Hedge funds cut NFLX, keep big bets on MSFT, AMZN, add NVDA

Introduction & Market Context

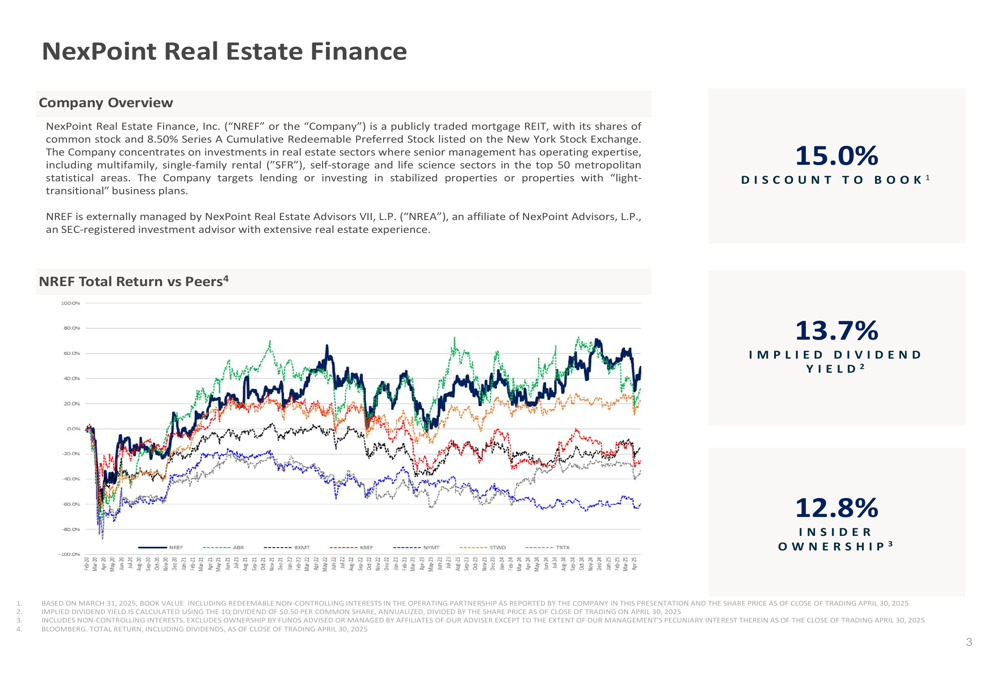

NexPoint Real Estate Finance, Inc. (NYSE:NREF) released its first quarter 2025 financial results on May 1, showing improved book value per share and maintaining its dividend despite challenging market conditions. The mortgage REIT, which focuses on investments in multifamily, single-family rental, self-storage, and life science sectors, continues to execute its diversification strategy while trading at a notable discount to book value.

The company’s presentation comes amid ongoing volatility in commercial real estate markets, with NREF’s stock trading down 3.51% to $14.63 on the day of the announcement, reflecting broader market concerns despite the company’s relatively stable performance.

