US stock futures flat after Wall St drops on Trump tariffs, soft jobs data

Newell Brands Inc (NASDAQ:NWL) shared its Q1 2025 investor presentation on April 30, highlighting progress in its multi-year turnaround strategy despite ongoing sales challenges. The consumer goods company, which owns brands like Rubbermaid, Sharpie, and Coleman, reported improving financial metrics while continuing to implement significant operational changes.

Executive Summary

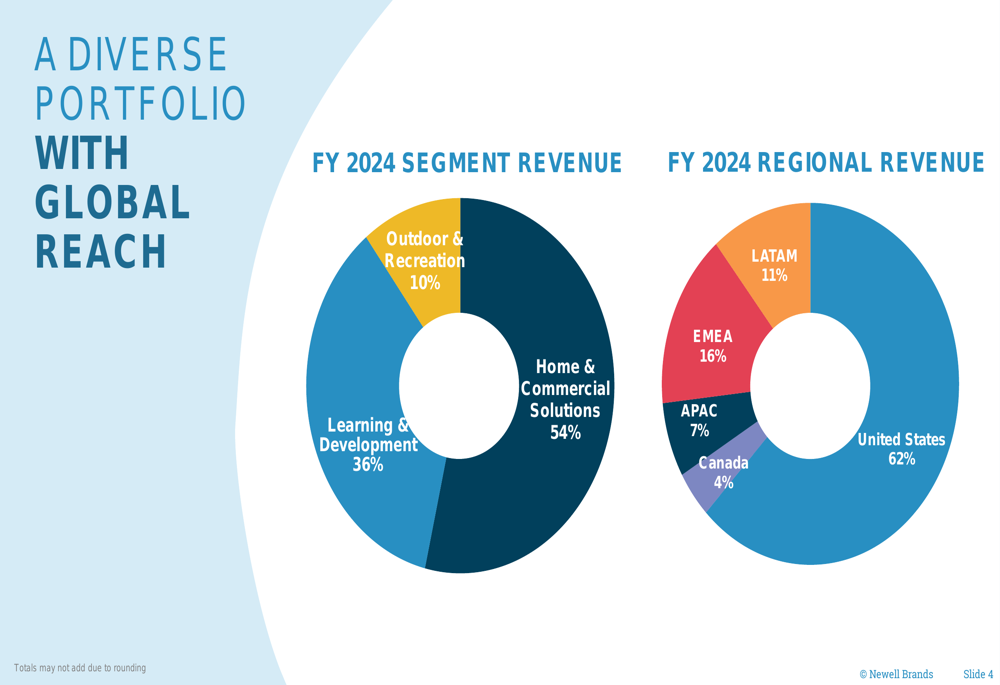

Newell Brands reported $7.6 billion in net sales and $900 million in normalized EBITDA for the year ending 2024. The company’s portfolio consists of 25 brands representing 90% of net sales, with operations concentrated in 10 countries accounting for 90% of revenue. International sales comprise 38% of the business, with the company employing approximately 24,000 people globally.

As shown in the following overview of Newell’s business:

The company’s revenue is diversified across three main segments: Home & Commercial Solutions (54%), Learning & Development (36%), and Outdoor & Recreation (10%). Geographically, the United States remains Newell’s largest market at 62% of revenue, followed by EMEA (16%), Latin America (11%), Asia-Pacific (7%), and Canada (4%).

