Gold prices snap 4-day losing streak after Fed rate cut, Trump-Xi meeting

Introduction & Market Context

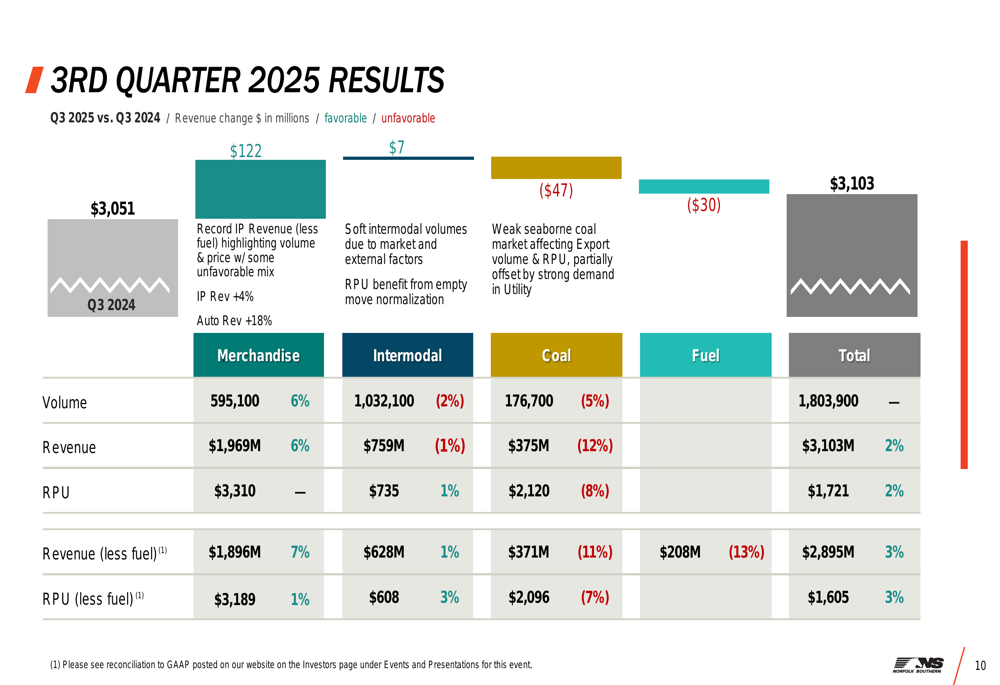

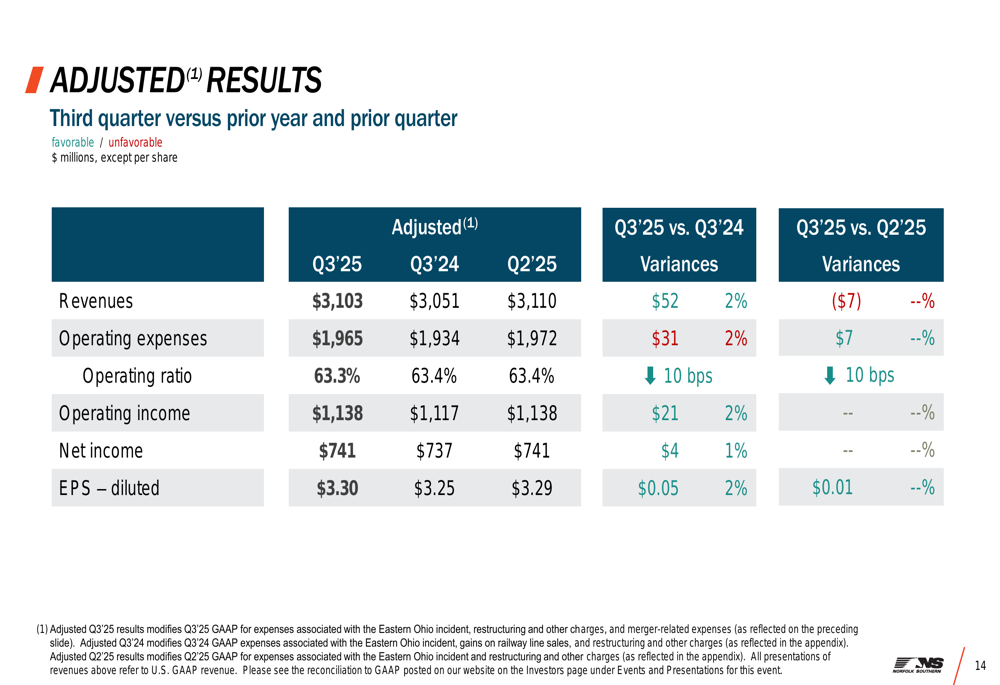

Norfolk Southern Corporation (NYSE:NSC) reported a 2% year-over-year revenue increase in its third quarter of 2025, reaching $3.103 billion despite facing headwinds in its intermodal and coal segments. The railway operator presented its quarterly results during an earnings call on October 23, 2025, highlighting operational improvements and cost-cutting initiatives that helped deliver adjusted earnings per share of $3.30, slightly above analyst expectations of $3.20.

