Walmart halts H-1B visa offers amid Trump’s $100,000 fee increase - Bloomberg

Introduction & Market Context

nLIGHT Inc . (NASDAQ:LASR) presented its first quarter 2025 results on May 8, showing a significant recovery from the previous quarter’s disappointing performance. The laser manufacturer reported revenue and margins that exceeded expectations, primarily driven by strength in its Aerospace & Defense (A&D) segment. The company’s stock responded positively, rising 5.13% during regular trading hours and adding another 5.6% in after-hours trading.

This performance marks a notable turnaround from Q4 2024, when nLIGHT missed analyst expectations with an EPS of -$0.30 against a forecast of -$0.06, and revenue of $47.38 million versus projected $59.97 million.

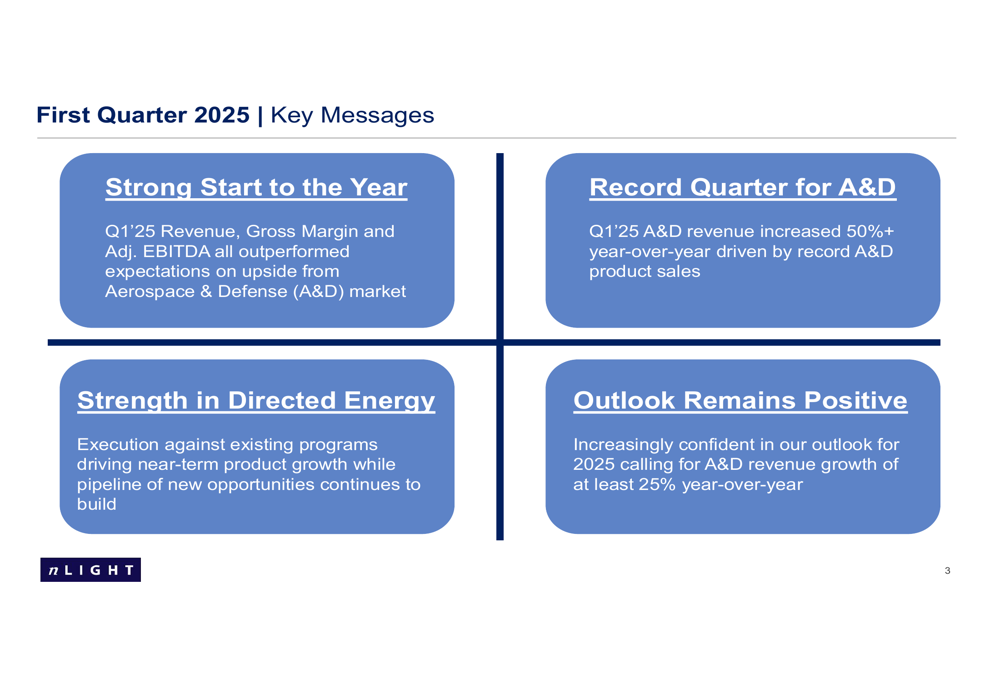

As shown in the following key messages from the company’s presentation, nLIGHT emphasized its strong start to 2025:

