BofA update shows where active managers are putting money

Introduction & Market Context

NCR (NYSE:VYX) Atleos Corp (NYSE:NATL) reported its second quarter 2025 financial results on August 7, showcasing continued momentum in its high-margin services business while reaffirming full-year guidance. The company’s shares responded positively, rising 1.38% in after-hours trading to $32.30, building on a 2.01% gain during the regular session.

The global ATM solutions provider demonstrated resilience in its core business segments, with particularly strong performance in its ATM as a Service (ATMaaS) offering, which has become a key growth driver for the company. This follows a solid first quarter where the company posted a 56% year-over-year increase in non-GAAP EPS.

Quarterly Performance Highlights

NCR Atleos reported core revenue growth of 4% year-over-year for Q2 2025, in line with management’s expectations. Adjusted EBITDA reached $205 million, representing a 4% increase compared to the same period last year and landing at the high end of the company’s guidance range. Notably, adjusted diluted EPS grew 9% year-over-year to $0.93, exceeding the high end of the company’s guidance range.

As shown in the following consolidated financial results chart, the company has maintained consistent growth in its key metrics:

The company highlighted several operational achievements, including increased monetization of its global installed base, improved service levels reaching new highs, and enhanced customer satisfaction scores that improved 160 basis points year-to-date. These improvements reflect management’s strategic focus on service excellence and operational efficiency.

Segment Analysis

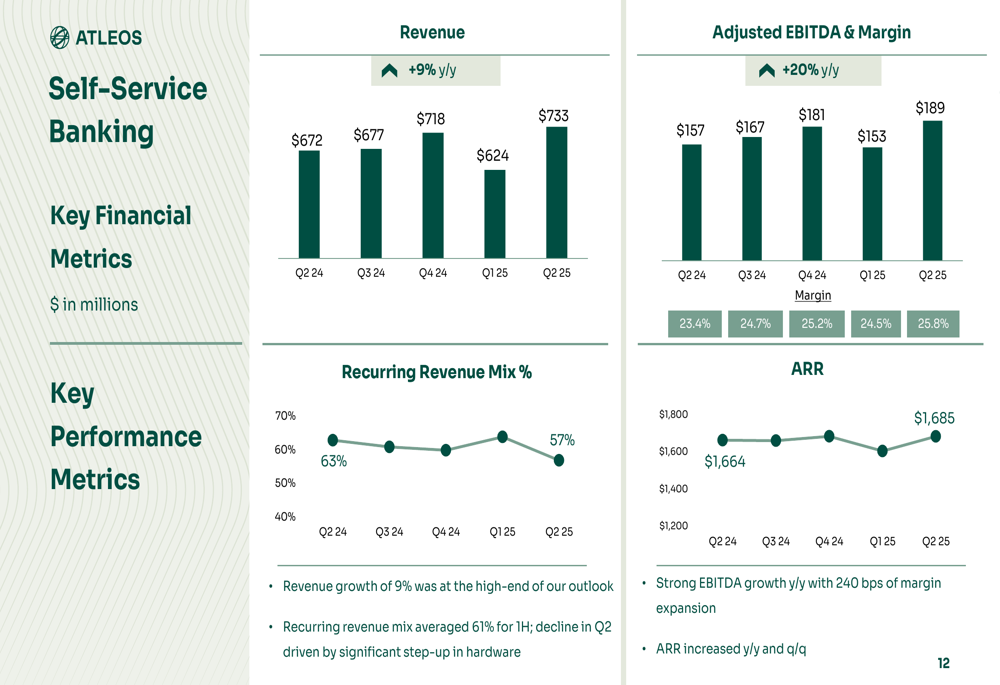

The Self-Service Banking segment, which represents the largest portion of NCR Atleos’ business, delivered strong results with revenue growth of 9% year-over-year and adjusted EBITDA growth of 20%. This impressive performance was driven by margin expansion of approximately 240 basis points across service, software, and hardware offerings.

