TSX drops after Canadian index edges higher in prior session

Introduction & Market Context

Mycronic publ AB (STO:MYCR) reported mixed third-quarter 2025 results on October 23, featuring strong order intake growth despite declining sales and profitability. The company’s stock responded positively, rising 3.87% to SEK 205.50, as investors focused on the robust order backlog and future growth potential rather than near-term challenges.

The Swedish electronics equipment manufacturer operates in a growing global electronics market, which is forecast to expand by 7.9% in 2025 to reach $2,756 billion. Mycronic’s performance varied significantly across its four divisions, with Pattern Generators and Global Technologies driving the substantial order intake growth.

Quarterly Performance Highlights

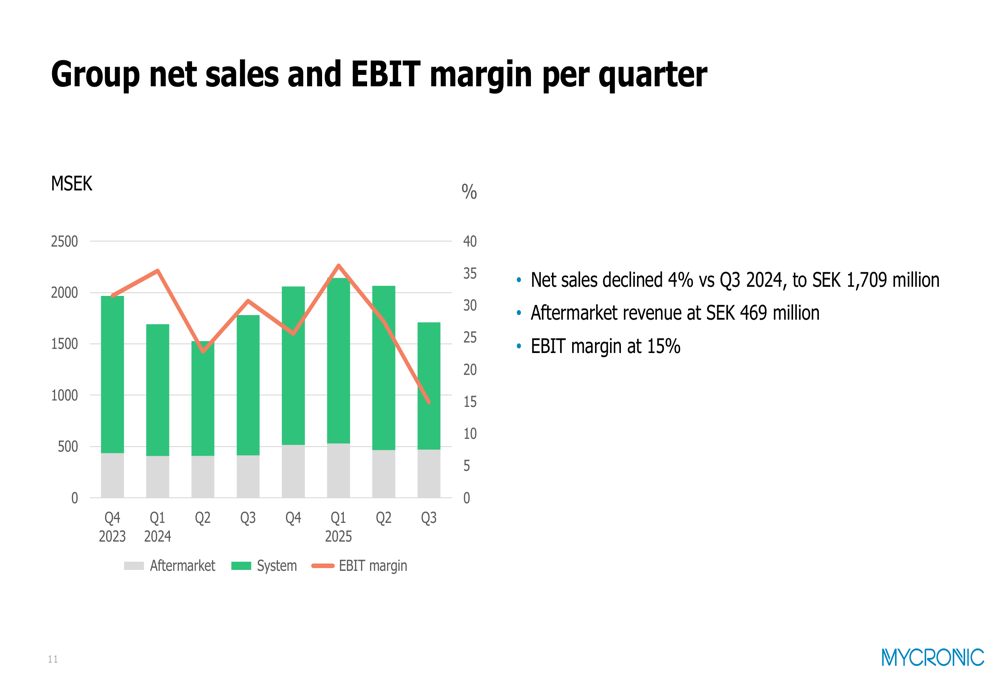

Mycronic reported a 67% year-over-year increase in order intake to SEK 2,431 million for Q3 2025, while net sales declined 4% to SEK 1,709 million. The company’s EBIT fell to SEK 255 million from SEK 547 million in the same period last year, resulting in an EBIT margin of 15% compared to 31% in Q3 2024.

As shown in the following quarterly performance overview:

The company’s order backlog increased to SEK 4,763 million, up from SEK 4,379 million a year earlier, providing solid revenue visibility for coming quarters. Aftermarket revenue reached SEK 469 million, representing approximately 25% of total net sales.