The stock reacted negatively in aftermarket trading, declining 1.66% to $286.97, as investors processed the mixed results and cautious outlook for the remainder of the year. Norfolk Southern’s performance reflects broader challenges in the rail transportation sector, including a soft truck freight environment and weakening seaborne coal prices.

Quarterly Performance Highlights

Norfolk Southern’s Q3 2025 financial results showed modest improvement over the prior year, with adjusted operating income reaching $1.138 billion compared to $1.117 billion in Q3 2024. The company maintained stable performance quarter-over-quarter, with identical operating income figures in Q2 and Q3 2025.

As shown in the following quarterly results breakdown:

The merchandise segment emerged as the primary growth driver, with revenue increasing 6% year-over-year to $1.969 billion, supported by a 6% volume increase. However, this growth was partially offset by declines in both intermodal and coal segments, which saw revenue decreases of 1% and 12% respectively. The company’s overall volume increased by 1% compared to Q3 2024.

Adjusted earnings per share improved from $3.25 in Q3 2024 to $3.30 in Q3 2025, as illustrated in this comparison of adjusted results:

Operational Improvements and Cost Initiatives

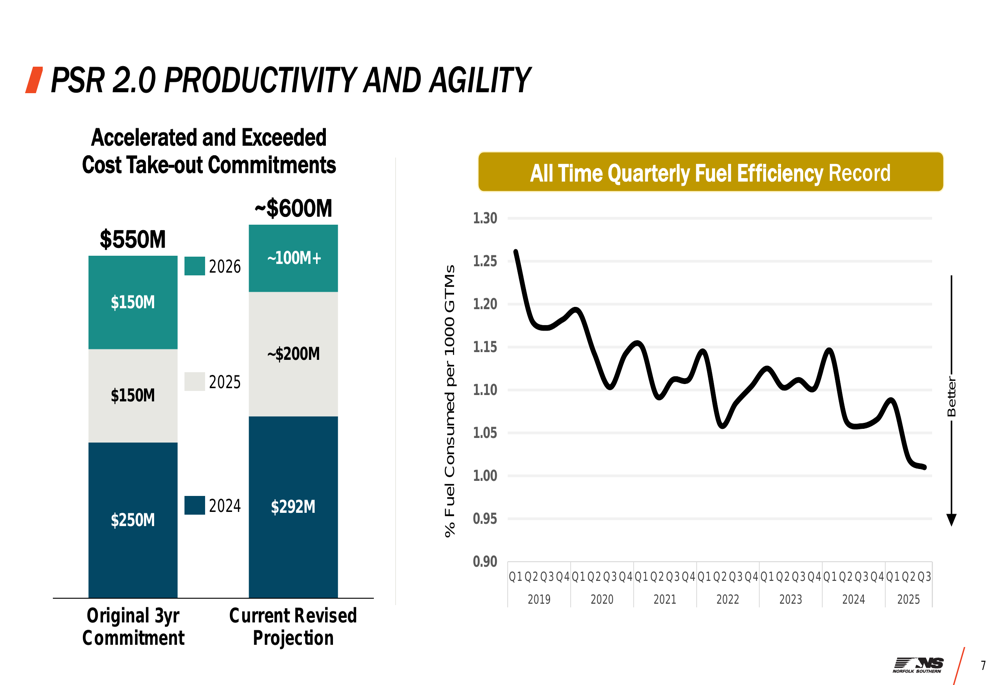

A standout achievement highlighted in Norfolk Southern’s presentation was the company’s success in exceeding its cost reduction targets. The railroad has revised its three-year cost take-out commitment upward from $550 million to approximately $600 million, having already achieved $292 million in 2024 against an original target of $250 million.

