TSX drops after Canadian index edges higher in prior session

Introduction & Executive Summary

Nidec Corporation (TSE:6594) reported mixed financial results for the first quarter of fiscal year 2025, with a slight decline in net sales but an improvement in operating profit margin. The Japanese motor manufacturer’s preliminary report, presented on July 24, 2025, highlighted its strategic pivot toward profitability over growth through a new mid-term management plan called "Conversion 2027."

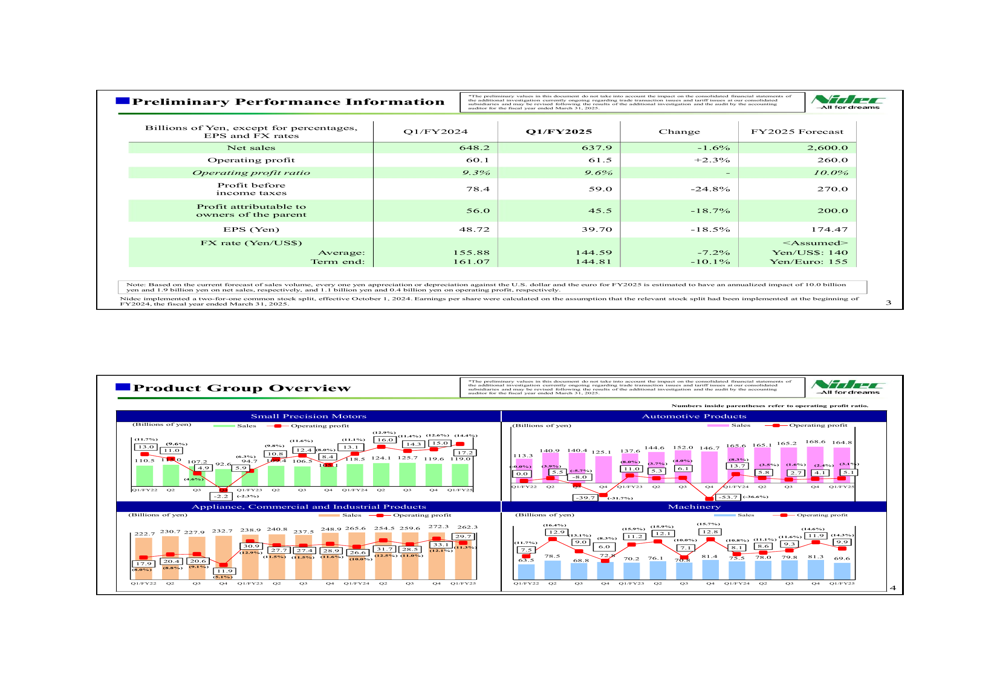

The company reported Q1 FY2025 net sales of 637.9 billion yen, down 1.6% year-over-year, while operating profit increased by 2.3% to 61.5 billion yen. However, profit attributable to owners declined 18.7% to 45.5 billion yen, largely due to currency headwinds from the strengthening yen, which appreciated 7.2% against the US dollar compared to the same period last year.

Quarterly Performance Highlights

Nidec’s preliminary financial results showed a mixed performance across its business segments. While net sales declined slightly, the company managed to improve its operating profit ratio to 9.6% from 9.3% in the same quarter last year.

As shown in the following chart of quarterly performance metrics:

The company’s profit before income taxes fell 24.8% to 59.0 billion yen, while earnings per share decreased 18.5% to 39.70 yen. This decline was primarily attributed to the stronger yen and the absence of a one-time gain from the step acquisition of Nidec PSA emotors recorded in the previous year.

