Moody’s downgrades Senegal to Caa1 amid rising debt concerns

Introduction & Market Context

Neuronetics Inc. (NASDAQ:STIM), a leader in transcranial magnetic stimulation (TMS) therapy for mental health disorders, presented its Q2 2025 corporate update on August 5, 2025, highlighting significant revenue growth following its merger with Greenbrook. The presentation comes as the mental health technology sector faces increasing demand amid ongoing challenges in treatment-resistant depression.

The company’s stock has shown considerable volatility, with a beta of 1.92 according to recent data. Despite impressive six-month gains of 278%, STIM is facing investor scrutiny over profitability concerns, with shares down 10.09% in premarket trading following the presentation.

Quarterly Performance Highlights

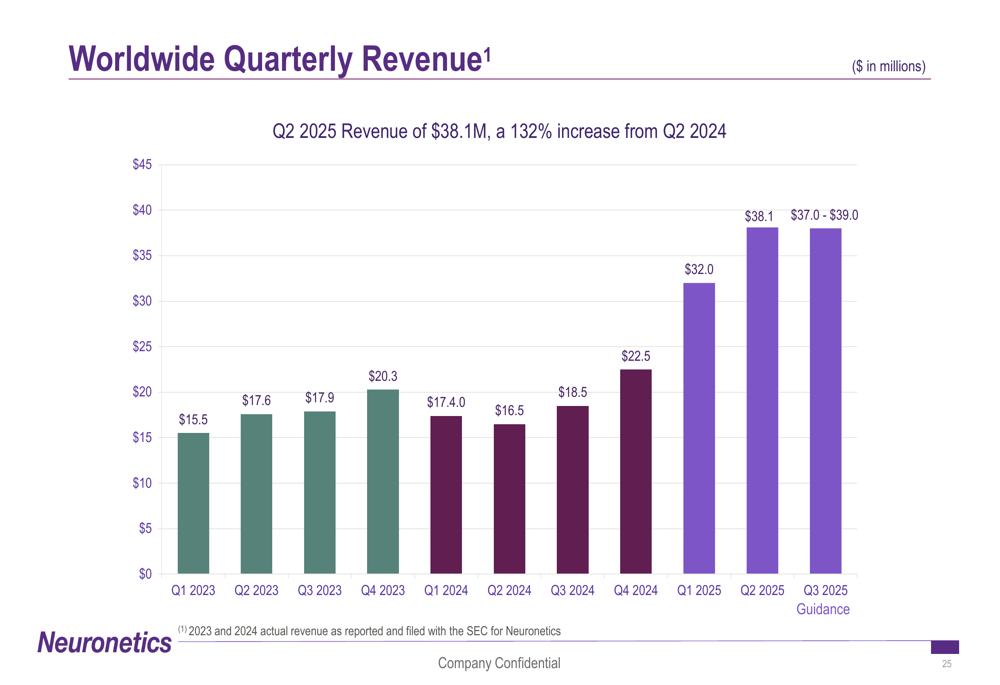

Neuronetics reported Q2 2025 revenue of $38.1 million, representing a substantial 132% increase compared to Q2 2024. This growth reflects the successful integration of Greenbrook’s operations and expansion of the company’s treatment network.

As shown in the following chart of quarterly revenue growth:

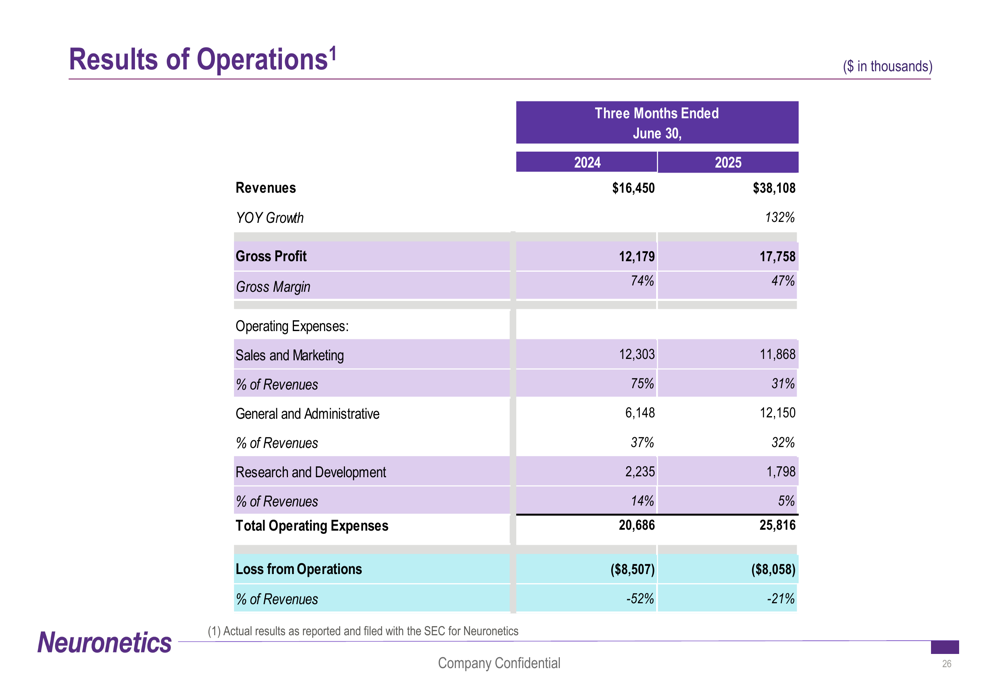

The company’s gross profit increased from $12.2 million in Q2 2024 to $17.8 million in Q2 2025, though operating expenses have also grown significantly following the Greenbrook acquisition. The detailed financial results demonstrate the scale of the combined operations:

Despite the impressive revenue growth, Neuronetics continues to face profitability challenges. The company’s Q1 2025 earnings release showed a net loss of $0.21 per share, missing analyst expectations of a $0.19 loss, which contributed to a 21.79% stock drop at that time.

Strategic Initiatives

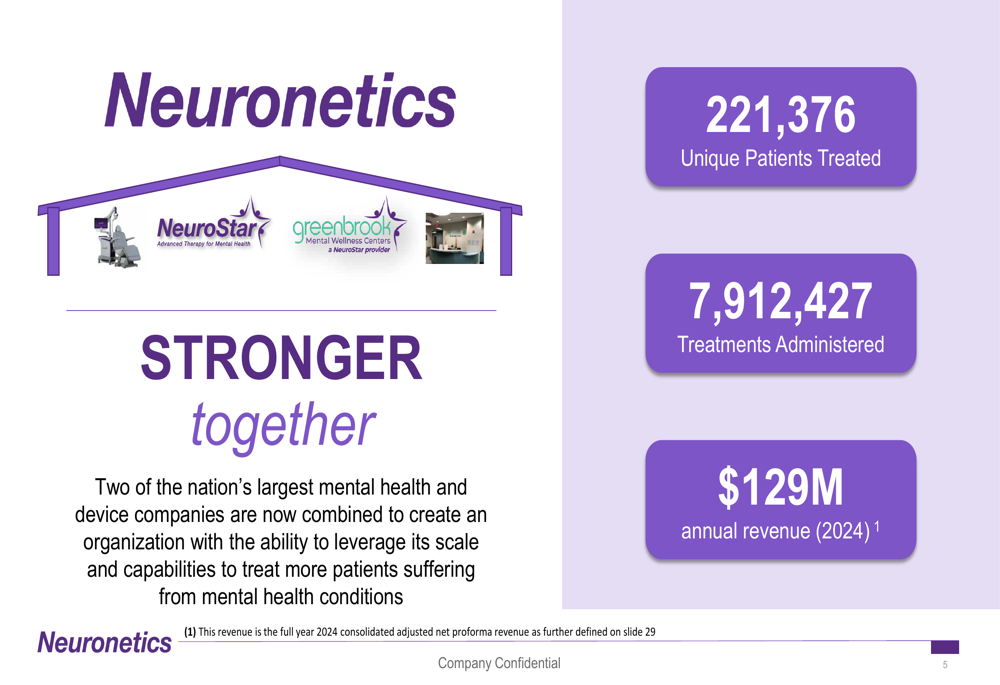

The merger between Neuronetics and Greenbrook has created what management describes as a diversified business model combining technology development with direct patient care. The company now operates 95 treatment clinics in 15 states through Greenbrook, while its Better Me Provider (BMP) program encompasses over 390 clinics across 49 states.

