Stock market today: S&P 500 extends monthly win streak despite Nvidia-led stumble

Introduction & Market Context

Norconsult ASA (OB:NORCO) presented its Q1 2025 interim results on May 14, 2025, reporting moderate organic growth and significantly improved profitability, largely influenced by favorable calendar effects. The Nordic engineering and design firm saw its stock close at NOK 47.3 on May 13, down 0.84% ahead of the results announcement, reflecting cautious investor sentiment.

The company continues to navigate varying market conditions across its segments, with weakness in private Buildings & Architecture offset by strength in public sector projects and steady performance in Infrastructure and Energy sectors. This diversification strategy has proven effective as Norconsult maintains growth momentum from the 7% organic growth reported in Q4 2024.

Quarterly Performance Highlights

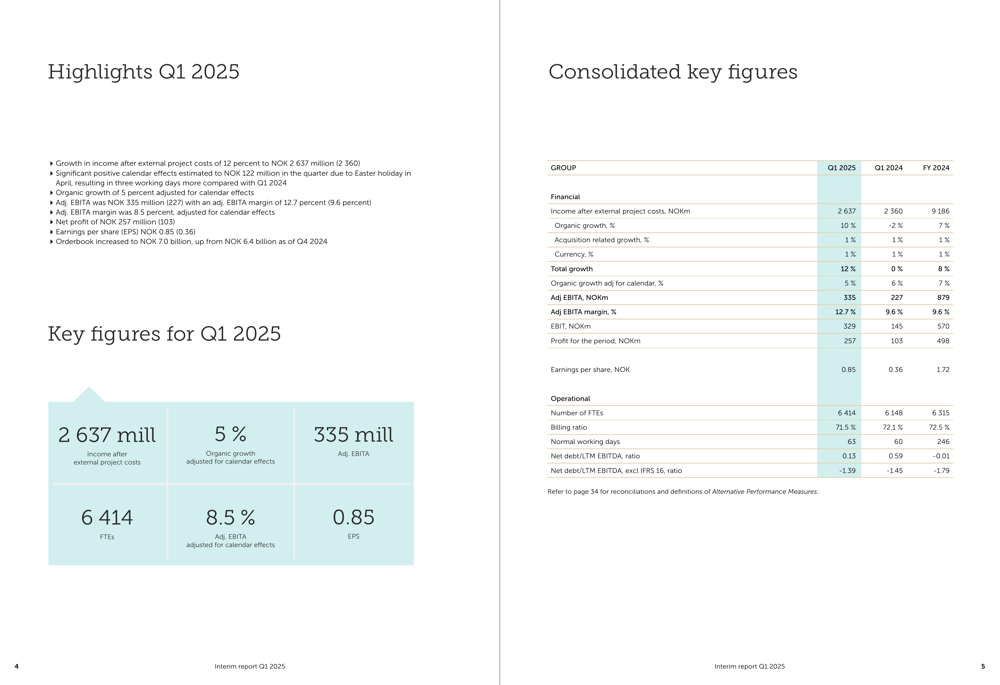

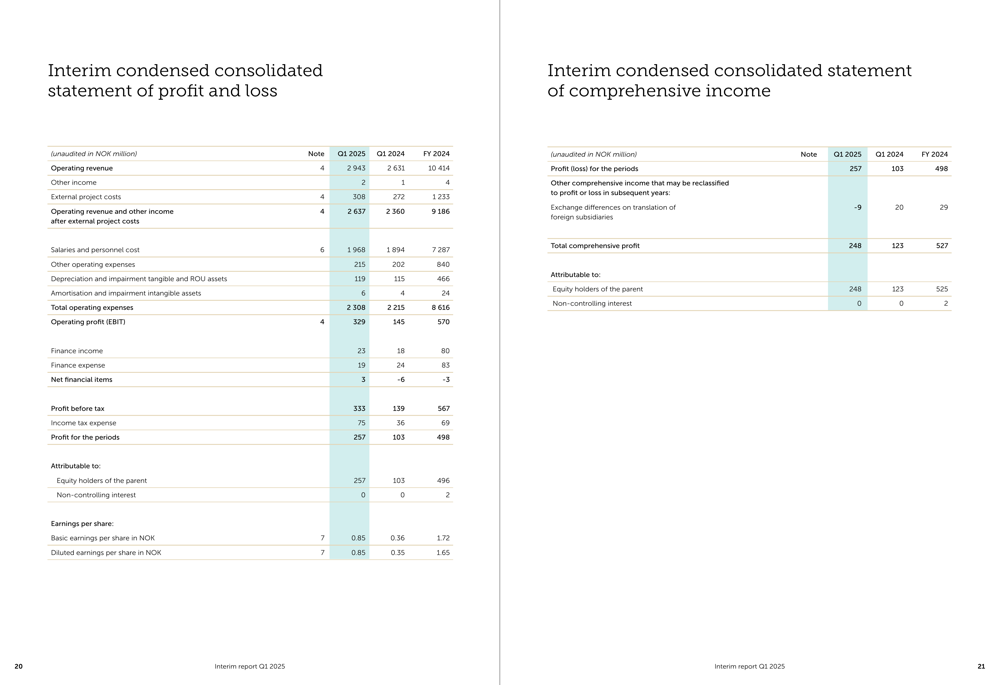

Norconsult reported income after external project costs of NOK 2,637 million for Q1 2025, representing a 12% increase from NOK 2,360 million in the same period last year. However, the company highlighted that this performance was significantly boosted by calendar effects related to Easter timing, which provided three additional working days compared to Q1 2024.

"Norconsult delivers moderate revenue growth and profitability in the first quarter of 2025," stated CEO Egil Hogna, noting that when adjusted for calendar effects, the company achieved 5% organic growth, driven by higher employee numbers and billing rates.