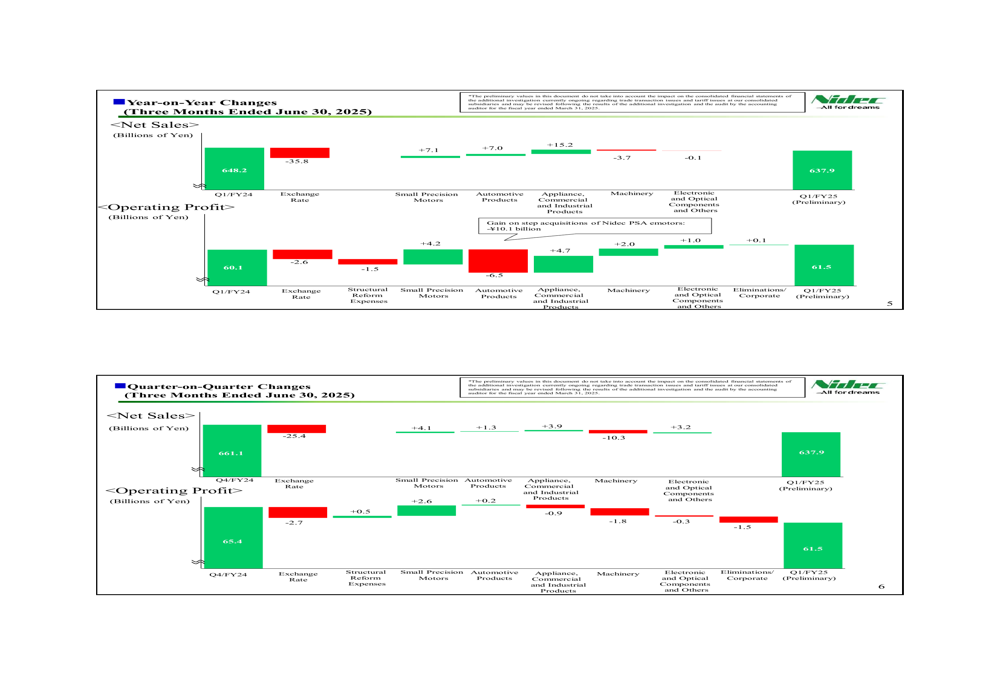

The year-on-year changes in net sales and operating profit reveal how different business segments contributed to the overall performance:

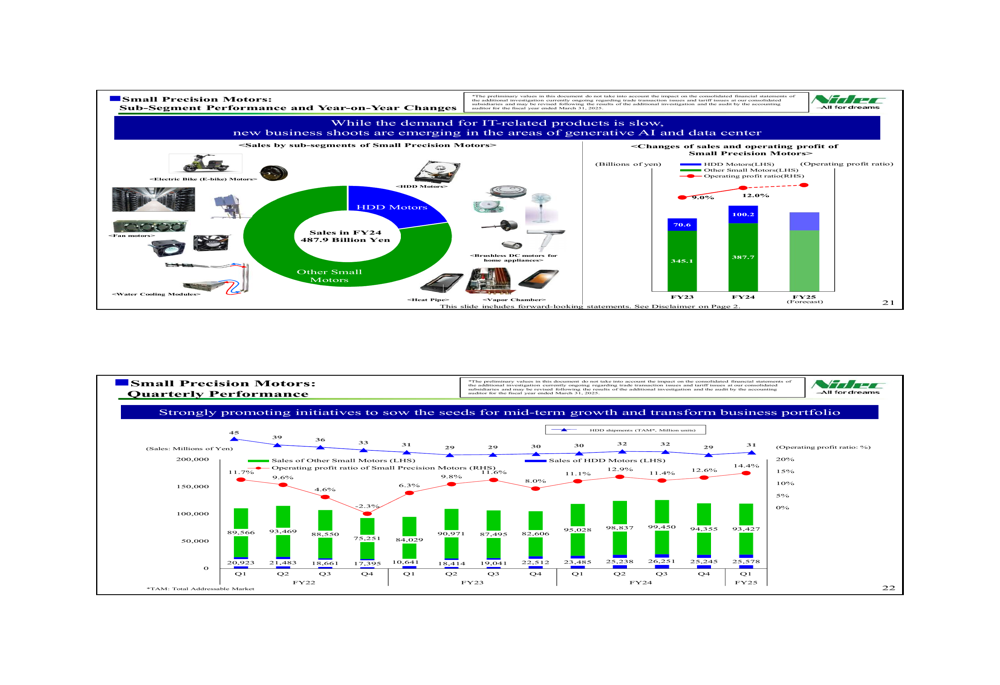

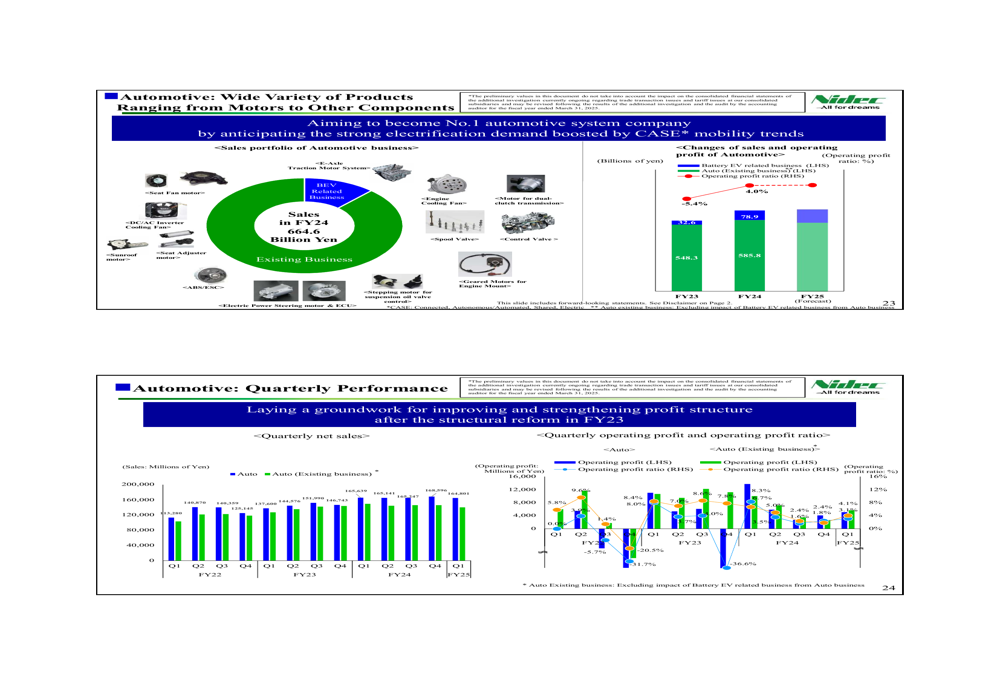

Notably, Small Precision Motors saw a significant sales decrease of 15.2 billion yen, while Automotive Products and Appliance, Commercial and Industrial Products segments showed increases of 7.1 billion yen and 7.0 billion yen, respectively.

Free cash flow turned negative in Q1 FY2025 at -21.8 billion yen, compared to a positive 9.8 billion yen in the same period last year:

Strategic Initiatives

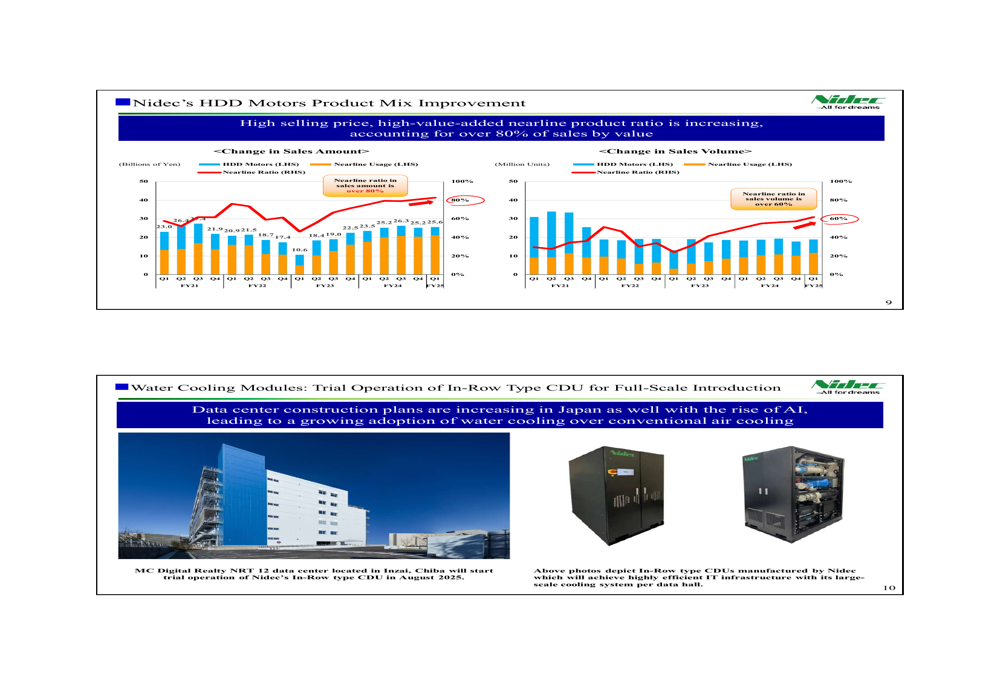

Nidec is pursuing several strategic initiatives to enhance its competitive position in high-growth markets. One notable development is the improvement in the company’s HDD motors product mix, with a focus on high-value-added nearline products:

The company has successfully increased the ratio of nearline products to over 80% in sales amount and over 60% in sales volume, enhancing profitability in this segment despite overall market challenges in the HDD sector.

In the data center cooling space, Nidec is preparing for a trial operation of its In-Row Type CDU (Cooling Distribution Unit) at MC Digital Realty’s NRT 12 data center in Inzai, Chiba, beginning in August 2025:

This initiative aligns with the growing demand for efficient cooling solutions in data centers, particularly as AI applications drive increased computing power requirements.