The company highlighted key metrics demonstrating its market position:

A major focus of Neuronetics’ growth strategy is the expansion of TMS treatment for adolescents, following FDA clearance as the first TMS treatment for adolescent depression. Unlike adult applications, NeuroStar can be used as a first-line treatment for adolescents without requiring prior medication failures.

The company is also expanding its SPRAVATO (esketamine) program, which currently operates in 77 treatment centers with plans to reach over 80 centers by the end of fiscal 2025. This treatment complements TMS therapy by addressing treatment-resistant depression through a different mechanism.

Forward-Looking Statements

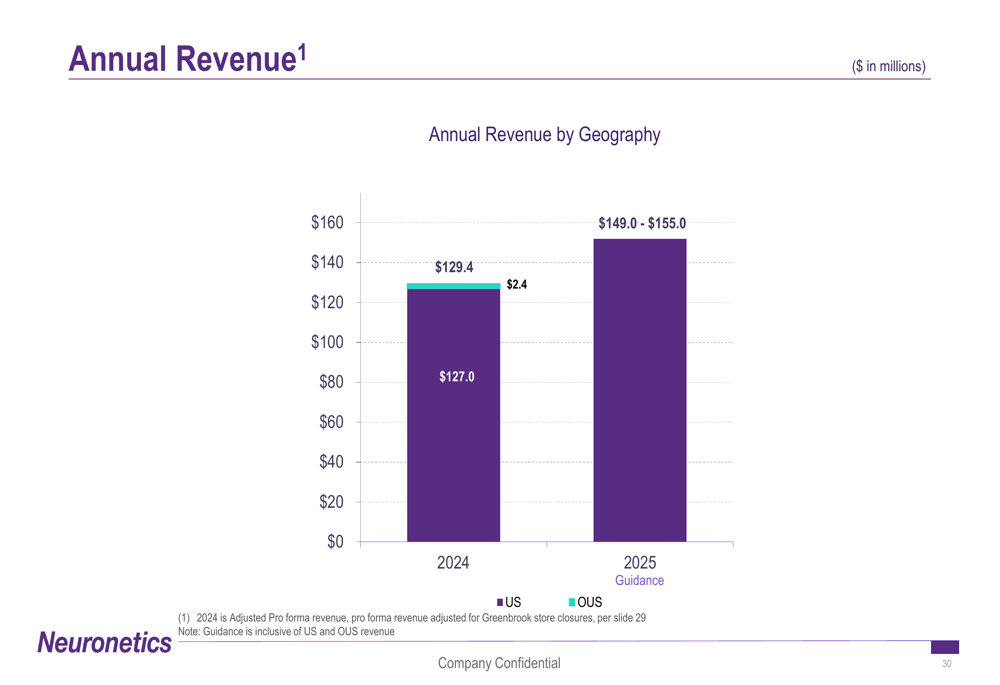

Neuronetics provided financial guidance for fiscal year 2025, projecting revenue between $149 million and $155 million, representing 15-19% year-over-year growth on a pro forma basis. The company expects gross margins between 48% and 50%, with operating expenses ranging from $100 million to $105 million.

Management anticipates achieving positive cash flow from operations by Q4 2025, with Q3 cash flow from operations projected between $(3) million and $0 million. This progression toward profitability is illustrated in the annual revenue forecast:

The company’s Better Me Program (BMP) remains a key growth driver, with BMP clinics treating 3.3 times more patients than non-BMP clinics. The program has significantly reduced the time from patient interest to treatment initiation, from 96 days in 2023 (pre-BMP) to 42 days in Q4 2024 and Q1 2025.

Market Reaction

Despite the strong revenue growth and positive outlook, investors appear concerned about Neuronetics’ path to profitability. The stock was down 10.09% in premarket trading following the presentation, suggesting the market remains cautious about the company’s ability to translate revenue growth into bottom-line results.

This reaction follows a pattern seen after the Q1 2025 earnings release, when the stock dropped nearly 22% despite revenue exceeding expectations. The company’s financial position as of June 30, 2025, showed cash and cash equivalents of $10.97 million, with long-term debt of $55.54 million, highlighting the importance of achieving positive cash flow in the coming quarters.

The market’s response underscores the challenges Neuronetics faces in balancing growth investments with profitability goals as it continues to expand its treatment network and technology platform in the competitive mental health sector.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.