ReElement Technologies stock soars after securing $1.4B government deal

Introduction & Market Context

Myers Industries, Inc. (NYSE:MYE) presented its third-quarter 2025 results on October 30, 2025, revealing modest growth amid mixed segment performance. The company reported adjusted earnings per share of $0.26, which represents a 4% year-over-year increase but fell short of analyst expectations of $0.28. Following the earnings release, Myers Industries’ stock showed minimal movement, with a slight increase of 0.23% to $17.38.

The industrial manufacturer continues to navigate varying demand conditions across its end markets, with infrastructure and industrial growth helping to offset weaknesses in vehicle, consumer, and automotive aftermarket segments. The company’s ongoing "Focused Transformation" strategy appears to be yielding some positive results in profitability and cash flow generation, despite the earnings miss.

Quarterly Performance Highlights

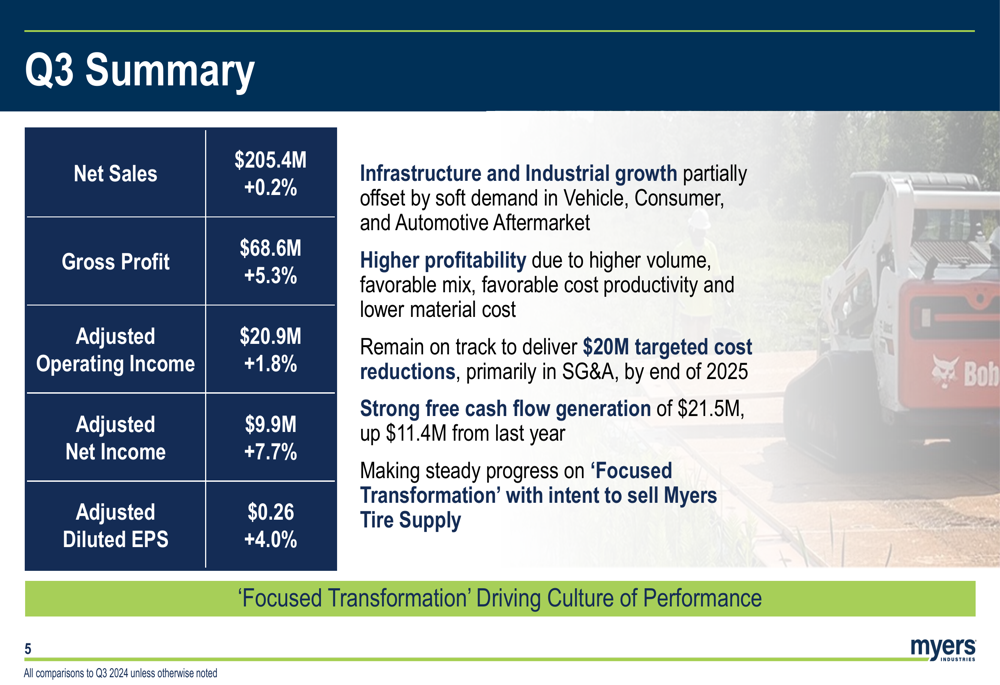

Myers Industries reported Q3 2025 net sales of $205.4 million, representing a marginal increase of 0.2% compared to the same period last year. While this figure slightly missed the expected $206.4 million, the company achieved more substantial improvements in profitability metrics. Adjusted gross profit increased by 5.3% to $68.6 million, with gross margin expanding by 150 basis points to 33.9%.

As shown in the following financial performance summary:

The company’s adjusted operating income grew by 1.8% to $20.9 million, while adjusted net income increased by 7.7% to $9.9 million. These improvements reflect the company’s success in implementing cost reduction initiatives and favorable mix shifts, despite relatively flat sales.

