SoFi CEO enters prepaid forward contract on 1.5 million shares

Introduction & Market Context

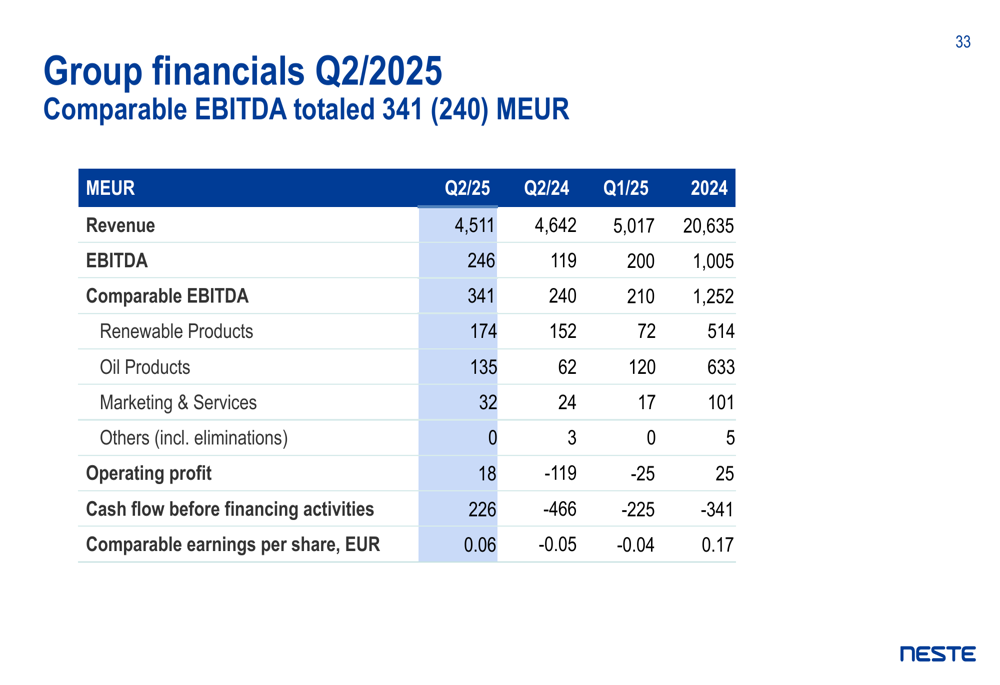

Neste Oyj (HEL:NESTE) presented its second quarter 2025 results on July 24, showing a significant recovery from the challenging first quarter. The Finnish renewable fuels producer reported a comparable EBITDA of 341 million euros, up 62% from 210 million euros in Q1, demonstrating the company’s ability to navigate a complex market environment. This performance comes after Neste’s stock had already risen 7.8% following Q1 results, suggesting investor confidence in the company’s strategic direction that appears to have been justified by these improved Q2 figures.

The company’s current share price of 13.13 euros represents a significant recovery from its 52-week low of 6.79 euros, though still well below the 52-week high of 22.14 euros, reflecting ongoing market challenges despite operational improvements.