Quarterly Performance Highlights

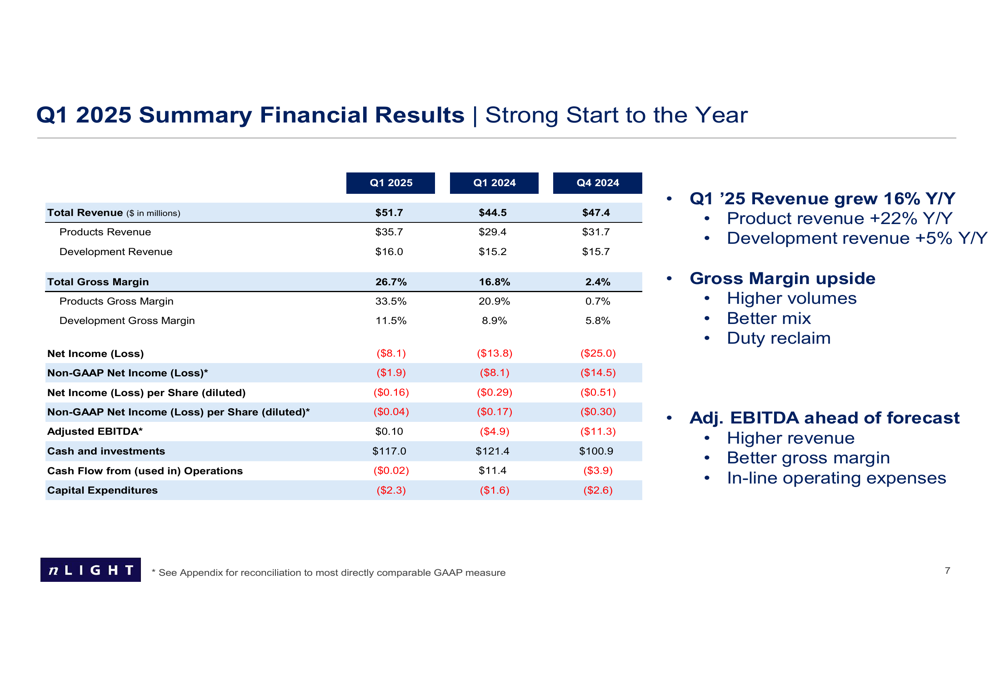

nLIGHT reported Q1 2025 revenue of $51.7 million, representing a 16% increase year-over-year and a 9% improvement sequentially. This performance exceeded the high end of the company’s guidance range. Product revenue grew 22% year-over-year to $35.7 million, while development revenue increased 5% to $16.0 million.

The company’s gross margin saw a dramatic improvement, reaching 26.7% overall and 33.5% for products, compared to just 2.4% and 0.7% respectively in Q4 2024. This recovery in margins was attributed to higher volumes, better product mix, and duty reclaim benefits.

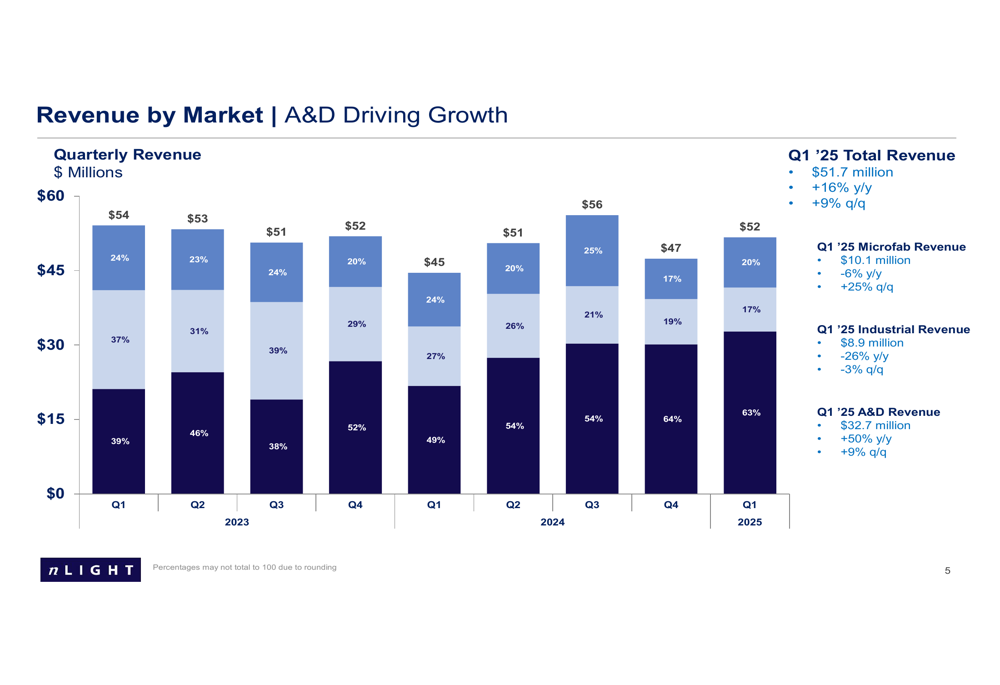

The following chart illustrates the company’s revenue breakdown by market segment, highlighting the growing importance of the A&D segment:

The A&D segment was the standout performer, with revenue increasing by more than 50% year-over-year to $32.7 million, representing 63% of total revenue. This contrasted sharply with the Industrial segment, which declined 26% year-over-year to $8.9 million, and the Microfabrication segment, which fell 6% to $10.1 million but showed a 25% sequential improvement.

