BofA update shows where active managers are putting money

Norwegian Cruise Line Holdings Ltd (NYSE:NCLH) reported strong second-quarter 2025 results that exceeded guidance across multiple key metrics, according to the company’s earnings presentation released on July 31, 2025. The cruise operator’s shares rose 5.77% in premarket trading to $24.75, rebounding from challenges faced in the previous quarter.

Executive Summary

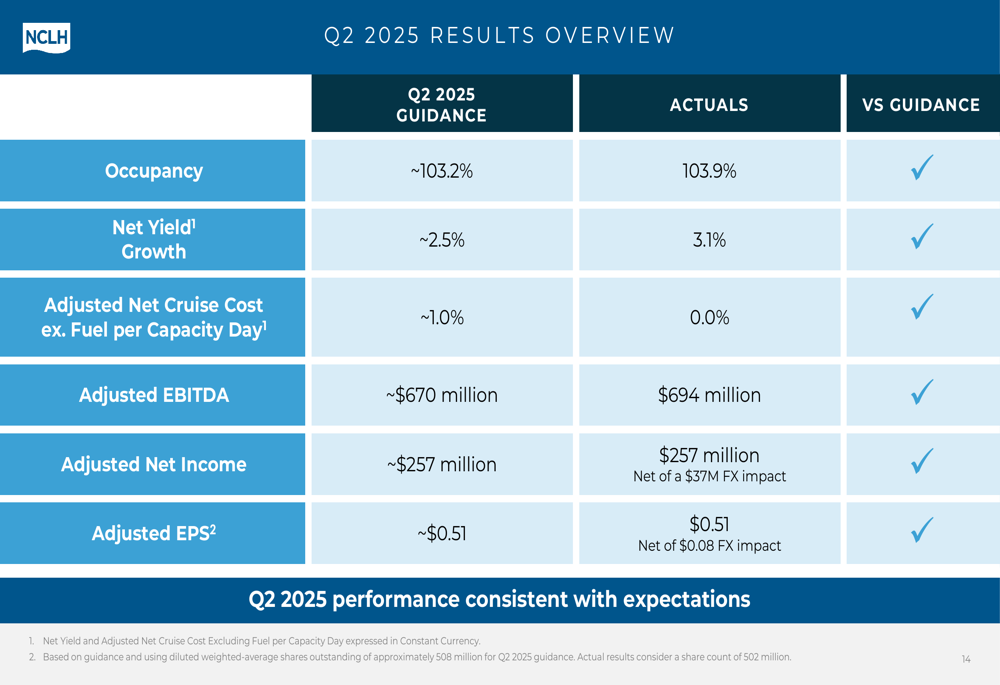

Norwegian Cruise Line Holdings delivered Q2 2025 performance that surpassed expectations, with net yield growth of 3.1% compared to 2024, exceeding guidance by 60 basis points. The company achieved an adjusted EBITDA of $694 million, above its guidance of approximately $670 million, while maintaining its adjusted EPS target of $0.51 despite an $0.08 foreign exchange headwind.

As shown in the following results overview, the company met or exceeded all key performance metrics for the quarter:

"We delivered strong Q2 performance ahead of expectations," the company stated in its presentation, highlighting operational improvements that drove margin expansion and continued deleveraging progress.

