Moody’s upgrades Agnico Eagle’s rating to A3 on debt reduction

Introduction & Market Context

NFI Group Inc. (TSX:NFI) presented its second quarter 2025 financial results on August 1, 2025, revealing operational improvements amid significant one-time charges. The global bus and coach manufacturer reported a net loss of $160.8 million, heavily impacted by refinancing costs and restructuring charges, but showed encouraging signs in its adjusted figures and operational metrics.

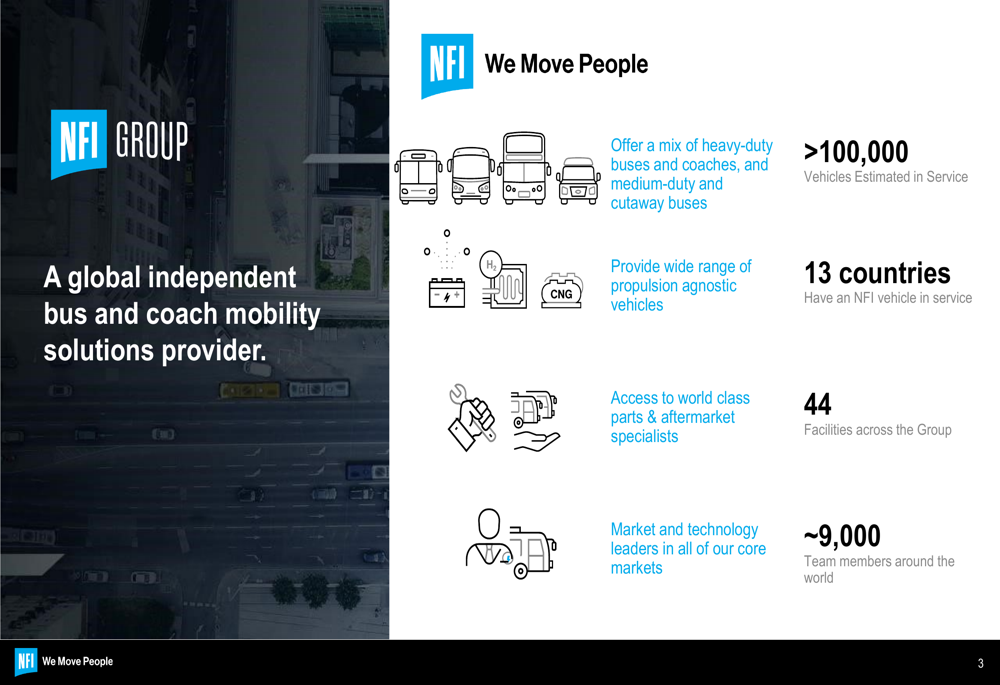

The company operates in a competitive transportation manufacturing sector, with operations spanning 13 countries and approximately 9,000 team members worldwide. NFI’s diverse product portfolio includes a range of propulsion options, positioning it well in the ongoing transition to zero-emission vehicles.

As shown in the following company overview, NFI has established a significant global presence with over 100,000 vehicles estimated in service:

Quarterly Performance Highlights

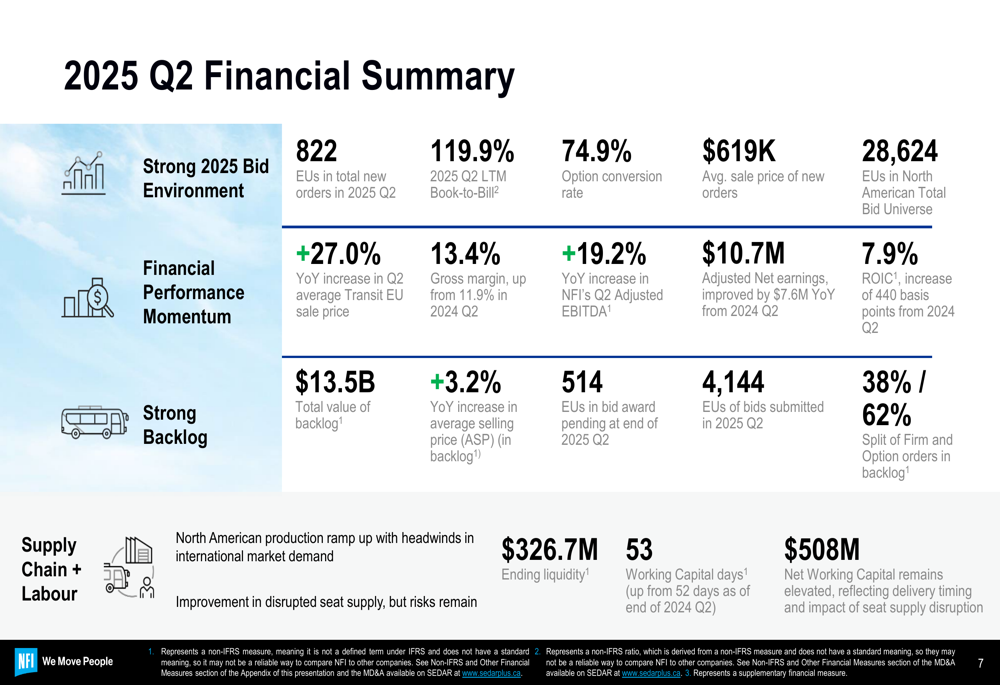

NFI’s Q2 2025 financial performance showed notable year-over-year improvements in several key metrics. The company achieved a 27% increase in average transit equivalent unit (EU) sale price and a 19.2% year-over-year improvement in Adjusted EBITDA. Gross margin expanded to 13.4%, up from 11.9% in Q2 2024, reflecting improved operational efficiency.

The company’s comprehensive financial summary highlights these improvements alongside other key performance indicators:

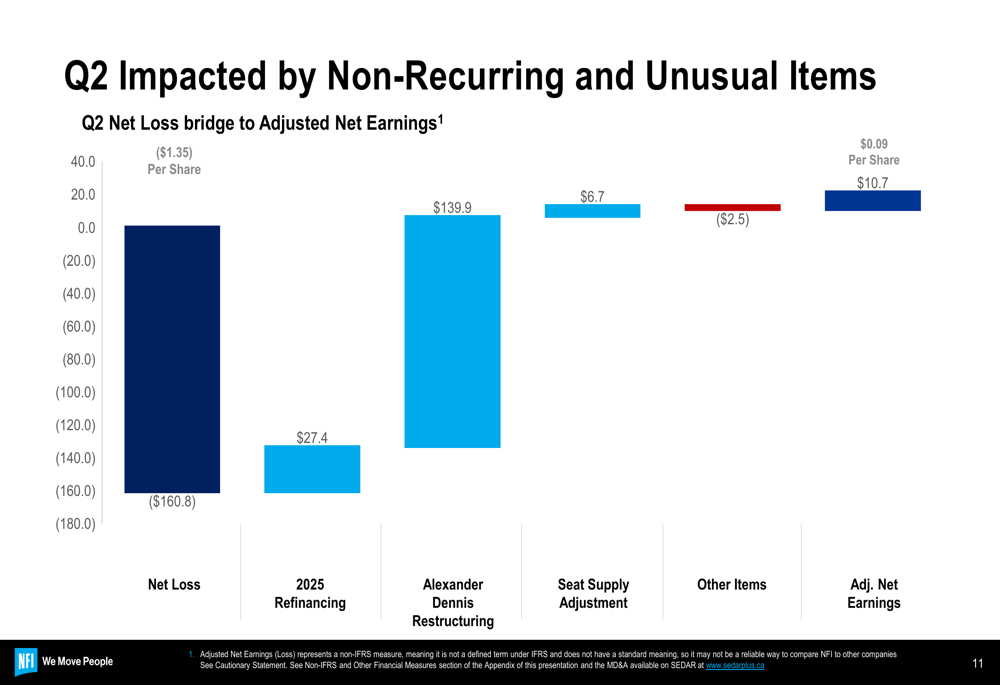

Despite these operational gains, NFI reported a net loss of $160.8 million for the quarter. However, this figure was heavily impacted by non-recurring items, including $27.4 million in refinancing costs and $139.9 million related to Alexander Dennis restructuring. After adjusting for these and other unusual items, NFI achieved adjusted net earnings of $10.7 million ($0.09 per share), representing a $7.6 million improvement year-over-year.

The following bridge chart illustrates the impact of these adjustments:

Detailed Financial Analysis

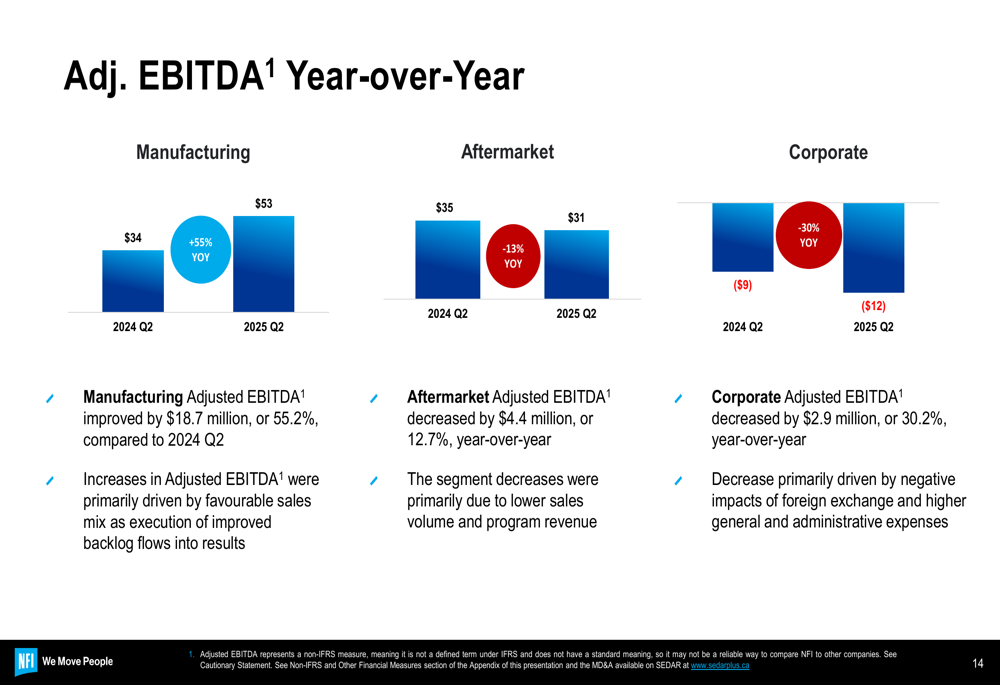

NFI’s segment performance showed mixed results, with Manufacturing Adjusted EBITDA increasing by 55% year-over-year, while Aftermarket and Corporate segments declined by 13% and 30% respectively. The manufacturing improvements were driven by higher deliveries, improved pricing, and enhanced operational efficiency.

The segment performance comparison is illustrated in the following chart:

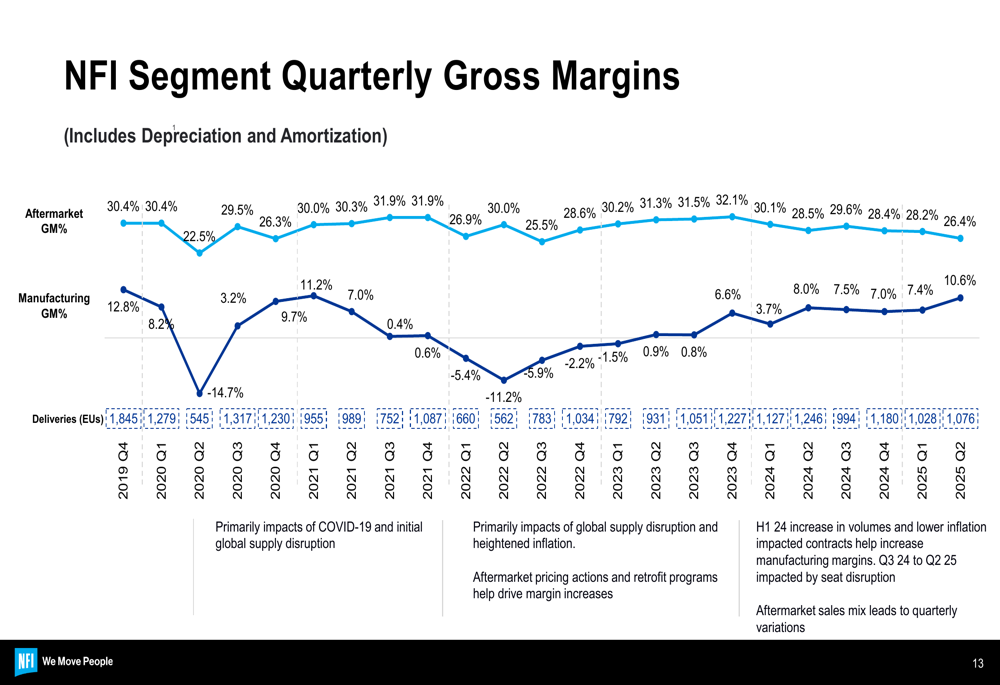

Looking at longer-term trends, NFI’s manufacturing segment has shown substantial improvement over the past two years, with a $135 million increase in LTM Adjusted EBITDA from 2023 to 2024, followed by another $109 million improvement from 2024 to 2025.

