Walmart halts H-1B visa offers amid Trump’s $100,000 fee increase - Bloomberg

Introduction & Market Context

The National Bank of Greece (NBG) presented its Q2 2025 financial results on July 31, 2025, highlighting resilient performance despite the normalizing interest rate environment. The bank maintained strong profitability and upgraded several key performance indicators in its full-year guidance, while operating in a Greek economy that continues to show growth momentum amid global headwinds.

NBG positions itself as the most trusted bank in Greece with the largest savings deposit franchise, supported by a robust balance sheet structure and leading capital levels among European peers.

As shown in the following overview of NBG’s key strengths and market positioning:

Quarterly Performance Highlights

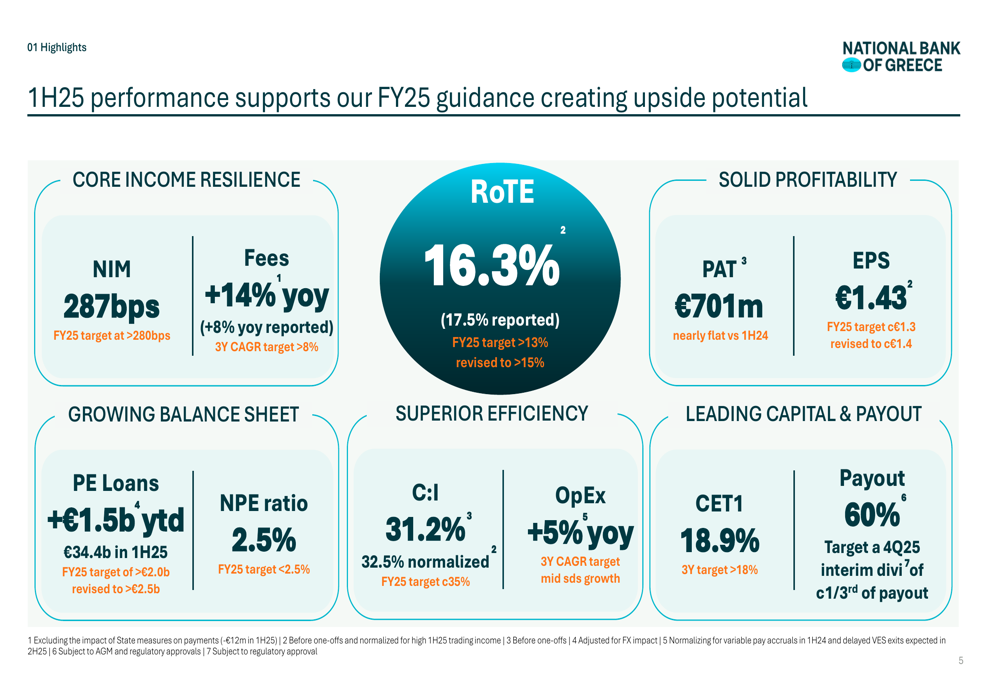

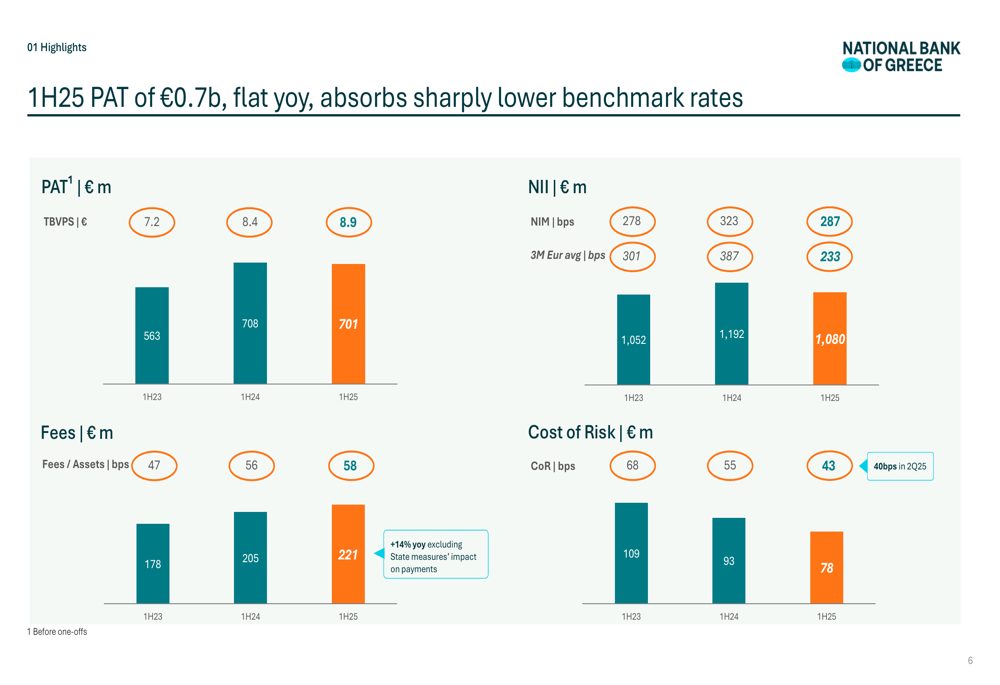

For the first half of 2025, NBG reported a Profit After Tax (PAT) of €701 million, essentially flat year-over-year compared to €708 million in 1H24. The bank achieved a Return on Tangible Equity (RoTE) of 16.3% on a recurring basis (17.5% reported), demonstrating resilient profitability despite pressure from lower interest rates.