Quarterly Performance Highlights

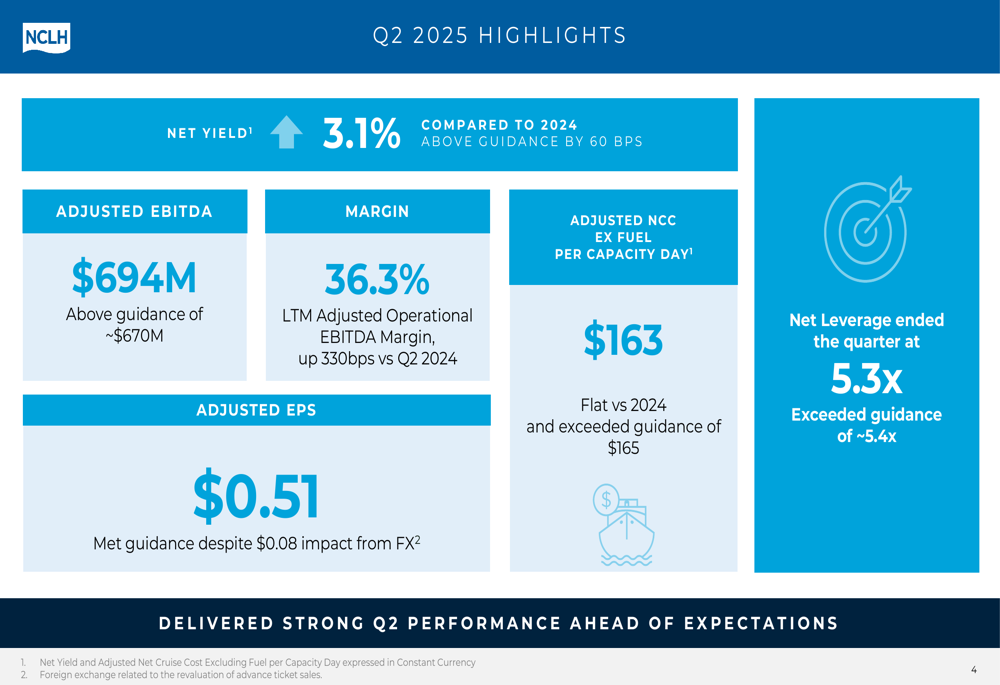

Norwegian Cruise Line Holdings reported significant improvements in profitability metrics during Q2 2025. The company’s last twelve months (LTM) adjusted operational EBITDA margin reached 36.3%, representing a 330 basis point increase compared to Q2 2024. Adjusted net cruise cost excluding fuel per capacity day remained flat year-over-year at $163, outperforming guidance of $165.

The following slide illustrates key Q2 highlights:

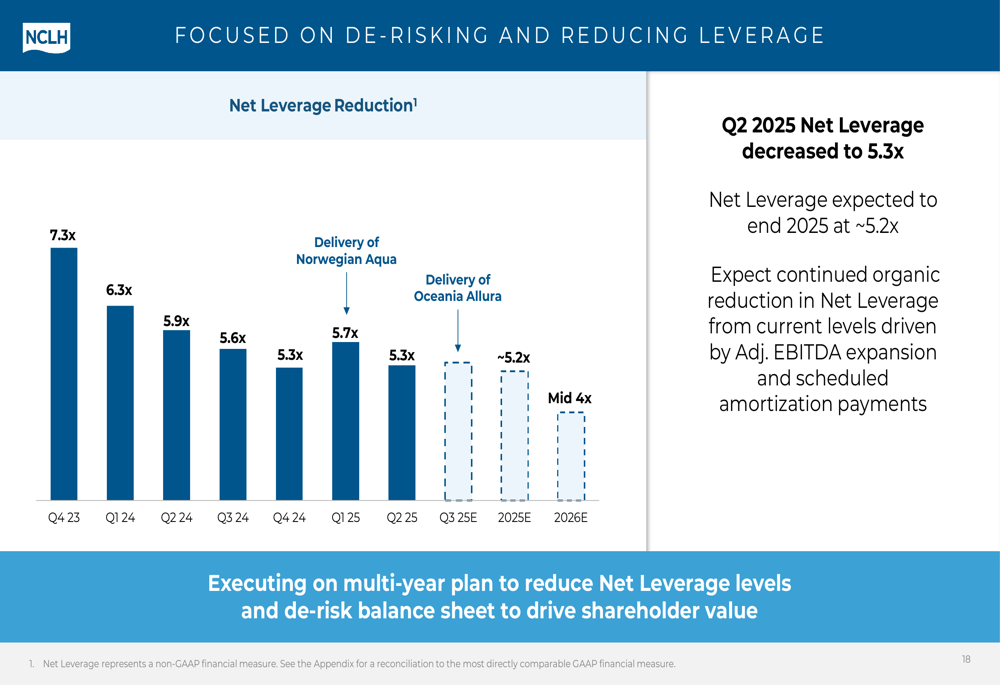

The company’s net leverage ratio ended the quarter at 5.3x, better than the guided 5.4x, demonstrating continued progress in strengthening the balance sheet. This represents substantial improvement from the 7.3x leverage ratio reported in Q4 2023, reflecting the company’s commitment to deleveraging.

