ReElement Technologies stock soars after securing $1.4B government deal

Introduction & Market Context

Nickel Mines Ltd (ASX:NIC) released its quarterly activities presentation for Q2 2025, revealing a mixed performance across its operations while maintaining an overall solid adjusted EBITDA of US$86 million. The company, which has seen its stock rise approximately 40% over the past year, demonstrated resilience in its mining division while facing headwinds in its RKEF (Rotary Kiln Electric Furnace) and trading segments. Currently trading at A$0.755, Nickel Mines continues to navigate the volatile nickel market with its diversified operational portfolio.

The presentation, covering the quarter ended June 30, 2025, comes at a time when the company is balancing operational performance with significant project developments and sustainability initiatives. Despite challenges in some divisions, the company’s stock has maintained positive momentum, reflecting investor confidence in its long-term strategy.

Quarterly Performance Highlights

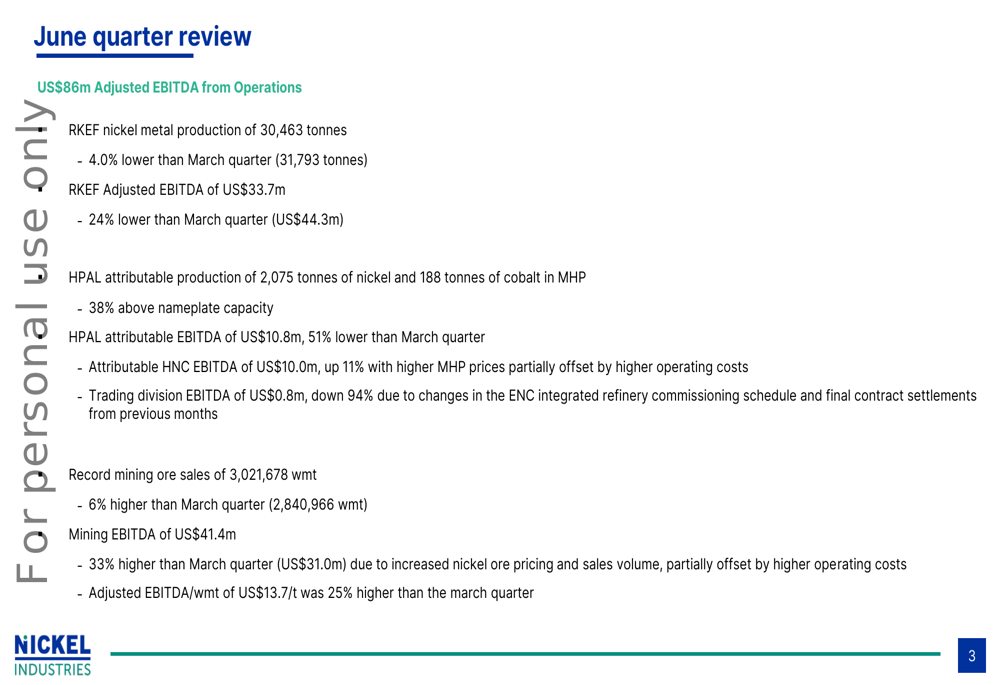

Nickel Mines reported an adjusted EBITDA of US$86 million for Q2 2025, contributing to a first-half total of US$183.6 million. The quarter saw varied performance across the company’s operational divisions, with mining operations emerging as a particular bright spot.

As shown in the key financial summary from the company’s presentation:

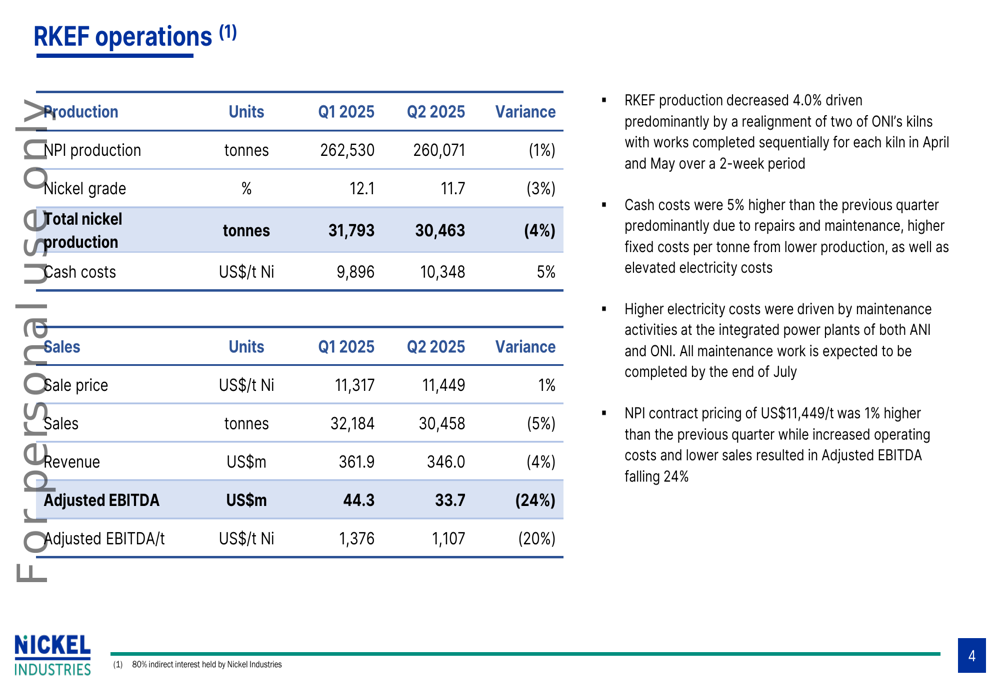

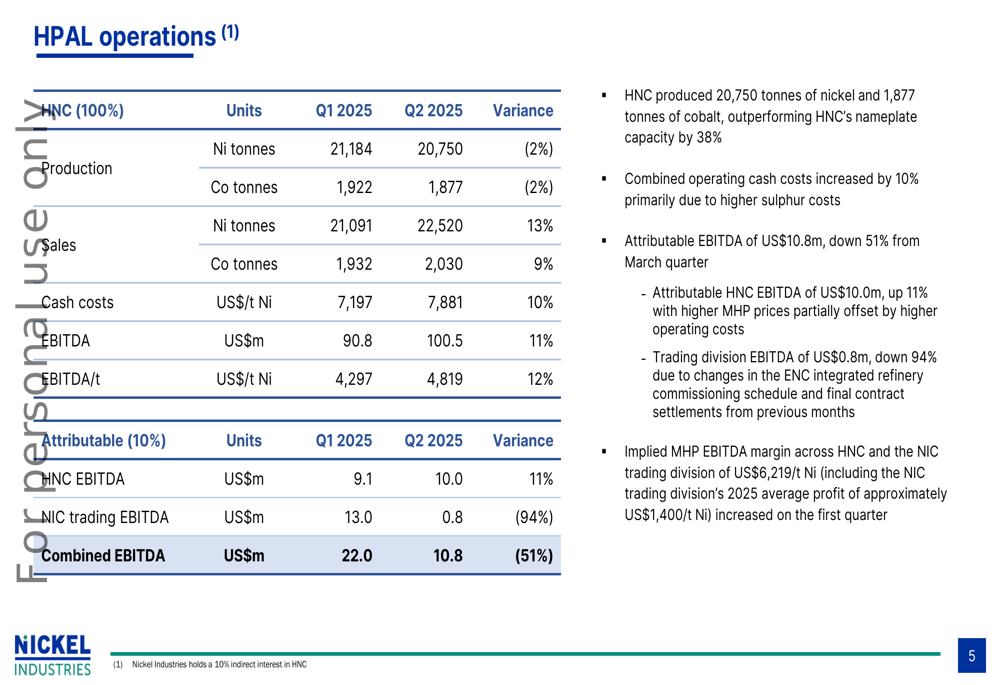

RKEF operations produced 30,463 tonnes of nickel metal, a 4.0% decrease from the previous quarter’s 31,793 tonnes, resulting in an adjusted EBITDA of US$33.7 million, down 24% from Q1’s US$44.3 million. Meanwhile, HPAL attributable production reached 2,075 tonnes of nickel and 188 tonnes of cobalt in MHP, operating at 38% above nameplate capacity, though attributable EBITDA fell 51% to US$10.8 million.

The trading division experienced a significant decline, with EBITDA falling 94% to US$0.8 million, primarily due to changes in the ENC integrated refinery commissioning schedule and final contract settlements from previous months.

Operational Analysis by Division

RKEF Operations

The RKEF operations saw a 4% decrease in production compared to the previous quarter, primarily due to kiln realignment. Cash costs increased by 5% to US$10,348 per tonne of nickel, driven by maintenance activities and higher electricity costs. Despite a slight 1% increase in NPI contract pricing to US$11,449 per tonne, the division’s adjusted EBITDA fell 24% to US$33.7 million.

The detailed breakdown of RKEF performance metrics shows:

HPAL Operations

The HPAL operations demonstrated strong production capabilities, operating at 38% above nameplate capacity. However, attributable EBITDA decreased significantly from the March quarter, falling 51% to US$10.8 million. This decline was partially offset by the HNC component, which saw an 11% increase in EBITDA to US$10.0 million, benefiting from higher MHP prices despite increased operating costs.

