TSX drops after Canadian index edges higher in prior session

Introduction & Market Context

NatWest Group (NYSE:NWG) presented its H1 2025 results on July 25, 2025, showcasing strong financial performance that enabled the bank to significantly strengthen its full-year guidance. The presentation, led by CEO Paul Thwaite and CFO Katie Murray, highlighted robust growth across key metrics, improved efficiency, and enhanced shareholder returns. The positive momentum has continued beyond the first half, with NatWest’s Q3 2025 results subsequently exceeding analyst expectations, driving the stock price to near its 52-week high of $15.69.

Financial Performance Highlights

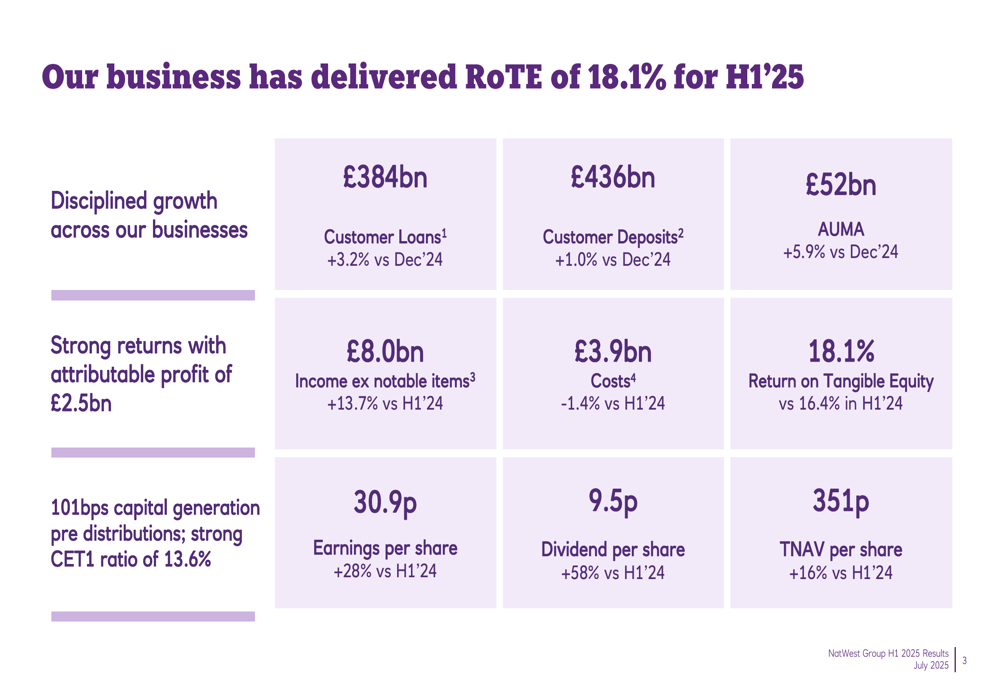

NatWest delivered impressive H1 2025 results, with income excluding notable items reaching £8.0 billion, representing a 13.7% increase compared to H1 2024. The bank maintained strong cost discipline, reducing expenses by 1.4% year-over-year to £3.9 billion. These factors contributed to a significant improvement in profitability, with Return on Tangible Equity (ROTE) rising to 18.1% from 16.4% in the same period last year.

As shown in the following financial highlights chart, earnings per share grew by 28% to 30.9p, while dividend per share increased by 58% to 9.5p:

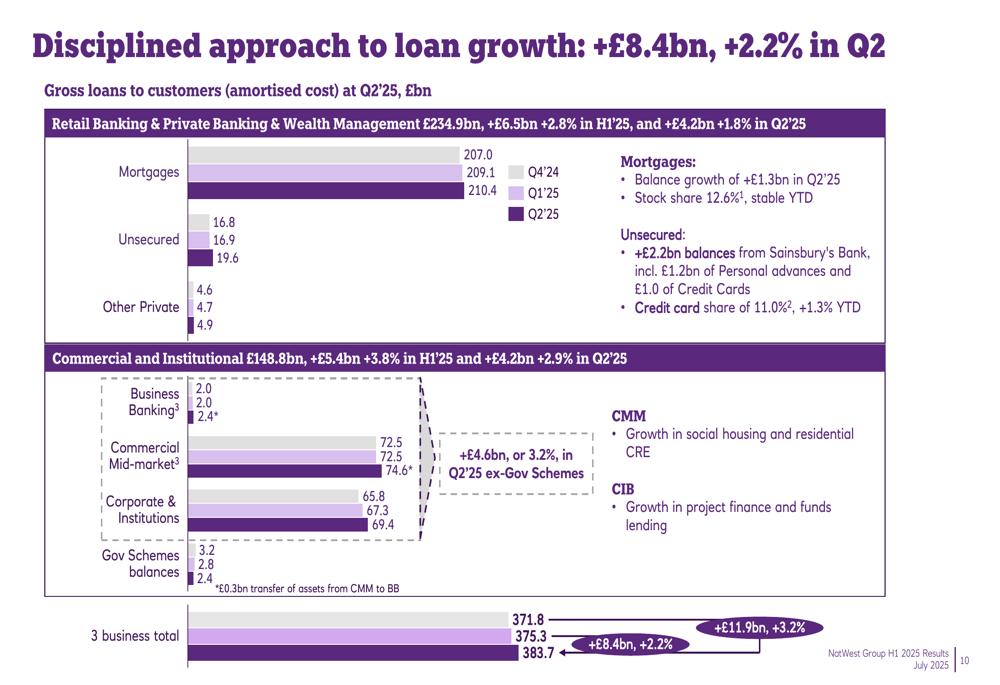

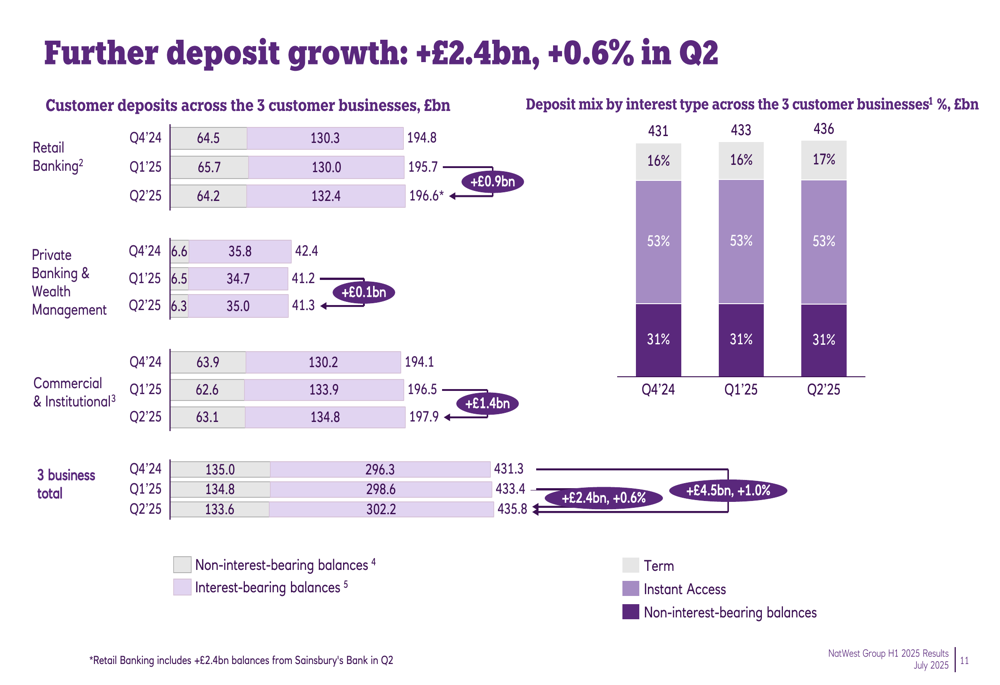

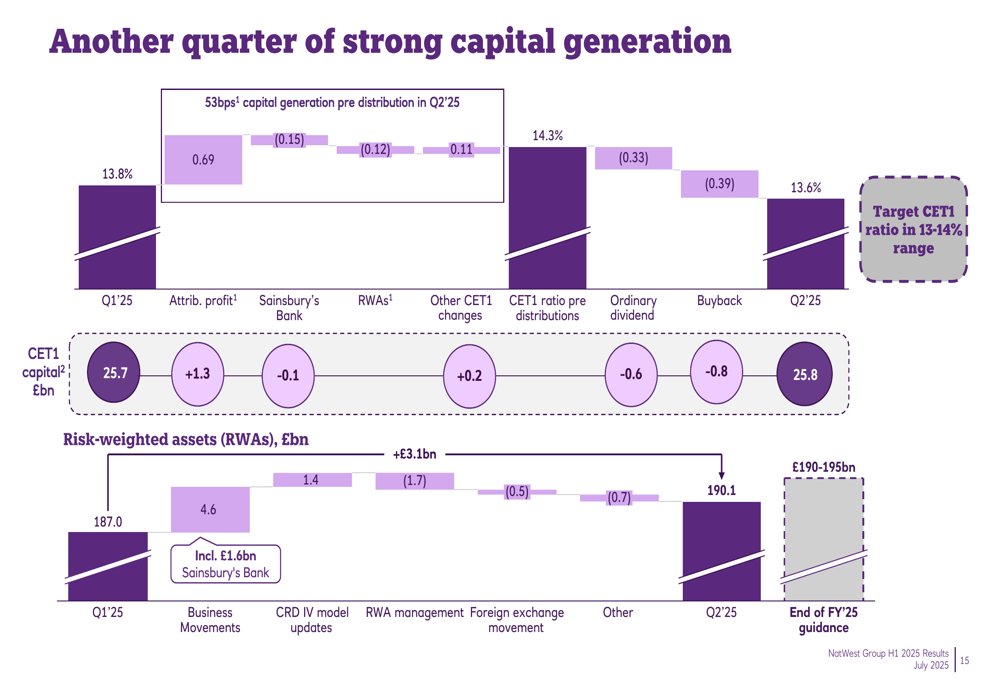

The bank demonstrated disciplined growth in its balance sheet, with customer loans increasing by 3.2% to £384 billion since December 2024. Customer deposits grew by 1.0% to £436 billion, while Assets Under