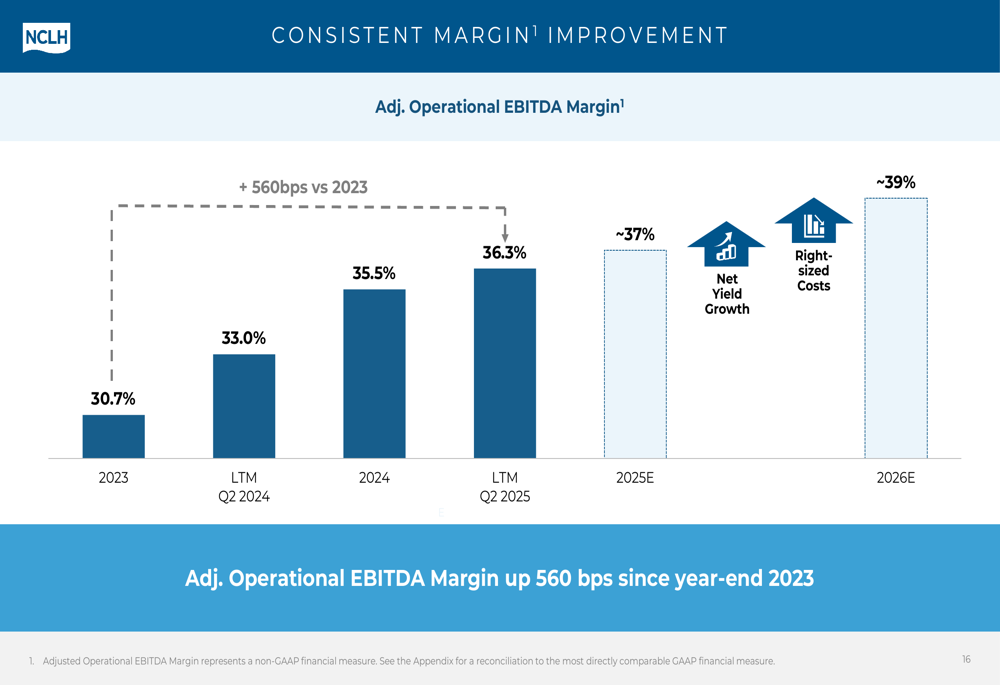

The margin improvement trajectory has been consistent, as illustrated in this chart:

This performance marks a significant turnaround from Q1 2025, when Norwegian reported an earnings miss that led to an 8.57% stock decline. The Q1 adjusted EPS of $0.07 fell short of the expected $0.09, while revenue reached $2.13 billion against forecasts of $2.15 billion. The company attributed those misses primarily to foreign exchange headwinds.