Nidec also announced the acquisition of Xecom, a Chinese scroll compressor manufacturer, to expand its presence in air conditioning and heat pump markets:

The acquisition, now renamed Nidec Scroll Technology (Changzhou) Co., Ltd., brings expertise in high-performance scroll compressors for air conditioning, heat pumps, and refrigeration applications. The company generated approximately 2.5 billion yen in net sales for the fiscal year ended December 31, 2024.

Mid-Term Management Plan

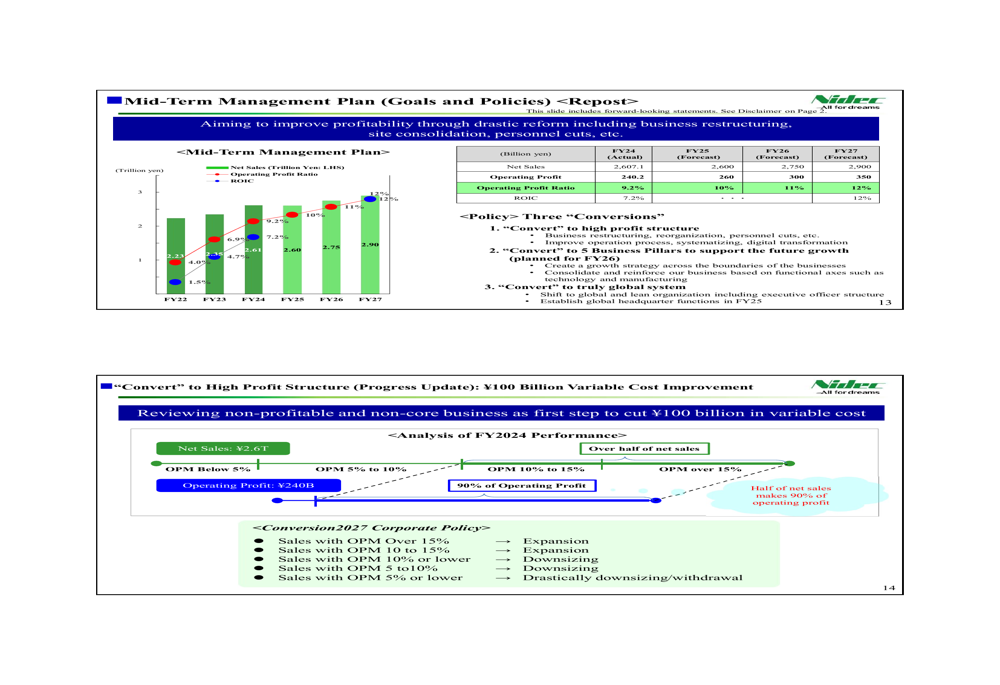

The centerpiece of Nidec’s presentation was the introduction of its new mid-term management plan, "Conversion 2027," which outlines ambitious targets for profitability improvement:

The plan focuses on three key "conversions": shifting to a high-profit structure, reorganizing into five business pillars to support future growth, and evolving into a truly global system. By fiscal year 2027, Nidec aims to achieve 2,900 billion yen in net sales with an operating profit of 350 billion yen, representing an operating profit ratio of 12%, up from 9.2% in FY2024.

A critical component of this strategy is the company’s plan to review non-profitable and non-core businesses, targeting a 100 billion yen reduction in variable costs:

The company has established clear criteria for its business portfolio, planning to expand segments with operating profit margins over 10%, while downsizing or withdrawing from businesses with margins below 5%.

