Moody’s downgrades Senegal to Caa1 amid rising debt concerns

Introduction & Market Context

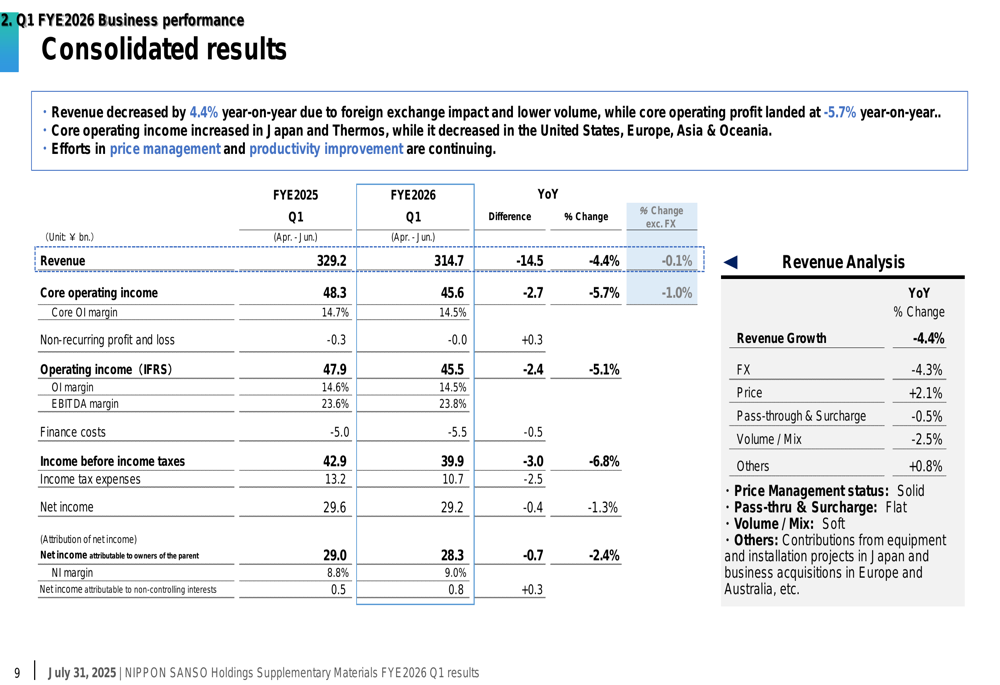

Nippon Sanso Holdings (TYO:4091) reported its first quarter results for the fiscal year ending March 2026 on July 31, 2025, revealing a decline in both revenue and core operating income. The industrial gas specialist faced headwinds from foreign exchange impacts and lower volumes across most regions, though price management initiatives helped partially offset these challenges.

The company’s stock has recently declined 2.61% to ¥5,110, reflecting investor reaction to the mixed quarterly performance. Despite the challenging start to the fiscal year, management maintained its full-year forecast, suggesting confidence in improvement over the coming quarters.

Quarterly Performance Highlights

Nippon Sanso reported Q1 FYE2026 revenue of ¥314.7 billion, down 4.4% year-on-year, while core operating income decreased 5.7% to ¥45.6 billion. The revenue decline was primarily attributed to foreign exchange impact (-4.3%) and lower volume/mix (-2.5%), partially offset by price increases (+2.1%).

As shown in the following consolidated results breakdown:

The company’s net income attributable to owners of the parent decreased 3.9% to ¥27.4 billion. Despite these declines, management emphasized its focus on maintaining profitability through price management and productivity improvements across its operations.