The segment’s performance is illustrated in the following chart:

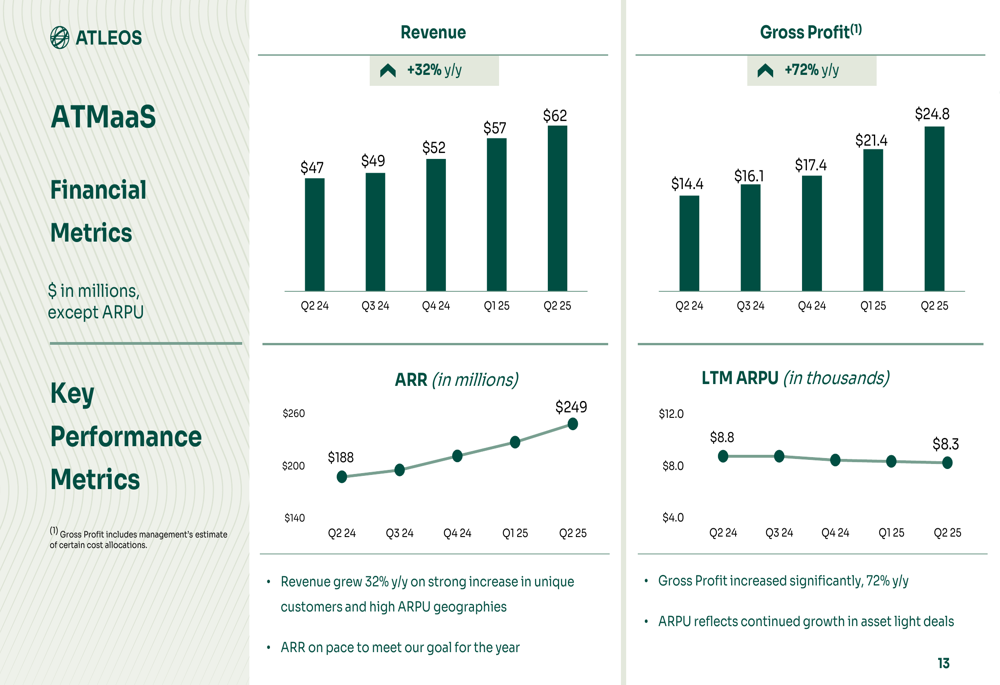

A standout performer within the Self-Service Banking segment was the ATMaaS business, which saw revenue surge 32% year-over-year while gross profit jumped an impressive 72%. This growth was attributed to an increase in unique customers and expansion in high-ARPU geographies.

The ATMaaS business metrics demonstrate the accelerating adoption of this service model:

The Network segment presented a more mixed picture, with revenue declining 2% year-over-year but growing 7% sequentially from Q1 2025. Adjusted EBITDA for this segment decreased 15% year-over-year, primarily due to anticipated higher vault cash costs. Despite these challenges, the segment achieved a solid adjusted EBITDA margin of approximately 27%.

CEO Tim Oliver emphasized the strength of the service business during the earnings call, echoing his comments from Q1 where he stated, "Our service business is hitting on all cylinders right now." This focus on service excellence appears to be yielding results across the company’s operations.

Strategic Initiatives and Growth Drivers

NCR Atleos continues to position itself as an industry leader in self-service banking solutions, leveraging its extensive installed base of over 500,000 ATMs and recognition as the #1 ATMaaS and Managed Services Provider.

The company’s strategic positioning is illustrated in this comprehensive overview:

Key strategic initiatives highlighted in the presentation include:

1. Expanding the company’s ATMaaS offering, which ended Q2 with a robust backlog up 105% year-over-year

2. Launching cloud-based auto-scheduling and routing solutions in North America

3. Implementing AI-driven diagnostics and service tools for technicians

4. Expanding cash deposit-enabled locations, with cash deposit transactions up 170% year-over-year for the first half of 2025