Quarterly Performance Highlights

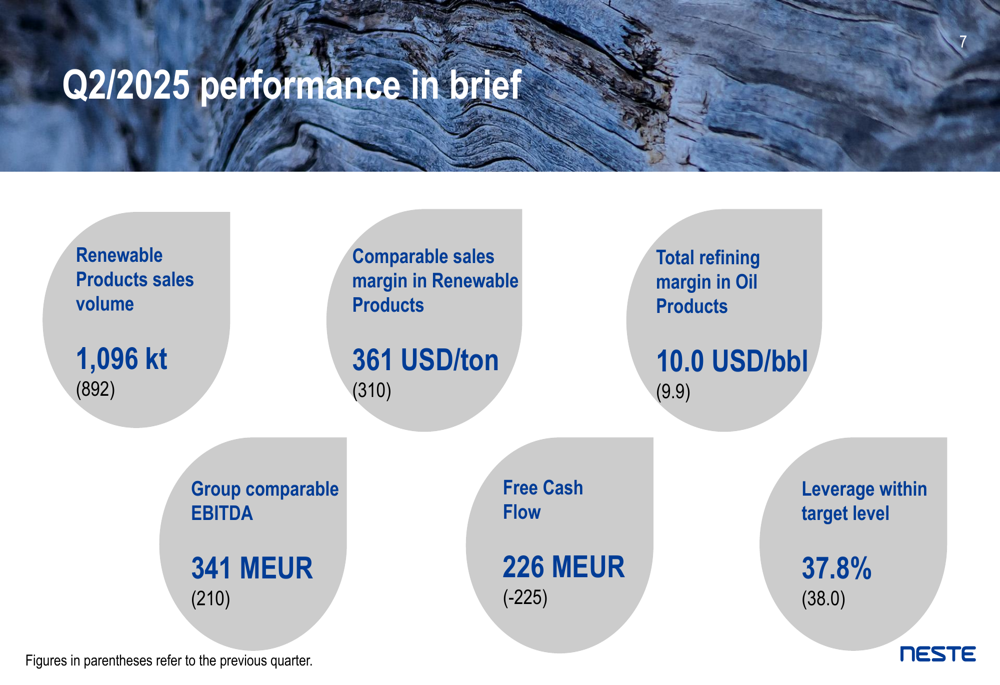

Neste’s Q2 2025 showed broad-based improvement across all key metrics compared to the previous quarter. The company achieved record high renewable sales volumes while successfully turning its cash flow positive.

As shown in the following comprehensive performance overview:

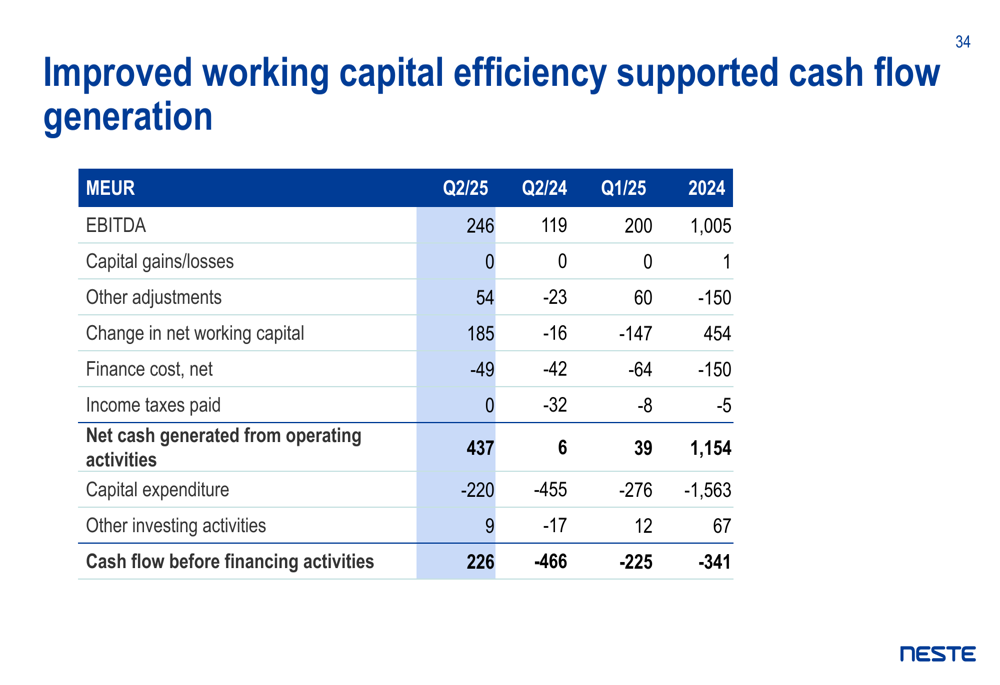

Free cash flow turned strongly positive at 226 million euros, compared to negative 225 million euros in Q1, while leverage remained stable at 37.8%, slightly below the company’s target level of 40%. The renewable products segment saw sales volumes increase to 1,096 kilotons from 892 kilotons in Q1, with comparable sales margin improving to 361 USD/ton from 310 USD/ton. Oil Products also showed modest improvement with total refining margin at 10.0 USD/bbl compared to 9.9 USD/bbl in the previous quarter.

The detailed financial results demonstrate the extent of the recovery across all segments:

Segment Performance

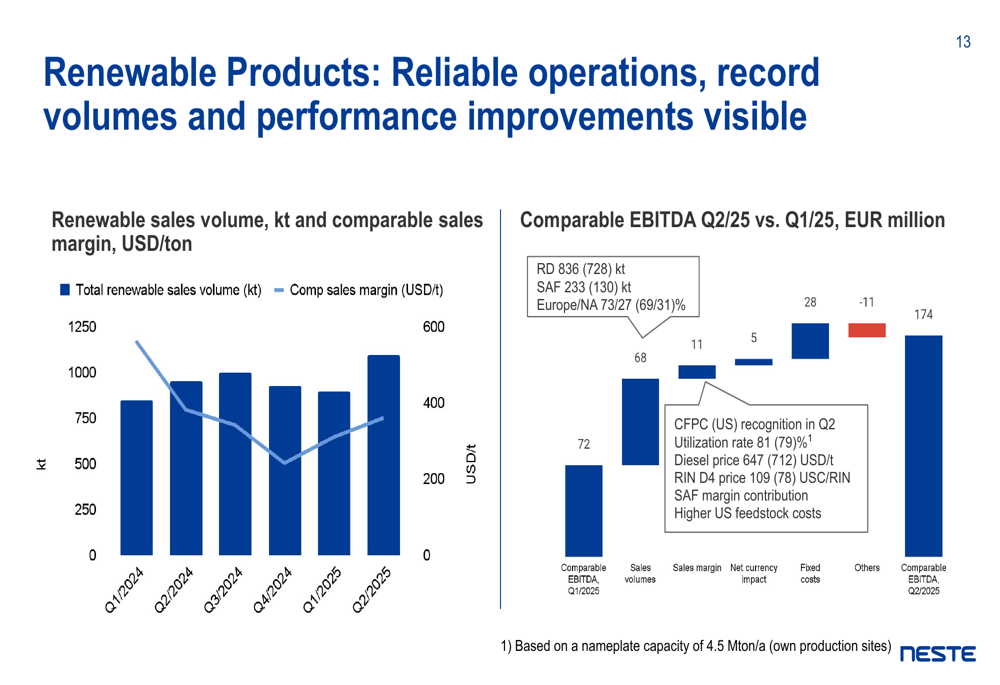

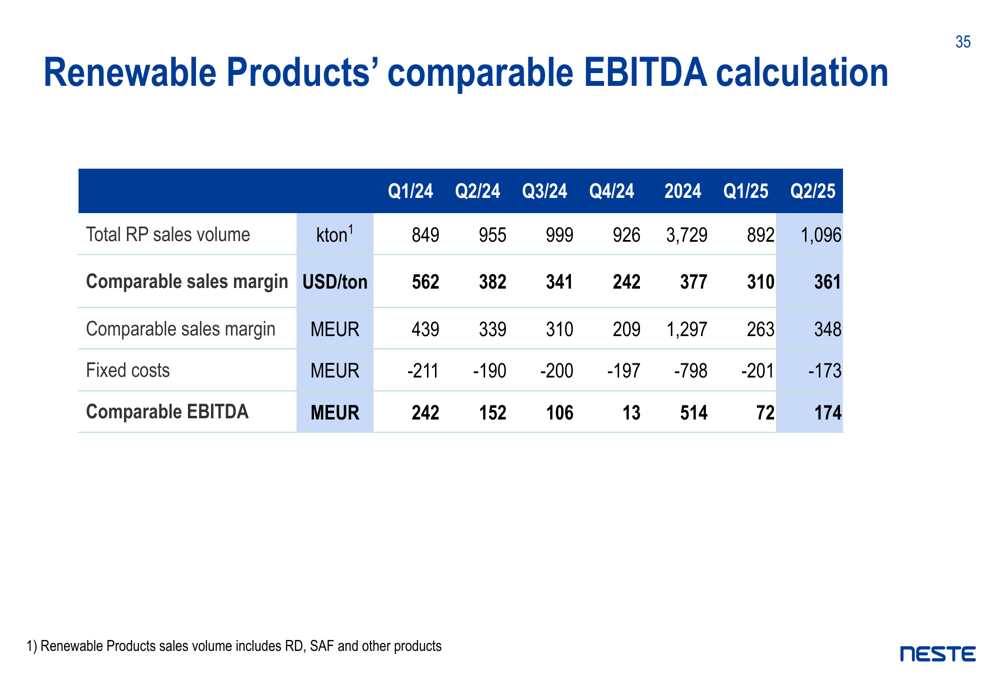

The Renewable Products segment showed the most dramatic improvement, with comparable EBITDA more than doubling from 72 million euros in Q1 to 174 million euros in Q2. This was driven by record high sales volumes and improved sales margins, despite continued high feedstock prices.

