Walmart halts H-1B visa offers amid Trump’s $100,000 fee increase - Bloomberg

Introduction & Market Context

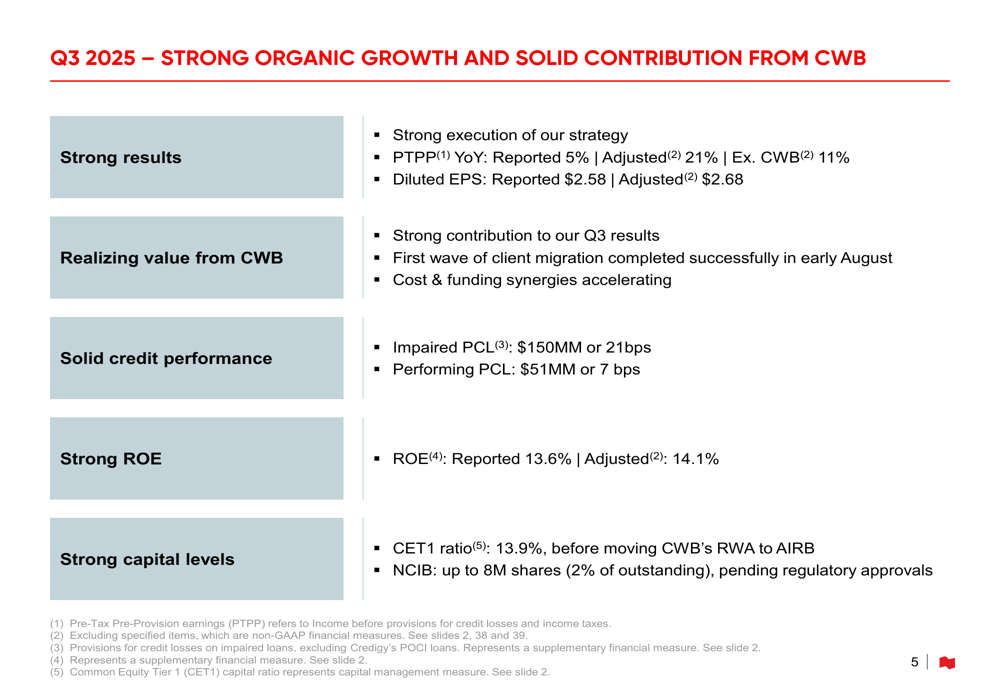

National Bank of Canada (TSX:NA) released its third quarter 2025 investor presentation on August 27, 2025, highlighting solid financial performance across its business segments with a significant contribution from its recently acquired Canadian Western Bank (CWB). The bank reported diluted earnings per share (EPS) of $2.58 on a reported basis and $2.68 on an adjusted basis, showing a sequential decline from the $2.85 reported in Q2 2025.

The bank’s shares closed at $150.41 on August 26, 2025, near its 52-week high of $151.97, reflecting investor confidence despite the slight quarter-over-quarter earnings decline. The presentation comes amid an environment of economic uncertainty, with the bank maintaining strong capital and liquidity positions.

Quarterly Performance Highlights

National Bank reported strong results across all business segments in Q3 2025, with pre-tax pre-provision earnings (PTPP) up 5% on a reported basis, 21% on an adjusted basis, and 11% excluding the CWB acquisition. The bank achieved a return on equity (ROE) of 13.6% on a reported basis and 14.1% on an adjusted basis, slightly below the 15.6% reported in the previous quarter.

Revenue growth was robust across all business segments, with Personal & Commercial (P&C) Banking up 21% year-over-year on a reported basis (2% excluding CWB), Wealth Management up 13%, Financial Markets up 13%, and US Specialty Finance & International (USSF&I) up 11%.

