Is this U.S.-China selloff a buy? A top Wall Street voice weighs in

Introduction & Market Context

Neuronetics , Inc. (NASDAQ:STIM), a leader in transcranial magnetic stimulation (TMS) therapy for mental health disorders, presented its Q1 2025 corporate overview on May 6, 2025, highlighting the company’s transformation following its strategic acquisition of Greenbrook TMS. The presentation showcased strong revenue growth and outlined a path to profitability, though recent market activity suggests investors may have mixed reactions to the company’s progress.

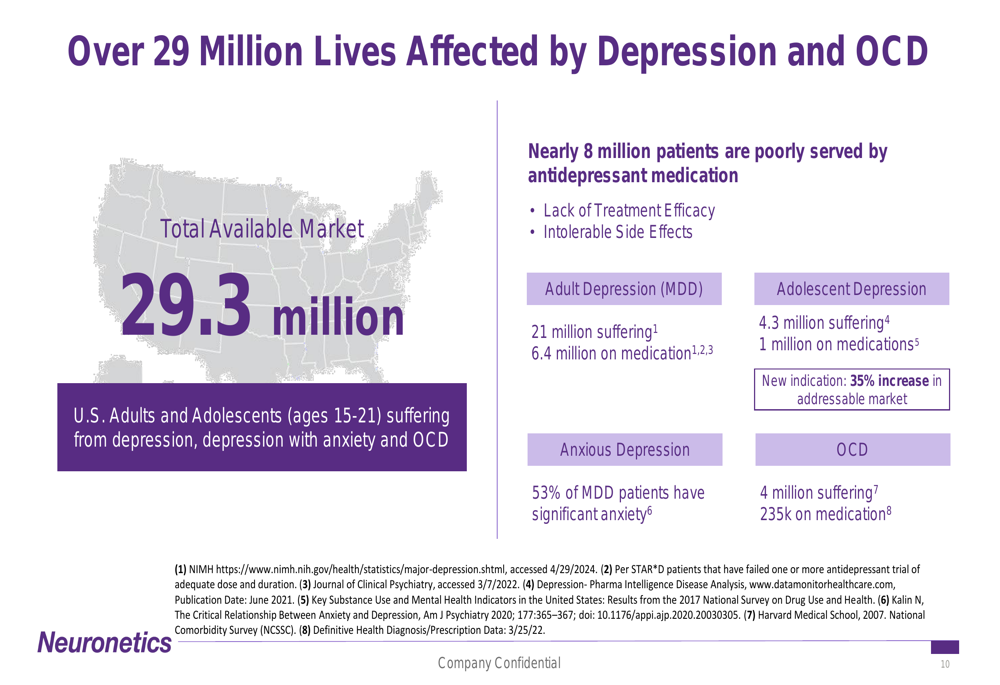

The mental health treatment market represents a significant opportunity, with over 29 million lives affected by depression and obsessive-compulsive disorder (OCD) in the United States alone. Neuronetics is positioning itself to address this market through its expanded capabilities and treatment network.

As shown in the following slide detailing the market opportunity:

Strategic Transformation Through Acquisition

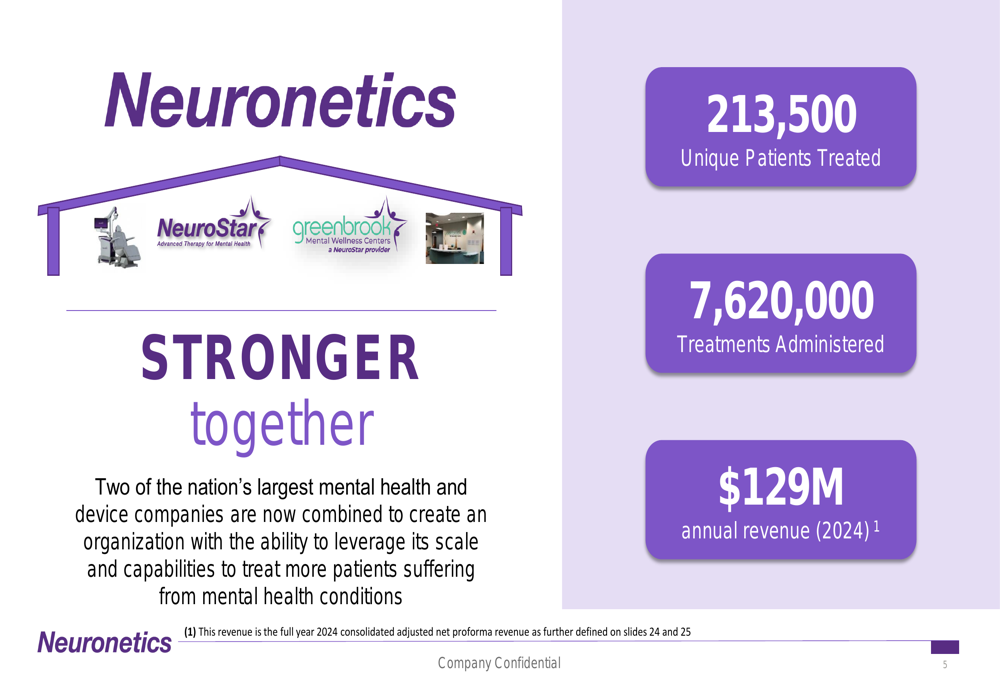

The cornerstone of Neuronetics’ strategy is the combination of its NeuroStar TMS technology business with Greenbrook’s treatment center network, creating what the company describes as a "stronger together" entity. This integration combines NeuroStar’s position as a market leader in TMS technology with Greenbrook’s extensive network of treatment clinics.

The combined company now reports impressive scale metrics, including 213,500 unique patients treated and over 7.6 million treatments administered, generating $129 million in annual revenue for 2024.

As illustrated in this overview of the combined entity:

The acquisition has significantly expanded Neuronetics’ commercial footprint, with 95 Greenbrook treatment clinics across 15 states complementing the broader network of over 375 Better Me Provider (BMP) practices in 49 states. This expanded presence gives Neuronetics both manufacturing and service delivery capabilities, creating a vertically integrated mental health treatment company.

