Bitcoin price today: nosedives to $83k as mixed US jobs data dents Fed cut hopes

Introduction & Market Context

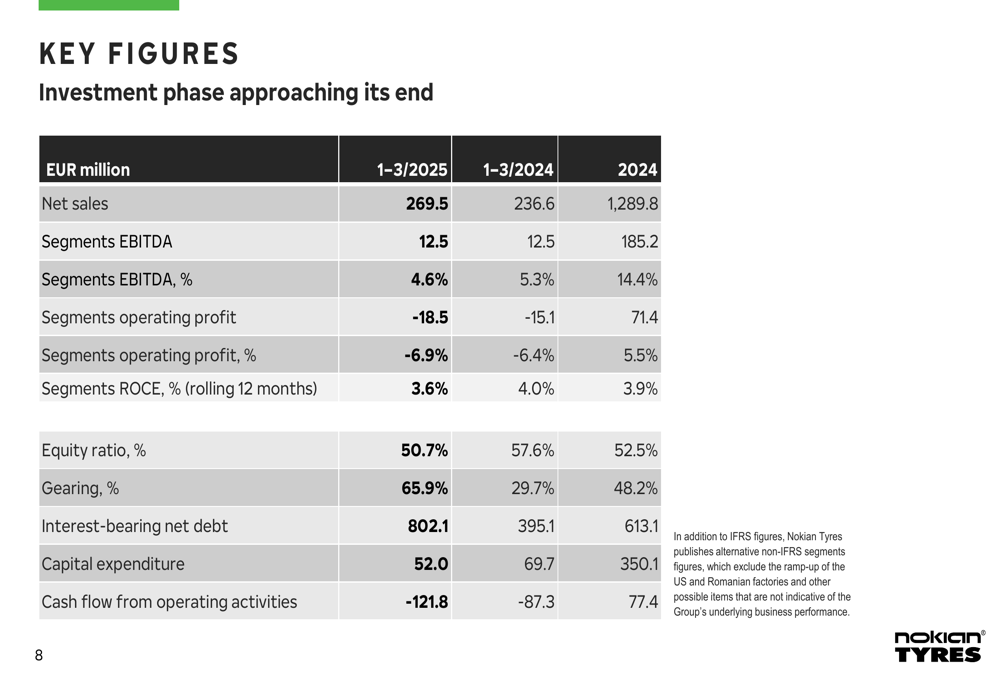

Nokian Tyres (HEL:TYRES) reported strong sales growth but declining profitability in its Q1 2025 results presentation on May 6, 2025. The Finnish tire manufacturer saw net sales increase by 14.2% with comparable currencies to €269.5 million, outperforming the market in all regions despite challenging conditions. However, the company’s segments operating profit declined to €-18.5 million (-6.9% of net sales) compared to €-15.1 million (-6.4%) in Q1 2024.

The market reacted negatively to the results, with Nokian’s stock price falling 12.41% to €6.14 on the day of the announcement, approaching its 52-week low of €5.95 and well below its high of €9.20.

As shown in the following key figures from the presentation:

Quarterly Performance Highlights

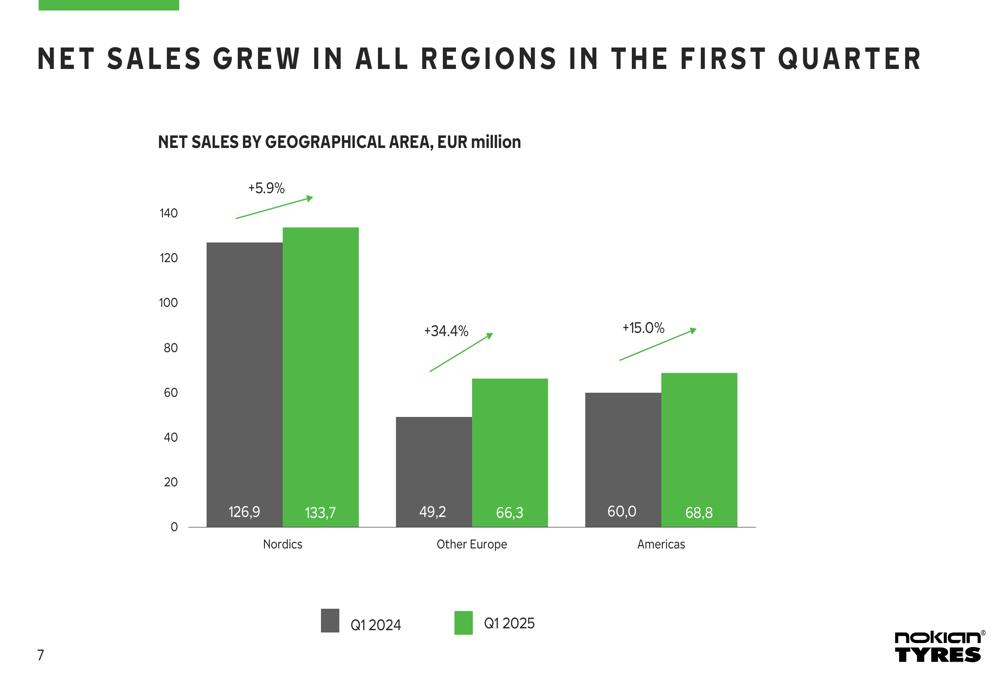

Nokian Tyres reported sales growth across all geographical regions in Q1 2025. The strongest performance came from Other Europe with a 34.4% increase to €66.3 million, while the Americas grew by 15.0% to €68.8 million and the Nordics by 5.9% to €133.7 million. This regional diversification highlights the company’s expanding global footprint beyond its traditional Nordic stronghold.

The following chart illustrates this geographical sales distribution:

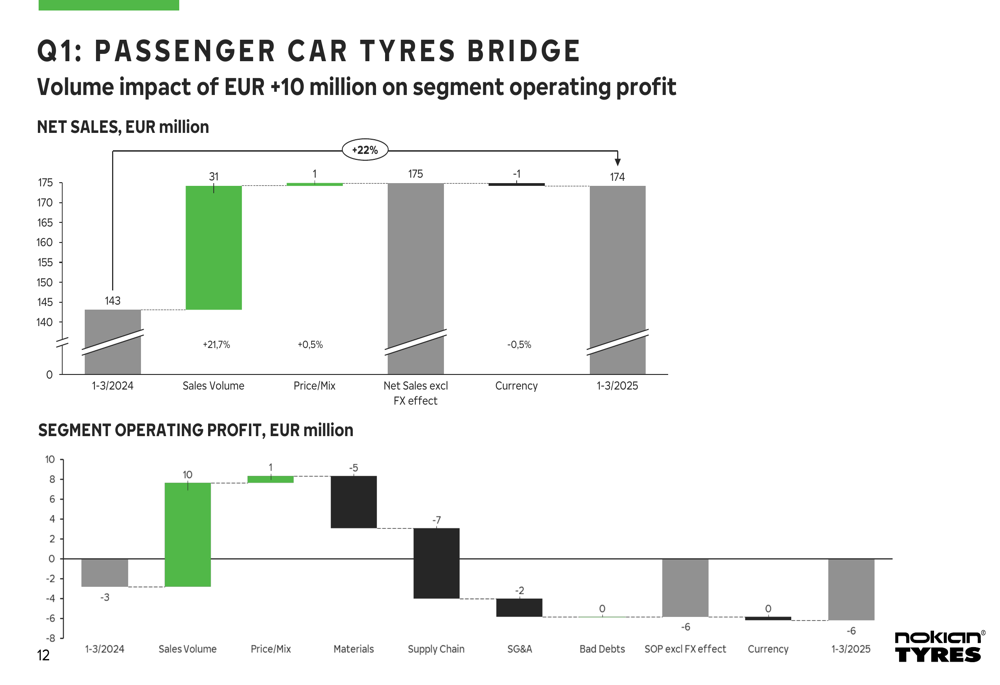

In the Passenger Car Tyres segment, net sales increased to €174.1 million (from €143.1 million), driven by higher sales volumes due to increased product availability. However, profitability decreased to -3.6% (from -2.0%) due to higher raw material and SG&A costs. The company implemented price increases in Q1 which are expected to offset increased raw material costs from Q2 onwards.