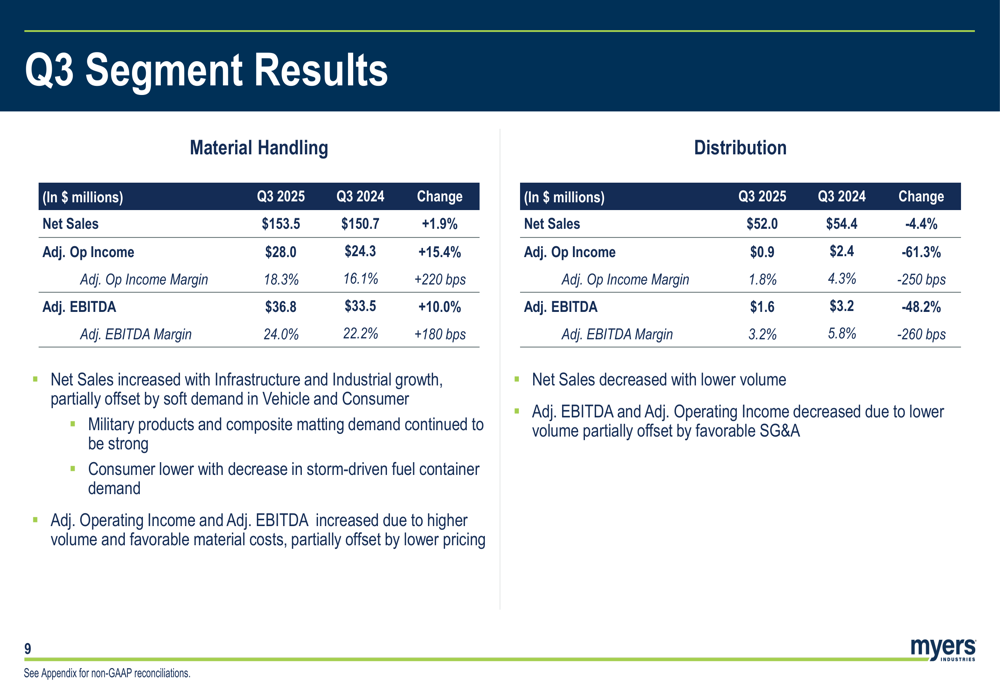

Segment performance revealed a stark contrast between the company’s two business units:

The Material Handling segment, which represents 75% of total sales, delivered net sales of $153.5 million, up 1.9% year-over-year. More impressively, the segment’s adjusted operating income surged 15.4% to $28.0 million, and adjusted EBITDA increased by 10.0% to $36.8 million. This growth was primarily driven by increased demand in infrastructure and industrial markets.

In contrast, the Distribution segment, accounting for 25% of sales, experienced a 4.4% decline in net sales to $52.0 million. More concerning was the 61.3% drop in adjusted operating income to $0.9 million and a 48.2% decrease in adjusted EBITDA to $1.6 million. These results reflect ongoing challenges in the automotive aftermarket, which have prompted strategic reassessment of this business unit.

Strategic Initiatives

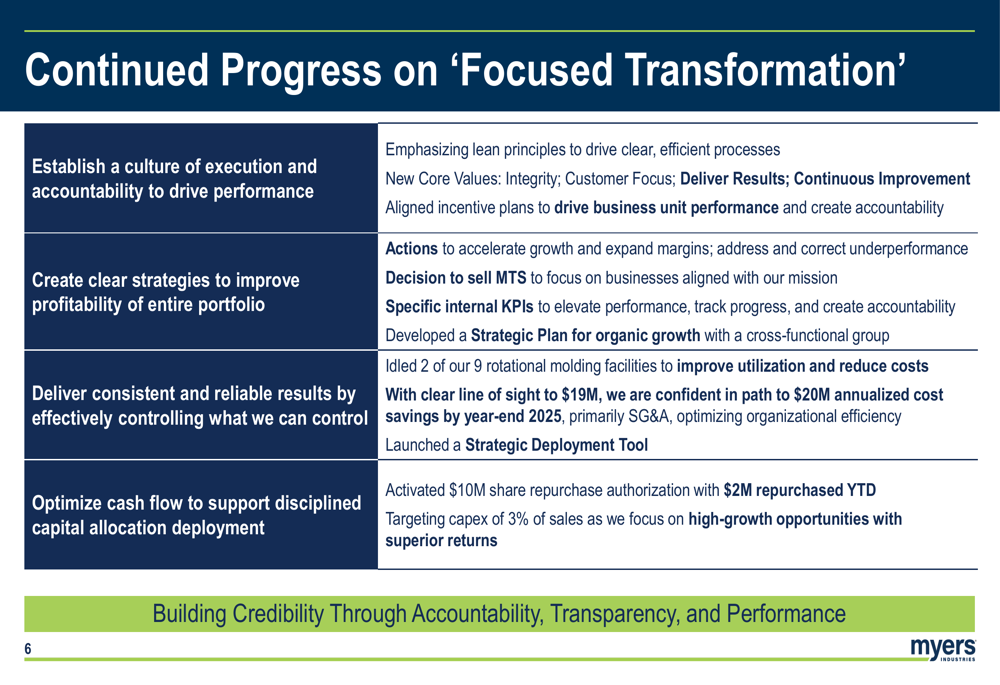

Myers Industries continues to advance its "Focused Transformation" strategy, which focuses on establishing a culture of execution and accountability while improving portfolio profitability. A significant development announced during the presentation was the company’s intent to sell Myers Tire Supply, signaling a strategic shift away from the underperforming Distribution segment.