Turnaround Strategy

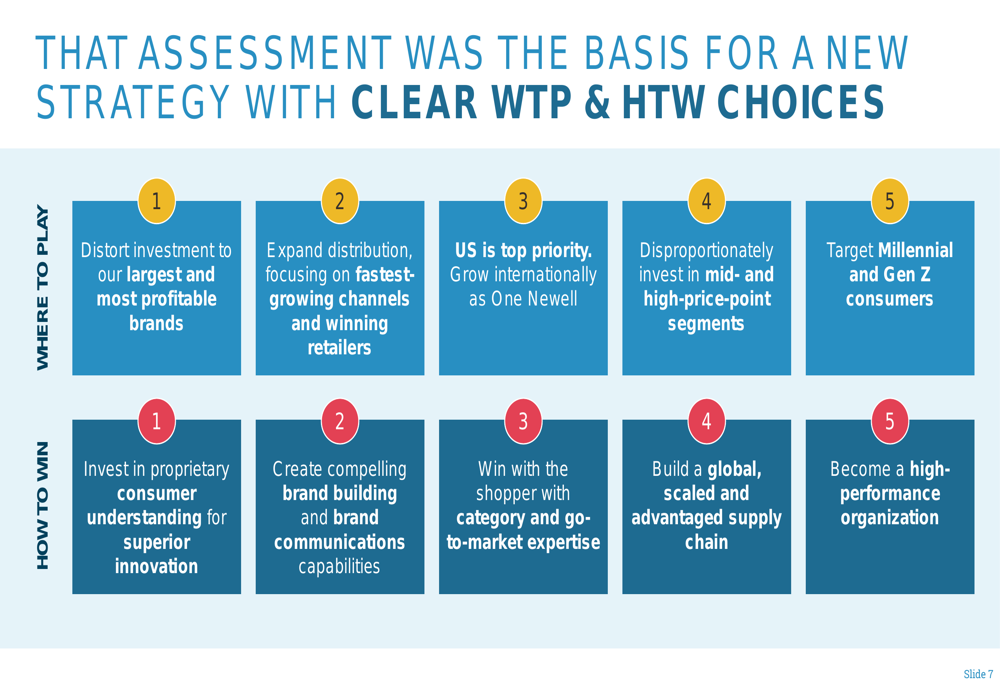

Newell Brands initiated its turnaround strategy in 2023 following a comprehensive capability assessment. The strategy is built around clear "Where to Play" and "How to Win" choices, focusing on improving topline performance, expanding margins, and enhancing cash flow.

The "Where to Play" strategy prioritizes investment in the largest and most profitable brands, expansion into faster-growing channels and retailers, focus on the US market, investment in mid- and high-price-point segments, and targeting Millennial and Gen Z consumers.

The "How to Win" approach emphasizes proprietary consumer understanding, brand building, shopper expertise, supply chain optimization, and creating a high-performance organization.

Chris Peterson, CEO of Newell Brands, has led significant changes to the company’s operating model, including establishing a consumer-first Global Brand Management organization, standardizing the International Operating Model, centralizing the U.S. sales team, creating a New Business Development Team, and centralizing Supply Chain, Finance and HR functions.

