Two 59%+ winners, four above 25% in Aug – How this AI model keeps picking winners

Introduction & Market Context

Myriad Genetics (NASDAQ:MYGN) reported its first quarter 2025 financial results on May 6, revealing a 3% year-over-year revenue decline and significantly reduced full-year guidance. The genetic testing company’s stock plummeted 18.02% in aftermarket trading to $5.96 following the announcement, as investors reacted to the disappointing results and lowered outlook.

The company faced several headwinds during the quarter, including the impact of UnitedHealthcare’s coverage changes for GeneSight testing and slower-than-expected growth in hereditary cancer testing for unaffected populations. While some segments showed strength, particularly in prenatal testing, the overall performance prompted management to take a more conservative approach to their 2025 projections.

Quarterly Performance Highlights

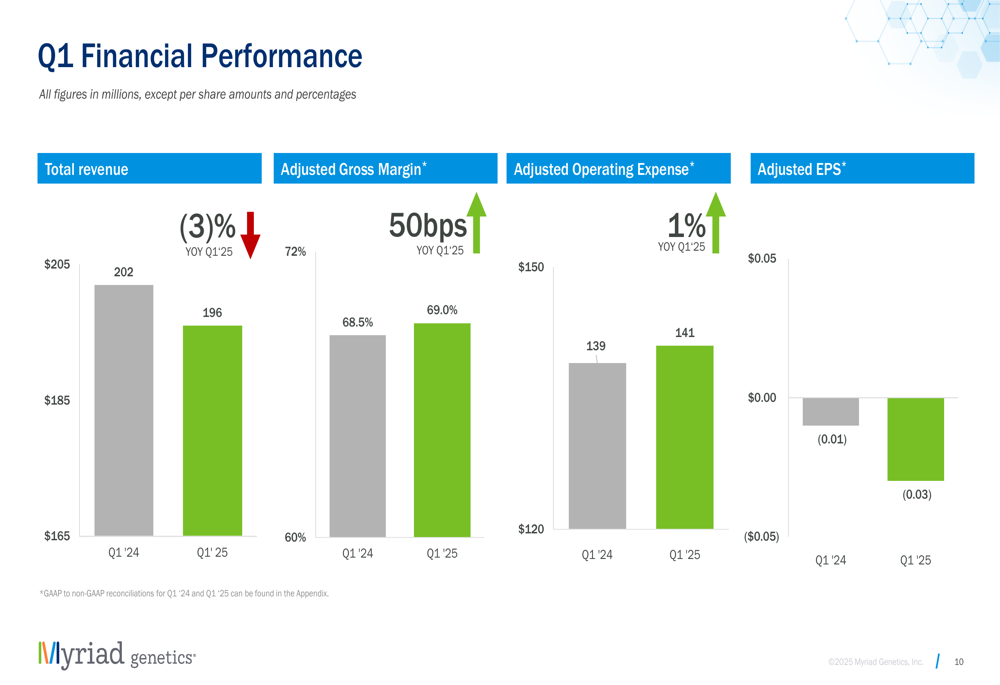

Myriad Genetics reported total revenue of $196 million for Q1 2025, down 3% from $202 million in the same period last year. The company posted an adjusted loss per share of $0.03, compared to a loss of $0.01 in Q1 2024.

As shown in the following chart of quarterly financial performance:

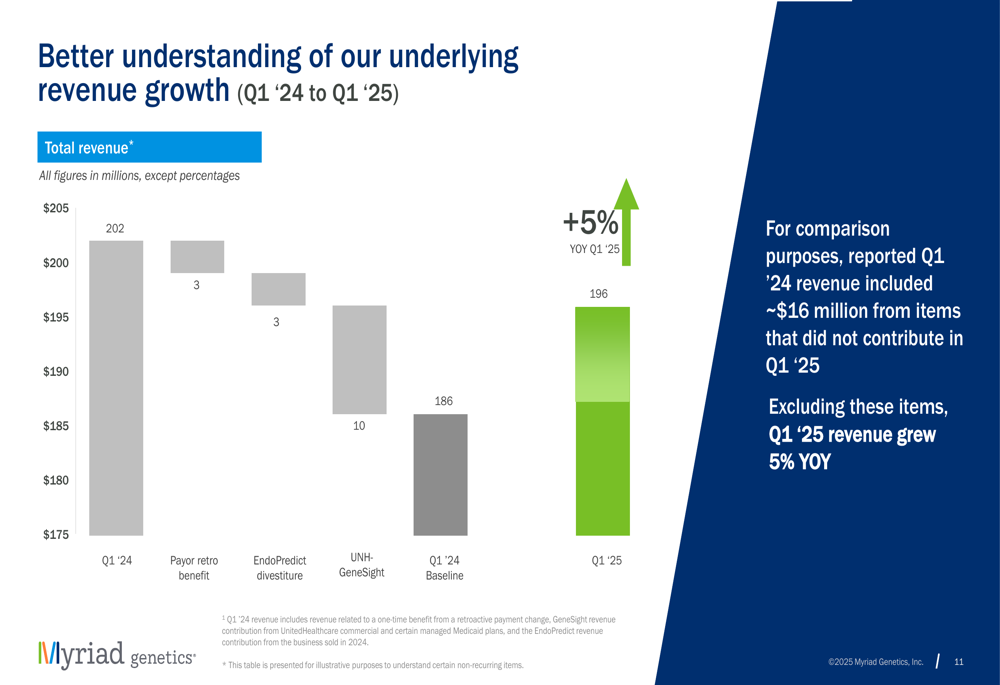

However, management emphasized that when excluding certain one-time factors, the underlying business showed growth. Specifically, when removing the impact of UnitedHealthcare’s GeneSight coverage changes, the EndoPredict divestiture, and a one-time retroactive payment benefit from Q1 2024, revenue actually grew by 5% year-over-year.

The following waterfall chart illustrates these adjustments to better understand the underlying revenue growth:

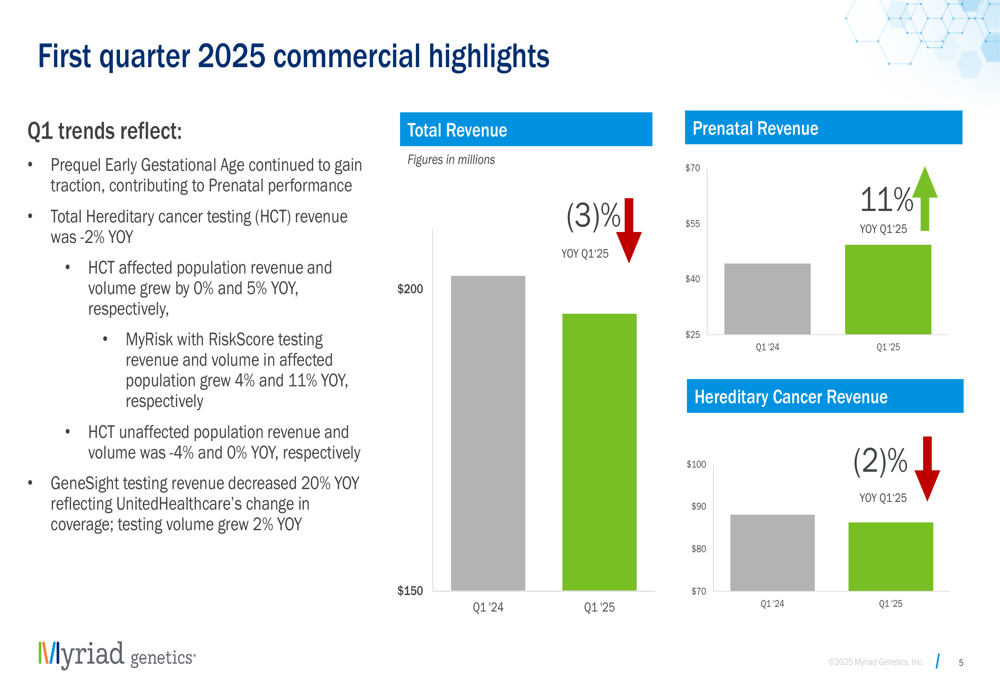

By segment, prenatal testing was a bright spot with revenue increasing 11% year-over-year to $55 million, while hereditary cancer revenue declined 2% to $70 million. Testing volumes showed modest growth of 1% overall, with Foresight and Prequel prenatal tests up 10% and hereditary cancer testing for cancer patients up 5%.