The company’s gross margin trends also reflect this recovery, particularly in the manufacturing segment:

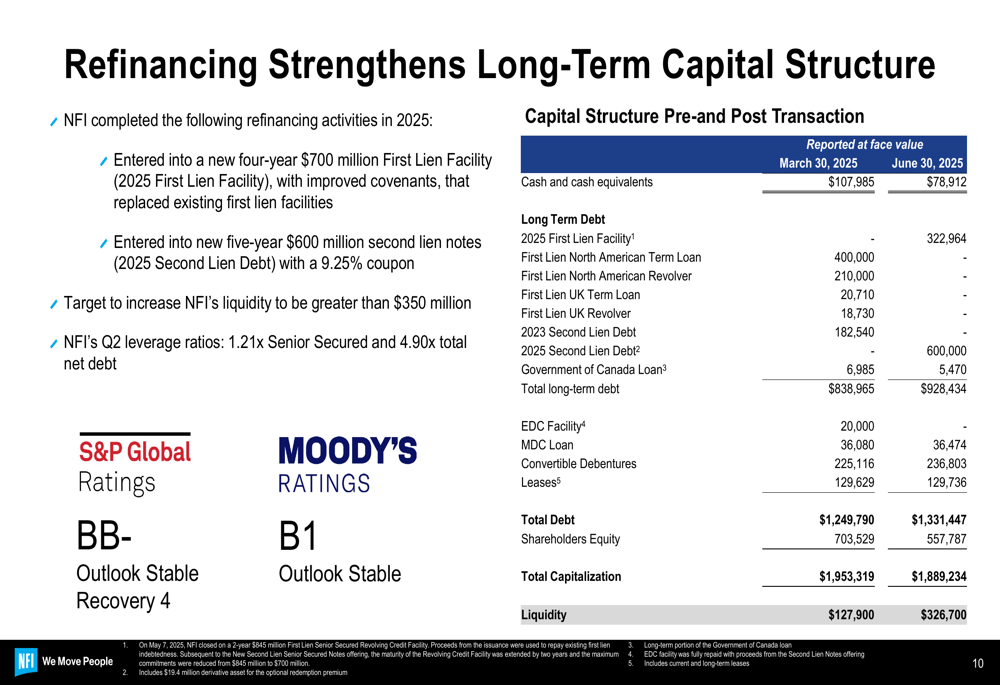

A significant development during the quarter was NFI’s refinancing activities, which strengthened its long-term capital structure. The company entered into a new four-year $700 million First Lien Facility and new five-year $600 million second lien notes with a 9.25% coupon. These actions are expected to increase liquidity to greater than $350 million, with leverage ratios of 1.21x Senior Secured and 4.90x total net debt.

The following slide details the changes to NFI’s capital structure:

Strategic Initiatives

NFI continues to address supply chain challenges, with notable progress in reducing high and moderate risk suppliers. Currently, only one high-risk supplier remains in NFI’s top 800, a significant improvement from previous quarters. This remaining high-risk supplier is providing seats, which has been a particular pain point for the company.

The seat supply disruption has shown improvement, with missing seat buses reduced to 74 at the end of the quarter and further down to 56 units in July. NFI recorded a $9.7 million adjustment for impacts related to this issue, including labor, overhead costs, and liquidated damages. The company has also onboarded a new Buy America compliant seat supplier and targets full recovery in the second half of 2025.