Simplification Initiatives

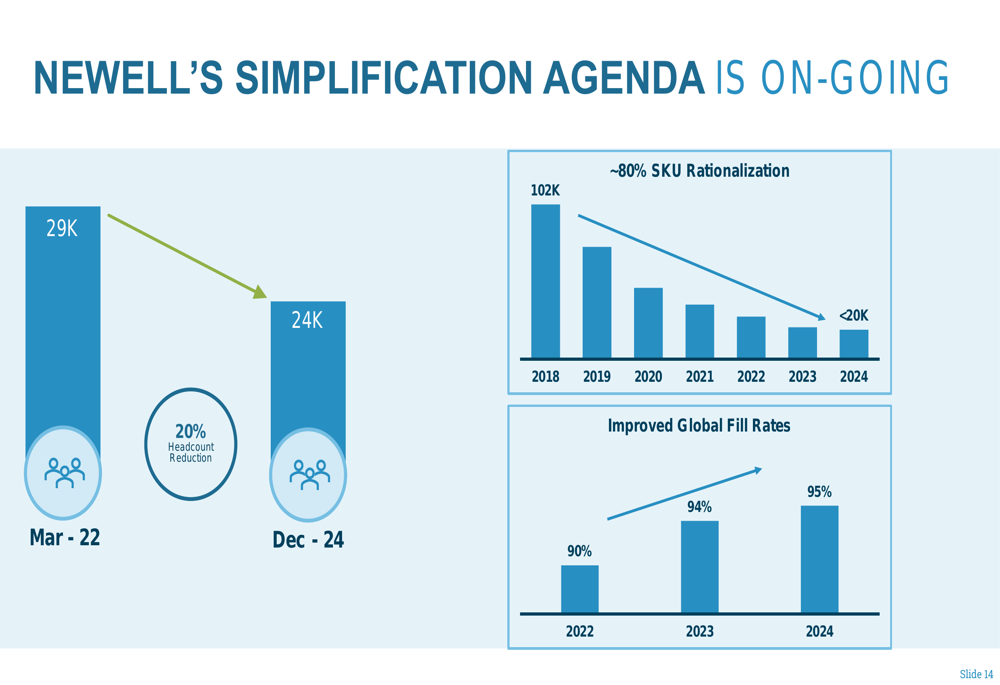

A key component of Newell’s turnaround has been its simplification agenda. The company has reduced headcount by 20% (from 29,000 in March 2022 to 24,000 in December 2024), rationalized SKUs by approximately 80% (from 102,000 in 2018 to under 20,000 in 2024), and improved global fill rates from 90% in 2022 to 95% in 2024.

The following chart illustrates these operational improvements:

Additionally, Newell has streamlined its brand portfolio from approximately 80 brands to around 55 brands, focusing resources on its most profitable and promising assets.

Innovation Pipeline

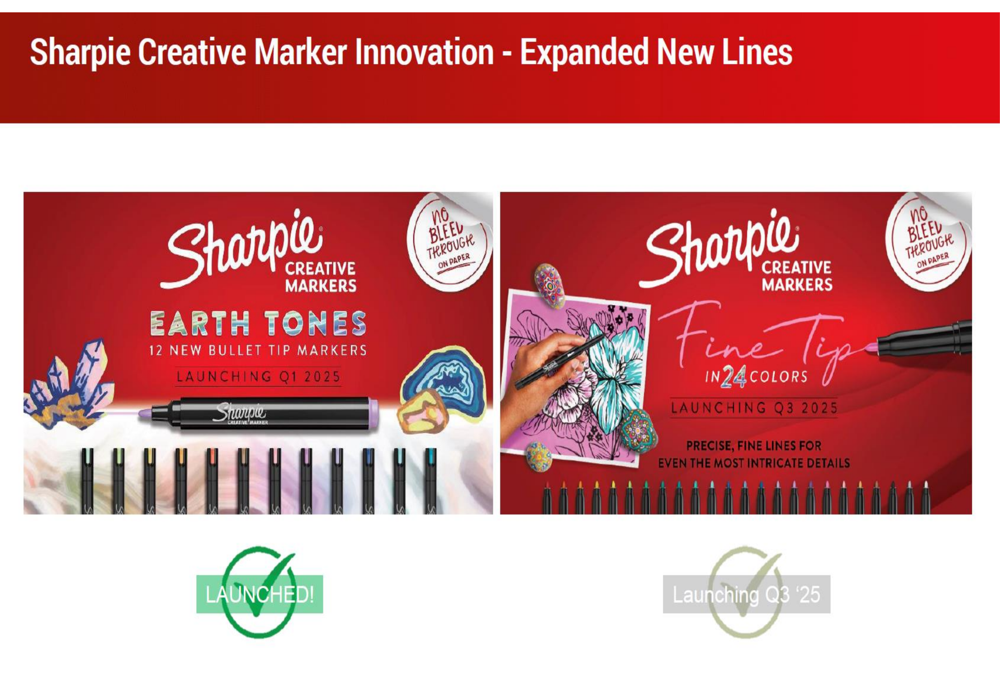

Newell is emphasizing consumer-driven innovation across its brand portfolio. The company has reinvented its consumer insights approach, established a project tiering system, eliminated small or dilutive projects, and focused its new product development funnel on the top 25 brands.