5. Activating the first phase of approximately 1,000 locations for a partnership with FCTI

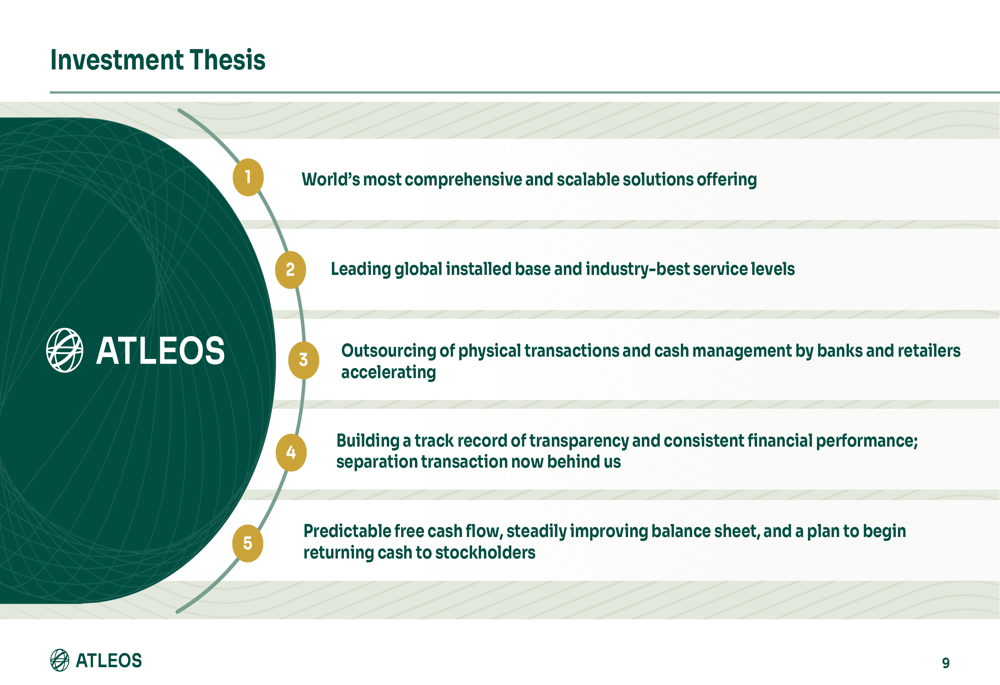

The company also outlined its investment thesis, emphasizing its comprehensive solutions offering, leading global installed base, and the accelerating trend of banks and retailers outsourcing physical transactions and cash management:

Financial Position and Outlook

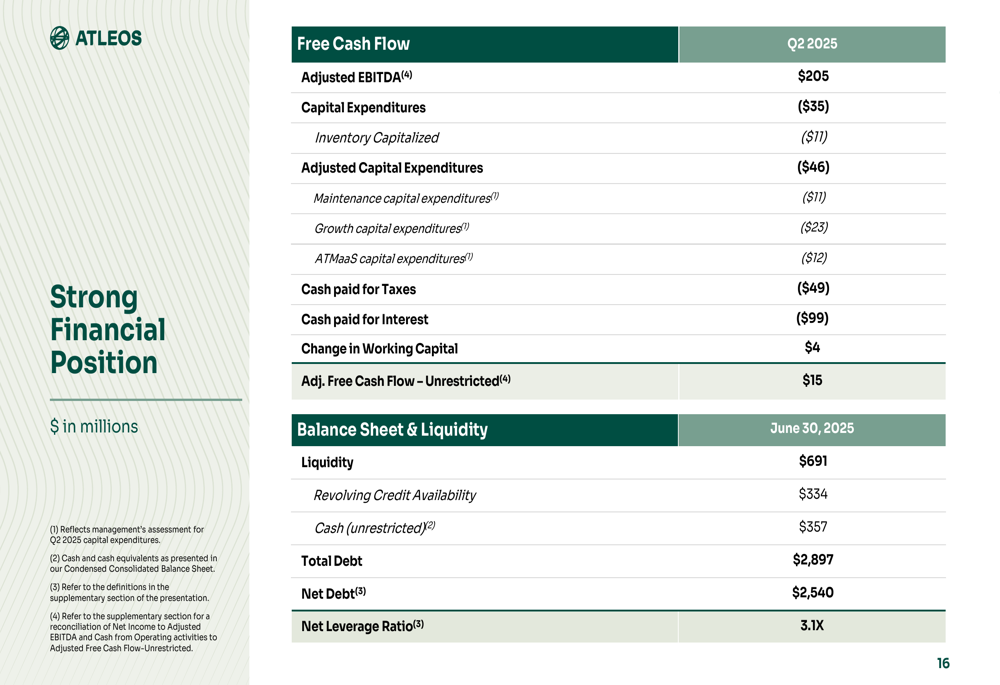

NCR Atleos maintains a strong financial position with liquidity of $691 million as of June 30, 2025. The company reported a net leverage ratio of 3.1x and adjusted free cash flow of $15 million for the quarter.