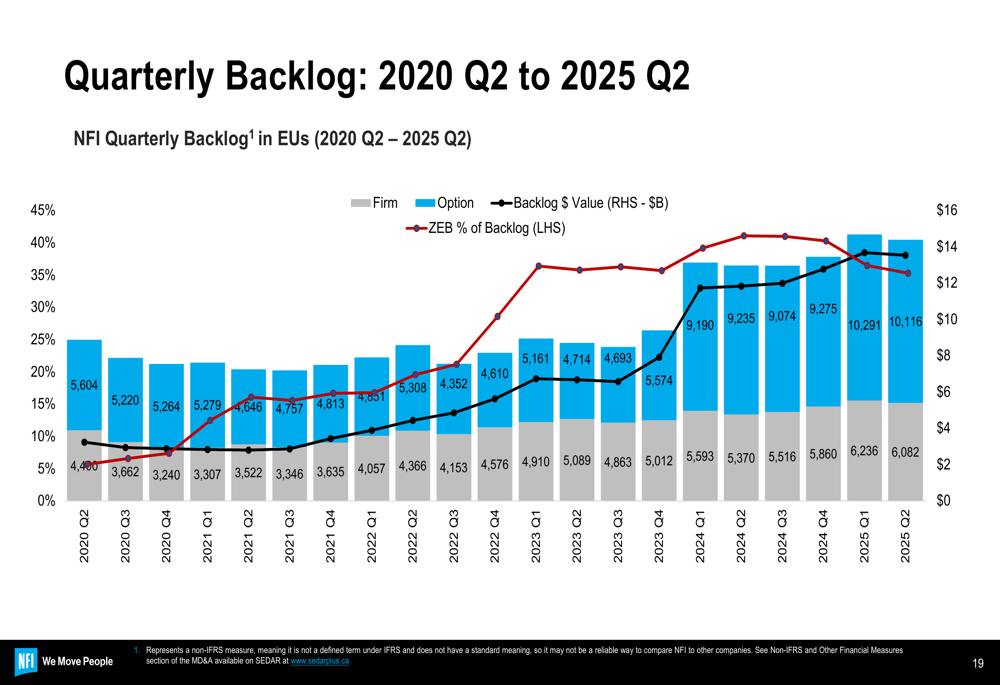

NFI’s backlog remains robust at $13.5 billion, with a book-to-bill ratio of 119.9% for the last twelve months. The backlog includes a healthy mix of firm orders (38%) and options (62%), providing good visibility into future production.

The quarterly backlog trend is illustrated in the following chart:

The company continues to see strong demand for zero-emission buses (ZEBs), which now represent a significant portion of the backlog. Average sale prices have also been trending upward, driven by pricing, sales mix, higher ZEB orders, and improving market dynamics.

Forward-Looking Statements

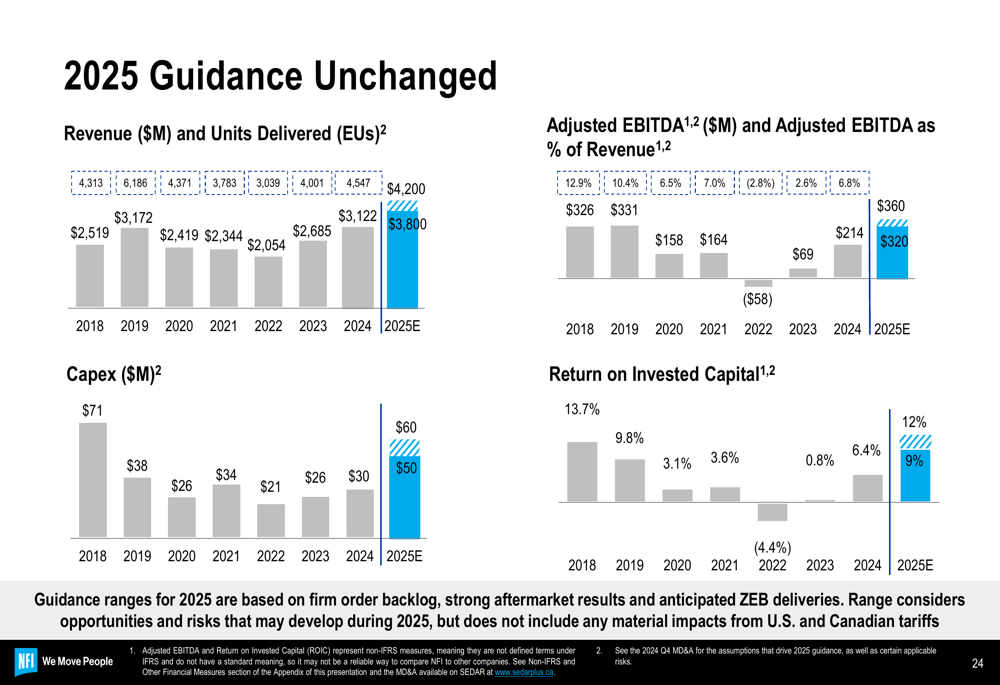

NFI maintained its 2025 guidance, targeting revenue of $4.2 billion and 4,200 equivalent units delivered. The company also expects capital expenditures of $60-70 million, Adjusted EBITDA of $400-450 million, and a Return on Invested Capital of 8-10%.

The unchanged guidance is summarized in the following slide:

The company noted potential challenges from tariffs on imports of steel and aluminum into the U.S., as well as tariffs associated with imports of certain goods from outside North America used in Canadian and U.S. manufacturing and aftermarket operations. Management indicated they are taking necessary actions to limit the impact and exposure to these tariffs.

Despite these challenges, NFI expressed confidence in its outlook, citing strong momentum in the first half of 2025, greater capital visibility following refinancing, and a robust backlog that supports production plans for 2025 and 2026. The company also highlighted its second-highest quarterly ZEB deliveries in company history during Q2 2025, reinforcing its leadership position in the transition to zero-emission transportation.

With improving operational metrics, a strengthened capital structure, and a substantial backlog, NFI appears well-positioned to continue its recovery trajectory despite the one-time charges that impacted this quarter’s bottom line.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.