered exceptional performance this quarter where we achieved third quarter records for consolidated net sales, gross margin, adjusted EBITDA and adjusted net income per share," said Marty Zakas, President and CEO, according to the presentation.

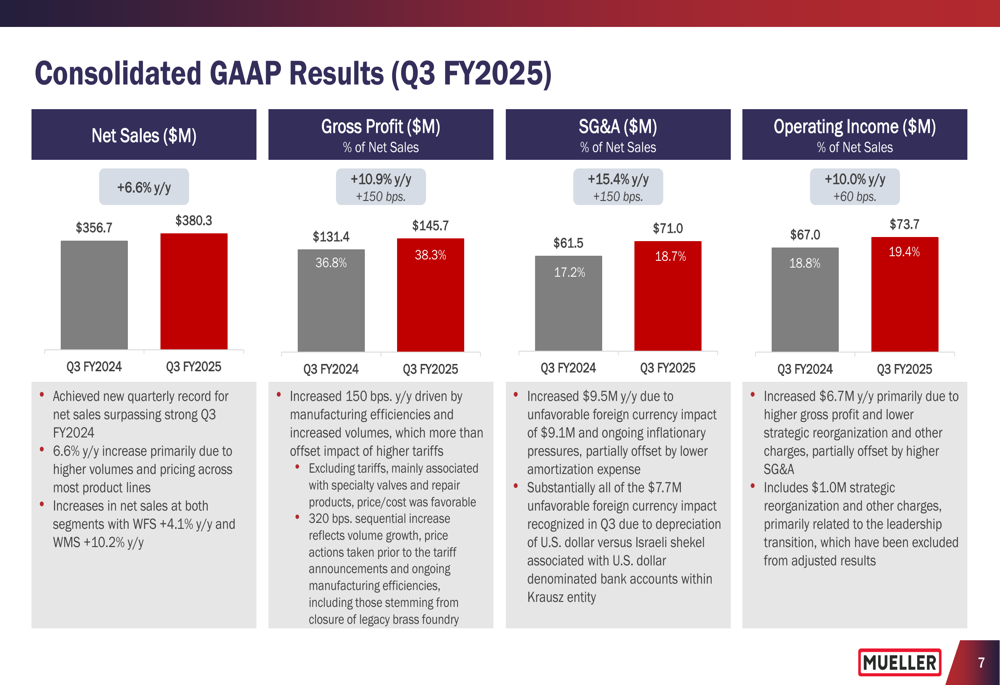

The GAAP results showed particularly strong improvement in gross profit, which increased 10.9% year-over-year to $145.7 million:

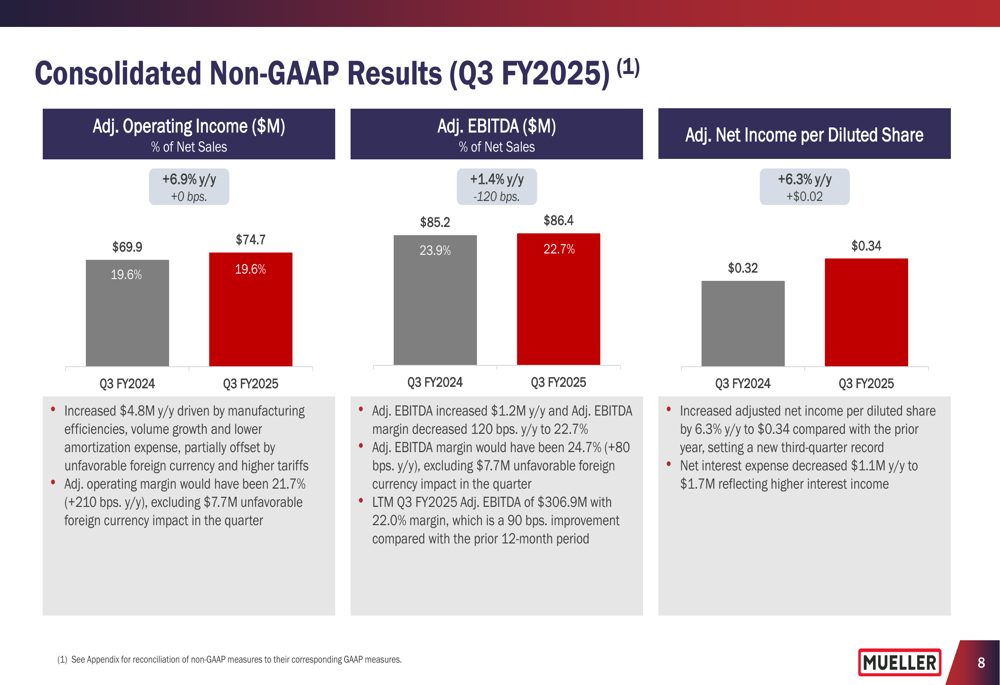

On a non-GAAP basis, adjusted operating income grew 6.9% to $74.7 million, maintaining a margin of 19.6%:

Segment Analysis

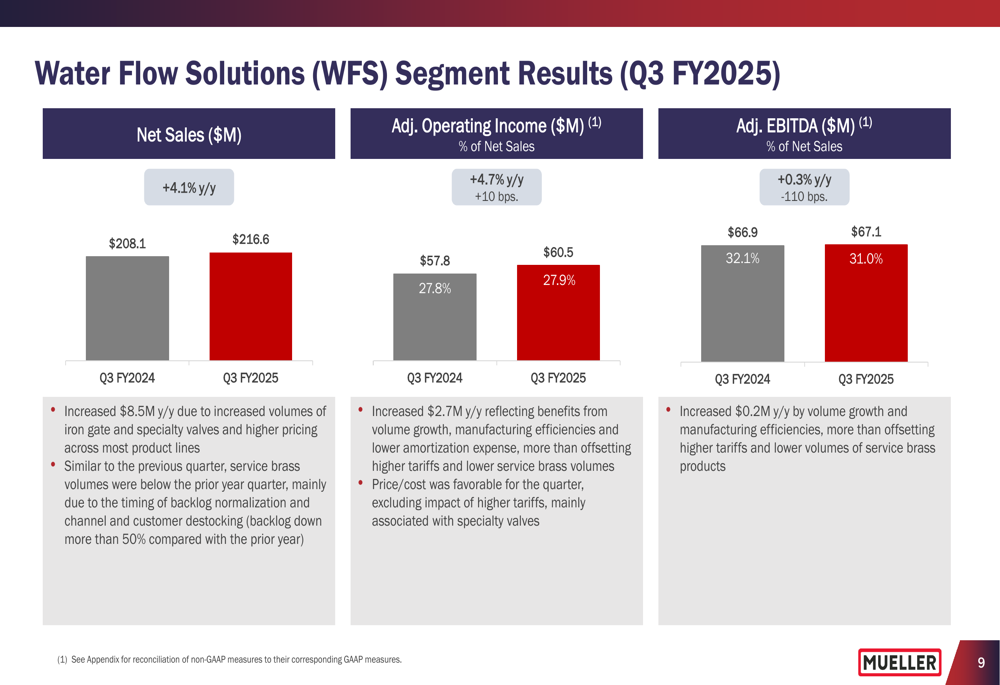

Both of Mueller’s business segments contributed to the strong quarterly performance. The Water Flow Solutions (WFS) segment, which includes the company’s fire hydrants and gate valves products, reported net sales of $216.6 million, up 4.1% year-over-year. Adjusted operating income for this segment increased 4.7% to $60.5 million, with a slight margin improvement of 10 basis points to 27.9%.

The segment results demonstrate continued demand for the company’s core infrastructure products:

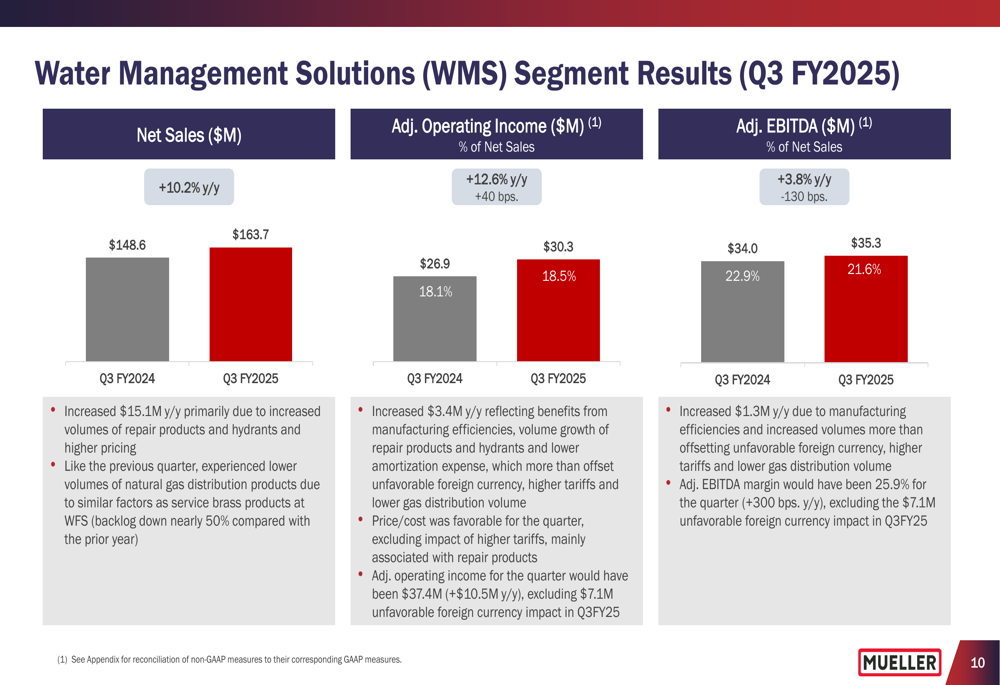

The Water Management Solutions (WMS) segment, which includes specialty valves, repair products and digital solutions, delivered even stronger growth with net sales increasing 10.2% to $163.7 million. Adjusted operating income for this segment rose 12.6% to $30.3 million, with margin expanding 40 basis points to 18.5%.

The WMS segment’s performance highlights the company’s success in higher-growth specialty products:

Tariff Mitigation Strategies

A key focus of the presentation was Mueller’s approach to managing the impact of recently enacted tariffs. The company has implemented several strategies to mitigate these challenges, including pricing actions and operational improvements.

As detailed in the tariff impact slide, Mueller has exposure to various tariff regimes affecting goods from China, Israel, and other regions:

Despite these headwinds, the company achieved record quarterly gross margin with more than 300 basis points improvement compared to Q2. Management noted that the company has implemented pricing for specialty valve and repair products in Q4 and continues to monitor the situation for additional actions as needed.

Balance Sheet Strength

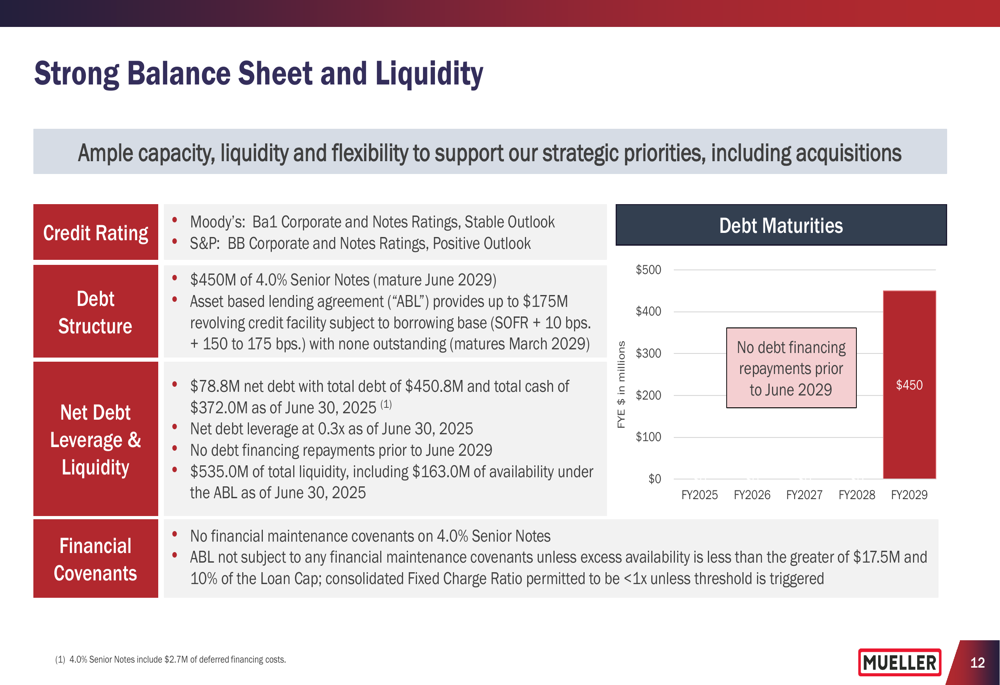

Mueller Water Products maintained a strong financial position, with $78.8 million in net debt and a low net debt leverage ratio of 0.3x. The company reported $535 million in available liquidity, providing substantial flexibility for future investments and shareholder returns.

