Gold prices steady, holding sharp gains in wake of soft U.S. jobs data

Introduction & Market Context

Northrop Grumman Corporation (NYSE:NOC) released its first quarter 2025 financial results on April 22, revealing significant pressure on profitability despite maintaining its full-year sales growth outlook. The defense contractor reported a 49% drop in operating income, primarily due to adjustments related to its B-21 bomber program. The stock fell sharply in pre-market trading, down 8.72% to $485, reflecting investor concerns about the reduced profit guidance.

Quarterly Performance Highlights

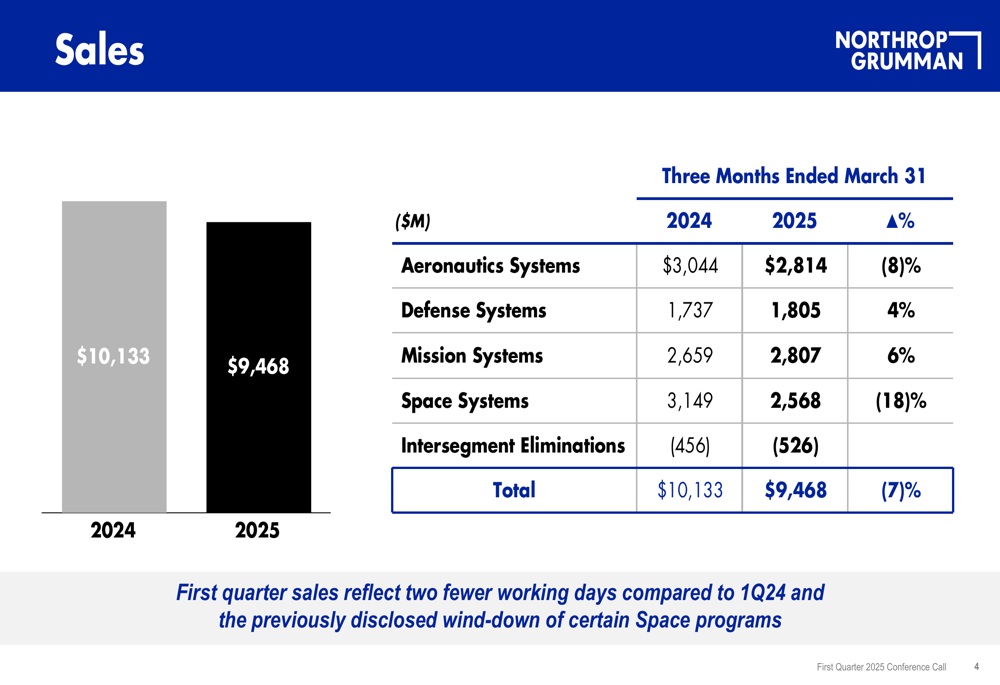

Northrop Grumman reported total sales of $9.47 billion for Q1 2025, representing a 7% decrease compared to $10.13 billion in the same period last year. The company noted that first quarter sales reflect two fewer working days compared to Q1 2024 and the previously disclosed wind-down of certain Space programs.

As shown in the following segment sales breakdown:

Segment performance was mixed, with Defense Systems sales increasing 4% to $1.81 billion and Mission Systems sales growing 6% to $2.81 billion. However, these gains were offset by declines in Aeronautics Systems (-8% to $2.81 billion) and Space Systems (-18% to $2.57 billion).

