Goldman Sachs expects Nvidia ’beat and raise,’ lifts price target to $240

Introduction & Market Context

Nimbus Group AB (BOAT) presented its third-quarter 2025 results on October 23, revealing significant challenges in a marine market that has reached its lowest point in a decade. The company’s stock fell 11.66% in pre-market trading following the announcement, reflecting investor concerns about the steep decline in sales and continued negative EBITA.

The presentation, delivered by CEO Johan Inden and CFO Rasmus Alvemyr, highlighted particularly soft market conditions in North America, which has been a key driver of the company’s underperformance. Despite these headwinds, management emphasized several strategic initiatives aimed at navigating the downturn.

Quarterly Performance Highlights

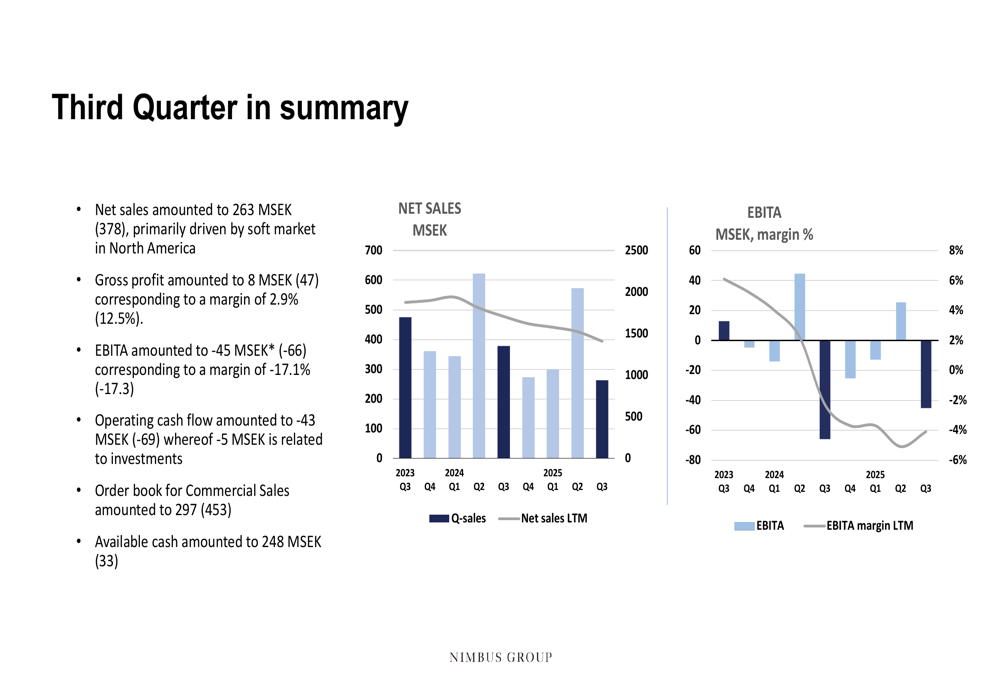

Nimbus Group reported net sales of 263 MSEK for Q3 2025, a substantial decline from 378 MSEK in the same period last year. Gross profit plummeted to 8 MSEK (down from 47 MSEK), resulting in a gross margin of just 2.9% compared to 12.5% in Q3 2024.

The company posted an EBITA of -45 MSEK, which represents a slight improvement from -66 MSEK in the previous year. Similarly, the EBITA margin showed a minimal improvement to -17.1% from -17.3%.