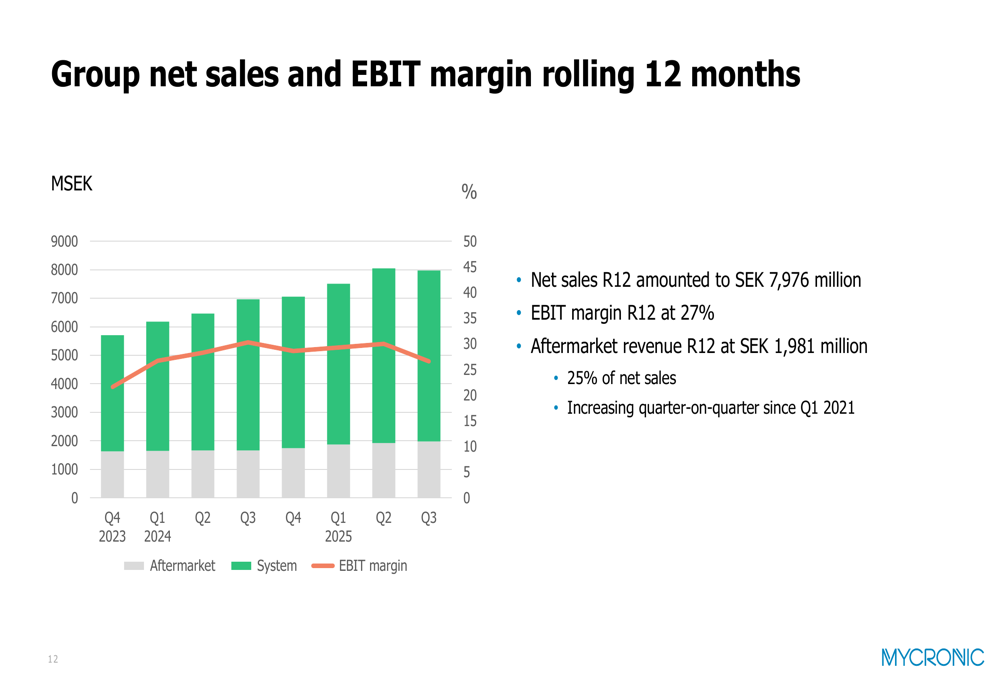

The quarterly net sales and EBIT margin trend illustrates the company’s recent performance trajectory:

Detailed Financial Analysis

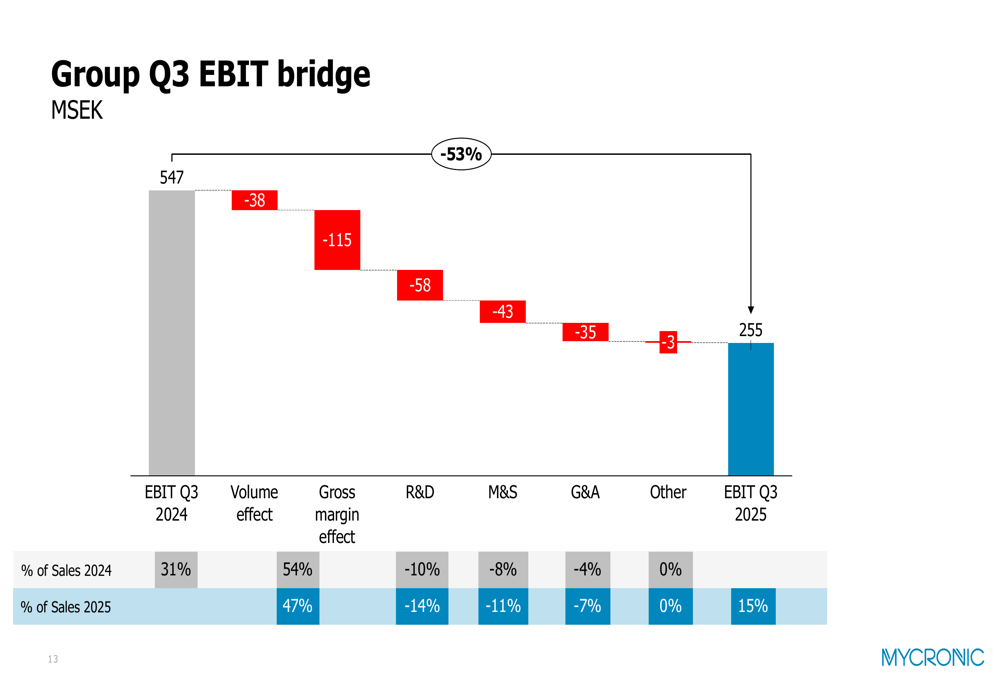

Mycronic’s EBIT decline from SEK 547 million in Q3 2024 to SEK 255 million in Q3 2025 was driven by several factors, as illustrated in this EBIT bridge:

The primary contributors to the EBIT reduction were a negative gross margin effect of SEK 115 million and increased operating expenses across R&D (SEK 58 million), marketing and sales (SEK 43 million), and general and administrative functions (SEK 35 million).