Quarterly Performance Highlights

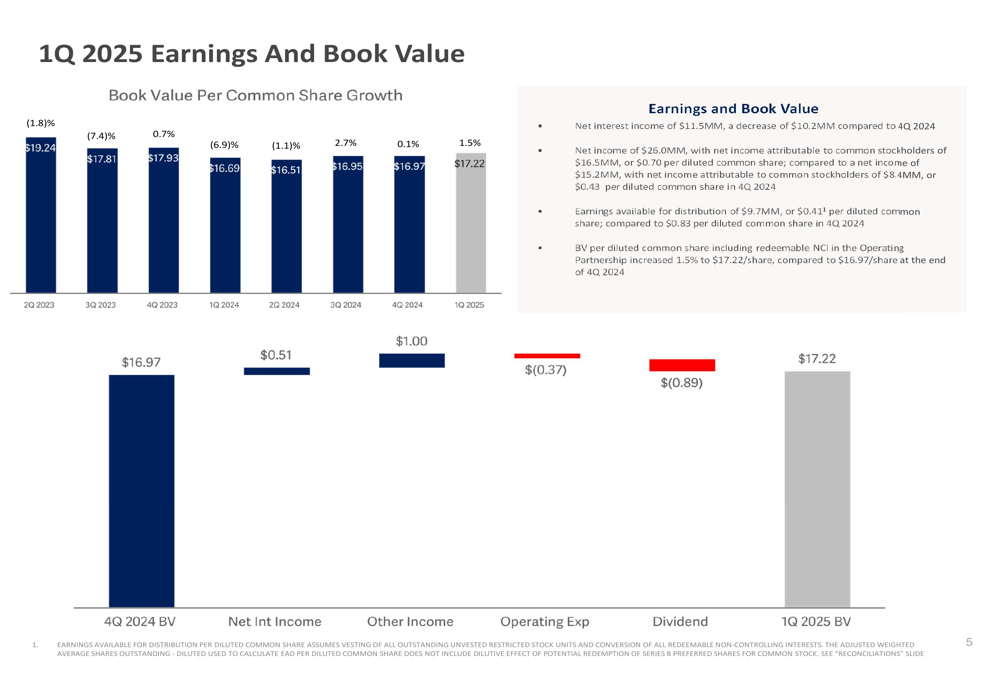

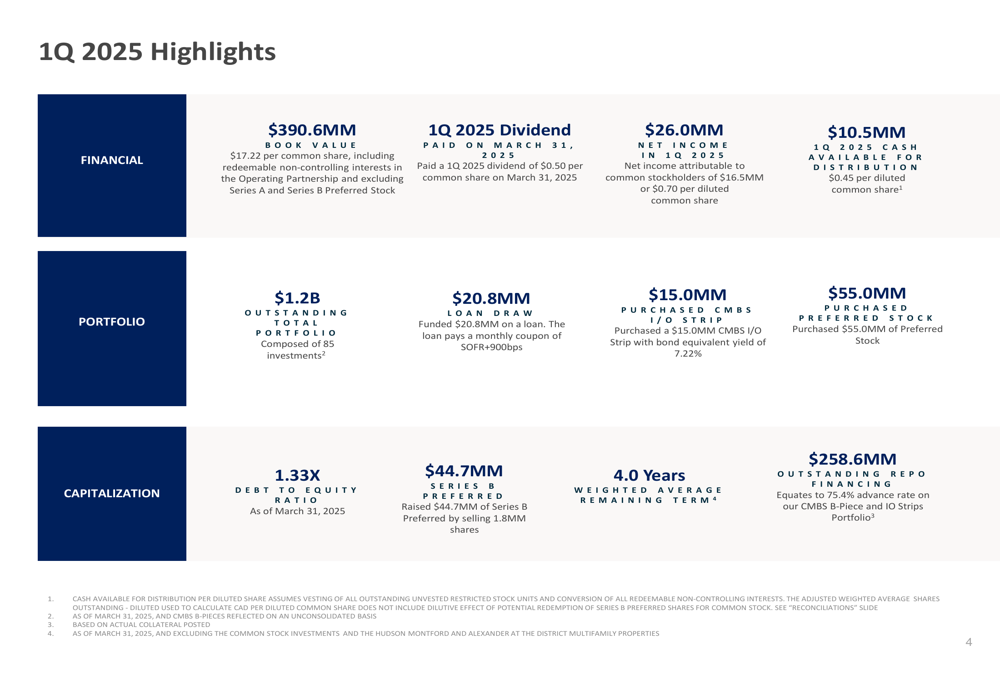

NexPoint reported a book value of $390.6 million ($17.22 per share) for Q1 2025, representing an increase from $16.97 per share in Q4 2024. Net income reached $26.0 million, with $16.5 million ($0.70 per share) attributable to common stockholders. Cash available for distribution (CAD) totaled $10.5 million ($0.45 per share).

As shown in the following chart detailing the company’s book value progression:

The company maintained its quarterly dividend at $0.50 per share, resulting in dividend coverage ratios of 1.40x based on EPS, 0.83x based on earnings available for distribution (EAD), and 0.90x based on CAD. This represents a strong EPS coverage but slightly undercovered dividends on an EAD and CAD basis.