As shown in the following chart of quarterly performance, both sales and EBITA have been on a declining trend:

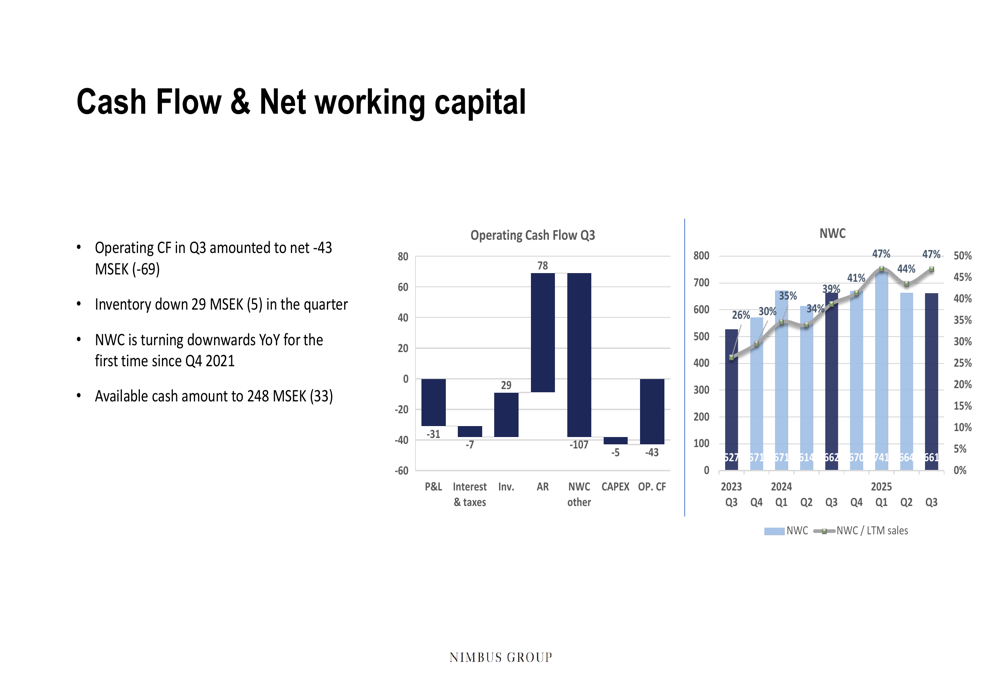

Operating cash flow improved to -43 MSEK from -69 MSEK in the same quarter last year, with 5 MSEK related to investments. The company’s available cash position strengthened significantly to 248 MSEK, up from 33 MSEK a year ago, providing some financial flexibility during this challenging period.