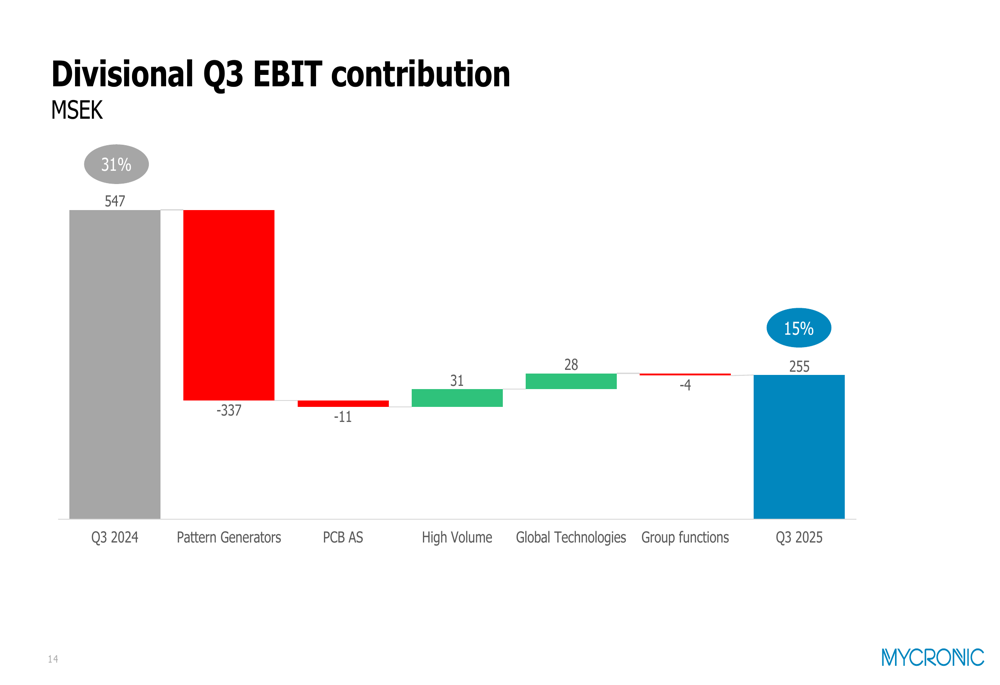

Division performance varied significantly, with Pattern Generators experiencing the largest negative impact on group EBIT:

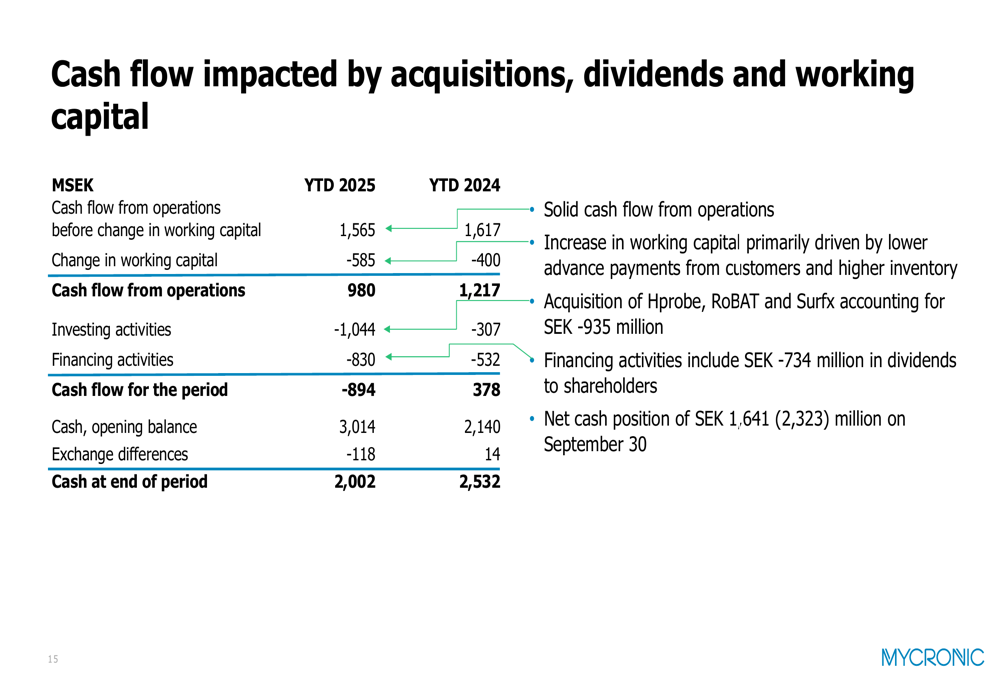

Cash flow was impacted by acquisitions, dividends, and working capital changes. While cash flow from operations before working capital changes remained solid at SEK 1,565 million year-to-date, the company’s cash position decreased to SEK 2,002 million from SEK 2,532 million a year earlier, primarily due to acquisition activities totaling SEK 935 million and dividend payments of SEK 734 million.