Financial Performance and Outlook

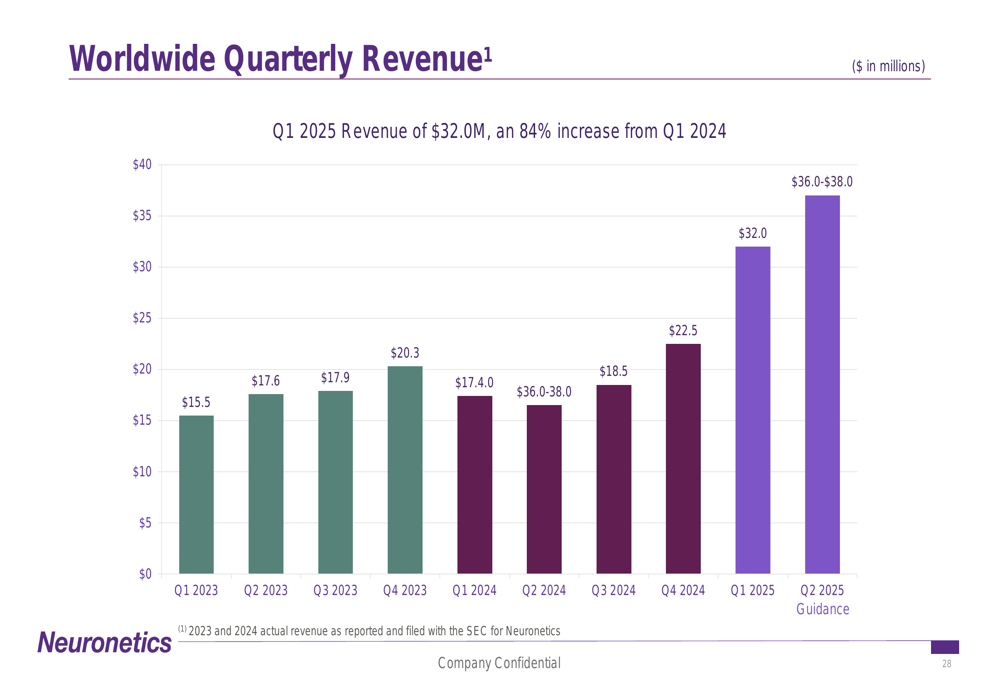

Neuronetics reported Q1 2025 revenue of $32.0 million, representing an 84% increase from Q1 2024, largely driven by the Greenbrook acquisition. However, on an adjusted basis that accounts for the combined entity, Q1 2025 revenue represents a more modest 7% year-over-year increase.

The quarterly revenue trend is visualized in the following chart:

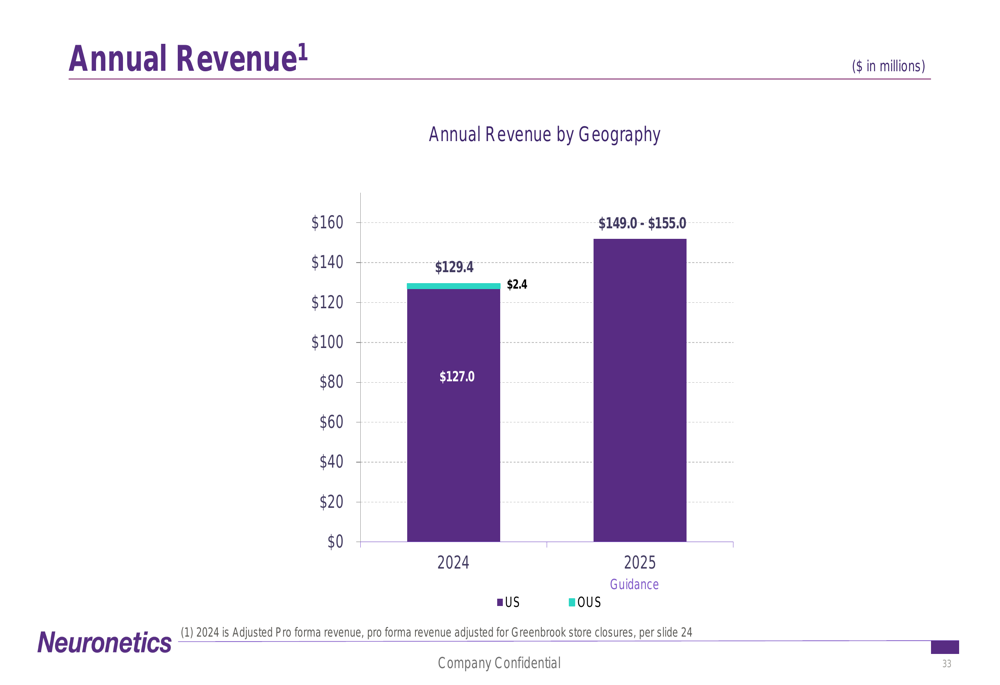

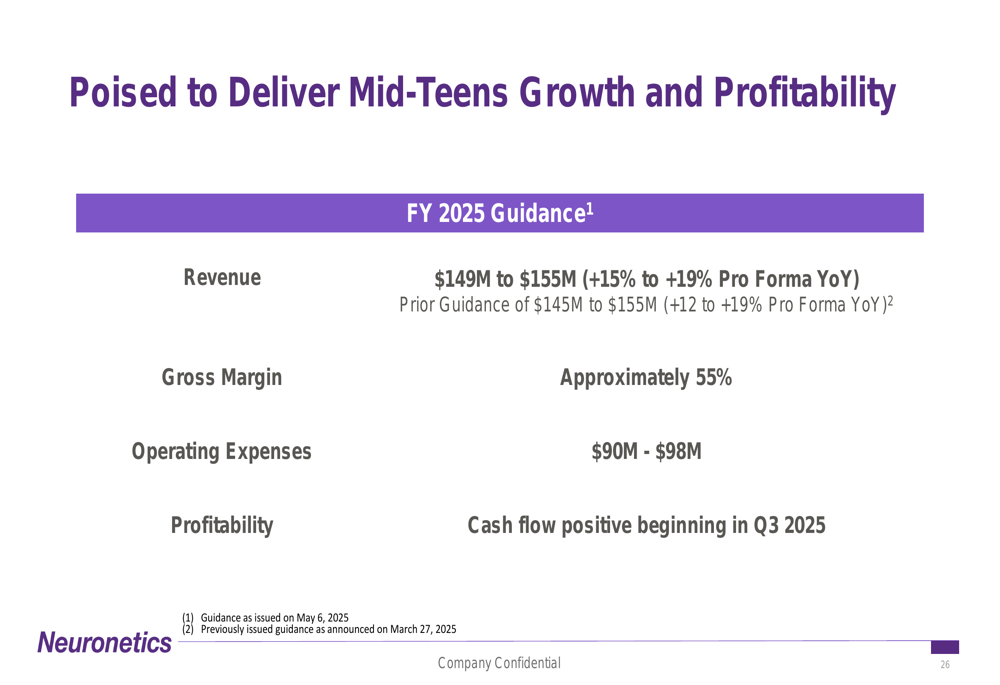

For the full year 2025, Neuronetics has provided revenue guidance of $149 million to $155 million, representing 15% to 19% year-over-year growth on a pro forma basis. The company also expects to achieve a gross margin of approximately 55%.

The company’s annual revenue projection is shown here:

Despite the strong revenue growth, Neuronetics continues to operate at a loss, reporting a Q1 2025 operating loss of $11.0 million, representing 34% of revenue. This marks a slight improvement from Q1 2024’s operating loss of 39% of revenue. The company’s gross margin decreased significantly from 75% in Q1 2024 to 49% in Q1 2025, likely reflecting the integration of Greenbrook’s service-based business model.

Cost Synergies and Path to Profitability

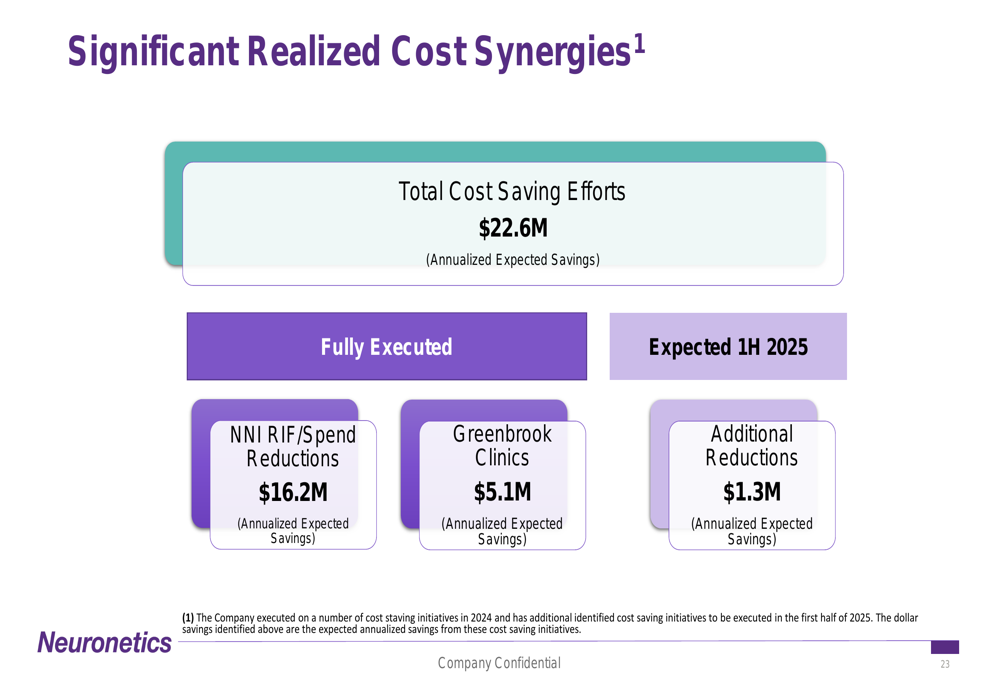

A key element of Neuronetics’ strategy is realizing cost synergies from the Greenbrook acquisition. The company reports having executed $21.3 million in cost savings, with an additional $1.3 million expected in the first half of 2025, bringing total cost synergies to $22.6 million.