Segment Performance Analysis

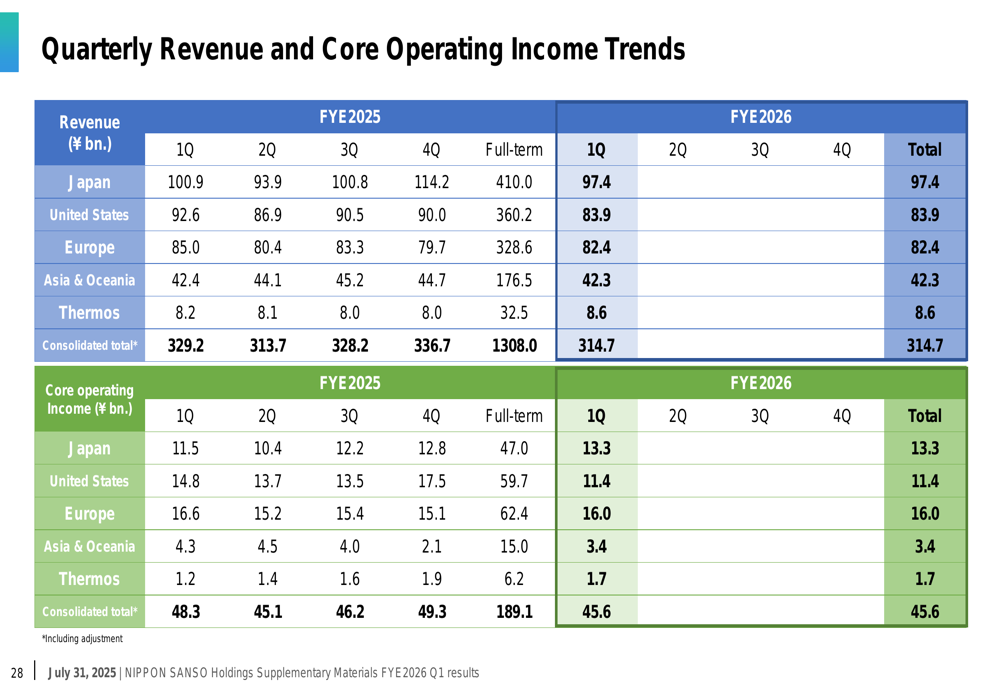

Nippon Sanso’s performance varied significantly across its geographic segments, with Japan and Thermos showing profit growth while the United States and Asia & Oceania experienced substantial declines.

In Japan, revenue decreased 3.5% to ¥97.4 billion, but segment income increased 15.6% to ¥13.3 billion, driven by progress in electronics-related construction and installation, along with effective price management. The segment’s operating margin improved to 13.7%.

The United States segment faced the most significant challenges, with revenue declining 9.3% to ¥83.9 billion and segment income dropping 22.6% to ¥11.4 billion. The company noted weakness in sales of products beyond bulk and onsite offerings.

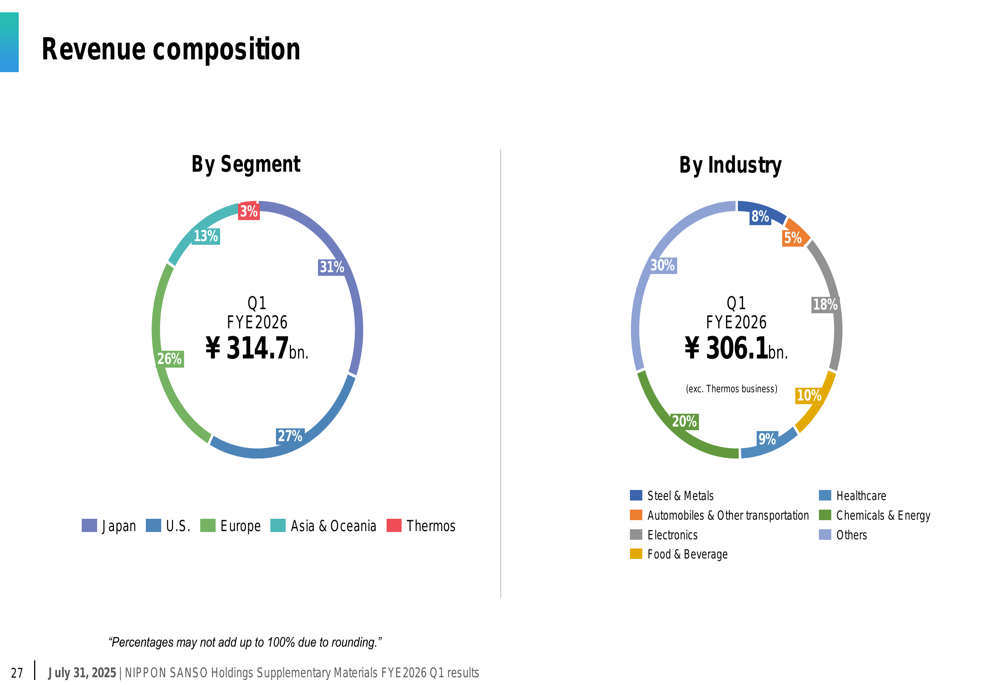

The following chart illustrates the company’s revenue composition by segment and industry:

Europe delivered relatively stable performance with revenue of ¥82.4 billion (-3.1%) and segment income of ¥16.0 billion (-3.6%). The European operations maintained the highest operating margin among all segments at 19.5%.