The commercial highlights by segment are illustrated in this breakdown:

Detailed Financial Analysis

Myriad’s adjusted gross margin improved slightly to 69.0% in Q1 2025, up from 68.5% in the prior-year period. Adjusted operating expenses increased 1% year-over-year to $141 million, which the company attributed to balancing higher investments in R&D with cost controls.

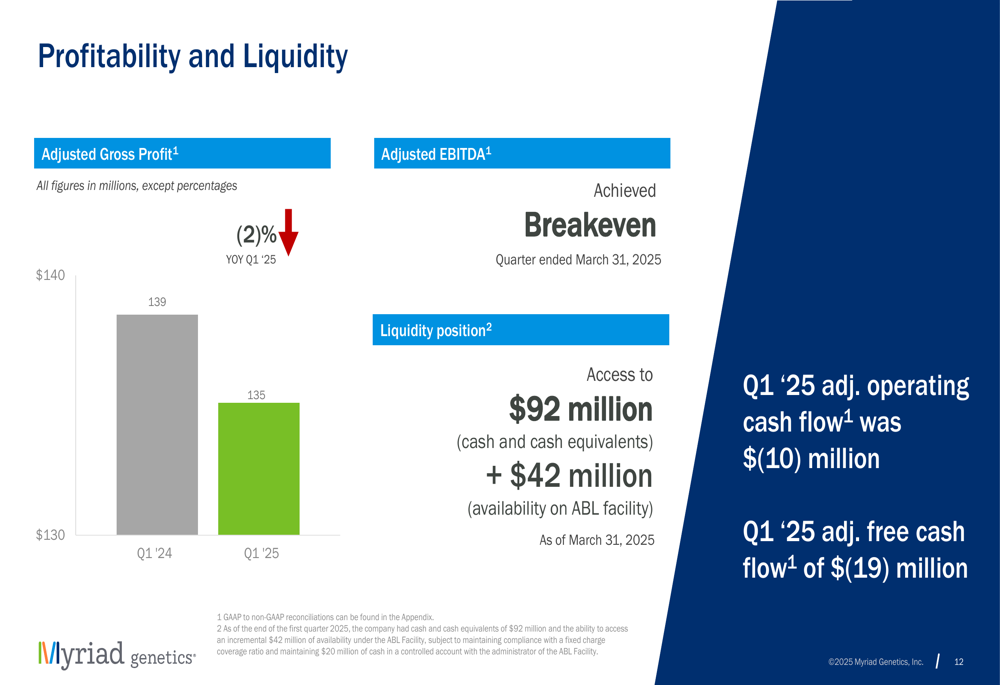

The company’s profitability and liquidity metrics reveal the financial challenges it faces:

Myriad ended the quarter with $92 million in cash and cash equivalents, plus access to $42 million on its ABL facility. This represents a significant decrease from the $158 million in liquidity reported at the end of Q4 2024. Adjusted operating cash flow was negative $10 million, and adjusted free cash flow was negative $19 million for the quarter.

Segment Performance

In the Oncology segment, hereditary cancer testing revenue remained flat year-over-year, though volume grew by 5%. MyRisk with RiskScore testing in the affected population showed stronger performance with 4% revenue growth and 11% volume growth. Prolaris revenue declined 2% year-over-year but has stabilized following National Comprehensive Cancer Network guideline updates.

The Women’s Health segment was the strongest performer, with Foresight and Prequel prenatal tests achieving 15% revenue growth and 10% volume growth. The company highlighted ongoing traction of the recently launched Prequel Early Gestational Age NIPS test and new research presented at the Society for Maternal-Fetal Medicine Conference.

The Pharmacogenomics segment, which includes GeneSight, faced significant challenges with revenue decreasing 20% year-over-year due to UnitedHealthcare’s coverage changes. Despite this setback, testing volume grew 2% year-over-year, and the provider network expanded to over 30,000 healthcare professionals.