Adjusted EBITA reached NOK 335 million, up from NOK 227 million in Q1 2024, resulting in a margin of 12.7% compared to 9.6% in the previous year. However, when accounting for the estimated NOK 122 million positive impact from calendar effects, the adjusted EBITA margin was 8.5%, actually lower than the previous year’s performance.

Net profit more than doubled to NOK 257 million from NOK 103 million, with earnings per share increasing to NOK 0.85 from NOK 0.36 in Q1 2024. The company’s orderbook showed strong growth, reaching NOK 7.0 billion at quarter-end, up from NOK 6.4 billion at the end of 2024.

Detailed Financial Analysis

The company’s financial performance reflects both organic growth and strategic expansion. Operating revenue increased by 12% to reach NOK 2,945 million, with organic growth contributing 5% when adjusted for calendar effects.

Despite the impressive headline numbers, there are some underlying concerns. The adjusted EBITA margin, when normalized for calendar effects, was negatively impacted by a lower billing ratio of 71.5% compared to 72.1% in the same period last year, as well as increased vacation time at the beginning of the year.

The company maintains a strong balance sheet with a net debt to LTM EBITDA ratio of just 0.13, significantly improved from 0.59 in Q1 2024. Excluding IFRS 16 effects, the company actually has a net cash position, with a ratio of -1.39.

Strategic Initiatives & Market Position

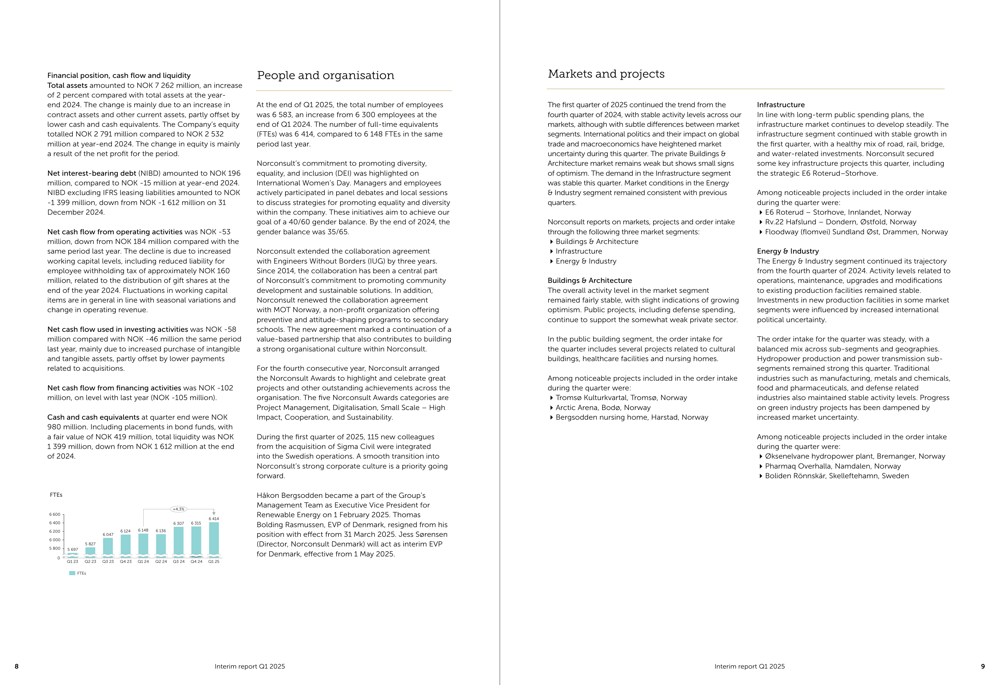

Norconsult continues to expand its workforce, with total employees reaching 6,583 at the end of Q1 2025, up from 6,300 in Q1 2024. Full-time equivalents (FTEs) increased to 6,414 from 6,148 in the same period last year, supporting the company’s capacity for future growth.