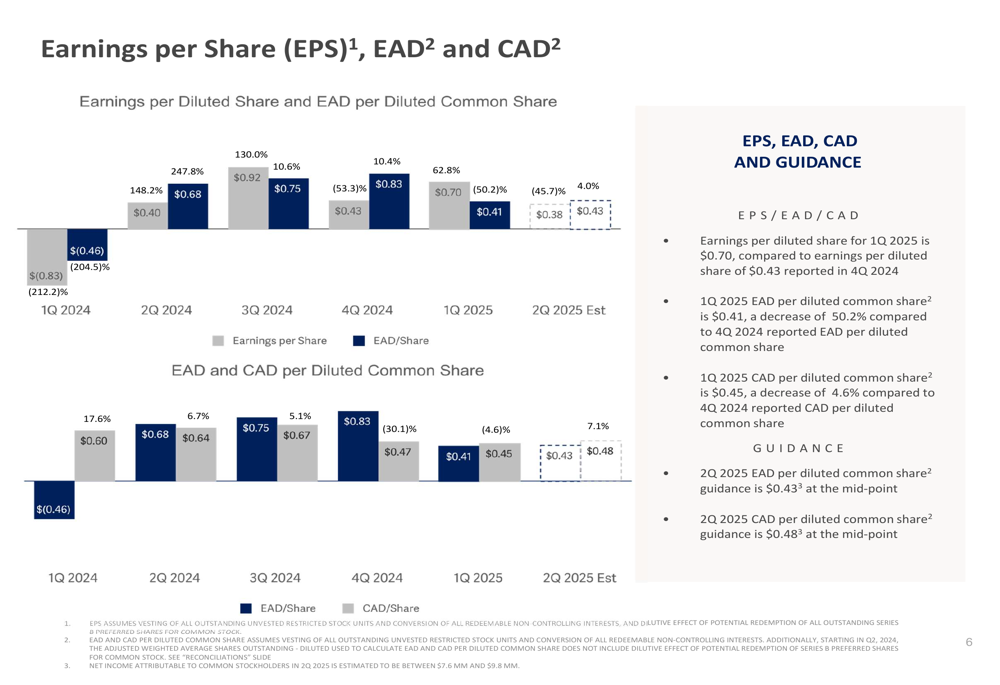

The following chart illustrates NREF’s earnings metrics over recent quarters:

Portfolio Composition and Strategy

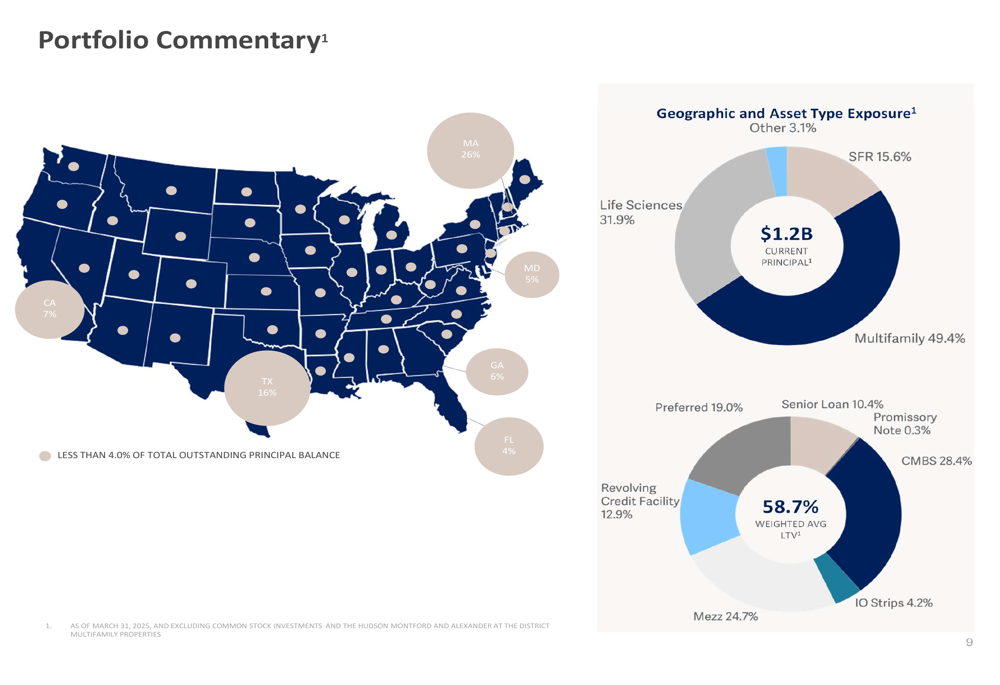

NexPoint’s investment portfolio stands at $1.2 billion, comprising 85 investments across various real estate sectors. The company maintains a defensive positioning with 75.2% of the portfolio in stabilized assets, a weighted average loan-to-value ratio of 58.7%, and a weighted average debt service coverage ratio of 1.46x.