As detailed in this breakdown of cost savings:

These cost reductions, combined with projected revenue growth, form the foundation of Neuronetics’ path to profitability. The company expects to become cash flow positive beginning in Q3 2025, a significant milestone that would mark its transition from growth-focused to sustainable operations.

The company’s financial guidance and profitability timeline are summarized here:

Growth Initiatives and Market Opportunity (SO:FTCE11B)

Neuronetics is pursuing multiple growth initiatives across both its network clinics and customer clinics. For network clinics, the company is focusing on patient identification and education, expanding the continuum of care, and implementing operational best practices. For customer clinics, key initiatives include expanding the Better Me Provider network, enhancing patient education, and broadening services to existing customers.

The company’s Better Me Program (BMP) has demonstrated significant impact, with BMP clinics treating three times more patients than non-BMP clinics. The program has also reduced the time from patient interest to treatment initiation from 84 days in 2023 to 38 days in 2024.

Another growth driver is the SPRAVATO program, which leverages Greenbrook’s infrastructure to deliver esketamine nasal spray treatment for treatment-resistant depression. Neuronetics expects to have nearly 85 treatment centers offering SPRAVATO by the end of fiscal 2025.

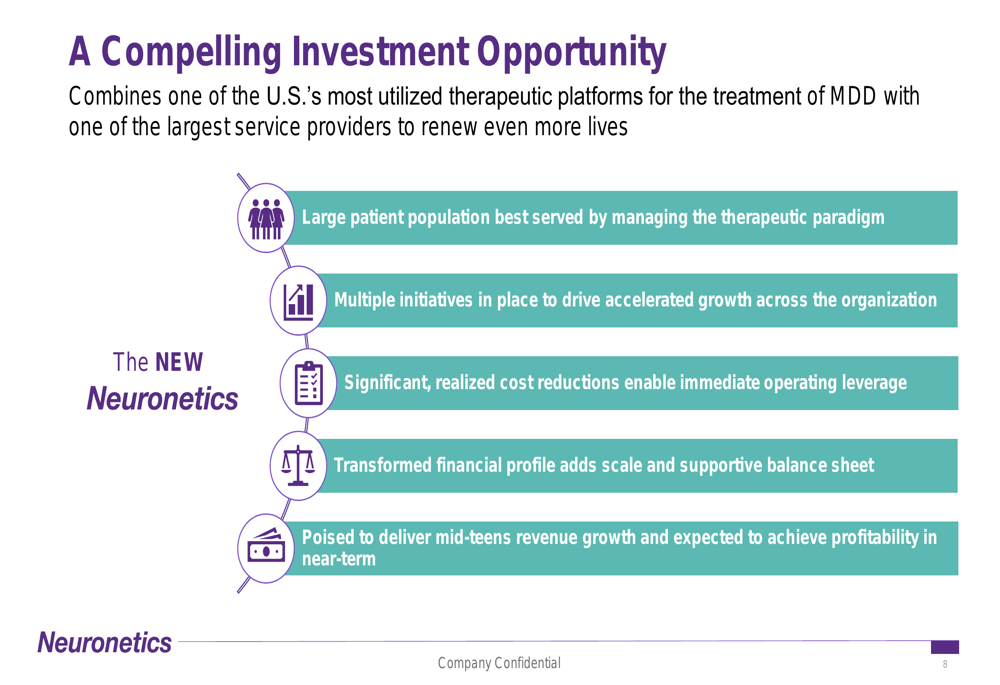

The company’s investment thesis is summarized in this slide:

Clinical Efficacy and Market Differentiation

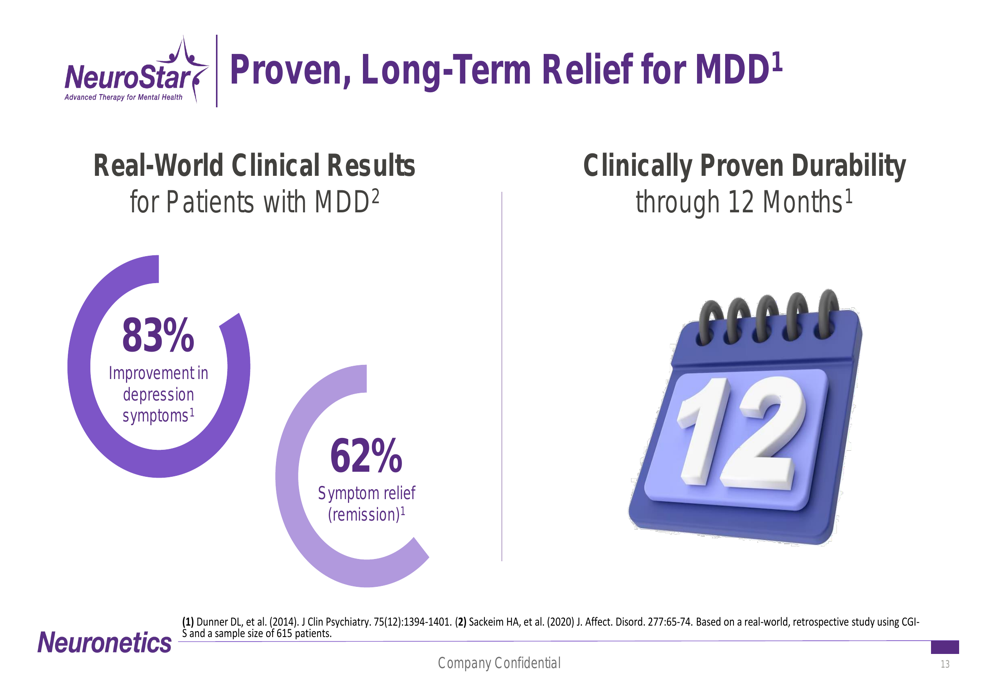

Neuronetics emphasizes the clinical efficacy of its NeuroStar TMS therapy, citing real-world data showing 83% improvement in depression symptoms and 62% symptom relief (remission) among patients with major depressive disorder (MDD). The company also highlights the durability of these results through 12 months.

As shown in this clinical outcomes summary:

A significant competitive advantage is NeuroStar’s status as the first FDA-cleared TMS treatment for adolescent depression. This expansion into the adolescent market opens up access to the 4.3 million adolescents suffering from depression in the United States.

Investor Considerations

While Neuronetics presents a compelling growth story and path to profitability, investors should consider several factors. The company’s recent financial performance shows mixed signals, with strong revenue growth but continued operating losses. The significant drop in gross margin from 75% to 49% year-over-year warrants attention, though this likely reflects the integration of Greenbrook’s different business model.

According to the recent earnings report, Neuronetics reported a Q4 2024 net loss of $0.33 per share, below the forecasted loss of $0.24 per share, indicating challenges in achieving profitability targets. However, the company’s revenue beat expectations, suggesting strong demand for its products and services.

The most recent market data shows Neuronetics stock (NASDAQ:STIM) trading at $4.50 as of May 5, 2025, with a significant premarket drop of 16.67% on the following day, indicating potential investor concerns despite the positive narrative presented in the corporate overview.

For investors, the key question remains whether Neuronetics can successfully execute its integration strategy, realize projected cost synergies, and achieve cash flow positivity by Q3 2025 as promised. The company’s expanded scale and market presence provide a stronger foundation, but the path to sustainable profitability will require disciplined execution in the quarters ahead.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.