Can anything shut down the Gold rally?

Introduction & Market Context

NGL Energy Partners LP (NYSE:NGL) released its investor presentation for August 2025, following its first quarter fiscal 2026 earnings announcement on August 7. The midstream energy company, which has been strategically repositioning itself as primarily a water solutions provider for oil and gas producers, reported mixed results with significant revenue shortfalls despite growth in its core water business.

The company’s stock closed at $4.00 following the earnings announcement, down 1.23% in after-hours trading, reflecting investor disappointment with the quarterly performance. With a market capitalization of approximately $528 million, NGL Energy Partners continues to trade within its 52-week range of $2.64 to $5.73.

Executive Summary

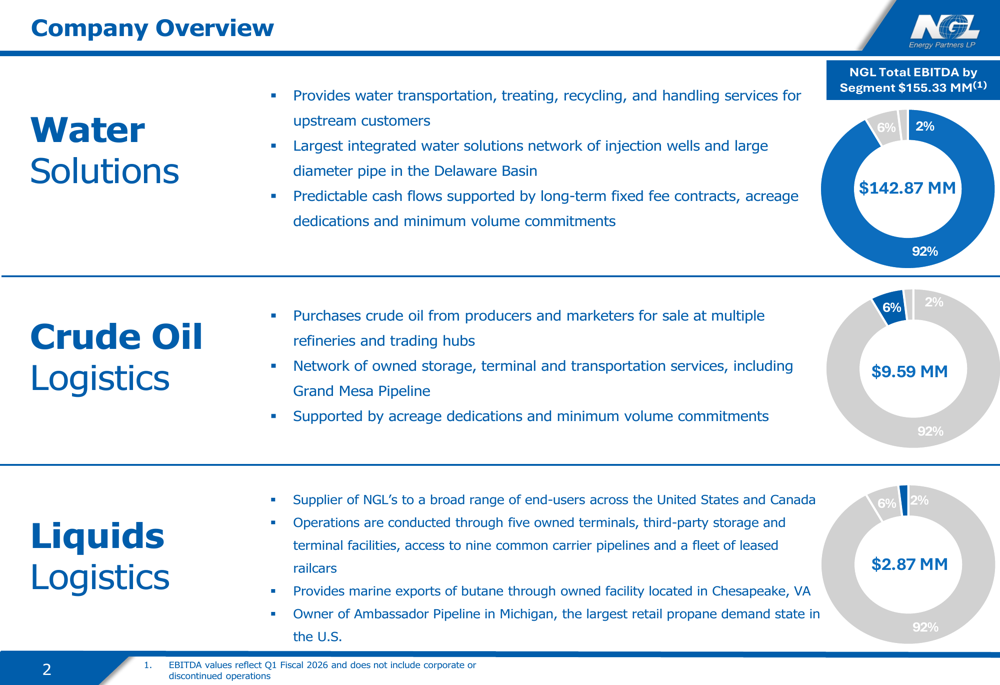

NGL Energy Partners’ presentation highlights the company’s transformation into a water solutions specialist, with this segment now accounting for 92% of total EBITDA. While the Water Solutions business showed impressive growth metrics, the company’s overall performance fell short of market expectations, with Q1 revenue of $622.16 million missing forecasts by 25.58%.

The presentation emphasizes NGL’s strategic initiatives, including debt reduction, non-core asset sales totaling approximately $270 million, and a common unit repurchase program of up to $50 million. These moves align with management’s stated focus on improving the company’s balance sheet and returning value to shareholders.

As shown in the following breakdown of the company’s business segments and their contribution to total EBITDA:

Water Solutions Segment Performance

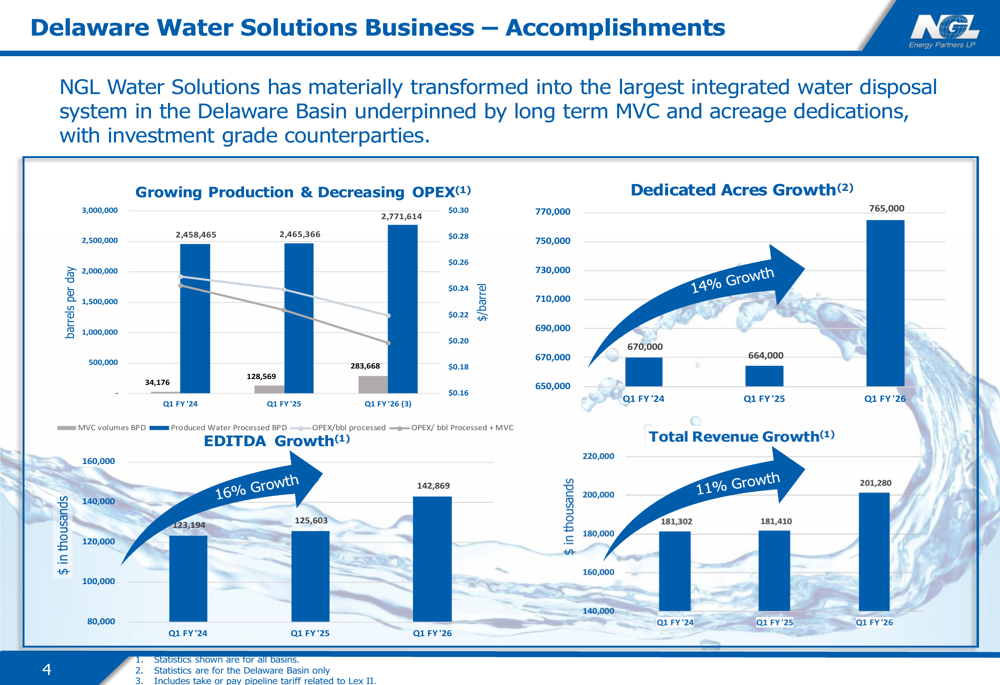

The Water Solutions segment continues to be the primary driver of NGL Energy Partners’ business, showing strong operational and financial growth. According to the presentation, produced water processed increased from 2.46 million barrels per day in Q1 FY2024 to 2.77 million barrels per day in Q1 FY2026, while operating expenses per barrel decreased from $0.26 to $0.16 over the same period.

The company has expanded its dedicated acreage in the Delaware Basin by 14%, from 670,000 acres to 765,000 acres, reinforcing its market position. This expansion has contributed to an 11% growth in total revenue for the segment, from $181.3 million to $201.3 million year-over-year.

The following chart illustrates these key performance metrics for the Water Solutions business:

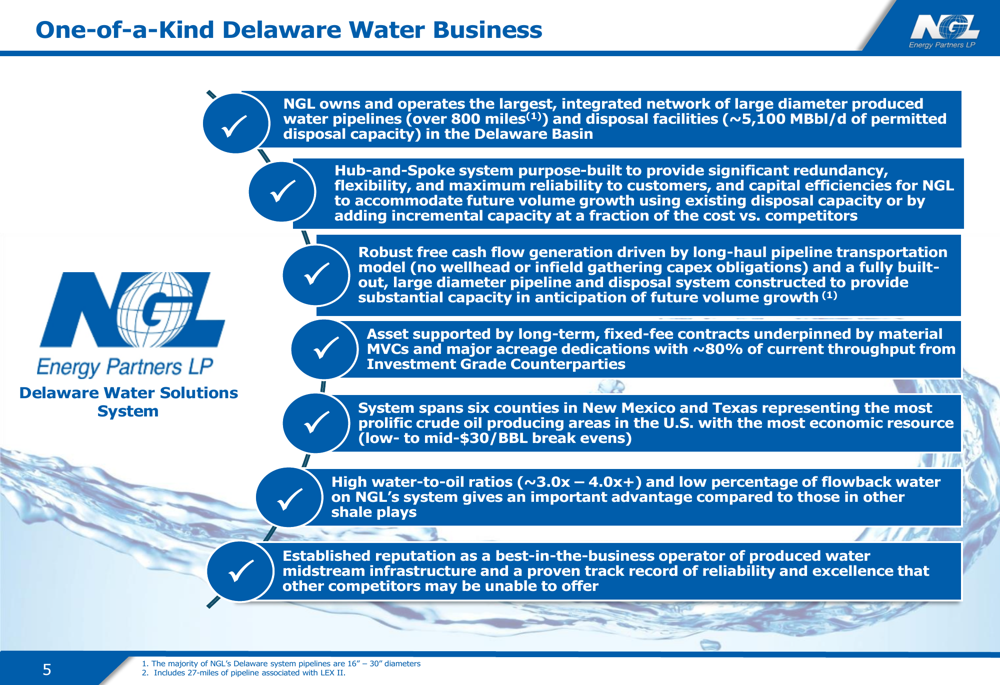

NGL Energy Partners has positioned itself as the largest integrated network provider in the Delaware Basin, with over 800 miles of large diameter produced water pipelines and approximately 5,100 MBbl/d of permitted disposal capacity. The company’s hub-and-spoke system provides significant redundancy and flexibility, creating barriers to entry for competitors.

The key attributes of NGL’s Delaware Water Business are highlighted in this slide:

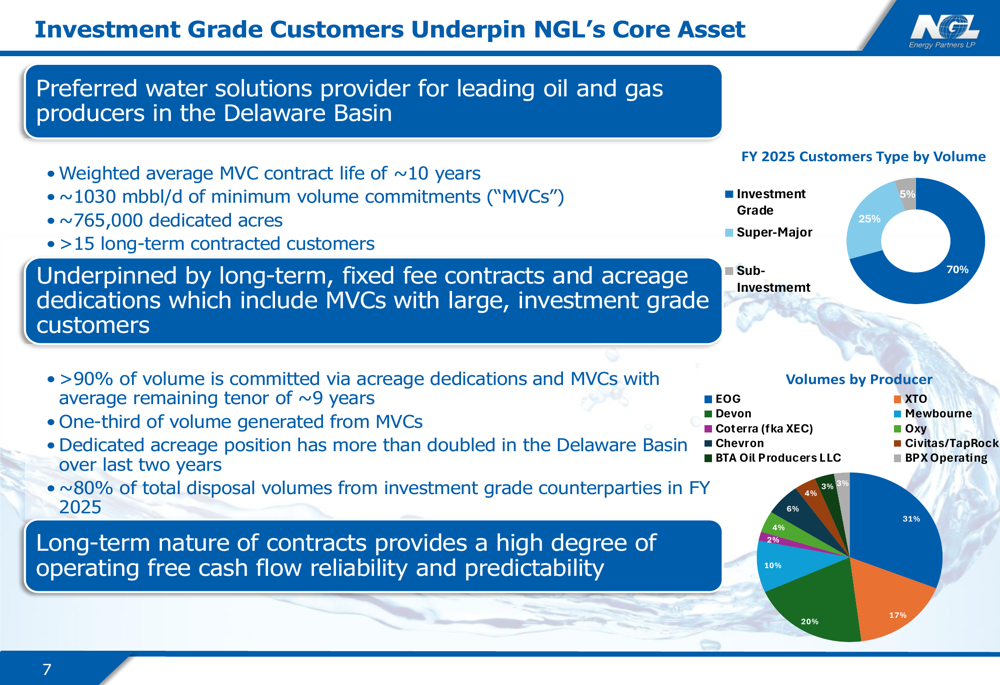

A critical component of NGL’s water business success is its customer base, which consists predominantly of investment-grade counterparties. According to the presentation, approximately 80% of current throughput comes from investment-grade customers, with contracts featuring a weighted average minimum volume commitment (MVC) life of approximately 10 years.

The following breakdown shows NGL’s customer composition, with investment-grade customers accounting for 70% of volume, super-majors for 25%, and sub-investment grade for just 5%:

Strategic Initiatives and Asset Sales

The presentation outlines several strategic moves executed by NGL Energy Partners over the past year, including:

1. Final arrearage payment to preferred unitholders in April 2024

2. Amendment of the Term Loan B agreement in August 2024, reducing the SOFR margin from 4.5% to 3.75%

3. Completion of the LEX II water pipeline project in October 2024, with an initial capacity of 200,000 barrels per day

4. Authorization of a $50 million common unit repurchase program in June 2024

5. Announcement of non-core asset sales totaling approximately $270 million in May 2025

6. Repurchase of 70,000 Class D preferred units (12% of outstanding) in Q1 FY2026

These initiatives align with CEO Mike Crimble’s statement from the earnings call that "Cash is being used to purchase and repay debt and equity that provides the highest return and greatest benefit to the partnership," highlighting the company’s focus on capital allocation and balance sheet improvement.