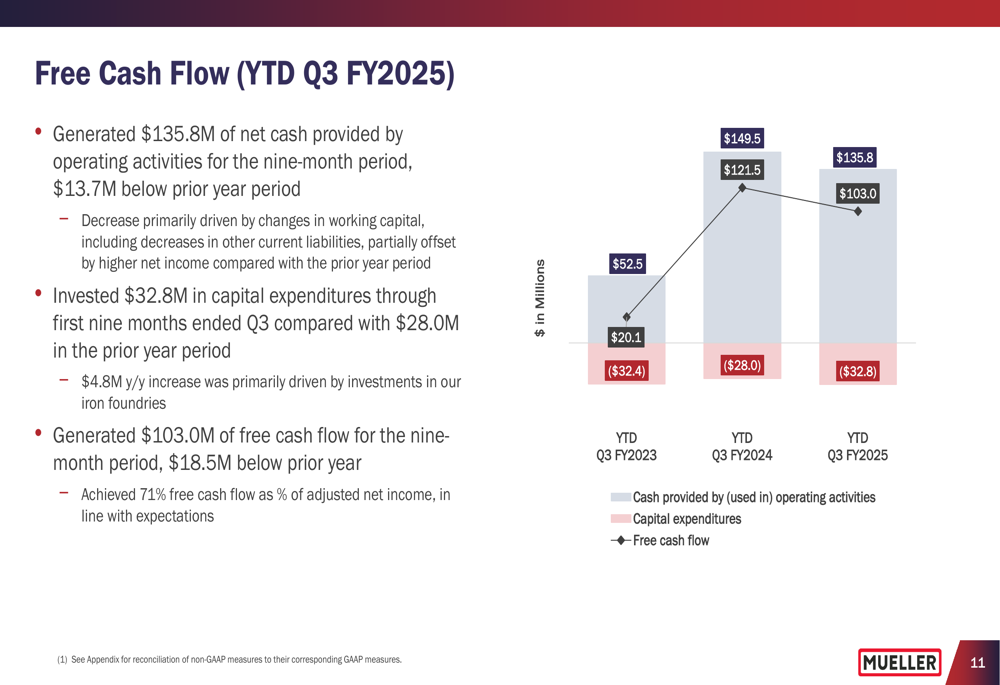

The company’s year-to-date free cash flow remained robust at $103 million, though slightly below the prior year:

The balance sheet details show a conservative financial approach with well-structured debt maturities:

ESG Initiatives

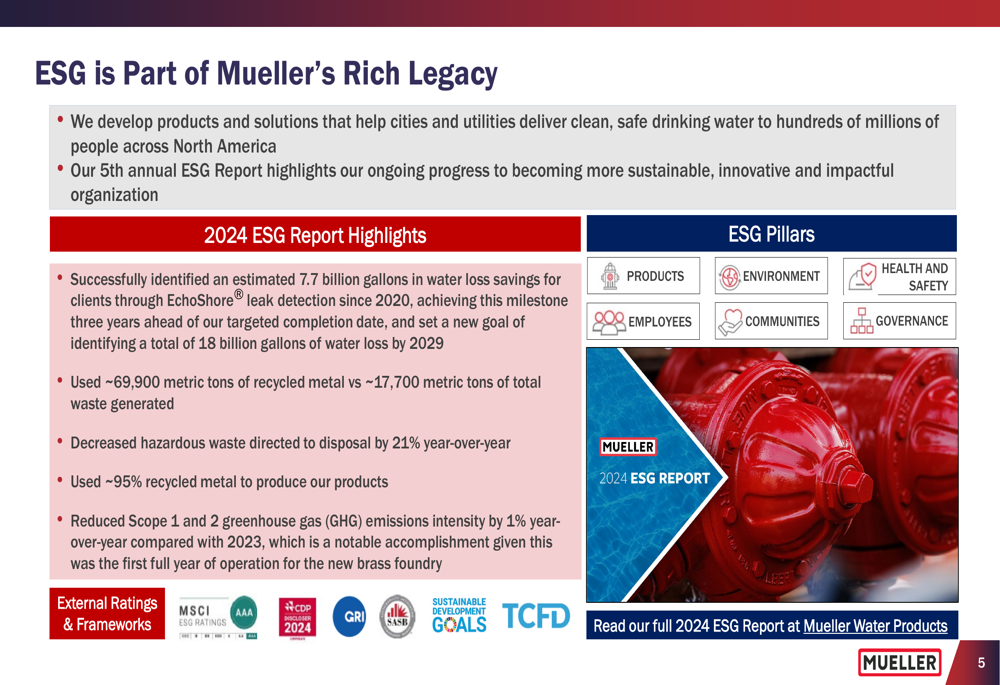

Mueller Water Products highlighted its commitment to environmental, social, and governance (ESG) factors. The company released its fifth annual ESG report, noting several achievements including identifying an estimated 7.7 billion gallons in water loss savings and using approximately 95% recycled metal in its products.

The company’s sustainability efforts are summarized in the following slide:

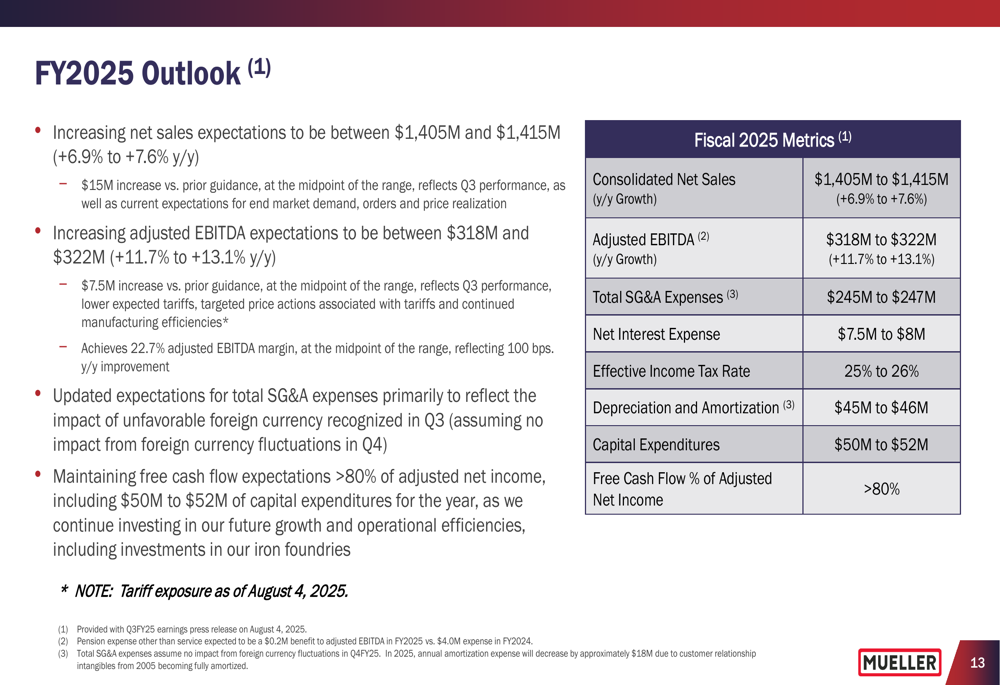

Outlook & Guidance

Based on the strong performance through the first three quarters, Mueller Water Products raised its full-year guidance for fiscal 2025. The company now expects net sales between $1,405 million and $1,415 million, up from the previous guidance. Adjusted EBITDA is projected to be between $318 million and $322 million.

The updated outlook reflects management’s confidence in continued strong execution:

Other guidance metrics include SG&A expenses of $245-247 million, net interest expense of $7.5-8 million, an effective tax rate of 25-26%, and capital expenditures of $50-52 million. The company expects free cash flow to be approximately 80% of adjusted net income.

Strategic Priorities

Mueller Water Products continues to focus on four key strategic priorities: improving operational excellence, accelerating sales growth through customer experience and innovation, fostering an inclusive culture, and increasing margins and free cash flow to support future investments.

The company’s stock closed at $23.94 on August 5, 2025, and saw a 4.64% increase in after-hours trading following the earnings release, reflecting positive investor reaction to the strong results and raised guidance.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.