The company’s financial strength is summarized in the following chart:

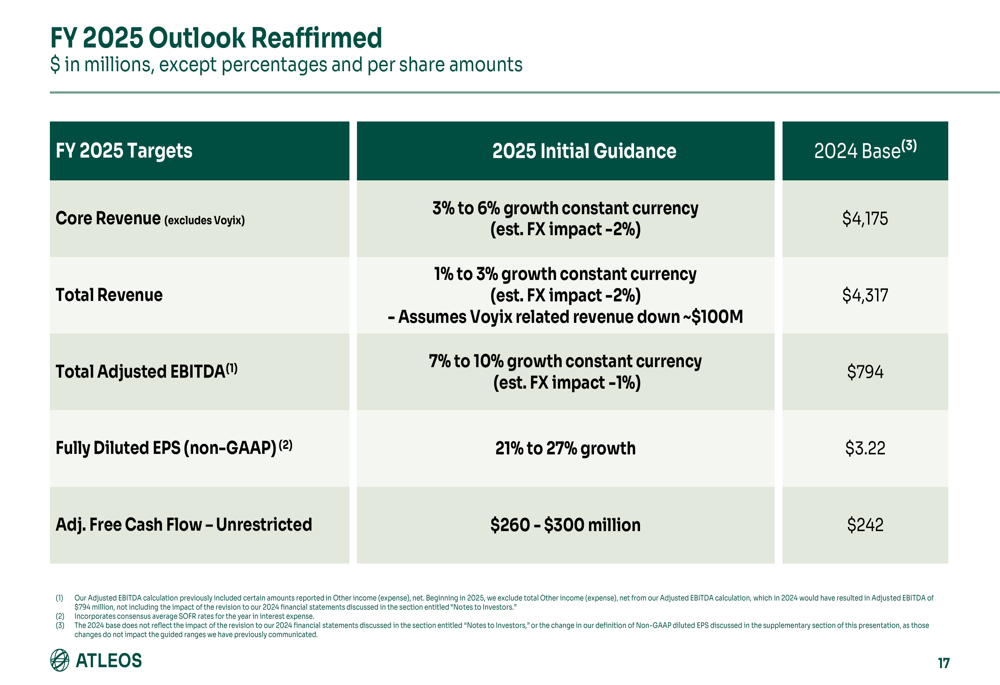

Management reaffirmed its full-year 2025 guidance, projecting core revenue growth of 3% to 6% on a constant currency basis (with an estimated -2% foreign exchange impact). Total (EPA:TTEF) adjusted EBITDA is expected to grow 7% to 10% on a constant currency basis, while fully diluted non-GAAP EPS is projected to increase 21% to 27%. Adjusted free cash flow is anticipated to be between $260 million and $300 million.

The detailed outlook is presented in the following chart:

This reaffirmed guidance aligns with the projections provided after Q1 results, suggesting management’s continued confidence in the company’s trajectory despite mixed performance across segments.

Conclusion

NCR Atleos’ Q2 2025 results demonstrate the company’s successful execution of its strategy focused on growing efficiently, prioritizing service excellence, and embracing operational simplicity. The strong performance in the high-margin ATMaaS business and overall service improvements are driving profitability growth that outpaces revenue expansion.

While challenges remain in certain segments, particularly related to vault cash costs in the Network business, the company’s diversified portfolio and strategic focus on recurring revenue streams position it well for continued growth. The positive market reaction to these results suggests investors are recognizing the progress being made in the company’s transformation toward higher-margin, more predictable revenue streams.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.