Net Interest Income (NII) stood at €1,080 million for 1H25, down from €1,192 million in 1H24, reflecting the impact of lower interest rates as the 3-month Euribor average decreased from 387 bps in 1H24 to 233 bps in 1H25. This was partially offset by strong fee income growth of 14% year-over-year (excluding state measures’ impact on payments).

The following chart illustrates NBG’s 1H25 performance and updated FY25 guidance:

The bank maintained operational efficiency with a Cost-to-Income ratio of 31.2%, while Cost of Risk improved to 43 bps in 1H25 compared to 55 bps in 1H24. NBG’s balance sheet continued to strengthen with performing loan growth of €1.5 billion year-to-date and a Non-Performing Exposure (NPE) ratio of 2.5%.

Key financial metrics for 1H25 are detailed in the following chart:

Detailed Financial Analysis

Income and Profitability

NBG demonstrated resilient income generation and profitability despite the challenging interest rate environment. Total (EPA:TTEF) income reached €1,448 million in 1H25, supporting a PAT of €701 million and Earnings Per Share (EPS) of €1.43. The bank maintained a strong payout ratio of 60%, positioning it favorably compared to European peers.

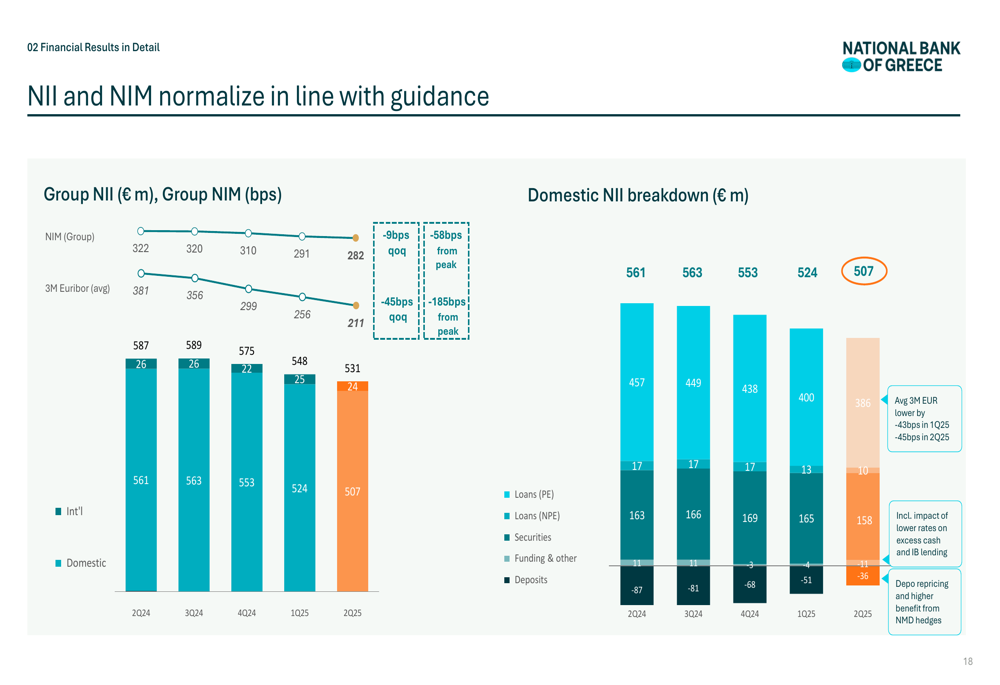

The bank’s income resilience is particularly noteworthy given the significant decline in interest rates, with Net Interest Margin (NIM) at 287 bps in 1H25 compared to 323 bps in 1H24. This normalization of NII and NIM is in line with management guidance.