Detailed Financial Analysis

nLIGHT’s financial results showed improvement across multiple metrics compared to both the previous quarter and the same period last year. The company reported a net loss of $8.1 million, or $0.16 per share, compared to a loss of $13.8 million, or $0.29 per share, in Q1 2024. On a non-GAAP basis, the net loss narrowed to $1.9 million, or $0.04 per share.

Notably, Adjusted EBITDA turned positive at $116,000, compared to negative $4.9 million in Q1 2024 and negative $11.3 million in Q4 2024. This improvement was driven by higher revenue, better gross margins, and disciplined operating expense management.

The comprehensive financial summary below shows the company’s performance across key metrics:

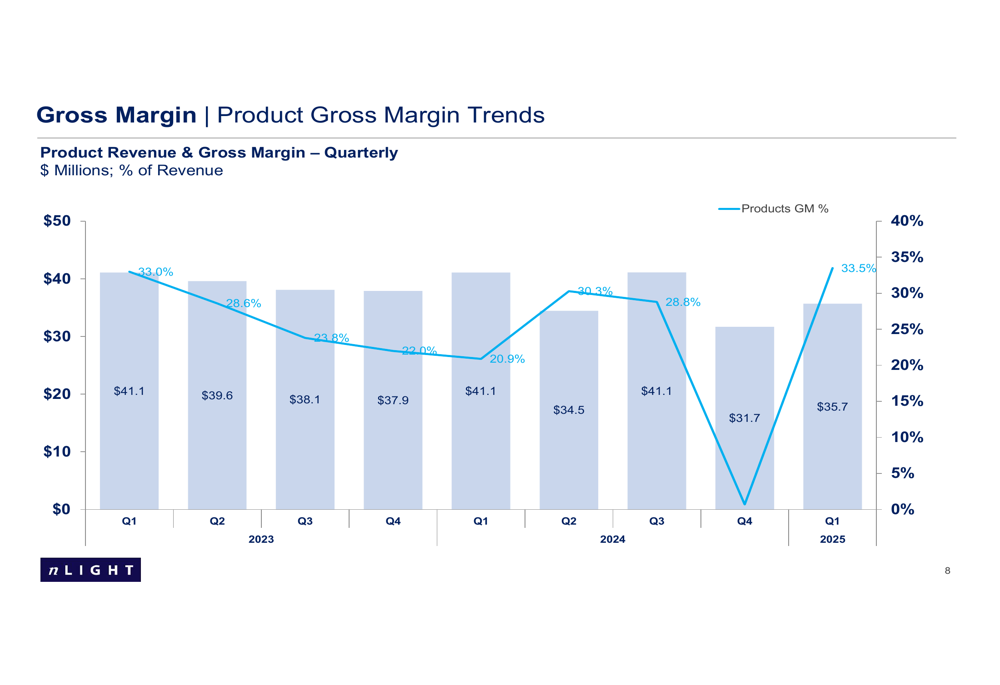

The company’s gross margin recovery is particularly noteworthy given the challenges faced in recent quarters. The following chart shows the product gross margin trend, which has rebounded strongly from the low point in Q4 2024:

nLIGHT maintained a strong balance sheet with $117.0 million in cash and marketable securities, up from $100.9 million at the end of Q4 2024. The company drew down $20 million from its $40 million line of credit during the quarter. Working capital management also showed improvement, with days of inventory reduced to 87 days in Q1 2025 from 152 days in Q1 2023.