The company outlined several key initiatives that are part of this transformation:

Cost reduction remains a central focus, with management expressing confidence in achieving $20 million in annualized cost savings by the end of 2025. These efforts include idling rotational molding facilities to improve utilization and reduce operational costs. The company has also implemented new core values—Integrity, Customer Focus, Deliver Results, and Continuous Improvement—and aligned incentive plans to drive performance.

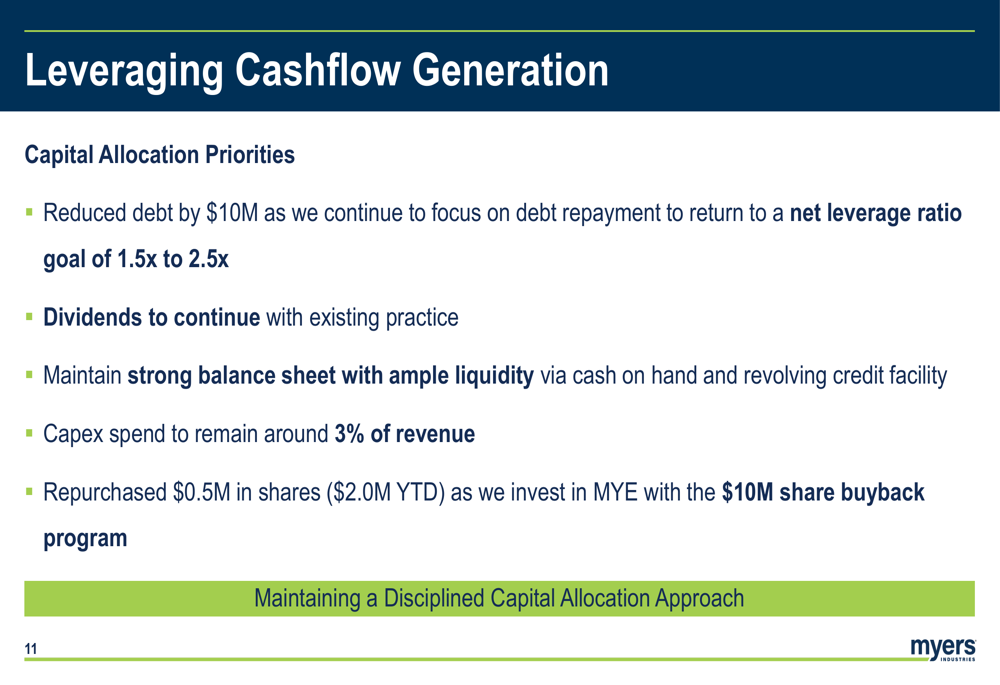

Cash flow optimization has enabled Myers Industries to activate a $10 million share repurchase authorization, with $2 million already repurchased year-to-date. The company is targeting capital expenditures of approximately 3% of sales, balancing investment needs with cash conservation.