Financial Performance and Outlook

Despite the strong performance in the Water Solutions segment, NGL Energy Partners’ overall financial results for Q1 FY2026 fell short of expectations. The company reported earnings per share of $0.04, missing the forecast of -$0.04, and revenue of $622.16 million, significantly below the expected $835.98 million.

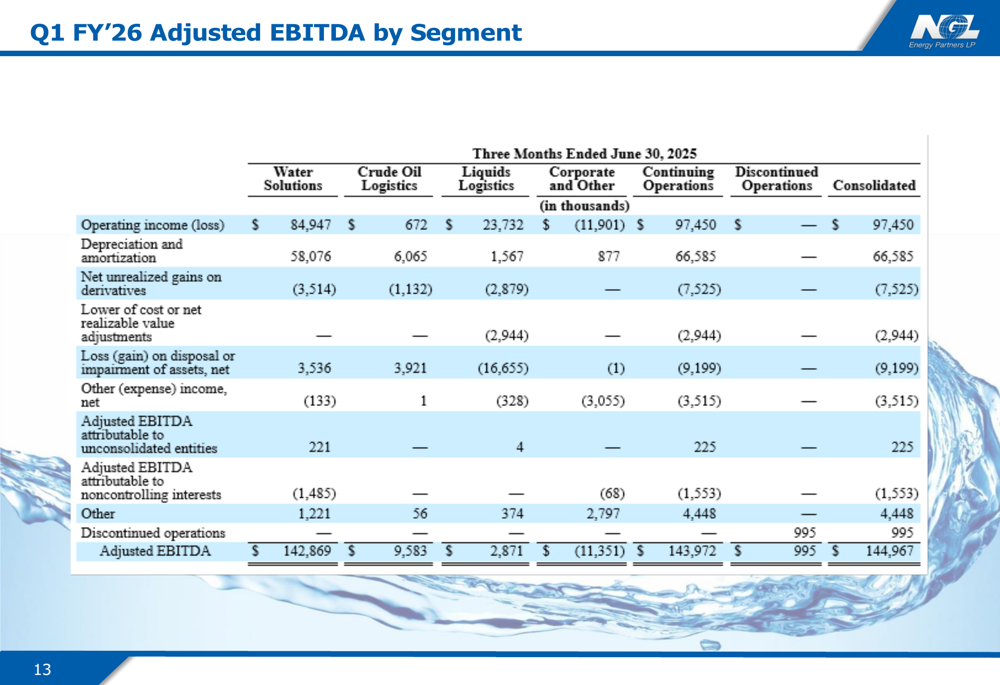

The presentation reveals that total Adjusted EBITDA for Q1 FY2026 was $144.97 million, showing modest growth from $144.34 million in Q1 FY2025 and $134.66 million in Q1 FY2024. However, this growth was driven almost entirely by the Water Solutions segment, which contributed $142.87 million (92%) of total EBITDA in Q1 FY2026.

The detailed breakdown of Q1 FY2026 Adjusted EBITDA by segment shows the following key components:

The Crude Oil Logistics and Liquids Logistics segments, which together account for just 8% of EBITDA, have seen declining performance. According to the earnings report, Crude Oil Logistics EBITDA fell to $9.6 million from $18.6 million in the prior year.

Despite the revenue miss, NGL Energy Partners maintains its full-year adjusted EBITDA guidance of $615-$625 million, suggesting confidence in continued strong performance from the Water Solutions segment and potential improvement in other business areas in the coming quarters.

The company faces ongoing challenges, including revenue shortfalls, declines in non-core segments, and competitive pressures in the water solutions market. However, its strong position in the Delaware Basin, long-term contracts with investment-grade customers, and strategic focus on debt reduction provide a foundation for potential future growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.