Futures lower; Tesla’s much-anticipated announcement - what’s moving markets

Introduction & Market Context

Mycronic (STO:MYCR) reported a stellar first quarter for 2025, achieving record sales and EBIT figures while navigating varying performance across its divisions. The company’s stock closed at SEK 381 on April 24, 2025, showing a 1.17% increase, reflecting positive market reception to the strong quarterly results.

The presentation, delivered by President and CEO Anders Lindqvist and CFO Pierre Brorsson, highlighted significant growth metrics while acknowledging challenges in certain markets and revising the company’s outlook for the remainder of 2025.

Quarterly Performance Highlights

Mycronic reported exceptional top-line growth in Q1 2025, with order intake increasing 25% to SEK 2,058 million compared to SEK 1,645 million in the same period last year. Net sales reached a record SEK 2,142 million, representing a 27% increase from Q1 2024’s SEK 1,692 million.

The company achieved its strongest EBIT ever at SEK 775 million, up from SEK 599 million in Q1 2024, with an improved EBIT margin of 36% compared to 35% in the prior year. The order backlog stood at SEK 4,617 million, providing solid visibility for future quarters.

As shown in the following summary of Q1 performance:

The quarter also saw strategic expansion through acquisitions, with Global Technologies acquiring Hprobe during the quarter and RoBAT after the quarter closed.

Detailed Financial Analysis

Mycronic’s financial performance showed strength across multiple metrics, with aftermarket revenue reaching a record SEK 531 million. The company’s EBIT bridge reveals that volume effects contributed significantly to the EBIT growth, adding SEK 261 million, while improved gross margins added another SEK 75 million.

The following EBIT bridge illustrates the key factors driving the 29% EBIT increase:

Breaking down the EBIT contribution by division reveals the significant impact of Pattern Generators, which added SEK 209 million to the overall EBIT growth. Global Technologies contributed SEK 24 million and High Volume added SEK 4 million, while High Flex (NASDAQ:FLEX) detracted SEK 15 million and group functions accounted for a SEK 46 million reduction.

The divisional EBIT contribution breakdown is illustrated here:

Despite the strong operational performance, cash flow from operations declined to SEK 241 million from SEK 737 million in Q1 2024, primarily due to a significant working capital increase. Cash flow before changes in working capital actually improved to SEK 686 million from SEK 610 million, but the SEK 444 million increase in working capital reversed this positive trend.

The cash flow dynamics are detailed in the following chart:

Divisional Performance

Mycronic’s divisions showed contrasting results, with Pattern Generators delivering exceptional performance while High Flex faced significant challenges.