Detailed Financial Analysis

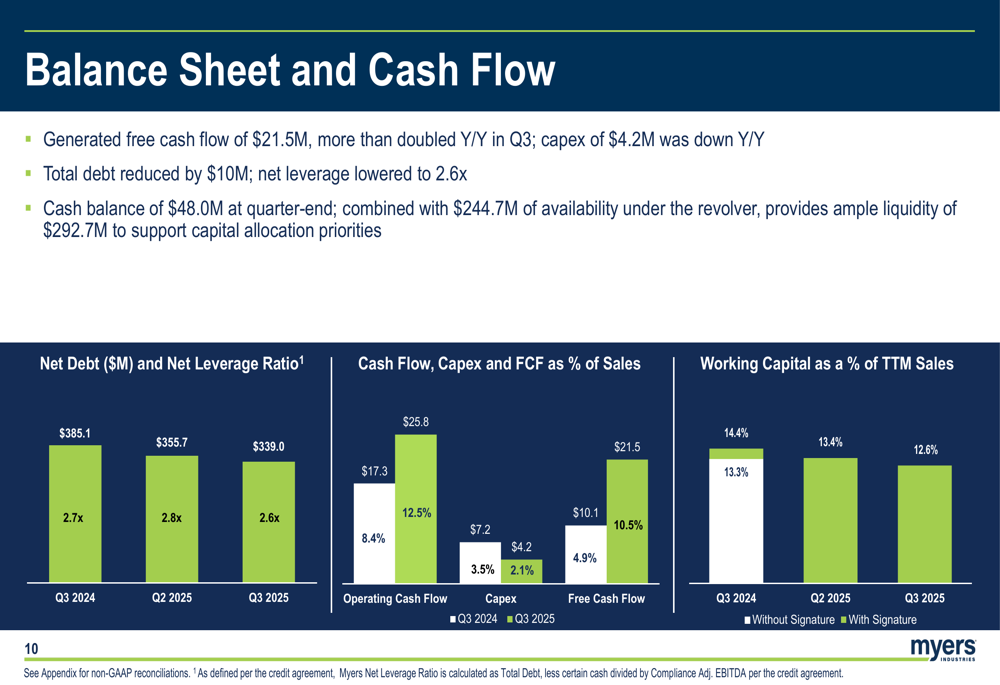

Myers Industries demonstrated strong financial discipline in Q3 2025, generating free cash flow of $21.5 million, more than double the amount from the same period last year. This robust cash generation allowed the company to reduce its total debt by $10 million and lower its net leverage ratio to 2.6x.

The following chart illustrates the company’s improving balance sheet and cash flow metrics:

The company maintained a solid liquidity position with a cash balance of $48.0 million at quarter-end. Combined with $244.7 million of availability under its revolving credit facility, Myers Industries has $292.7 million in total liquidity to support its capital allocation priorities.

Management outlined its approach to leveraging cash flow generation:

Working capital management has also improved, with working capital as a percentage of trailing twelve-month sales at 12.6%, reflecting the company’s focus on operational efficiency and inventory optimization.

Forward-Looking Statements

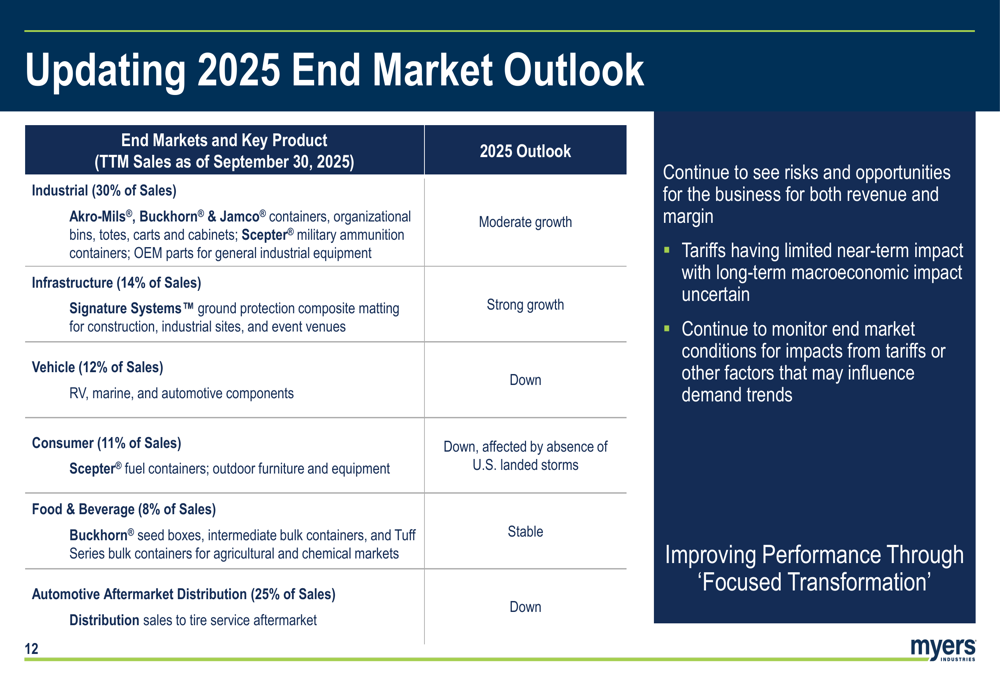

Myers Industries provided an updated outlook for its end markets for the remainder of 2025, highlighting both opportunities and challenges:

The industrial sector, representing 30% of sales, is expected to see moderate growth, while the infrastructure segment (14% of sales) is projected to experience strong growth. However, the vehicle (12%) and consumer (11%) end markets are anticipated to decline, with the latter affected by the absence of U.S. landed storms. The food and beverage sector (8%) is expected to remain stable, while the automotive aftermarket distribution business (25%) is forecasted to decline further.

Management noted that tariffs are having a limited near-term impact on the business, though the long-term macroeconomic effects remain uncertain. The company continues to monitor end market conditions for any factors that may influence demand trends.

Despite these mixed market conditions, Myers Industries remains committed to its transformation strategy, with CEO Aaron Schapper emphasizing, "We are creating operational rigor and instilling a mindset of continuous improvement." The company’s focus on cost reduction, operational excellence, and strategic portfolio optimization suggests a disciplined approach to navigating the current economic environment while positioning for future growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.