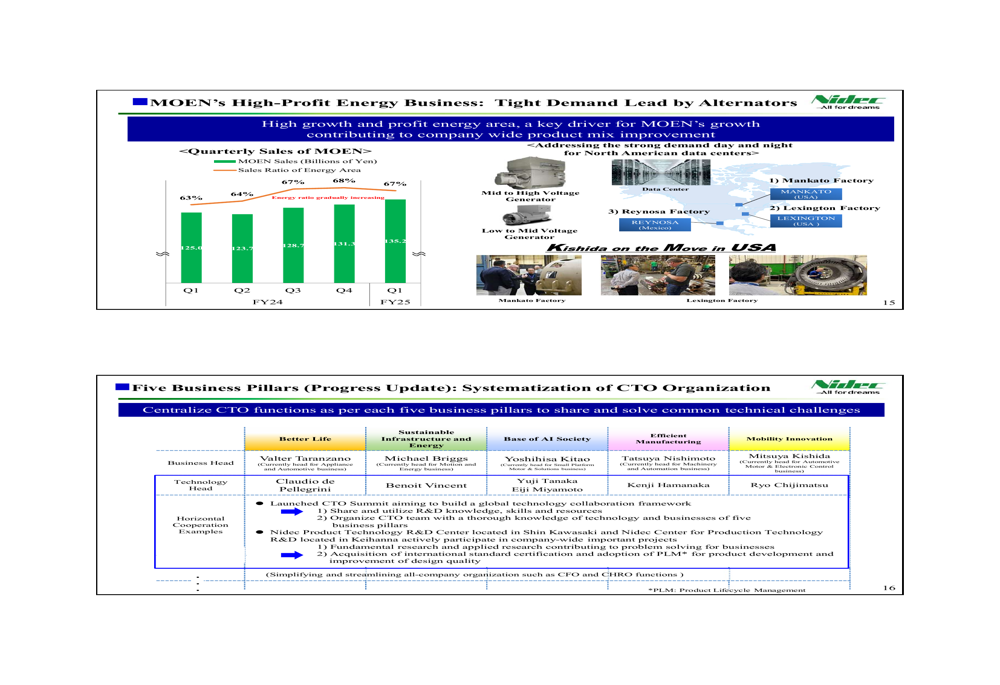

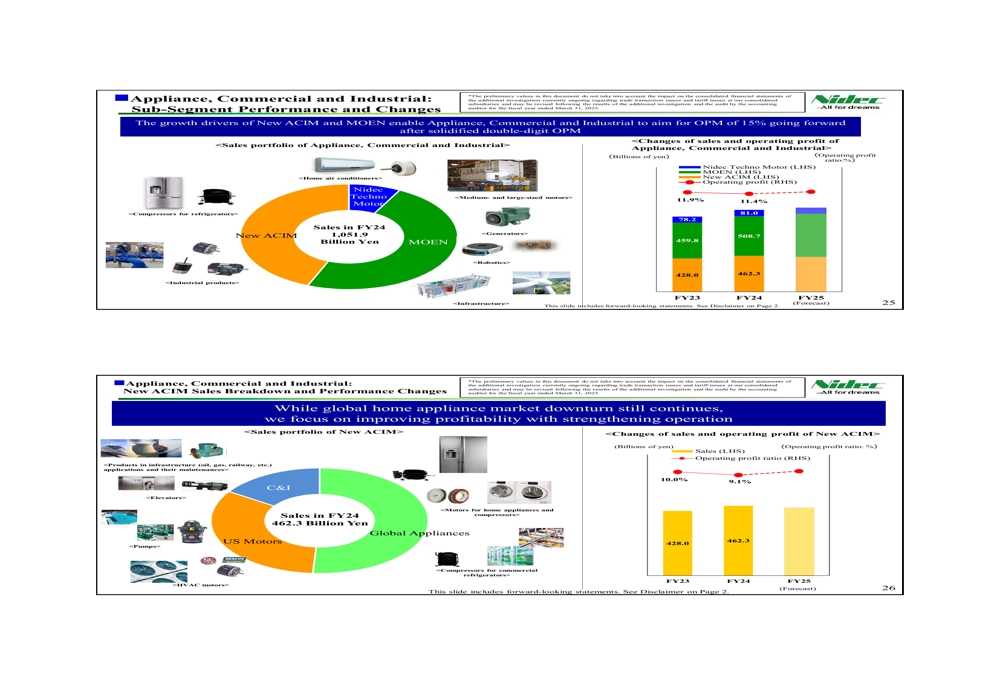

MOEN’s high-profit energy business represents one of the growth drivers for Nidec’s future:

This segment is experiencing strong demand from North American data centers and is contributing to the company’s overall product mix improvement.

Forward-Looking Statements

Nidec’s presentation emphasized its commitment to improving profitability through drastic reforms, including business restructuring, site consolidation, and personnel cuts. The company maintained its full-year FY2025 forecast of 2,600 billion yen in net sales, 260 billion yen in operating profit, and 200 billion yen in profit attributable to owners.

It’s worth noting that the preliminary values presented do not account for the impact of ongoing investigations regarding trade transaction issues and tariff issues at consolidated subsidiaries. These figures may be revised following the completion of these investigations and the audit for the fiscal year ended March 31, 2025.

Nidec’s strategic shift toward prioritizing profitability over pure revenue growth marks a significant evolution in the company’s approach as it navigates challenging global economic conditions and currency headwinds. The success of the "Conversion 2027" plan will depend on the company’s ability to execute its cost-cutting initiatives while maintaining momentum in high-growth segments like data center cooling solutions and energy systems.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.