As shown in the following performance highlights from the presentation:

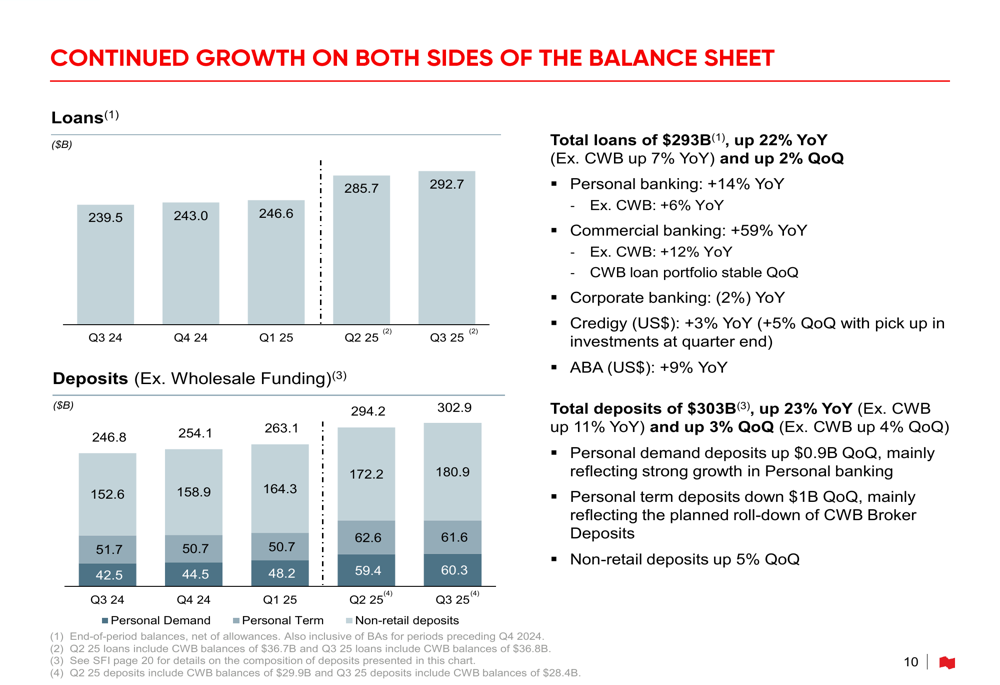

The bank’s balance sheet continued to expand, with total loans reaching $293 billion, up 22% year-over-year (7% excluding CWB), and total deposits of $303 billion, up 23% year-over-year (11% excluding CWB). This growth was driven by both the CWB acquisition and organic expansion across business lines.

The following chart illustrates the bank’s balance sheet growth:

CWB Acquisition Integration Progress

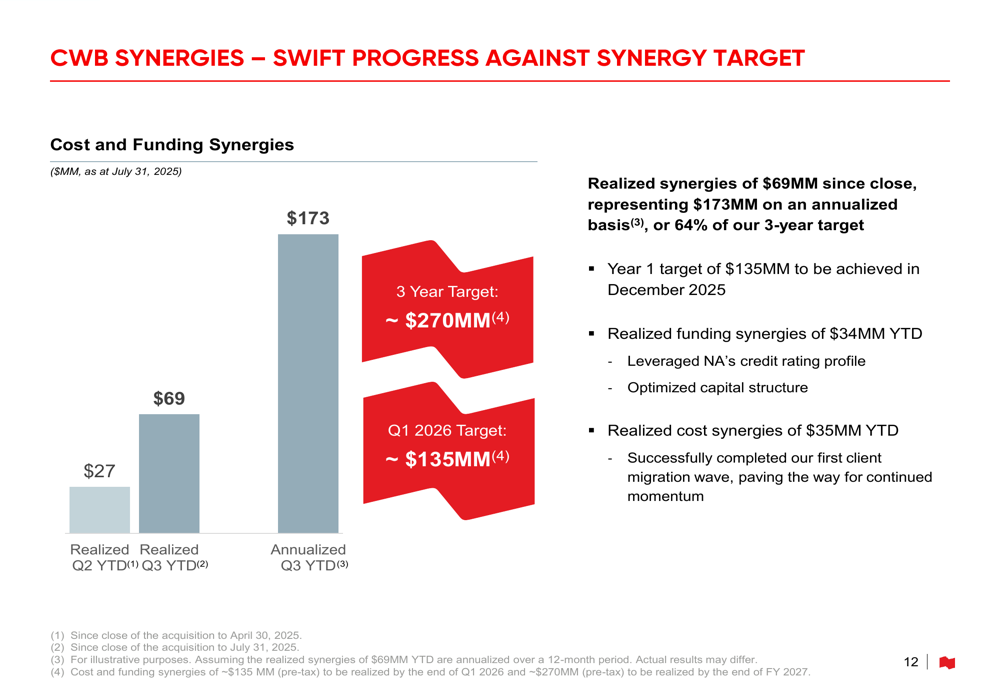

A significant focus of the presentation was the integration of Canadian Western Bank, which was acquired on February 3, 2025. The bank reported strong progress in realizing synergies from the acquisition, with $69 million in synergies realized since closing, representing $173 million on an annualized basis or 64% of the three-year target of approximately $270 million.