The Asia & Oceania segment saw a modest 0.3% revenue decline to ¥42.3 billion, but segment income fell sharply by 20.4% to ¥3.4 billion, resulting in an 8.1% operating margin.

A bright spot in the quarterly results was the Thermos segment, which achieved 4.6% revenue growth to ¥8.6 billion and an impressive 38.6% increase in segment income to ¥1.7 billion. The company attributed this performance to successful new product launches in Japan.

The quarterly performance trends across segments can be seen in the following chart:

Strategic Initiatives & Sustainability

Nippon Sanso completed the acquisition of Coregas on July 1st, implementing a new management structure. The company continues to actively pursue investments while carefully assessing risks, including potential impacts from US tariff policies.

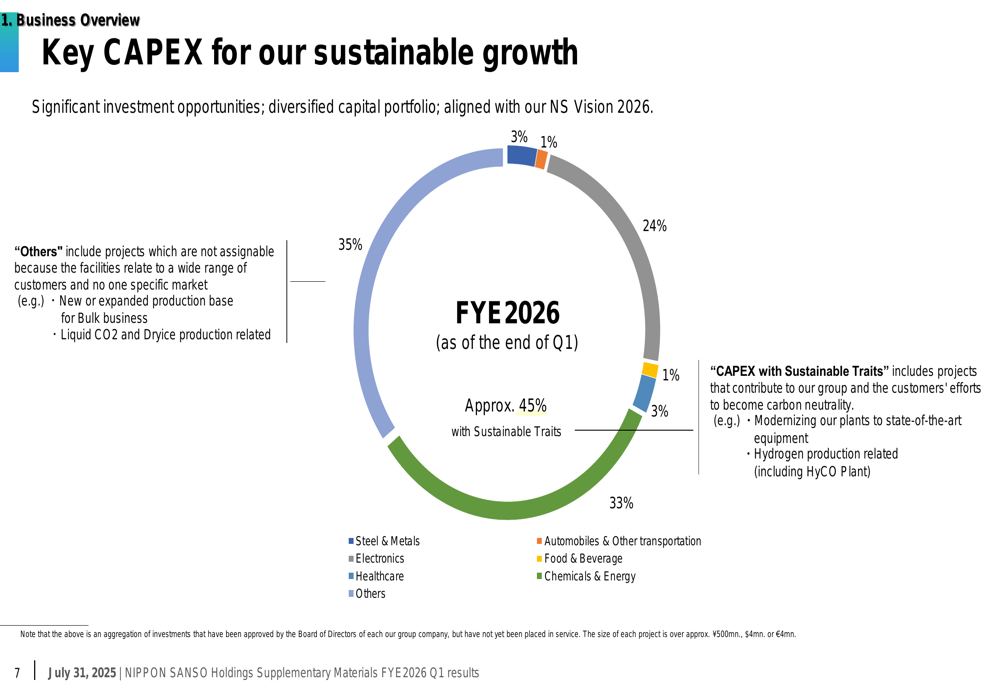

The company highlighted its commitment to sustainability, with approximately 45% of planned capital expenditure for FYE2026 classified as having "sustainable traits." These investments include projects contributing to carbon neutrality, such as plant modernization and hydrogen production initiatives.

The capital expenditure allocation by sector is illustrated below:

Electronics represents a significant focus area, accounting for 24% of planned CAPEX and 30% of overall revenue. Steel & metals remains the largest CAPEX category at 33%, reflecting the company’s continued commitment to its traditional industrial gas markets.