One example is the expansion of the Sharpie Creative Marker line with new Earth Tones colors launching in Q1 2025 and Fine Tip markers in 24 colors coming in Q3 2025:

Other innovation highlights include EXPO’s enhanced ink formulation with more vibrant colors launching in 2025:

And Graco (NYSE:GGG)’s EasyTurn™ 360 Convertible Car Seat, which features a 360-degree turning mechanism for easier access to the child:

Financial Performance

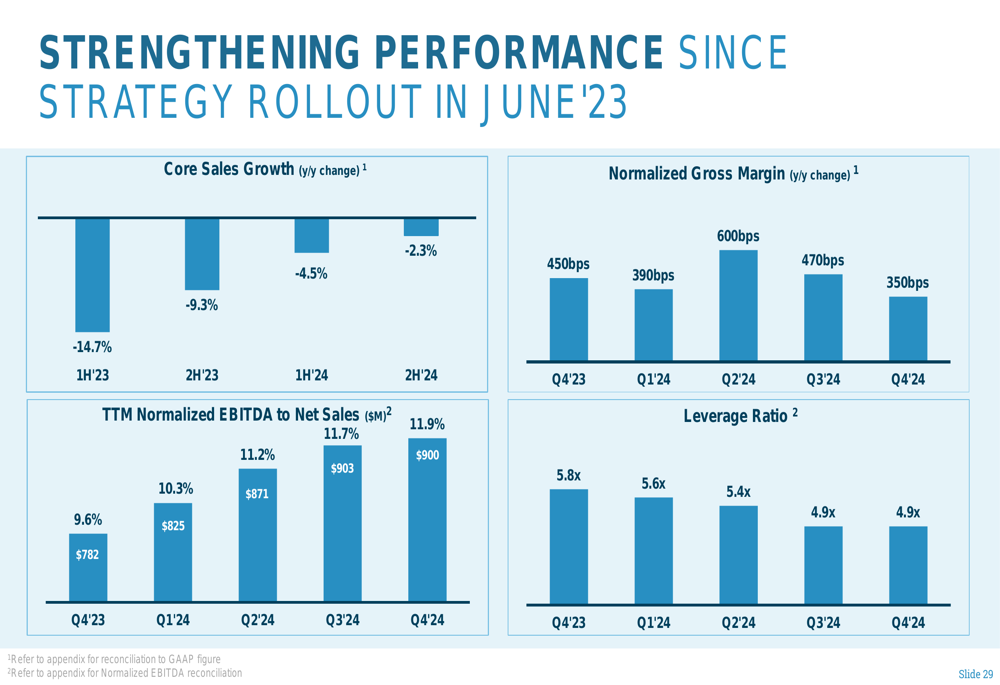

Since rolling out its new strategy in June 2023, Newell has shown improvement across key financial metrics. Core sales growth, while still negative, has improved from -14.7% in the first half of 2023 to -2.3% in the second half of 2024. Normalized gross margin has expanded, with year-over-year improvements of 450 basis points in Q4 2023 and 350 basis points in Q4 2024.

The company’s trailing twelve-month normalized EBITDA increased from $782 million in Q4 2023 to $900 million in Q4 2024, while its leverage ratio decreased from 5.8x to 4.9x during the same period.

The following chart demonstrates these improving trends:

These results align with the company’s Q2 2024 earnings report, which showed a core sales decline of 4.2% but gross margin expansion of 490 basis points. In that report, Newell raised its full-year guidance, expecting a core sales decline of 3-4% and a net sales decline of 6-7% for 2024.

Forward Outlook

Newell Brands has established long-term "evergreen" annual targets, including low single-digit core sales growth, 50 basis points of operating margin improvement annually, and approximately 90% free cash flow productivity.

The company’s capital allocation strategy prioritizes funding high-return internal growth opportunities, deleveraging to a 2.5x investment grade leverage ratio (down from the current 4.9x), and targeting a 30-35% dividend payout ratio.

While Newell’s stock has shown some recovery over the past year, with a reported 12.51% one-year price return as of mid-July 2024, it remains under pressure. The stock closed at $5.17 on April 29, 2025, and was trading down 2.32% in pre-market activity on April 30, suggesting investors remain cautious about the company’s turnaround prospects despite the improving financial metrics.

The company faces ongoing challenges, including consumer pressure from inflation outpacing wage gains and continued negative core sales growth. However, management remains optimistic about future performance, citing positive responses to its innovation pipeline, increased advertising and promotional activities, and significant supply chain savings expected to reduce cost of goods sold.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.