As illustrated in the following chart showing NII and NIM trends:

Balance Sheet and Capital Position

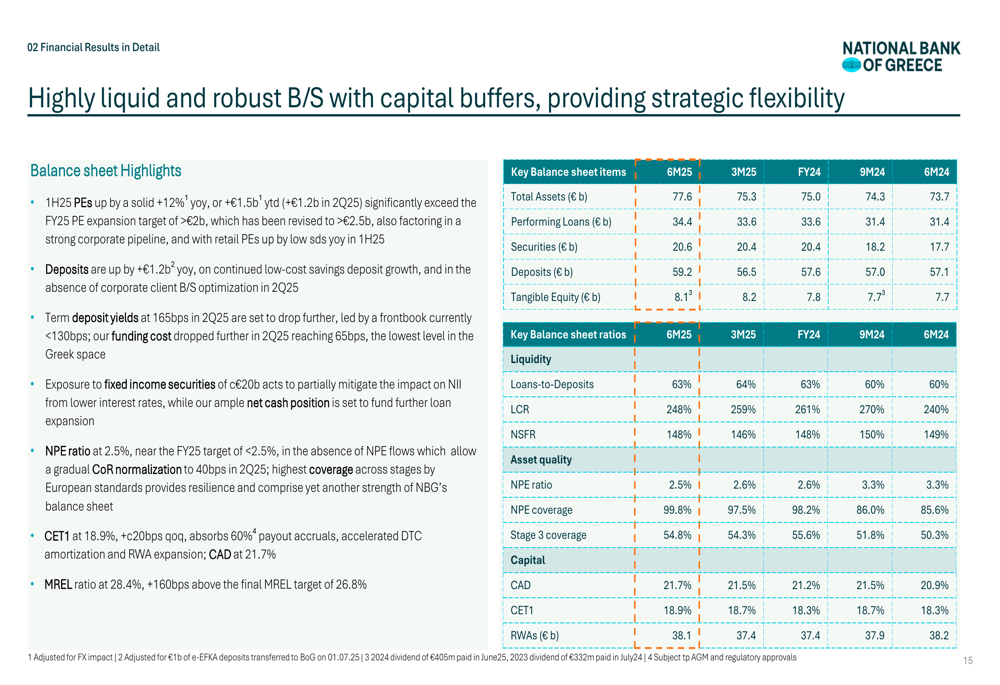

NBG maintained a robust balance sheet with total assets of €77.6 billion as of June 2025. The bank’s capital position remains exceptionally strong with a CET1 ratio of 18.9% and a total Capital Adequacy Ratio of 21.7%, well above regulatory requirements and providing significant flexibility for shareholder returns and strategic investments.

The bank’s liquidity position is equally impressive with a Liquidity Coverage Ratio (LCR) of 248% and a Net Stable Funding Ratio (NSFR) of 148%. The Loan-to-Deposit ratio stands at a conservative 63%, reflecting ample funding capacity for future growth.

The following table provides a comprehensive view of NBG’s balance sheet metrics:

Asset Quality

NBG continued to improve its asset quality with the NPE ratio decreasing to 2.5% in 2Q25, supported by an NPE coverage ratio of 99.8%. The Stage 3 coverage ratio stood at 54.8%, reflecting prudent risk management practices.

The bank’s performing loan portfolio grew by €1.5 billion year-to-date, with management upgrading its full-year guidance for performing loan growth from >€2.0 billion to >€2.5 billion, signaling confidence in continued business momentum.