Forward-Looking Statements

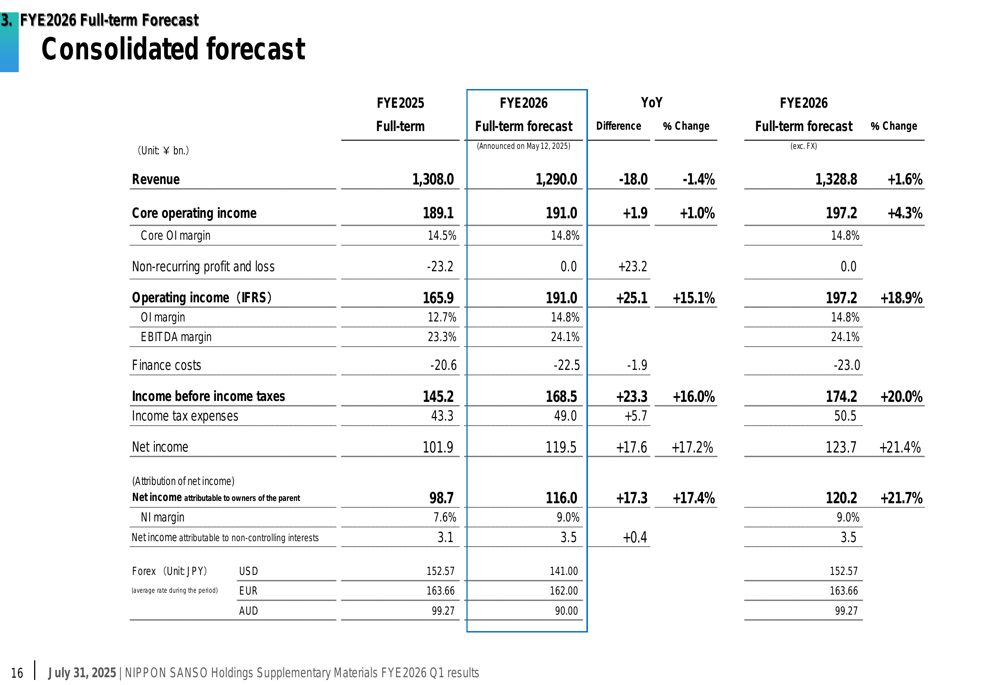

Despite the challenging first quarter, Nippon Sanso maintained its full-year FYE2026 forecast, projecting revenue of ¥1,290.0 billion (down 1.4% year-on-year) and core operating income of ¥191.0 billion (up 1.0%). The company expects net income attributable to owners of the parent to increase significantly by 17.4% to ¥116.0 billion.

The full-year forecast is detailed in the following chart:

These projections are based on foreign exchange rate assumptions of ¥141.00 per USD and ¥162.00 per EUR for the full fiscal year. The maintained guidance suggests management expects improved performance in the remaining quarters to offset the Q1 declines.

The company’s medium-term management plan continues to focus on cash management and greenhouse gas emissions reduction, with targets for improving ROCE and reducing its carbon footprint.

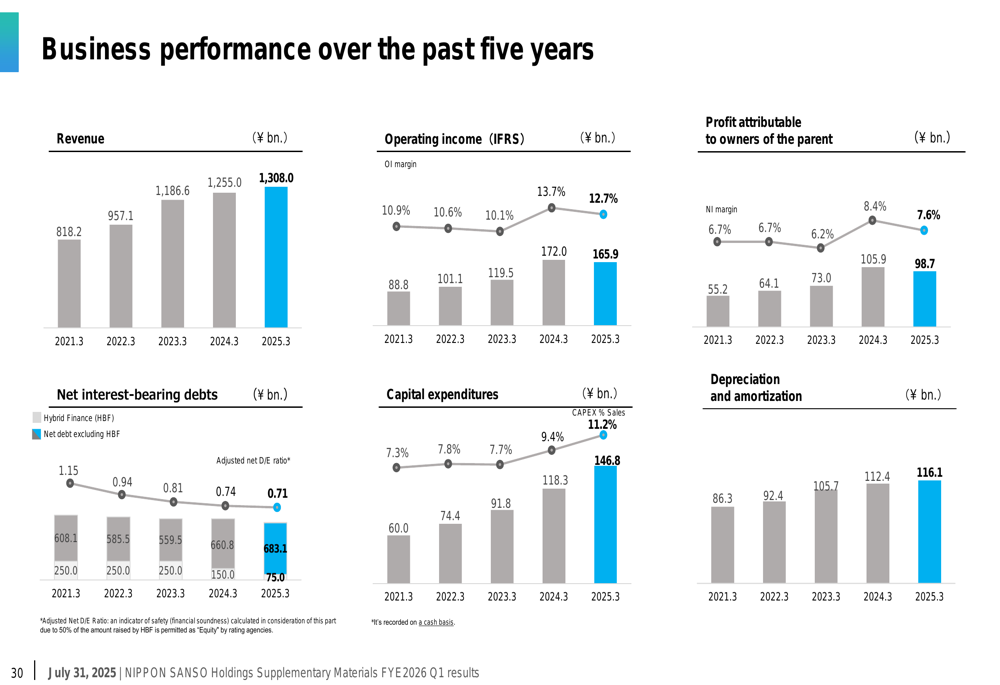

Nippon Sanso’s five-year performance trends provide context for evaluating the current results and outlook:

While the first quarter presented challenges, particularly in the US and Asia & Oceania segments, the company’s diversified geographic presence and strong position in the electronics sector provide a foundation for potential recovery in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.