Regional Performance Analysis

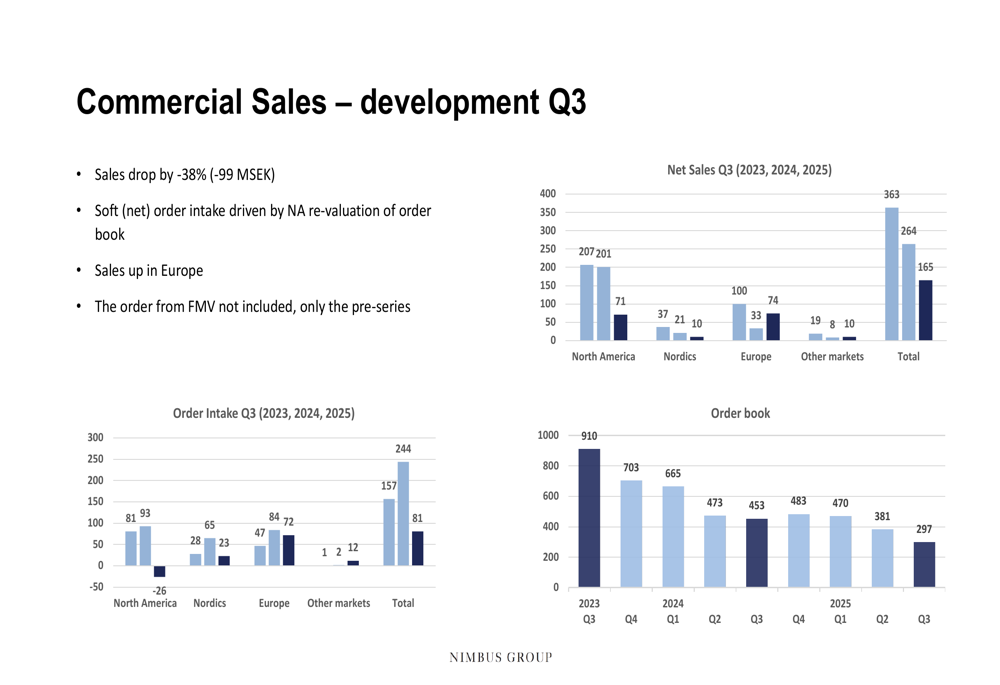

The presentation revealed that commercial sales dropped by 38% (-99 MSEK) in the third quarter, with North America showing particular weakness. The company also disclosed a downward adjustment of its North American order book, reflecting the deteriorating market conditions in the region.

The following chart illustrates the regional breakdown of commercial sales performance:

While North America struggled, European sales showed some resilience. The company’s order book for commercial sales stood at 297 MSEK, down from 453 MSEK in the previous year, continuing a downward trend that began in 2023.

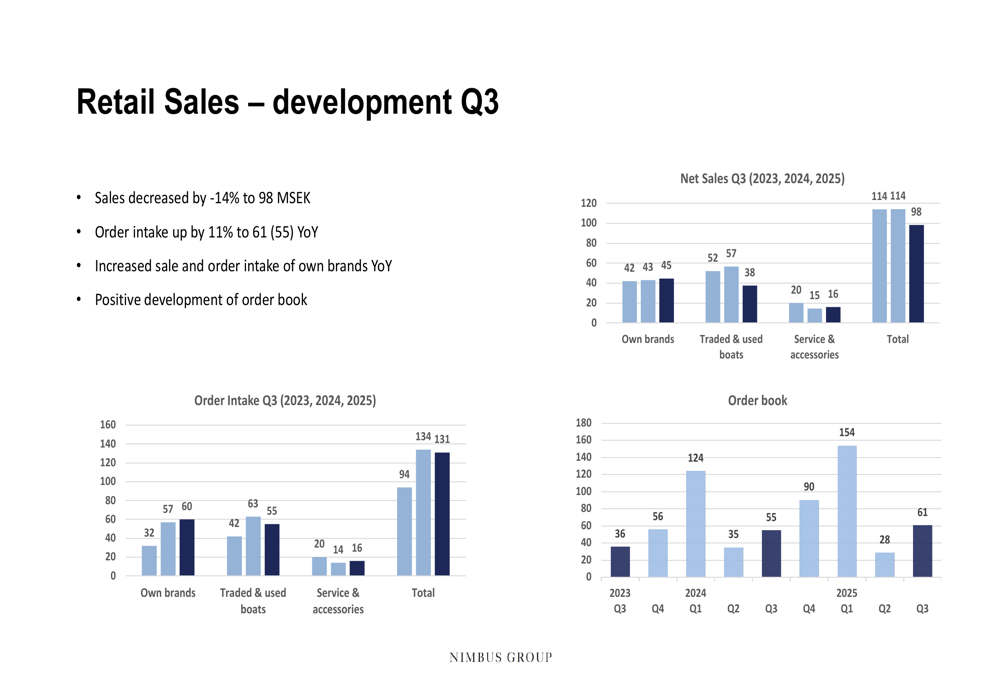

Retail sales fared somewhat better, decreasing by 14% to 98 MSEK. Encouragingly, order intake for retail sales increased by 11% to 61 MSEK year-over-year, with the company noting increased sales and order intake for its own brands.

The retail sales performance is detailed in this breakdown:

Financial Position & Outlook

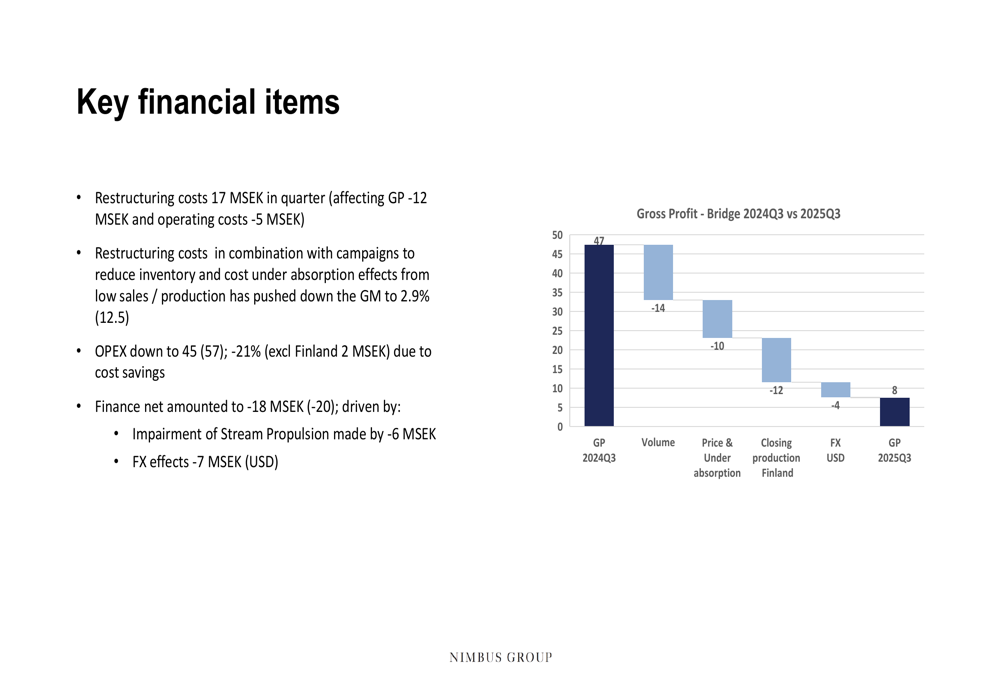

Nimbus Group’s gross margin was severely impacted by several factors in Q3, as illustrated in the following bridge chart:

The company incurred restructuring costs of 17 MSEK during the quarter, with 12 MSEK affecting gross profit and 5 MSEK impacting operating costs. These restructuring costs, combined with campaigns to reduce inventory and cost under-absorption effects from low sales and production, pushed the gross margin down to 2.9%.

On a positive note, operating expenses decreased by 21% to 45 MSEK (from 57 MSEK), reflecting the company’s cost-saving initiatives. The finance net amounted to -18 MSEK (-20 MSEK), which included a 6 MSEK impairment of Stream Propulsion and 7 MSEK in FX effects related to USD.

The company’s working capital management showed signs of improvement:

Inventory was reduced by 29 MSEK during the quarter, and net working capital turned downward year-over-year for the first time since Q4 2021, indicating progress in the company’s efforts to manage its balance sheet during the downturn.

Strategic Initiatives

Despite the challenging environment, Nimbus Group highlighted several strategic initiatives aimed at improving performance. The company is focusing on turning around its North American operations, securing brand and product portfolio performance, improving commercial capabilities, and maintaining strict cost control and cash management.

The presentation also noted several market highlights:

The company has expanded its dealer network with new appointments in Switzerland, Turkey, Florida, and Oslo. Additionally, the Swedish Defense Material Administration (FMV) has approved the design of the Alukin workboat, potentially opening new opportunities in the commercial segment.

Product innovation remains a priority, with the launch of the Edgewater 250 CC for the North American market and the public launch of the Flagship 495Fly at the Fort Lauderdale International Boat Show in mid-October. The company also announced that its Aquador 400HT has been nominated for "Best for Family 2025" in the Best of Boats awards.

CEO Johan Inden emphasized during the earnings call that "Each brand, each product in the portfolio has to be able to defend its own existence," underscoring the company’s focus on portfolio optimization. He also stressed the importance of effective cash management, noting that "Managing your working capital and your cash is everything in the marine business."

Looking ahead, Nimbus Group maintains its long-term financial targets of growth exceeding 10%, an EBITA margin of 10%, a capital structure with no financial debt, and a dividend policy of 30%, though current market conditions present significant challenges to achieving these goals in the near term.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.