The bank completed the first wave of client migration and reported that cost and funding synergies are accelerating. The realized synergies include $34 million in funding synergies and $35 million in cost synergies year-to-date.

As illustrated in the following chart of CWB synergy progress:

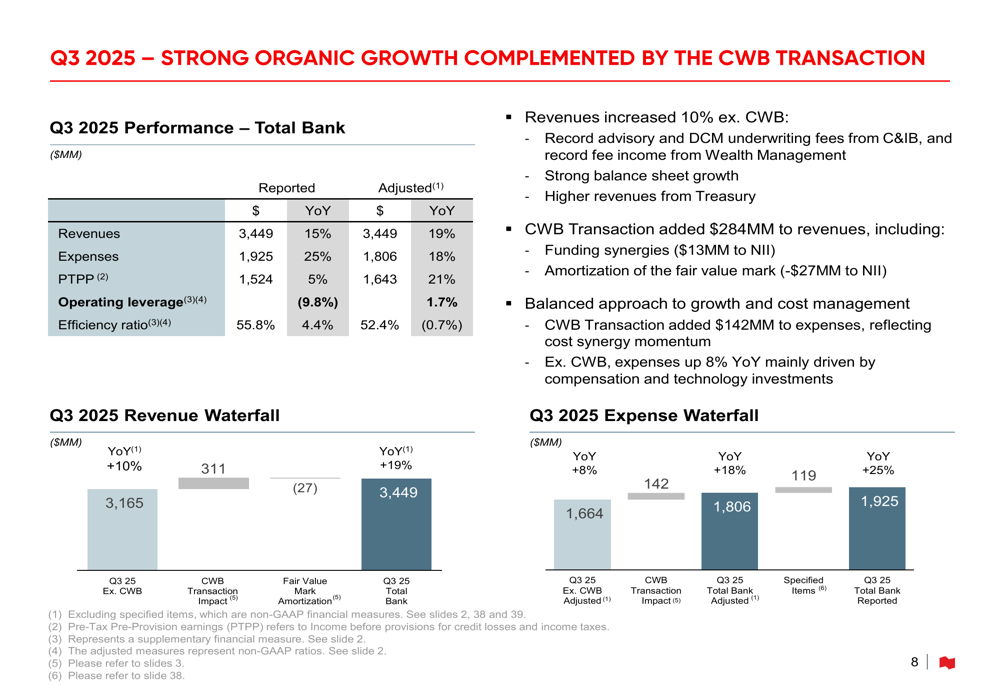

The presentation also provided a detailed breakdown of how the CWB transaction contributed to the bank’s financial results, with the acquisition adding $284 million to revenues, including funding synergies and amortization of fair value mark.

The following waterfall chart shows the impact of CWB on revenues and expenses:

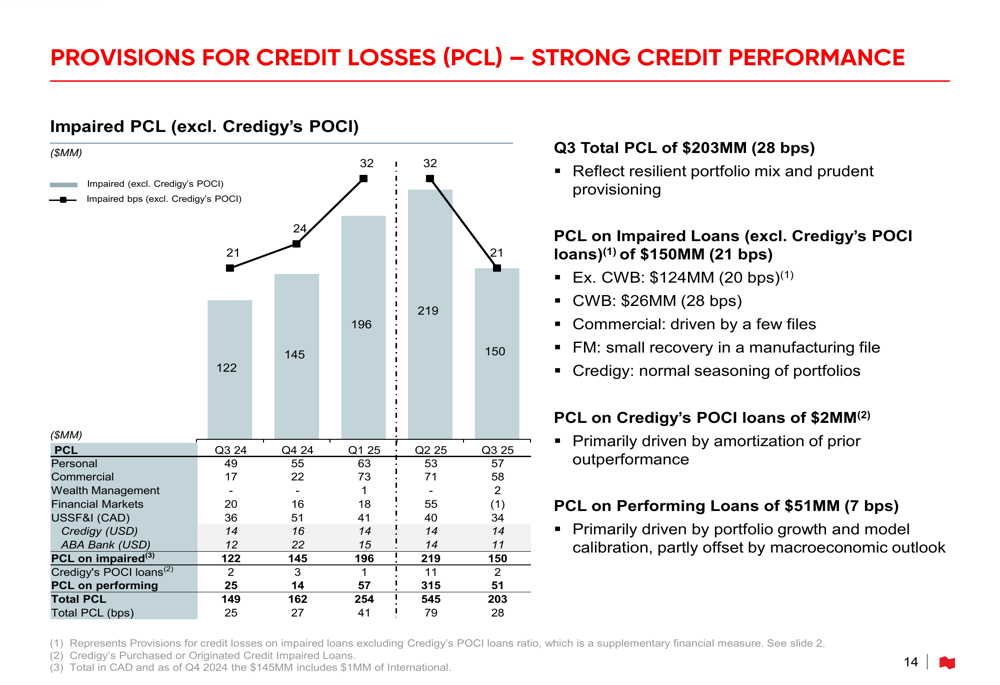

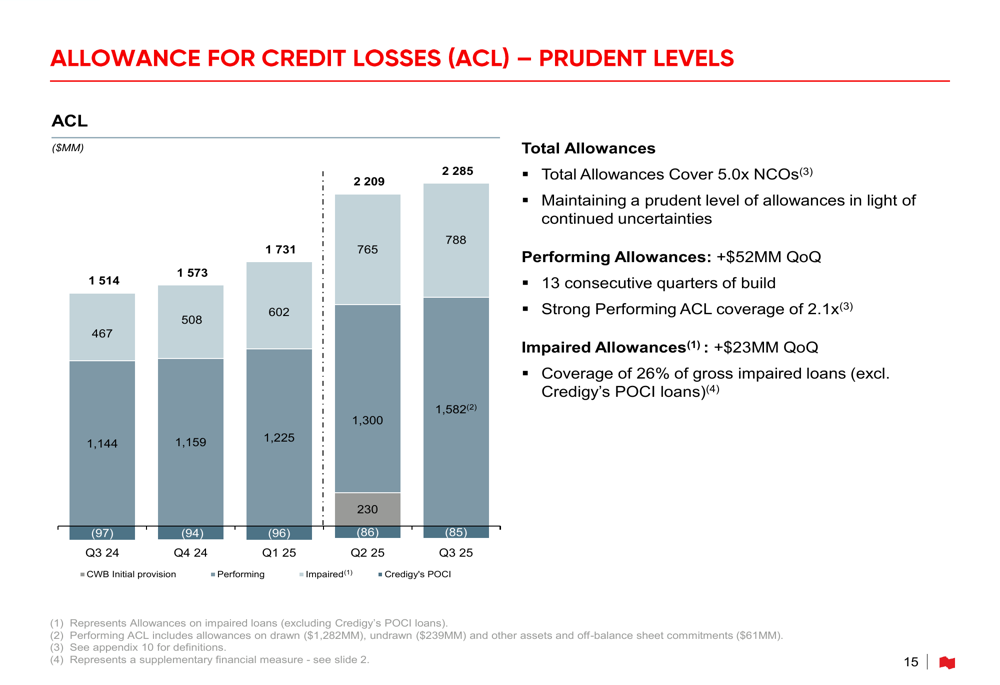

Credit Quality and Risk Management

National Bank reported a significant improvement in credit quality compared to the previous quarter. Total provisions for credit losses (PCL) were $203 million (28 basis points) in Q3 2025, down substantially from $545 million in Q2 2025. PCL on impaired loans was $150 million (21 basis points), while PCL on performing loans was $51 million (7 basis points).

The following chart details the provisions for credit losses:

The bank maintained strong allowances for credit losses, with total allowances covering 5.0 times net charge-offs. Performing allowances increased by $52 million quarter-over-quarter, providing a coverage of 2.1 times, while impaired allowances increased by $23 million, covering 26% of gross impaired loans.