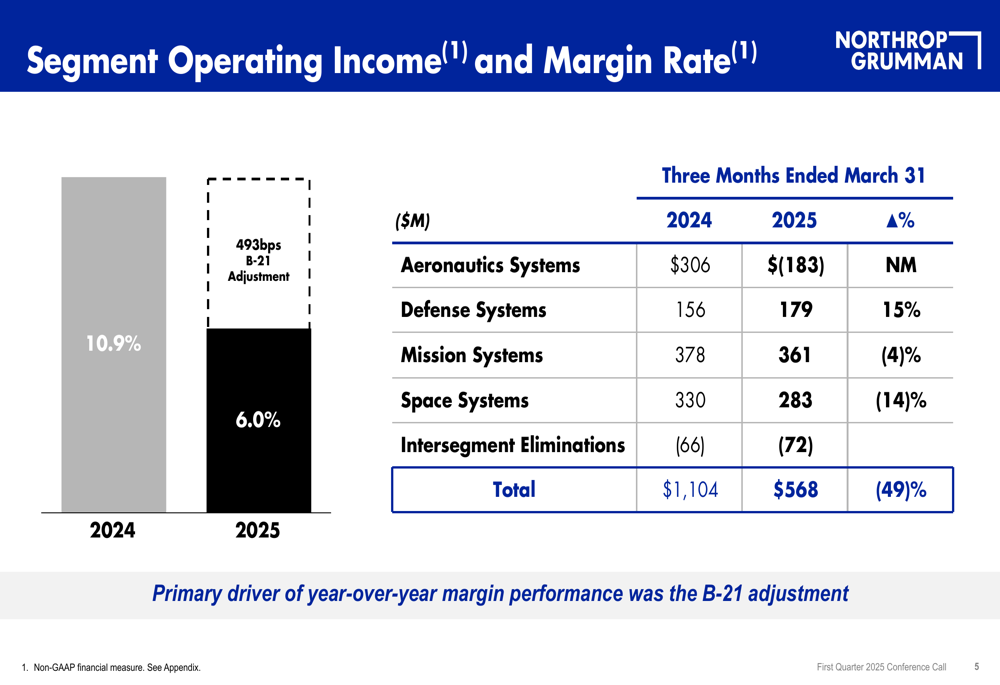

The most concerning aspect of the quarterly results was the dramatic decline in profitability. Total (EPA:TTEF) segment operating income fell 49% to $568 million, compared to $1.10 billion in Q1 2024. The operating margin rate decreased from 10.9% to 6.0%.

The segment operating income breakdown illustrates the severity of the decline:

Notably, Aeronautics Systems swung from a $306 million operating profit to a $183 million loss, which the company identified as the primary driver of the year-over-year margin performance deterioration due to the B-21 adjustment.

Detailed Financial Analysis

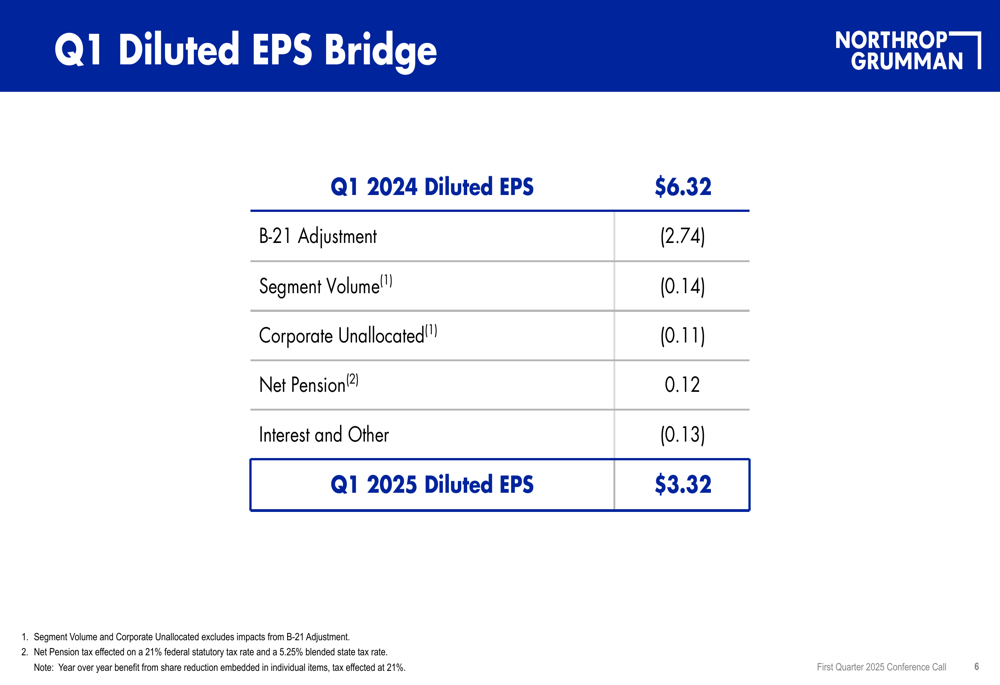

The company’s diluted earnings per share (EPS) fell to $3.32 in Q1 2025, down from $6.32 in the same period last year. The following bridge chart clearly illustrates the factors contributing to this decline:

The B-21 program adjustment had the most significant impact, reducing EPS by $2.74. Additional negative factors included segment volume (-$0.14), corporate unallocated expenses (-$0.11), and interest and other expenses (-$0.13). These were partially offset by a $0.12 positive contribution from net pension.