Strategic Initiatives

Green Bond Issuance

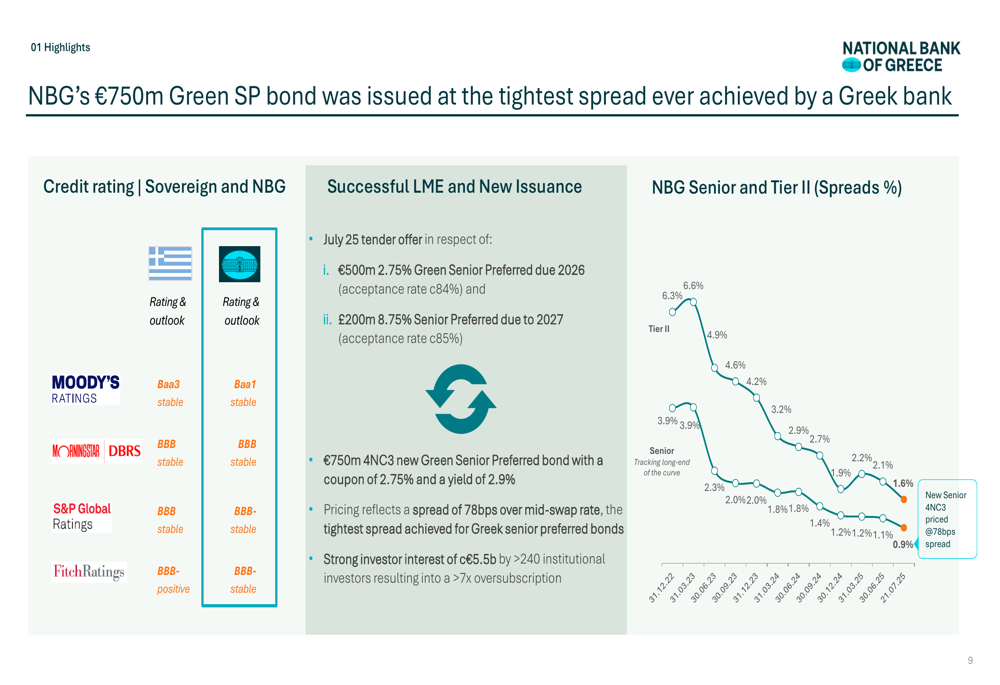

A significant achievement during the quarter was NBG’s successful issuance of a €750 million Green Senior Preferred bond with a coupon of 2.75% and a yield of 2.9%. The bond was priced at a spread of 78 bps over mid-swap rate, representing the tightest spread ever achieved by a Greek bank for senior preferred bonds. The issuance attracted strong investor interest with approximately €5.5 billion in orders from over 240 institutional investors, resulting in more than 7x oversubscription.

The details of this successful bond issuance are illustrated below:

Capital Allocation Strategy

NBG outlined a disciplined approach to excess capital utilization for FY25-27, with potential uses including higher shareholder payouts (above the current 60% ratio), incremental organic growth, international syndicated lending, reperforming assets, and strategic transactions.

The bank plans to distribute an interim dividend in Q4 2025 amounting to approximately one-third of the total expected payout, underscoring its commitment to shareholder returns.

Forward-Looking Statements

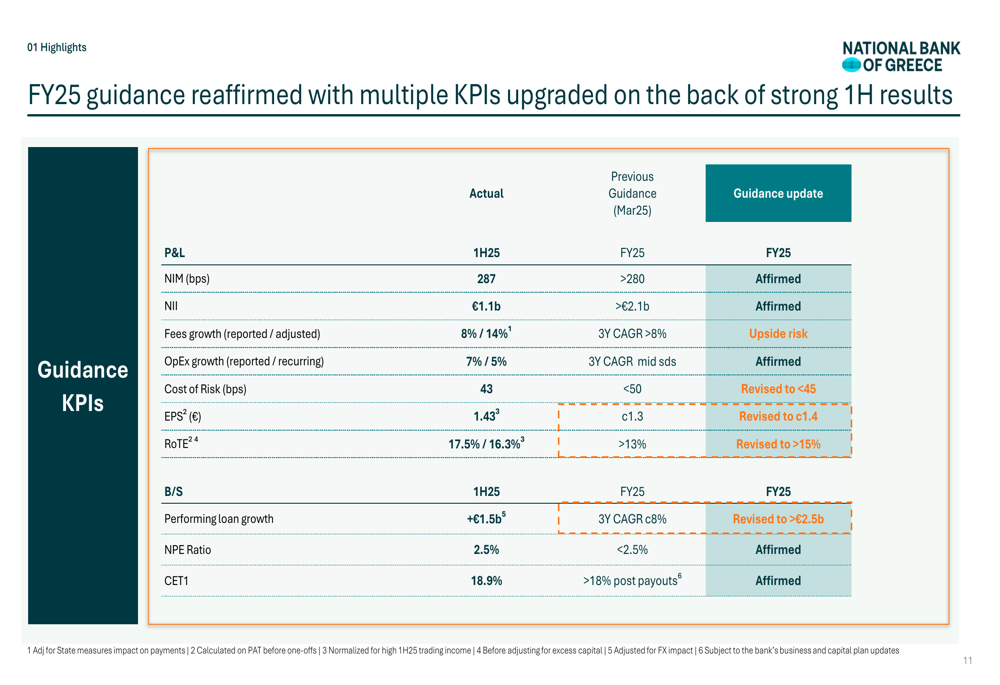

NBG reaffirmed its FY25 guidance while upgrading several key performance indicators. The Return on Tangible Equity (RoTE) target was revised upward from >13% to >15%, while the Cost of Risk guidance was improved to <45 bps. The bank also upgraded its performing loan growth target to >€2.5 billion for the full year.

The following table details NBG’s updated guidance for FY25:

Management expressed confidence in the bank’s ability to maintain resilient performance despite the normalizing interest rate environment, supported by strong fee income growth, operational efficiency, and solid asset quality. The Greek economic outlook remains positive with resilient growth expected to continue, providing a supportive backdrop for the bank’s operations.

NBG’s strategic focus on digital transformation, sustainable finance, and operational excellence positions it well to capitalize on growth opportunities while maintaining its leading market position in Greece.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.