The following chart illustrates the accelerated cost savings and record fuel efficiency:

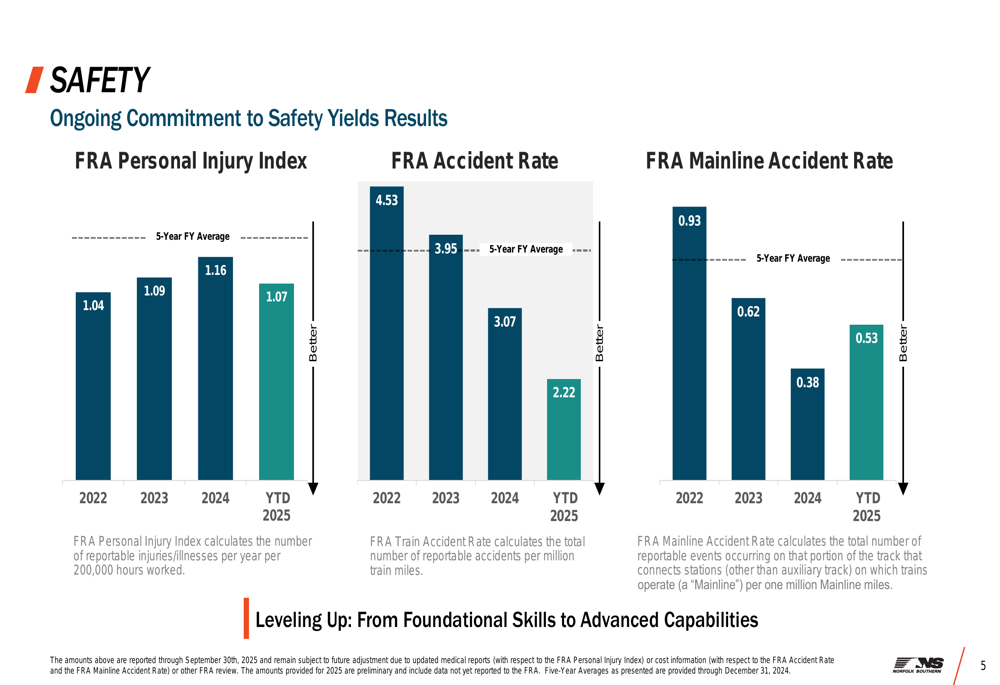

The company also reported significant progress in safety metrics, with the FRA Accident Rate improving from 3.07 in 2024 to 2.22 year-to-date in 2025, representing a continuation of a multi-year positive trend. The FRA Personal Injury Index also showed improvement, decreasing from 1.16 in 2024 to 1.07 year-to-date in 2025.

These safety improvements are visualized in the following chart:

Norfolk Southern has made substantial investments in technology to enhance operational efficiency. The company’s Premier Wheel Integrity System has contributed to a 36% year-over-year reduction in wayside stops, with approximately 4.2 million axles inspected daily. This technological advancement, along with other initiatives, supports the company’s focus on network fluidity and asset utilization.