Management and Administration (AUMA) rose by 5.9% to £52 billion. NatWest maintained a strong capital position with a CET1 ratio of 13.6% and generated 101 basis points of capital before distributions.

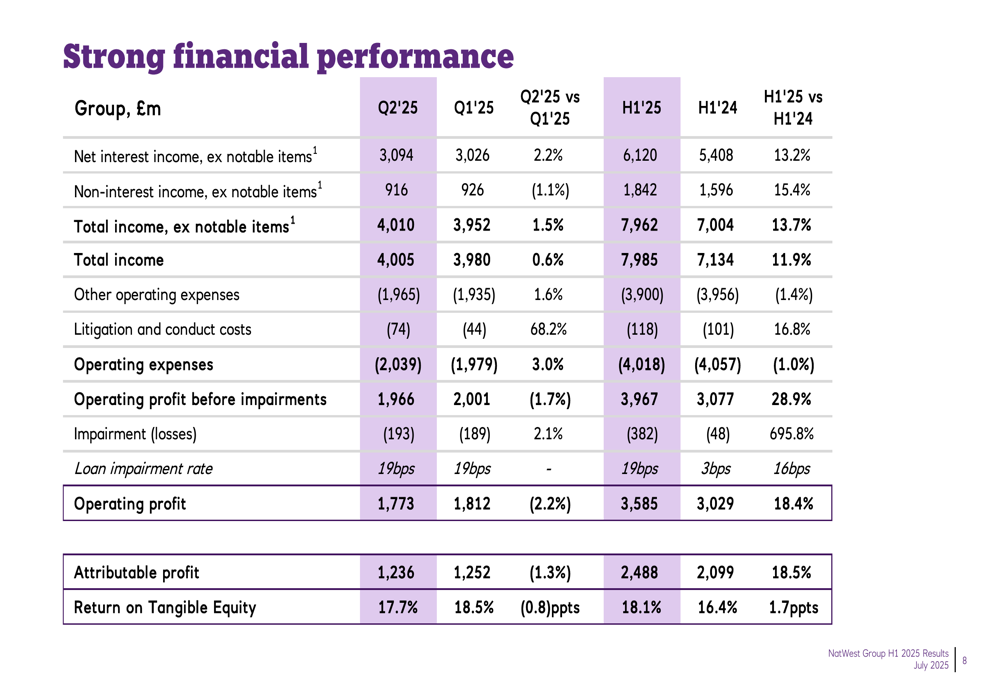

The detailed financial performance breakdown shows consistent improvement across key metrics:

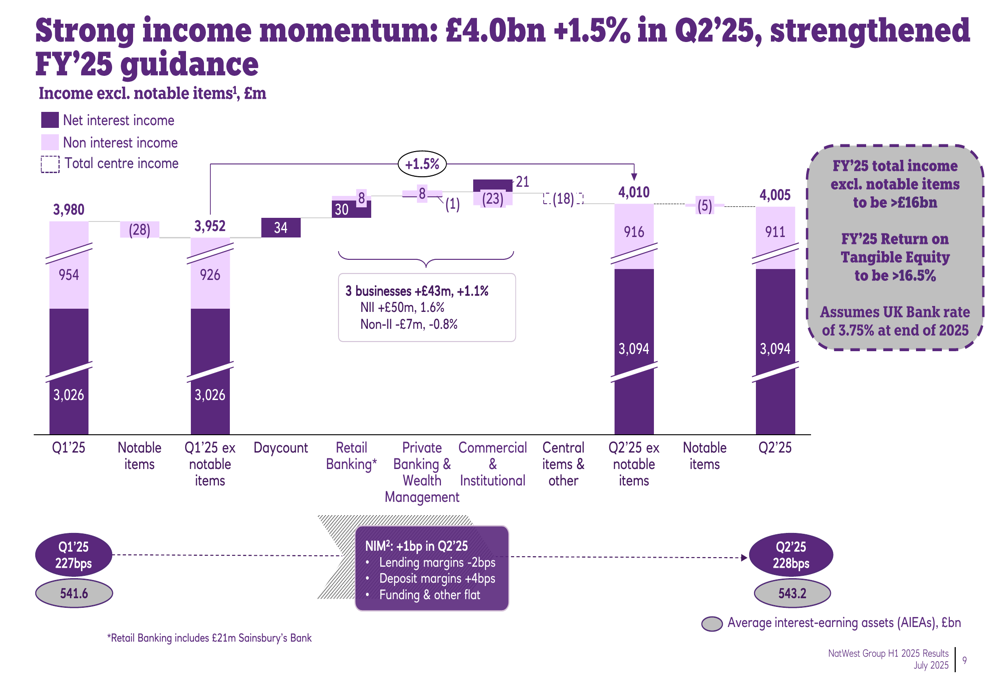

Income momentum remained strong throughout the first half of 2025, with Q2 total income excluding notable items reaching £4.01 billion, a 1.5% increase from Q1:

Strengthened Guidance

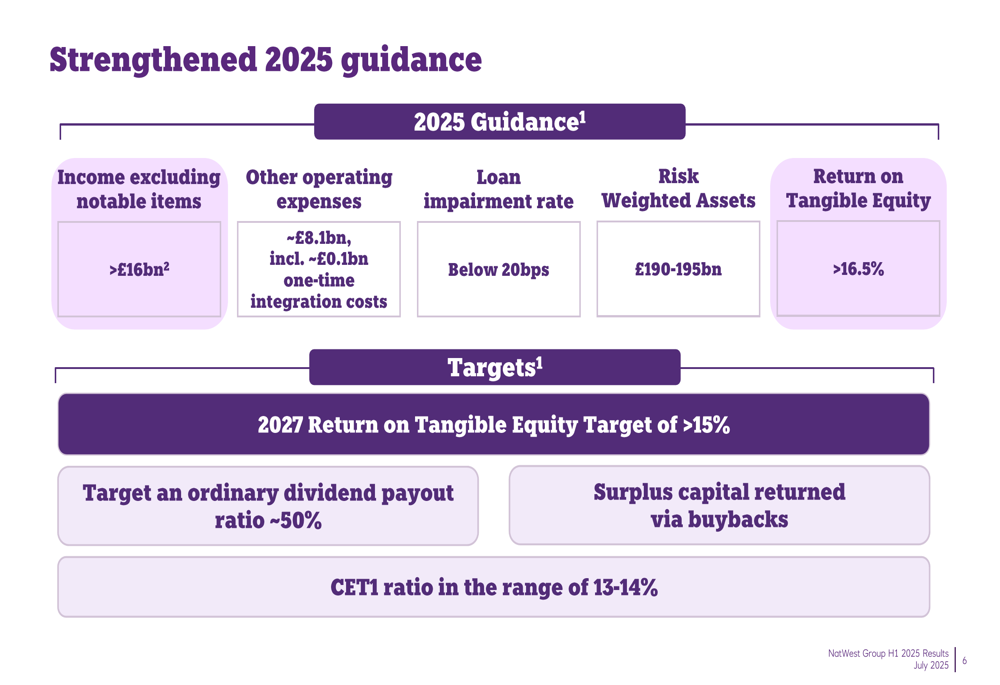

Based on the strong H1 2025 performance, NatWest significantly upgraded its full-year guidance. The bank now expects income excluding notable items to exceed £16 billion, up from the previous guidance of £15.2-15.7 billion. The Return on Tangible Equity target was raised to above 16.5%, compared to the previous range of 15-16%.

As illustrated in the following guidance summary, NatWest maintained its cost outlook while improving income and profitability targets:

This strengthened guidance reflects management’s confidence in the bank’s underlying performance and growth trajectory. Notably, subsequent Q3 2025 results have shown that NatWest continues to exceed these upgraded expectations, with the bank further revising its full-year income guidance to £16.3 billion and achieving a ROTE of 19.5% in Q3.