Gross impaired loans (excluding Credigy’s purchased or originated credit-impaired loans) were $2,992 million, up 4 basis points quarter-over-quarter to 102 basis points. Net formations were 12 basis points, down 21 basis points quarter-over-quarter, primarily driven by the CWB transaction.

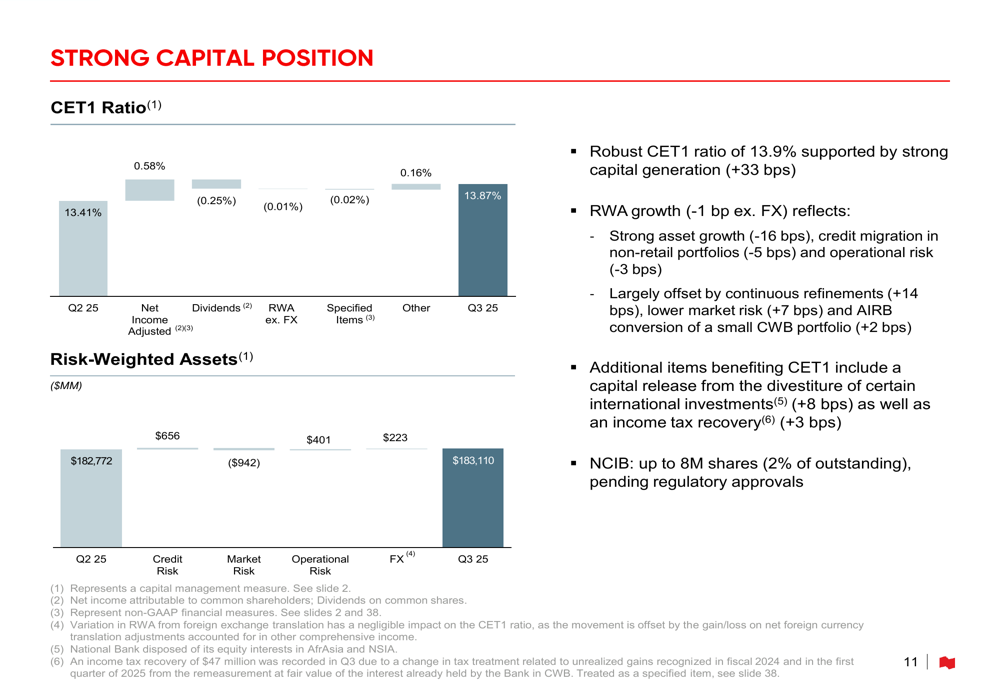

Capital Position and Shareholder Returns

National Bank maintained a strong capital position, with a Common Equity Tier 1 (CET1) ratio of 13.9% at the end of Q3 2025, up from 13.4% in the previous quarter. This improvement was supported by strong capital generation (+33 basis points), partially offset by risk-weighted asset growth (-1 basis point excluding foreign exchange effects).

The following chart illustrates the bank’s capital position:

The bank also announced a Normal Course Issuer Bid (NCIB) for up to 8 million shares, representing approximately 2% of outstanding shares, pending regulatory approvals. This move signals confidence in the bank’s financial strength and commitment to returning capital to shareholders.

Forward-Looking Statements

Looking ahead, National Bank expects to continue realizing synergies from the CWB acquisition, with a target of approximately $135 million in synergies by December 2025 (year 1) and approximately $270 million over three years. The bank is well-positioned to benefit from the integration of CWB’s operations, particularly in Western Canada.

The bank’s mortgage portfolio appears resilient, with approximately 80% of the Canadian mortgage portfolio already repriced to absorb the impact of interest rate increases. About 30% of the mortgage portfolio is variable rate with adjusted monthly payments, and these clients are benefiting from recent rate reductions.

While the bank previously targeted mid-single-digit EPS growth for 2025, the sequential decline in EPS from Q2 to Q3 may put pressure on this target. However, the improved credit quality and strong capital position provide a solid foundation for future growth.

National Bank’s diversified business model, with strong performances across all segments and geographic regions, positions it well to navigate the uncertain economic environment. The successful integration of CWB and the realization of synergies ahead of schedule further strengthen the bank’s competitive position in the Canadian banking landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.