The following chart illustrates the factors contributing to this significant improvement:

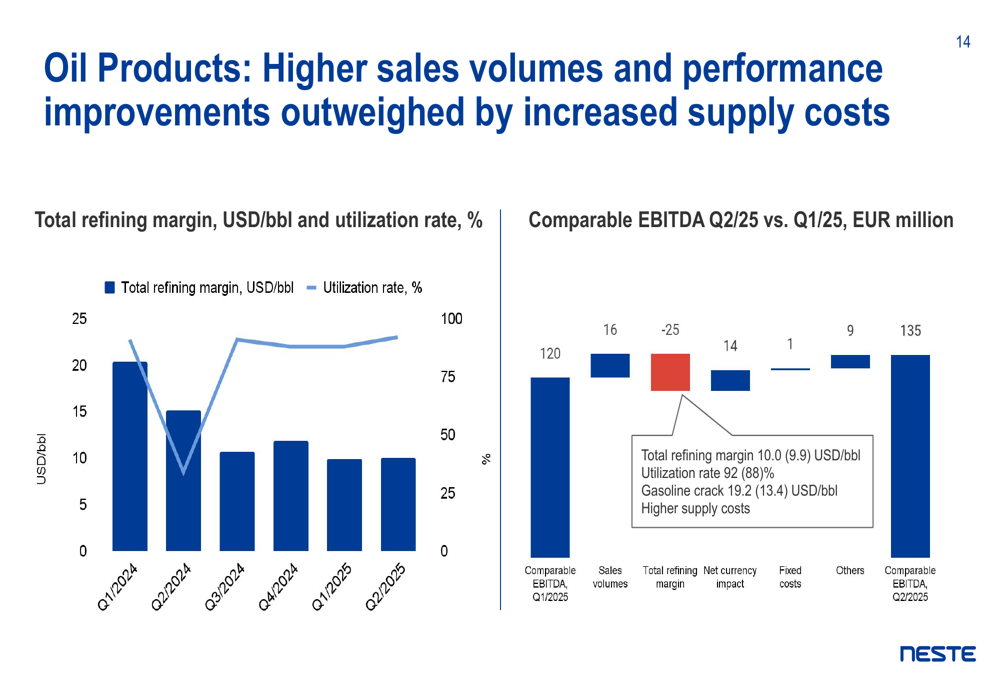

Oil Products also showed positive momentum, with comparable EBITDA increasing from 120 million euros to 135 million euros quarter-on-quarter. This improvement came despite some higher supply costs, as shown in the breakdown below:

The Marketing & Services segment nearly doubled its comparable EBITDA from 17 million euros to 32 million euros, with the company noting that "successful commercial operations" supported this strong performance despite some volume challenges.

Strategic Initiatives

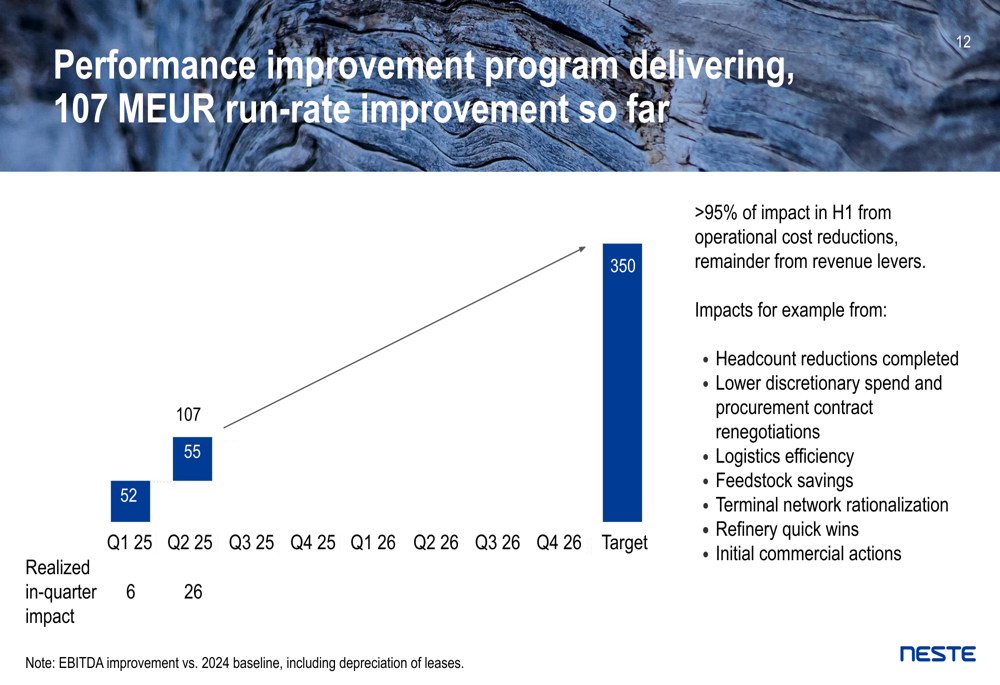

Neste’s performance improvement program is showing tangible results, delivering a 107 million euro annualized run rate improvement by the end of H1 2025, on track toward the target of 350 million euros by the end of 2026. The company noted that over 95% of the impact in H1 came from operational cost reductions, including headcount reductions and lower discretionary spending.