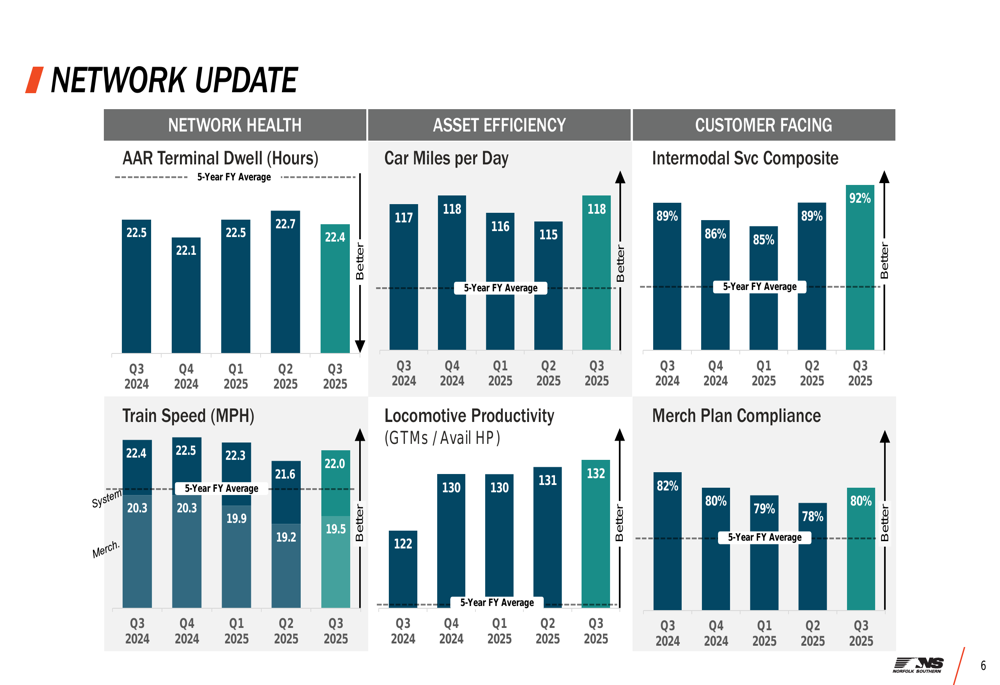

Network Performance and Service Metrics

The railroad’s operational metrics showed stability across multiple quarters, with modest improvements in key areas. Car miles per day increased slightly to 118 in Q3 2025 from 117 in Q3 2024, while the intermodal service composite improved to 92% from 89% in the same period last year.

The following network performance dashboard highlights these operational metrics:

Locomotive productivity continued its upward trend, reaching 132 GTMs per available horsepower in Q3 2025 compared to 122 in Q3 2024, reflecting the company’s ongoing focus on asset efficiency and operational excellence.

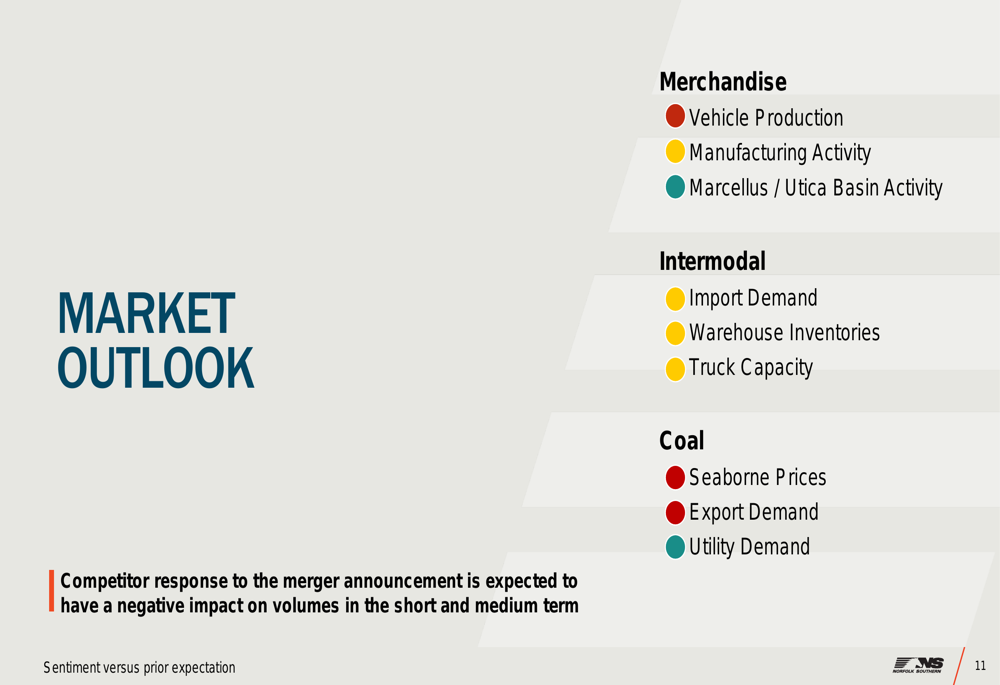

Market Outlook and Forward Guidance

Norfolk Southern provided a mixed outlook across its business segments. The merchandise segment shows positive indicators for manufacturing activity and Marcellus/Utica Basin activity, while intermodal faces a combination of positive import demand balanced against neutral warehouse inventories and truck capacity. The coal segment presents the most challenging outlook, with negative seaborne prices partially offset by positive utility demand.

This market sentiment is captured in the following outlook summary:

During the earnings call, CEO Mark George emphasized the company’s commitment to maintaining customer relationships despite competitive pressures, stating, "We are going to fight like hell over every available unit and dollar." The company acknowledged that competitor responses to merger announcements could negatively impact volumes in the short to medium term.

Looking ahead, Norfolk Southern anticipates Q4 costs to range between $2.0 and $2.1 billion, reflecting ongoing inflationary pressures. Despite these challenges, the company’s raised efficiency target of $600 million by 2026 signals confidence in its long-term strategic initiatives and ability to control costs in a challenging operating environment.

The presentation revealed a company successfully navigating a complex market landscape through operational excellence and cost discipline, though investors appear to remain cautious about future growth prospects amid broader economic uncertainties.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.