Competitive Industry Position

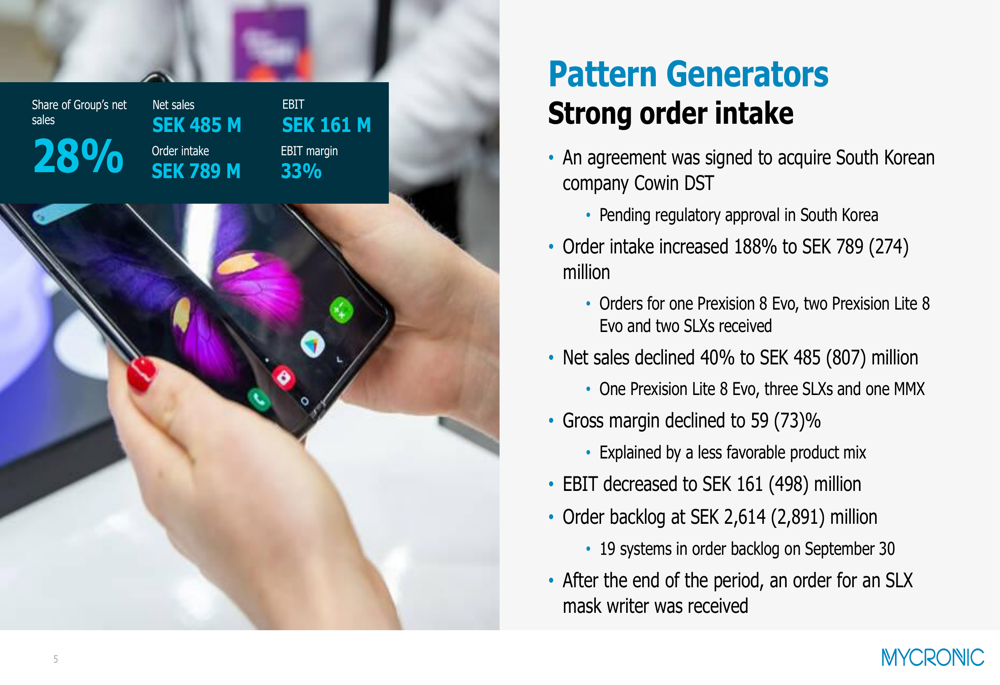

Mycronic’s performance reflects both company-specific factors and broader industry trends. The Pattern Generators division, which accounts for 28% of group sales, saw order intake surge 188% to SEK 789 million but experienced a 40% decline in net sales to SEK 485 million. This division secured orders for one Prexision 8 Evo, two Prexision Lite 8 Evo, and two SLX systems during the quarter.

The High Volume division, representing 29% of group sales, delivered healthy growth with net sales increasing 49% to SEK 499 million and EBIT rising to SEK 79 million. The division noted some weakening in the Chinese consumer electronics industry as customers front-loaded investments to the first half of the year, while markets outside China, such as South Korea and Southeast Asia, showed positive development.

Global Technologies posted the strongest overall performance with order intake increasing 94% to SEK 797 million and net sales rising 47% to SEK 416 million. The division’s gross margin improved significantly to 52% from 35% a year earlier.

PCB Assembly Solutions faced challenges with net sales declining 11% to SEK 314 million, though order intake rose 5% to SEK 405 million. The division successfully relocated production from Täby to new premises in Kista, Stockholm, during the quarter.

Strategic Initiatives

Mycronic continued its strategic expansion with the Pattern Generators division signing an agreement to acquire South Korean company Cowin DST, pending regulatory approval. This follows recent acquisitions of Hprobe, RoBAT, and Surfx, which contributed SEK 112 million to Global Technologies’ net sales in the quarter.

The company also reported progress on sustainability initiatives, with 95% of high-risk suppliers and 60% of all direct material suppliers having signed Mycronic’s Code of Conduct, improving from 90% and 49%, respectively, in 2024.

Forward-Looking Statements

Mycronic confirmed its 2025 outlook, projecting net sales of SEK 7.5 billion. The company’s rolling 12-month performance shows net sales of SEK 7,976 million with an EBIT margin of 27%, providing a foundation for achieving the full-year target:

Market forecasts support Mycronic’s growth outlook, with the semiconductor industry expected to grow 13.1% in 2025 to reach $710 billion, while the display market is forecast to grow 3.2% to $139 billion. The photomask market, critical for Mycronic’s Pattern Generators division, is expected to grow 4.9% in 2025.

The OLED display segment, where Mycronic holds a strong position with its mask writers, continues to show promising growth. The transition to OLED displays is expected to drive photomask demand at approximately double the rate of the overall photomask market growth.

Despite near-term challenges in certain divisions and markets, Mycronic’s strong order intake and growing backlog position the company to capitalize on favorable long-term industry trends in electronics manufacturing, semiconductor production, and advanced displays.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.