The portfolio’s geographic and asset type diversification is illustrated in the following visualization:

The company’s strategy focuses on senior loans, CMBS investments, mezzanine debt, and preferred equity in short-duration lease-term assets. Life sciences represents the largest sector allocation at 31.9%, followed by multifamily at 49.4%, reflecting the company’s emphasis on sectors with strong fundamentals.

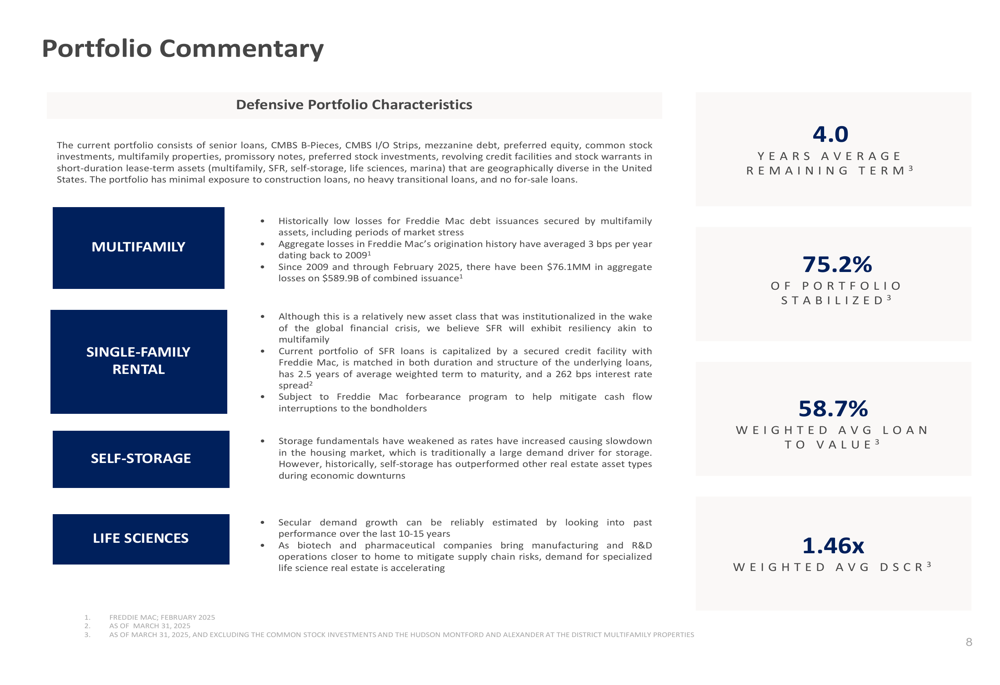

As shown in the following overview of the company’s defensive portfolio characteristics:

Financial Position and Outlook

NexPoint maintains a debt-to-equity ratio of 1.33x with outstanding repo financing of $258.6 million at a 75.4% advance rate. The company successfully raised $44.7 million through Series B preferred stock during the quarter, enhancing its capital position. The weighted average remaining term of its investments stands at 4.0 years.

Looking ahead, management provided guidance for Q2 2025, projecting EAD per diluted common share of $0.43 and CAD per diluted common share of $0.48, suggesting slight improvement from Q1 results.

The following slide summarizes the key financial highlights from the quarter:

Market Reaction and Valuation

Despite the company’s stable performance, NREF continues to trade at a significant discount to book value. According to the presentation, the stock trades at a 15.0% discount to book value with an implied dividend yield of 13.7%, potentially offering value for income-focused investors.

The company’s total return performance compared to peers is illustrated in the following chart:

This performance comparison shows NREF’s relative positioning against competitors including Arbor Realty Trust (NYSE:ABR), Blackstone Mortgage Trust (NYSE:BXMT), and Starwood Property Trust (NYSE:STWD), among others.

The high insider ownership of 12.8% suggests management’s confidence in the company’s strategy and valuation. However, the stock’s recent performance indicates that market participants remain cautious about the commercial real estate sector despite NREF’s focus on more defensive property types.

NexPoint’s Q1 2025 results demonstrate the company’s ability to navigate a challenging real estate environment while maintaining its dividend and growing book value. The significant discount to book value may present an opportunity for investors who share management’s confidence in the company’s diversified portfolio strategy and focus on defensive real estate sectors.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.