The Heavy Tyres business unit delivered solid performance despite market weakness, with net sales increasing to €55.8 million (from €55.1 million) and segment operating profit improving to €7.3 million or 13.0% of net sales (from €6.3 million or 11.5%). This improvement was mainly attributed to a favorable channel mix.

The Vianor retail chain saw net sales with comparable currencies increase by 5.7% to €58.8 million (from €55.9 million), though the first quarter is seasonally low for this segment, resulting in a negative operating profit of €-15.4 million.

Financial Analysis

While sales volumes increased significantly, Nokian’s profitability faced pressure from multiple directions. The following bridge analysis illustrates the key factors affecting the Passenger Car Tyres segment:

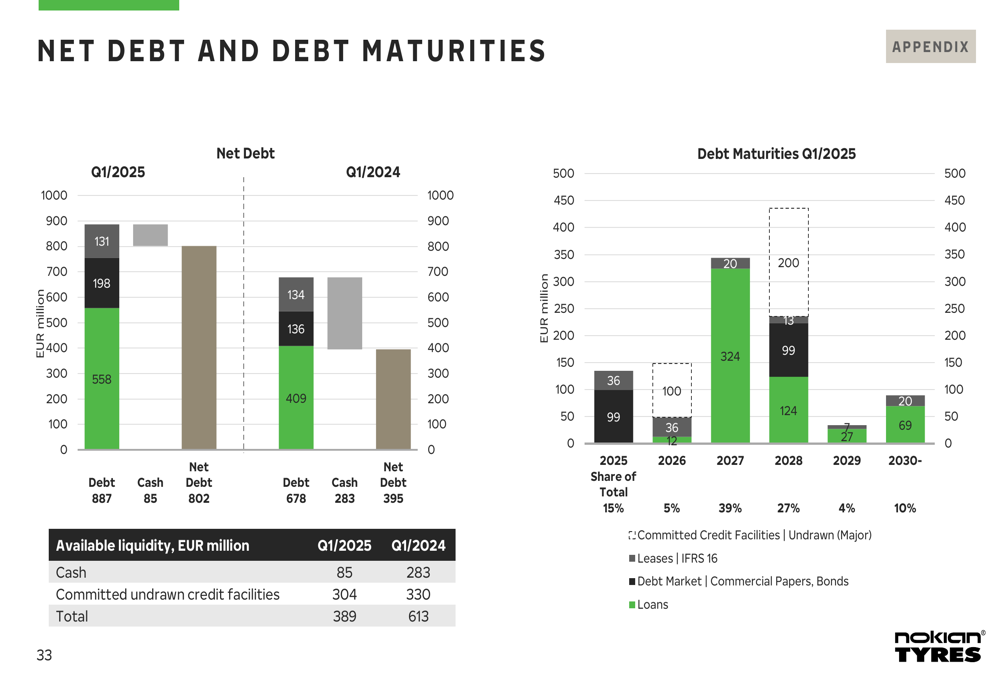

The company’s financial position shows increasing leverage as it continues its investment phase. Interest-bearing net debt rose to €802.1 million (from €395.1 million in Q1 2024), and gearing increased to 65.9% (from 29.7%). Cash flow from operating activities was negative at €-121.8 million (compared to €-87.3 million).