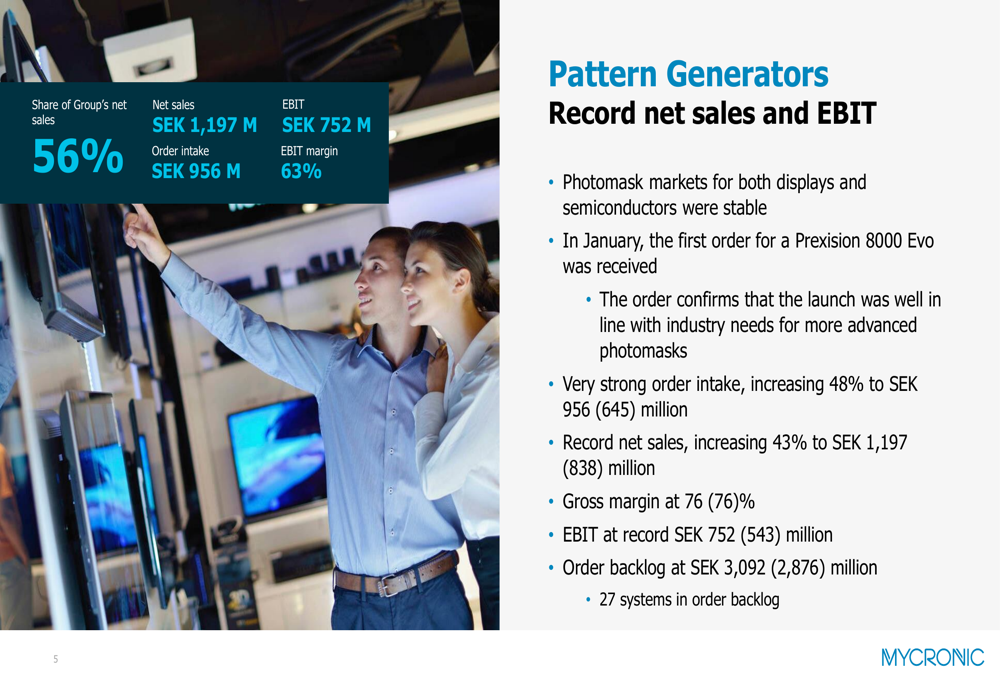

The Pattern Generators division, which accounted for 56% of the group’s net sales, reported record results with net sales increasing 43% to SEK 1,197 million and EBIT reaching a record SEK 752 million. The division maintained its impressive 76% gross margin and secured its first order for the Prexision 8000 Evo system. With 27 systems in the order backlog totaling SEK 3,092 million, this division remains the company’s primary growth driver.

The Pattern Generators performance is summarized in this slide:

In stark contrast, the High Flex division struggled with very weak demand in Europe, its largest geographical market. Order intake declined 12% to SEK 295 million, while net sales decreased slightly by 1% to SEK 292 million. Despite maintaining a gross margin of 37%, the division reported a negative EBIT of SEK 13 million, down from a positive SEK 1 million in Q1 2024.

The High Volume division showed strength, particularly in the Chinese domestic market, with order intake rising 42% to a record SEK 553 million and net sales increasing 6% to SEK 330 million. The division improved its gross margin to 43% and delivered an EBIT of SEK 59 million, representing an 18% EBIT margin.

Global Technologies reported mixed results with a slowdown in the Die Bonding business line but overall net sales growth of 31% to SEK 323 million. The division improved its gross margin to 46% and increased EBIT to SEK 54 million, representing a 17% EBIT margin.

Strategic Initiatives & Forward-Looking Statements

During Q1, Mycronic completed the acquisition of Hprobe, strengthening its Global Technologies division. The company also announced the acquisition of RoBAT, which was completed after the quarter ended, further expanding its technological capabilities.

The company launched sustainability initiatives during the quarter and completed its Sustainability Report for 2024, with plans to review reporting processes in 2025.

Despite the strong Q1 performance, Mycronic revised its outlook for 2025, projecting net sales of SEK 7.0-7.5 billion. This revision reflects increased uncertainty in the market, particularly related to tariffs.

The company noted that approximately 5% of its net sales are impacted by high tariffs between the US and China, with an additional 5-10% affected by US base tariffs. Mycronic stated that it does not intend to bear the cost of these tariffs, suggesting potential price adjustments or supply chain modifications may be necessary.

Market Context

Mycronic operates in a generally positive market environment, with the global electronics industry expected to grow 7.4% in 2025 after 4.9% growth in 2024. The semiconductor industry, which grew 19.2% in 2024, is forecast to grow 13.3% in 2025.

The display market, critical for Mycronic’s Pattern Generators division, grew 13.0% in 2024 and is expected to grow 6.1% in 2025. The display photomasks market grew 2.0% in 2024, while the semiconductor photomasks market grew 15.0%.

However, the company noted that all market forecasts were made before recent tariff announcements, which could potentially impact the outlook for the remainder of 2025.