Forward-Looking Statements

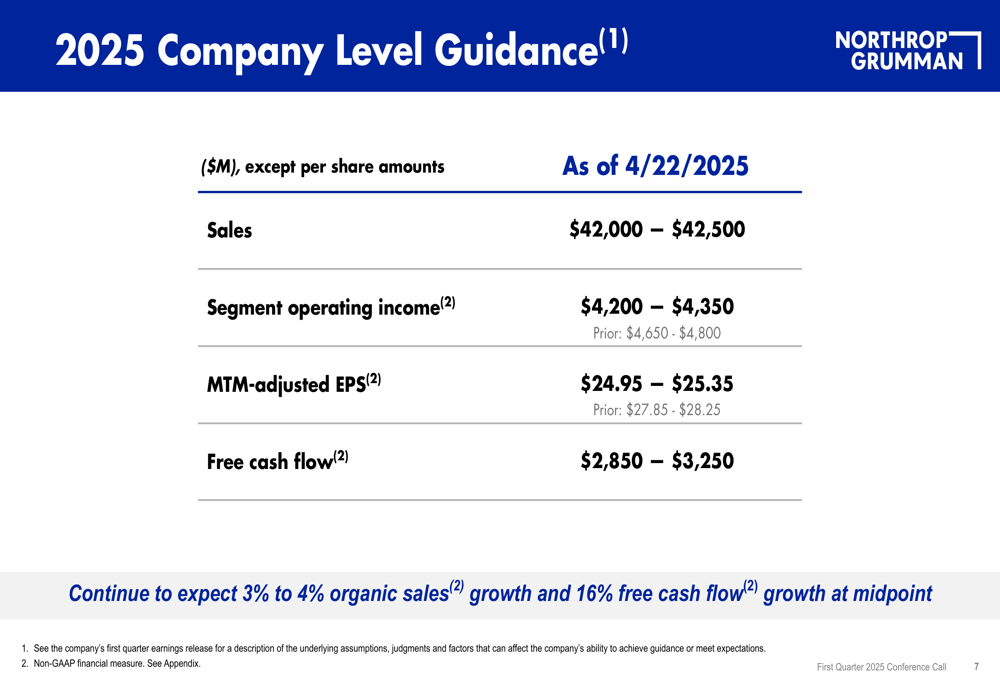

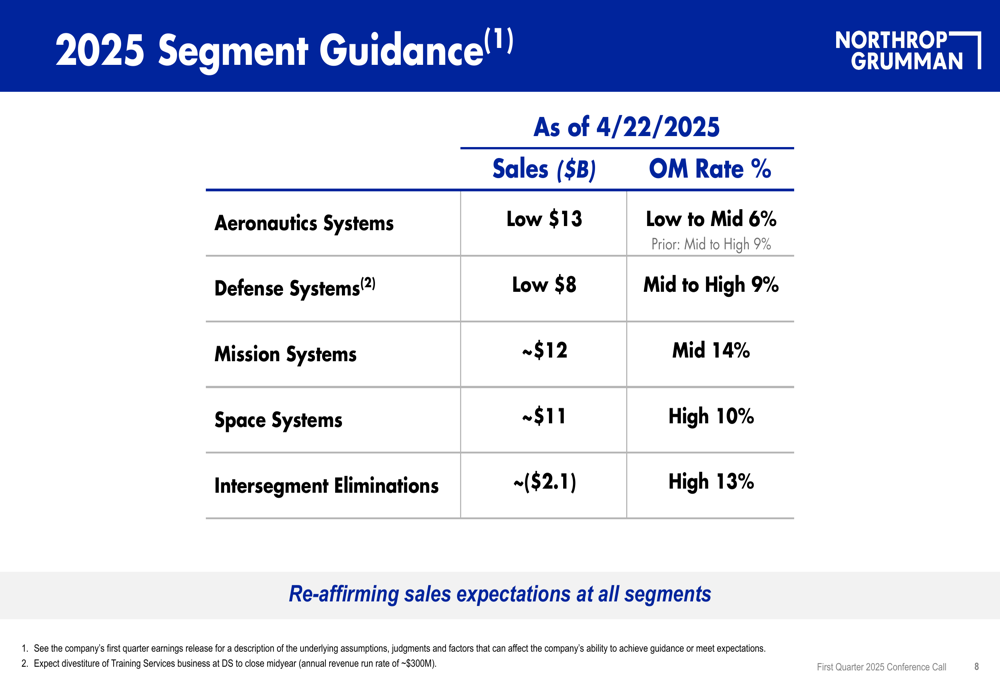

Despite the challenging quarter, Northrop Grumman maintained its 2025 organic sales growth outlook of 3% to 4%. However, the company significantly reduced its profit guidance, as shown in the following guidance summary:

Segment operating income is now projected at $4,200-$4,350 million, down from the previous guidance of $4,650-$4,800 million. Similarly, MTM-adjusted EPS guidance was cut to $24.95-$25.35 from the previous $27.85-$28.25. The company maintained its free cash flow growth target of 16% at the midpoint, with expected free cash flow of $2,850-$3,250 million.