The following chart provides an overview of the company’s debt position and available liquidity:

Strategic Initiatives

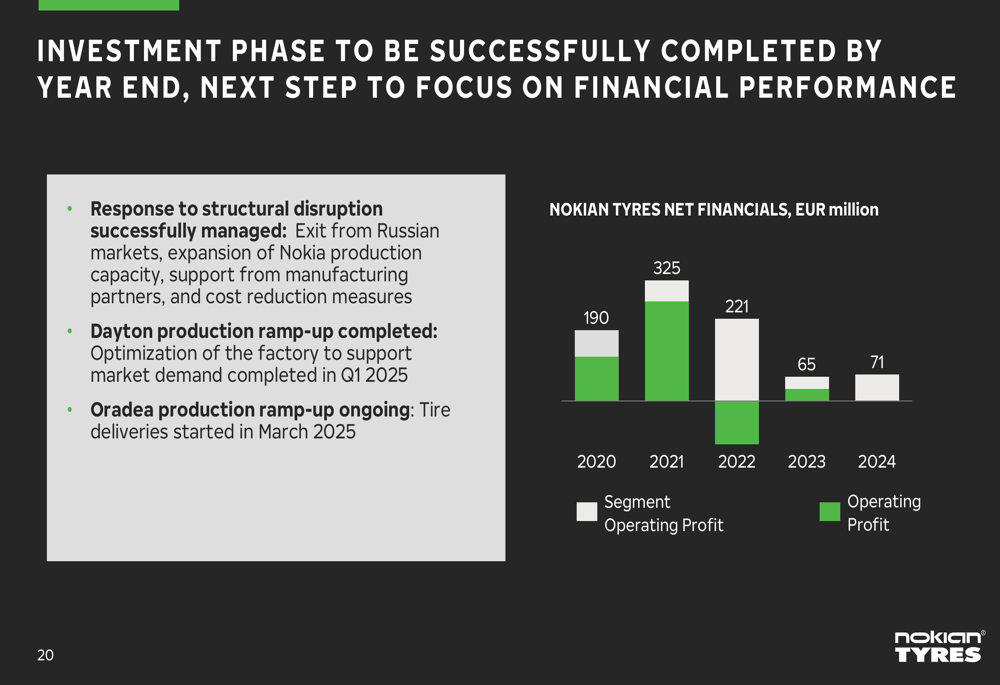

Nokian Tyres is approaching the end of its significant investment phase, which included establishing new production facilities following its exit from the Russian market. The company expects to complete this phase by the end of 2025, with net investments for the year estimated at €200 million. Total (EPA:TTEF) investments for 2023-2025 are projected to reach approximately €800 million, after which the company plans to return to an average capex of around €120 million.

As illustrated in the following investment timeline:

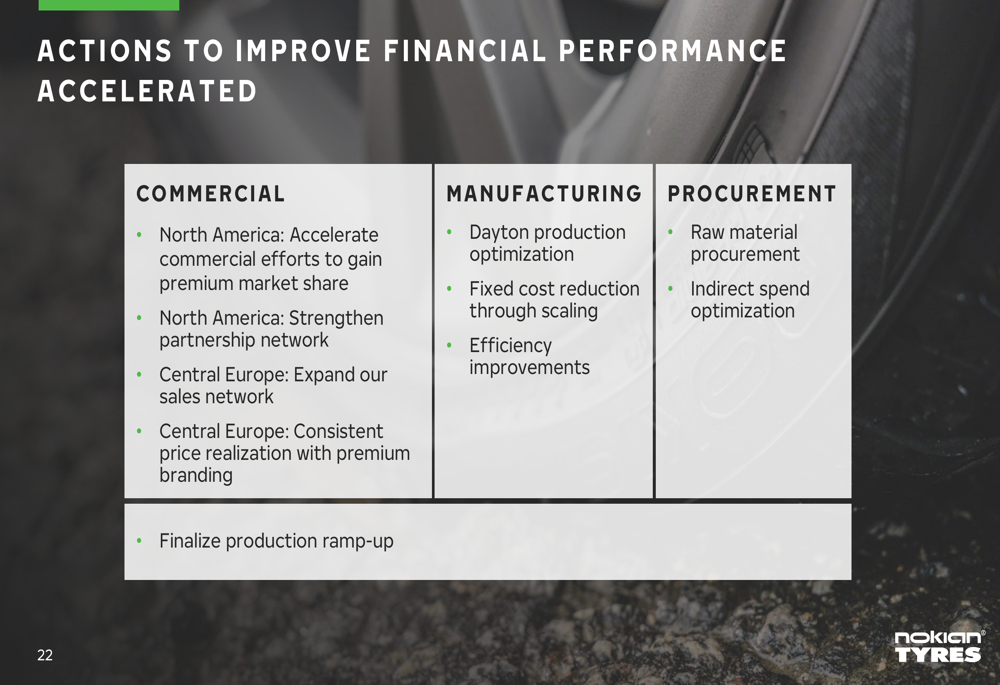

To address profitability challenges, Nokian is accelerating actions to improve financial performance across multiple areas:

The company has implemented a new operating model with stronger P&L and KPI ownership and accountability. This organizational change aims to drive systematic follow-ups and reporting practices to ensure delivery of results.

Forward-Looking Statements

Nokian Tyres maintained its guidance for 2025, expecting net sales to grow and segments operating profit as a percentage of net sales to improve compared to the previous year. The company’s assumptions include tire demand in its markets remaining at the previous year’s level, with growth coming from increasing capacity in the Romanian and US factories as well as good availability of finished goods inventories.

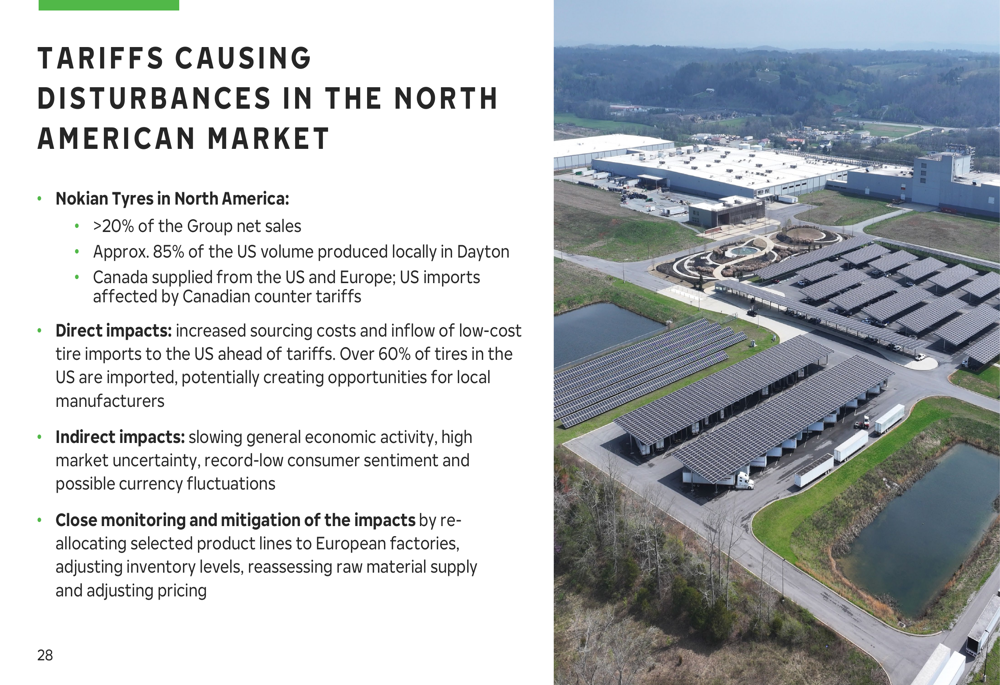

The company is closely monitoring tariff impacts in North America, where they account for over 20% of group net sales. Approximately 85% of US volume is produced locally in Dayton, which helps mitigate some tariff effects, but Canadian counter-tariffs are affecting US imports.

Looking ahead, Nokian is transitioning from its investment phase to a growth phase, with capital allocation priorities shifting accordingly. The company aims to substantially improve operating cash flow, maintain capex at around €120 million annually, and target a net debt to EBITDA ratio of 1-2x.

As Nokian Tyres navigates this transition period, the company faces both opportunities and challenges. While sales growth remains strong and new production facilities are coming online, profitability pressures and market uncertainties, particularly related to tariffs and raw material costs, continue to weigh on performance. The effectiveness of the company’s accelerated improvement actions will be critical in determining its ability to deliver on its ambitious financial targets in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.