The progress of this critical initiative is illustrated in the following chart:

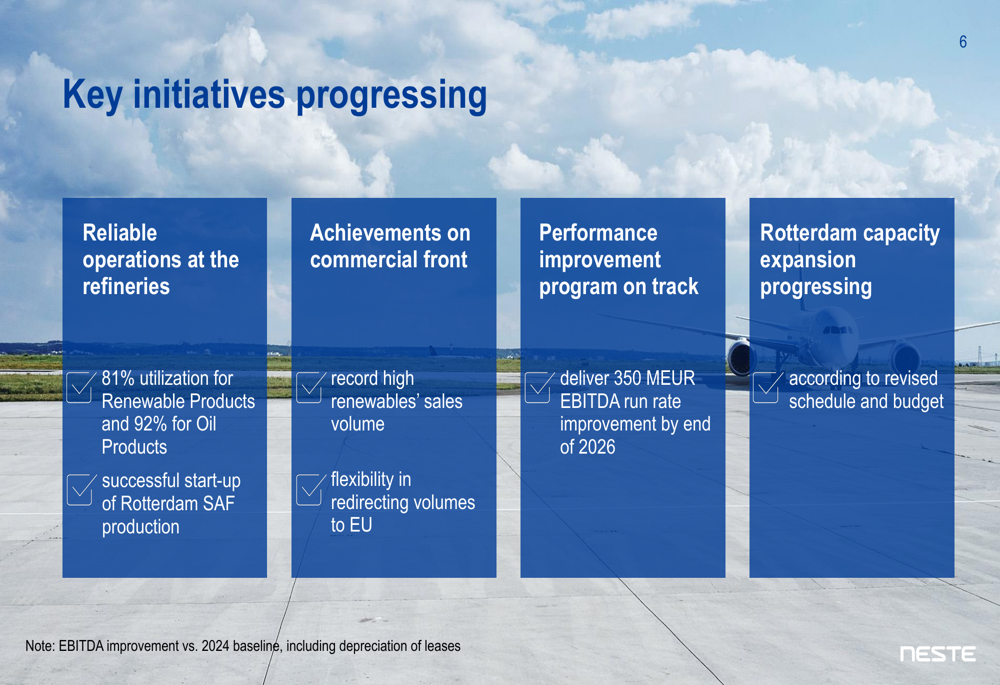

The company highlighted several key strategic initiatives that are progressing well, including the successful start-up of Sustainable Aviation Fuel (SAF) production in Rotterdam. Neste claims to be the world’s largest SAF producer, and by 2027, its Rotterdam SAF production capacity alone will be sufficient to meet the entire ReFuelEU mandate. The company has also strengthened collaborations with global clients including DHL, Amazon (NASDAQ:AMZN), and Fedex during 2025.

As shown in the following overview of key initiatives:

Forward-Looking Statements

Neste maintained its guidance for 2025, expecting higher sales volumes in both Renewable Products and Oil Products compared to 2024. The company anticipates that the Group’s comparable total fixed costs in 2025 will be below 2024 levels, excluding one-off costs. Capital expenditure for 2025 is estimated at approximately 1.0-1.2 billion euros.

The company’s financial targets for 2025-2026 remain unchanged, with a focus on achieving the 350 million euro EBITDA run rate improvement by the end of 2026 and maintaining leverage below 40%:

Regarding market conditions, Neste acknowledged that uncertainty in global trade and geopolitics continues to cause market volatility. The company expects the market for renewable fuels to remain oversupplied in 2025, presenting ongoing challenges despite the positive regulatory developments supporting long-term demand.

The improved cash flow generation is particularly noteworthy given the challenging market environment:

Neste’s detailed breakdown of its Renewable Products segment, which remains the strategic focus of the company, shows the improvement in both volumes and margins that drove the Q2 recovery:

Despite the oversupplied market conditions, Neste’s global presence across three continents and its ability to process a wide range of feedstocks provide competitive advantages that are helping the company navigate the current environment. The company remains focused on capturing market opportunities while ensuring safe and reliable operations, as it continues to benefit from supportive regulatory developments in key markets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.