The company highlighted its commitment to diversity, equality, and inclusion, particularly on International Women’s Day. Norconsult also extended its collaboration agreement with Engineers Without Borders for three years and renewed its partnership with MOT Norway, underscoring its focus on corporate social responsibility.

Market conditions vary across segments, with the CEO noting that "uncertainties from international politics affect markets differently." While the private Buildings & Architecture market remains weak, there are signs of optimism. The public sector and defense markets are providing compensation for this weakness, while the Infrastructure segment shows stable demand.

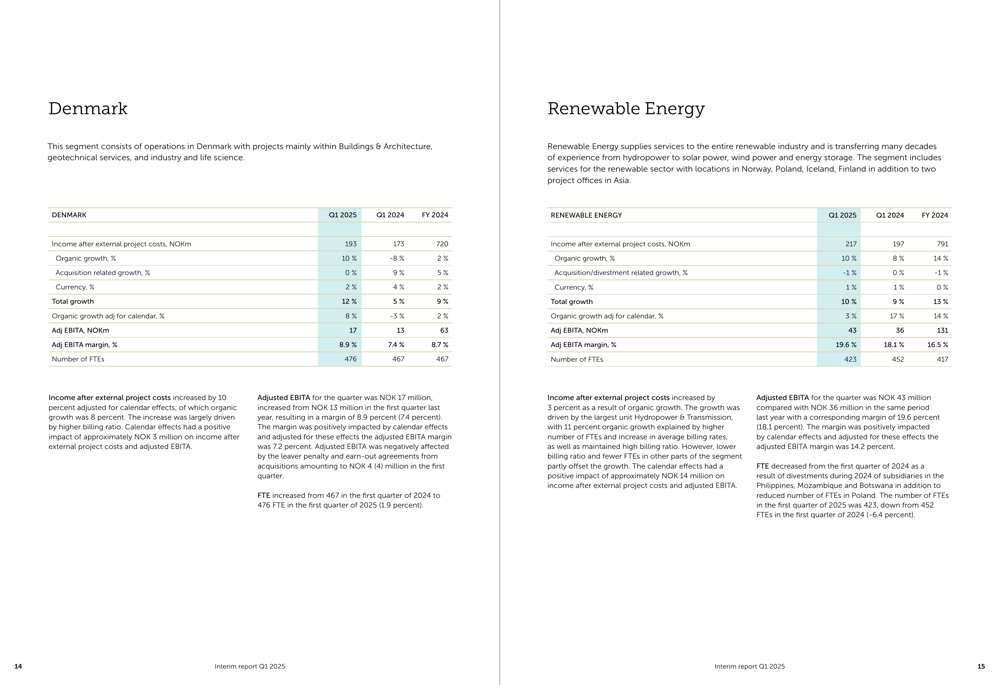

The Energy & Industry segment continues to see high demand in hydropower and transmission projects, though greenfield industry is affected by broader macroeconomic developments. Key projects highlighted include the E6 Roterud-Storhove road assignment, Øksenelvane hydropower plant, and Pharmaq Overhalla.

Forward-Looking Statements

Norconsult’s growing orderbook, which reached NOK 7.0 billion at the end of Q1 2025, provides a solid foundation for future revenue. The company’s diversification across market segments positions it well to navigate varying market conditions, with the ability to reallocate capacity between sectors as needed.

The Norway Head Office business area, which includes operations in the greater Oslo area and supports the Group with expertise, showed particularly strong performance with income after external project costs of NOK 802 million and organic growth of 11%. This segment achieved an adjusted EBITA margin of 15.4%, highlighting the strength of Norconsult’s core Norwegian operations.

While the company faces challenges from international political uncertainties and varying market conditions across segments, its diversified business model and strong orderbook suggest continued resilience. Investors will be watching closely to see if Norconsult can maintain its growth trajectory when the favorable calendar effects of Q1 are no longer present in future quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.