The comprehensive HPAL performance data reveals:

Mining Operations

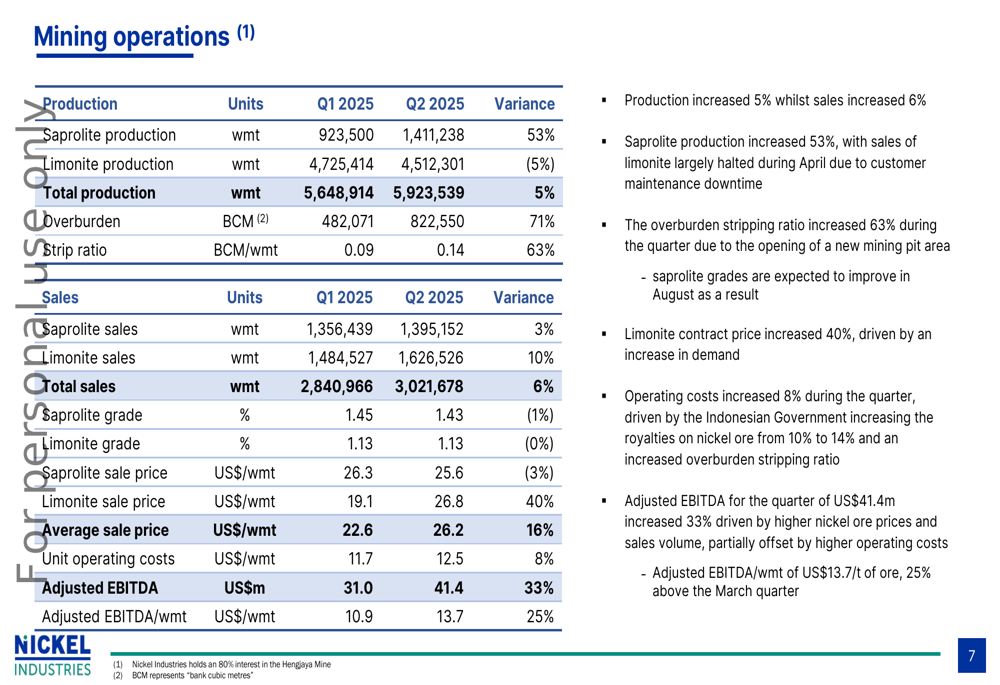

Mining emerged as the standout performer for the quarter, with record ore sales of 3,021,678 wet metric tonnes (wmt), representing a 6% increase from Q1. This strong sales performance, combined with favorable pricing, particularly for limonite ore (up 40% to US$26.8/wmt), drove mining EBITDA to US$41.4 million, a 33% increase from the previous quarter.

The detailed mining operations metrics highlight this strong performance:

During the earnings call, management emphasized the robust margins from mining operations, with EBITDA per tonne increasing 25% to US$13.7/wmt. This strong mining performance helped offset weaknesses in other divisions and underscores the value of the company’s diversified operational model.

Project Updates and Future Outlook

Nickel Mines provided significant updates on its project developments, particularly regarding the ENC integrated nickel refinery. The company has decided to defer commissioning of the refinery to better align working capital requirements with the anticipated issuance of the commercial sales license (IUI), now expected in early Q1 2026.

The ENC project update shows substantial progress with key equipment installation:

The Sampala Project is also advancing, with a detailed mine plan completed for the PT Erabaru Timur Lestari (ETL) IUP, targeting a production license of 6 million wmt per annum. Construction of infrastructure, including an 8km haul road, a 60-metre bridge, and internal road systems, is progressing well, creating approximately 450 new jobs. During the quarter, drilling activities were substantial, with 16 drill rigs completing 1,031 drill holes for 31,497 metres.

According to the earnings call, the company expects the first ore from the Sampala project early in H2 2025, contingent upon receiving the RKAB permit, anticipated in August. The company has allocated approximately US$30 million for remaining capital expenditures related to the Sampala project.

Safety and Sustainability Initiatives

Nickel Mines maintained a strong safety record, reporting a company-wide 12-month lost time injury frequency rate (LTIFR) of 0.05 as of the end of June 2025. No lost time injuries were recorded during the quarter, against 4.6 million work hours registered. The company’s 12-month rolling total recordable injury frequency rate (TRIFR) stood at 1.29.

The company also highlighted its sustainability initiatives, including:

The 2024 Sustainability Report marks significant progress in the company’s ESG commitments, including alignment with IFRS Sustainability Disclosure Standards and the Australian Accounting Standards Board Guidance. The formal establishment of the Nickel Industries Foundation underscores the company’s commitment to community development, with strategic programs focusing on education, health, environmental conservation, and economic empowerment.

Financial Outlook and Challenges

While Nickel Mines demonstrated resilience in Q2 2025, the company faces several challenges ahead. As noted in the earnings call, the company has significant debt servicing requirements, with US$33 million paid in July and US$100 million due by year-end. Management indicated they are "actively managing working capital and remain in active discussions of various other sources of financing."

The deferral of the ENC integrated refinery commissioning also represents a timeline adjustment that investors will need to monitor. However, the strong performance of the mining division and the progress on the Sampala project provide positive counterpoints to these challenges.

With revenue growth of 10.19% in the last twelve months and analysts expecting continued profitability, Nickel Mines appears positioned to navigate these challenges while capitalizing on its operational strengths, particularly in its mining division.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.