The segment-level guidance provides additional context for the company’s outlook:

Most notably, Aeronautics Systems margin rate guidance was reduced to "Low to Mid 6%" from the previous "Mid to High 9%" range, reflecting the ongoing challenges with the B-21 program. The company is re-affirming sales expectations across all segments, suggesting that while profitability is under pressure, demand for its products and services remains strong.

Strategic Initiatives

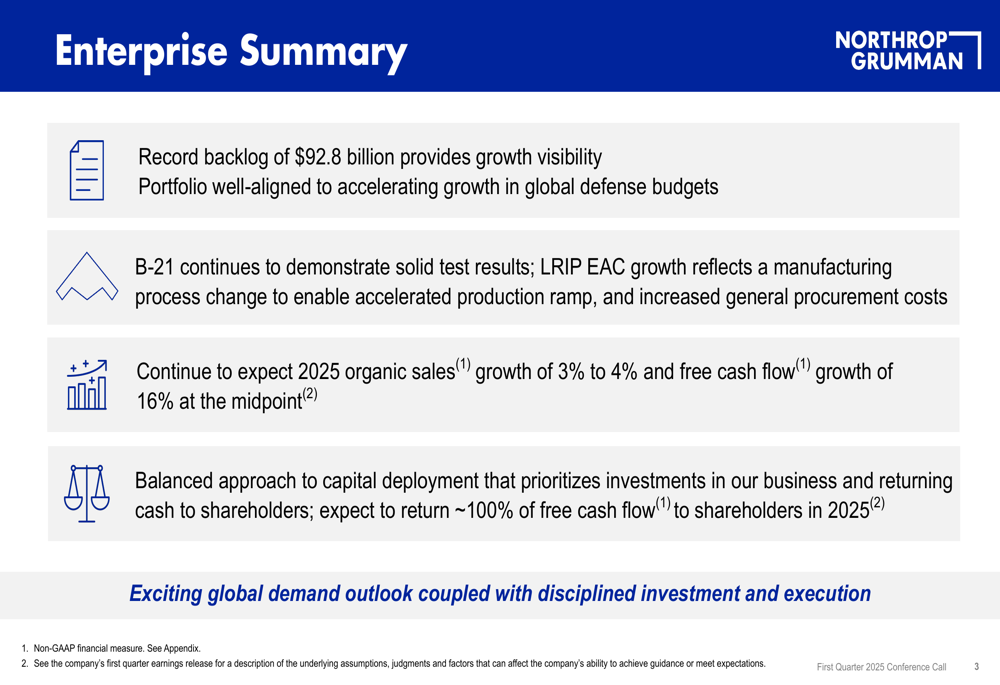

Northrop Grumman highlighted several strategic initiatives that provide a more positive long-term outlook despite the near-term challenges. The company emphasized its record backlog of $92.8 billion, which provides visibility for future growth. This strong order book is summarized in the enterprise overview:

The company also announced plans to divest its Training Services business, which has an annual revenue run rate of approximately $300 million. This divestiture, expected to close midyear, aligns with the company’s focus on its core defense technology capabilities.

International expansion represents another growth opportunity, with the company noting that rising global defense budgets continue to increase demand for its solutions. Northrop Grumman expects its international business to grow faster than U.S. sales in 2025, providing a potential offset to domestic challenges.

Competitive Industry Position

Despite the quarterly setback, Northrop Grumman emphasized its strong competitive positioning in the defense industry. The company highlighted its focus on technology innovation, particularly in microelectronics, and its advanced manufacturing capacity as key differentiators.

The company’s summary slide outlines its strategic positioning:

Northrop Grumman stated it is "well-positioned to advance Administration’s goal of peace through strength due to its technology innovation and advanced manufacturing capacity." The company also emphasized its "laser-focused on performance through discipline, technology enablement, and efficiencies."

Executive Summary

Northrop Grumman’s first quarter 2025 results present a mixed picture. The significant decline in operating income and EPS, primarily due to B-21 program adjustments, has understandably concerned investors, as reflected in the stock’s pre-market decline. The reduced profit guidance for the full year further suggests that these challenges will persist throughout 2025.

However, several positive factors provide a counterbalance to these concerns. The company’s record backlog, maintained sales growth outlook, and expected international expansion all point to continued demand for its products and services. The strategic divestiture of the Training Services business demonstrates management’s focus on core operations.

The key question for investors is whether the B-21 program issues represent a temporary setback or signal more fundamental challenges in program execution. Management’s characterization of the adjustment as reflecting "a manufacturing process change to enable accelerated production ramp" suggests the former, but the magnitude of the financial impact underscores the significance of the challenge.

As global defense spending continues to rise amid geopolitical tensions, Northrop Grumman’s long-term growth opportunities remain substantial. However, near-term execution, particularly in the Aeronautics segment, will be critical to restoring investor confidence and returning to the profitability levels seen in previous quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.