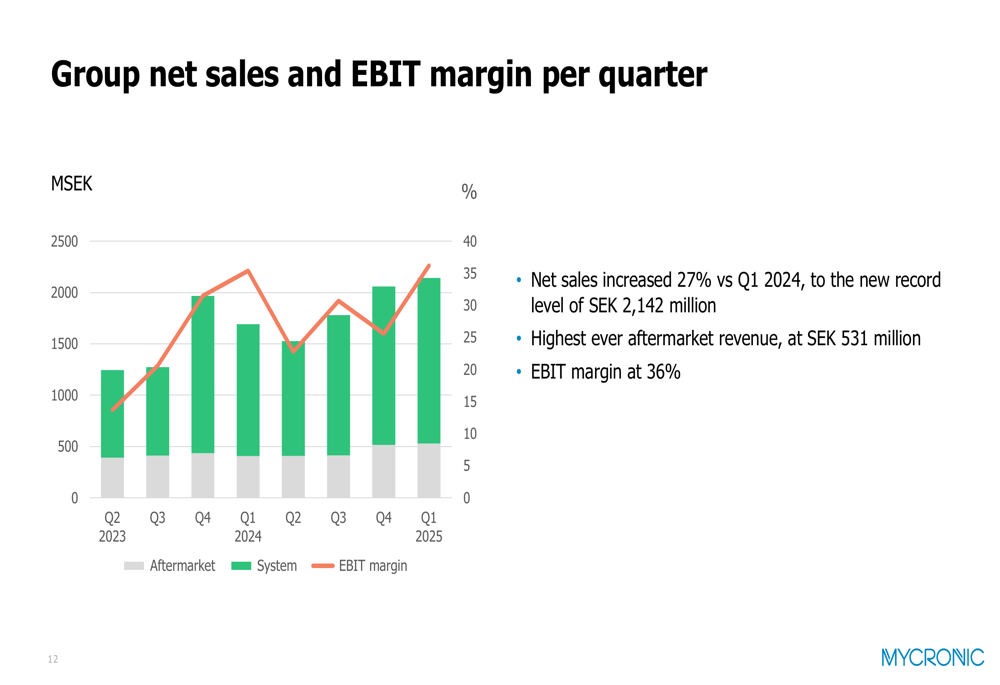

The quarterly net sales and EBIT margin trends shown below illustrate Mycronic’s consistent growth trajectory:

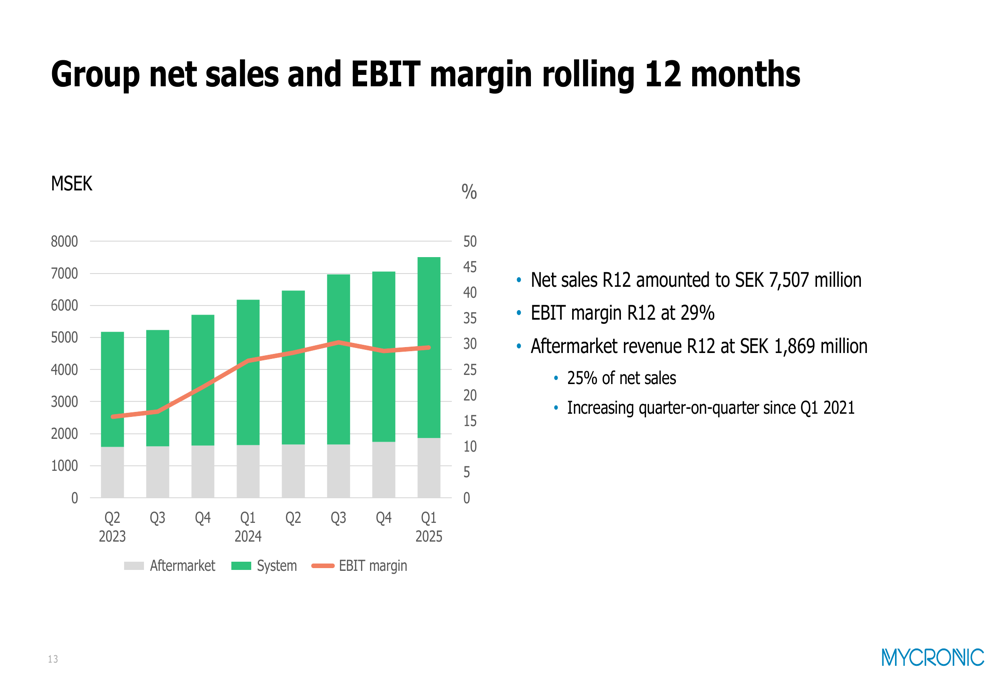

Looking at the rolling 12-month performance, Mycronic has achieved net sales of SEK 7,507 million with an EBIT margin of 29%. Aftermarket revenue for the rolling 12 months reached SEK 1,869 million, representing 25% of net sales and showing consistent quarter-on-quarter growth since Q1 2021.

Mycronic’s Q1 2025 results demonstrate the company’s ability to deliver strong performance in a complex market environment, though challenges in certain divisions and external factors like tariffs may impact future quarters. The revised outlook suggests a cautious approach despite the record-breaking start to the year.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.