Strategic Initiatives

NatWest’s presentation emphasized three strategic priorities: disciplined growth, bank-wide simplification, and active balance sheet and risk management. The bank reported adding 1.1 million customers in H1 2025, with growth across all three business segments. The integration of Sainsbury’s Bank is progressing according to plan, contributing to the expansion of NatWest’s retail banking operations.

The disciplined loan growth strategy is evident across different segments of the loan book:

Similarly, deposit growth remained positive, with an increase of £2.4 billion (0.6%) in Q2 2025:

The bank continues to focus on simplification initiatives, including productivity improvements, digitizing customer journeys, modernizing its technology estate, and accelerating data simplification and AI deployment. These efforts have contributed to the reduction in operating expenses and improved operational efficiency.

Capital Management & Shareholder Returns

NatWest demonstrated strong capital generation of 53 basis points pre-distribution in Q2 2025, supporting increased shareholder returns:

The bank announced a £750 million share buyback program alongside an interim dividend of 9.5p per share, representing a 58% increase compared to H1 2024. Total distributions to shareholders in H1 2025 amounted to approximately £1.5 billion.

NatWest’s tangible net asset value per share increased by 16% year-over-year to 351p. The bank targets an ordinary dividend payout ratio of around 50% from 2025 onward and aims to maintain a CET1 ratio in the range of 13-14%.

Forward-Looking Statements

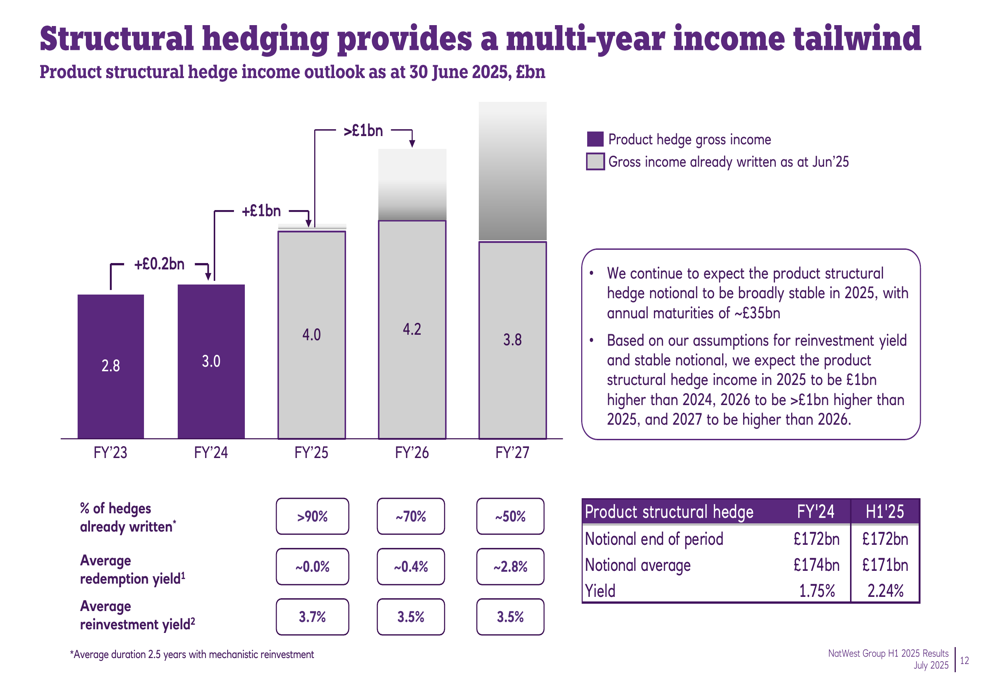

NatWest’s structural hedging strategy is expected to provide a significant income tailwind in the coming years:

The bank maintains a well-diversified, high-quality loan book, with mortgages representing 51% of group lending. The loan impairment rate remained stable at 19 basis points in H1 2025, below the target of 20 basis points, reflecting the bank’s prudent risk management approach.

Looking ahead, NatWest anticipates one more base rate cut in Q1 2026, targeting a terminal rate of 3.5%. Despite the expected rate cuts, the bank’s income outlook remains positive, supported by its structural hedge position and continued growth in customer balances.

Potential challenges include economic uncertainty, competitive pressures in the mortgage and lending sectors, regulatory changes, interest rate volatility, and geopolitical risks. However, NatWest’s strong capital position, diversified business model, and disciplined approach to growth position the bank well to navigate these challenges while continuing to deliver enhanced shareholder returns.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.