Strategic Initiatives & Segment Performance

nLIGHT’s strategic focus on the Aerospace & Defense market is clearly paying dividends, with the segment delivering record quarterly product revenue. The company highlighted its execution against existing Directed Energy programs as a key driver of near-term product growth, while noting that the pipeline of new opportunities continues to build.

The commercial segments presented a more challenging picture. The Industrial segment continues to face headwinds, while Microfabrication showed sequential improvement from Thai manufacturing operations but remains below year-ago levels.

Operating expenses remained well-controlled at $17.8 million on a non-GAAP basis in Q1 2025, reflecting the company’s disciplined approach to cost management while continuing to invest in strategic growth areas.

Forward-Looking Statements

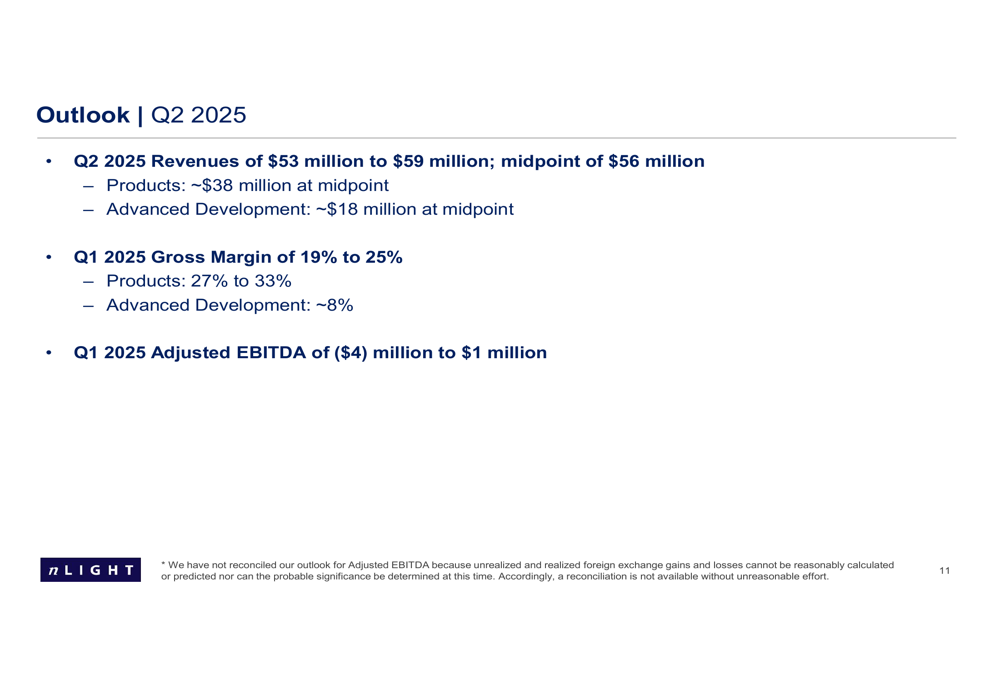

Looking ahead to Q2 2025, nLIGHT provided the following guidance:

The company expects Q2 2025 revenue between $53 million and $59 million, with a midpoint of $56 million. This comprises approximately $38 million in Products revenue and $18 million in Advanced Development revenue. Gross margin is projected to be between 19% and 25%, with Products gross margin of 27% to 33% and Advanced Development gross margin of approximately 8%. Adjusted EBITDA is expected to range from negative $4 million to positive $1 million.

nLIGHT expressed increasing confidence in its outlook for 2025, projecting A&D revenue growth of at least 25% year-over-year. This optimism is supported by the company’s strong performance in the A&D segment in Q1 and its growing pipeline of opportunities in Directed Energy applications.

The guidance suggests a more cautious outlook for the commercial segments, with the company continuing to navigate challenging market conditions in Industrial and Microfabrication. However, the sequential improvement in Microfabrication from Thai manufacturing operations provides some encouragement for potential recovery in this segment.

Overall, nLIGHT’s Q1 2025 results represent a significant improvement from the previous quarter’s disappointing performance, with the A&D segment emerging as the clear growth driver for the company. While challenges remain in the commercial segments, the company’s strategic focus on defense applications appears to be yielding positive results.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.