Forward-Looking Statements

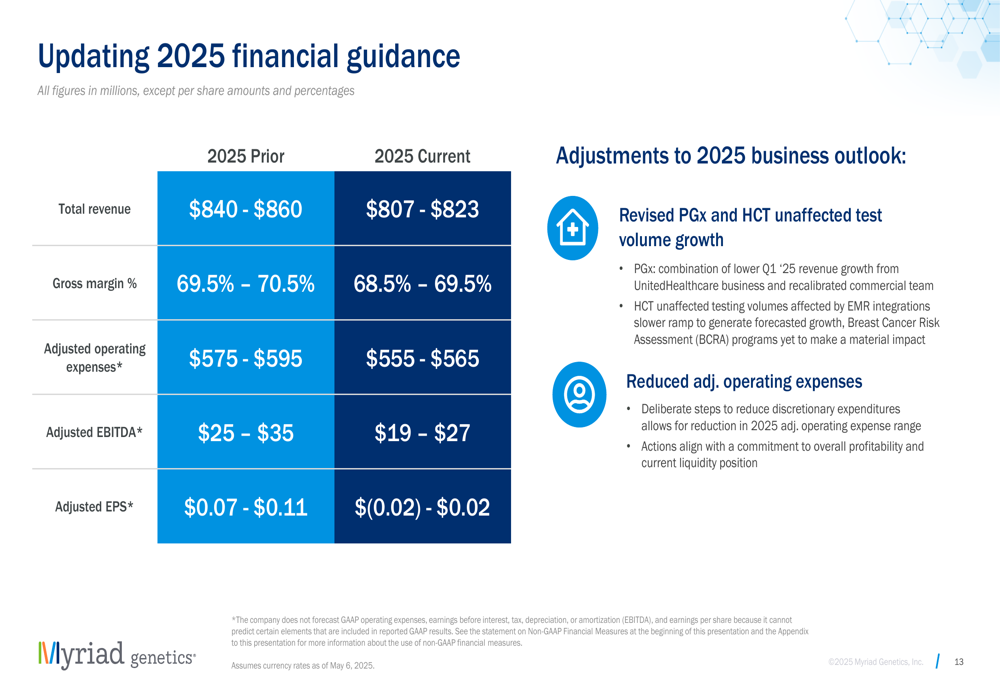

In response to the Q1 performance, Myriad Genetics substantially reduced its 2025 financial guidance across all metrics. The updated outlook is presented in the following table:

The company lowered its revenue guidance by $35 million at the midpoint to a range of $807-$823 million, down from the previous $840-$860 million. Adjusted EPS guidance was reduced to between a loss of $0.02 and a profit of $0.02, compared to the previous range of $0.07-$0.11.

Management attributed the guidance reduction to revised expectations for pharmacogenomics and hereditary cancer testing volume growth. Specifically, they cited lower GeneSight revenue growth from UnitedHealthcare business, slower-than-expected ramp of EMR integrations for hereditary cancer testing, and Breast Cancer Risk Assessment programs that have yet to make a material impact.

To address these challenges, the company is taking "deliberate steps to reduce discretionary expenditures," lowering its adjusted operating expense guidance by $25 million at the midpoint to $555-$565 million.

Strategic Initiatives

Despite the financial setbacks, Myriad Genetics highlighted several strategic developments that could drive future growth:

1. A partnership with PATHOMIQ that is generating high interest among clinicians

2. New clinical data for the Precise MRD test presented at AACR, with more to be presented at the upcoming ASCO conference

3. An agreement with INTERLINK Care Management enabling over 1 million CancerCARE for Life members to assess their eligibility for MyRisk testing

4. Continued traction of the Prequel Early Gestational Age test in the prenatal market

5. A new study published in the Journal of Clinical Psychopharmacology showing that patients with major depressive disorder had fewer psychiatric hospitalizations after taking the GeneSight test

The company emphasized its focus on "Strategy, Team, Execution" as it works to reinforce its foundation and build long-term shareholder value despite the near-term challenges.

The market’s strongly negative reaction to Myriad’s Q1 results and reduced guidance reflects investor concerns about the company’s growth trajectory and profitability path. With the stock now trading well below its 52-week high of $29.30, management faces significant pressure to demonstrate that their strategic initiatives can overcome the current headwinds and deliver improved financial performance in future quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.