Strategic Initiatives

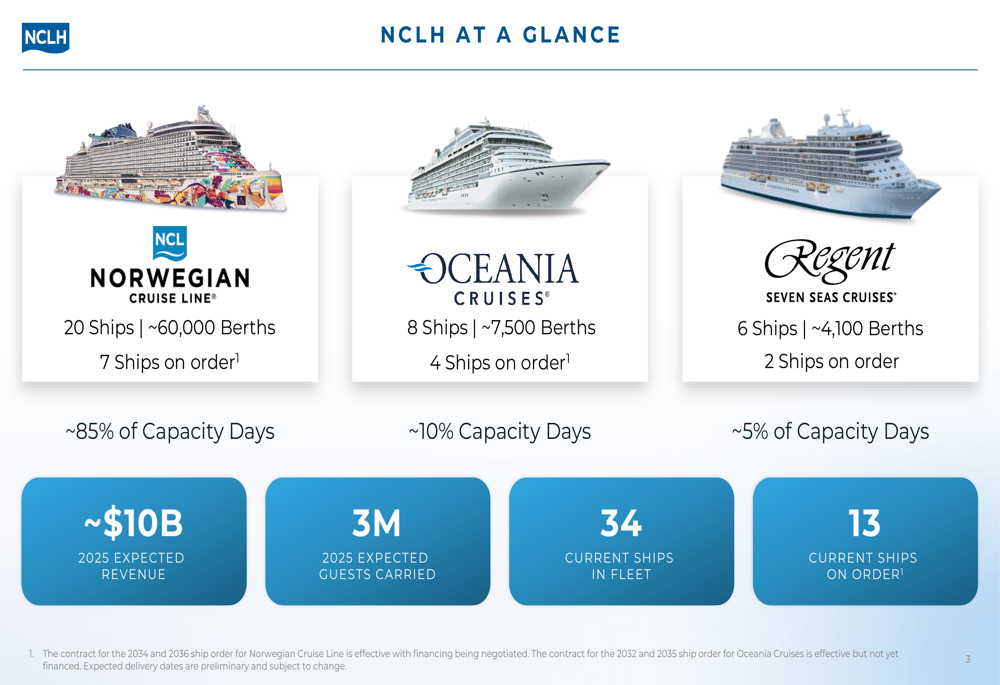

Norwegian Cruise Line Holdings continues to execute on several strategic initiatives aimed at driving long-term growth. The company’s fleet currently consists of 34 ships with 13 vessels on order through 2036, representing a measured capacity growth with a net CAGR of 4%.

The company provided this overview of its operations and brand positioning:

A key component of Norwegian’s strategy involves enhancing its private island destination, Great Stirrup Cay. The company is investing in expanded amenities including a two-ship pier, heated pool, splash pad, and welcome center by year-end 2025, with additional attractions like a waterpark with 19 slides planned for summer 2026.

Norwegian is also focusing on revenue enhancement through several initiatives, including newbuild design with richer cabin mix, optimized deployment with more "fun & sun" itineraries and shorter cruise lengths, enhanced revenue management systems, and digital transformation. The company recently appointed a new Chief Digital & Technology Officer and Chief Marketing Officer at Norwegian Cruise Line to drive these efforts.

The following slide outlines the company’s strategic framework and 2026 financial targets:

Financial Outlook

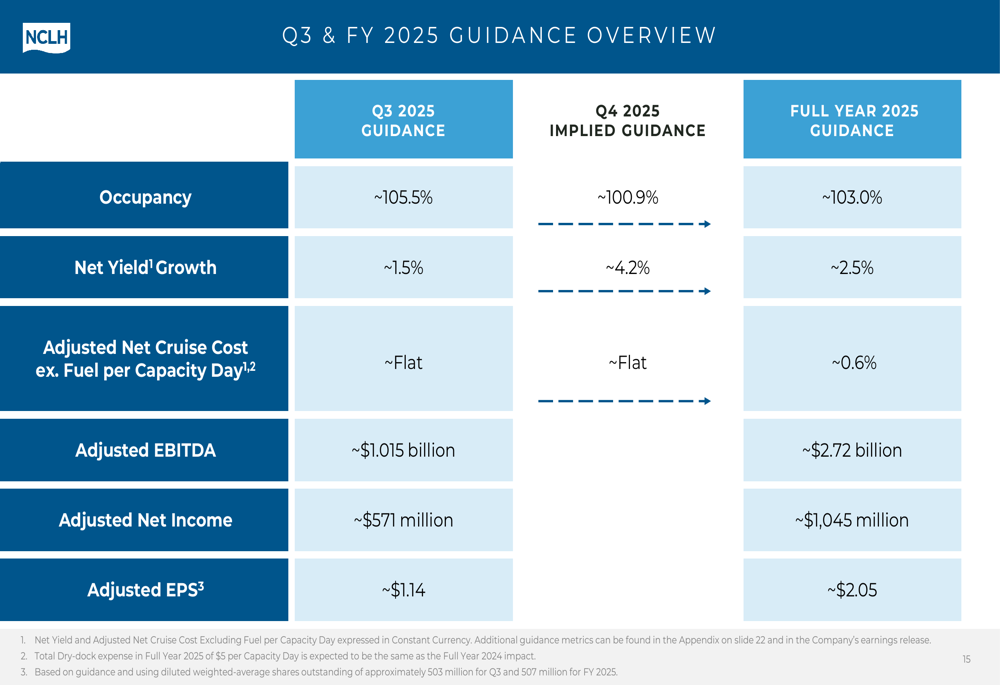

Norwegian Cruise Line Holdings maintained its full-year 2025 guidance and provided outlook for the third quarter. For Q3 2025, the company expects occupancy of approximately 105.5%, net yield growth of around 1.5%, and adjusted EBITDA of approximately $1.015 billion.

The detailed guidance is presented below:

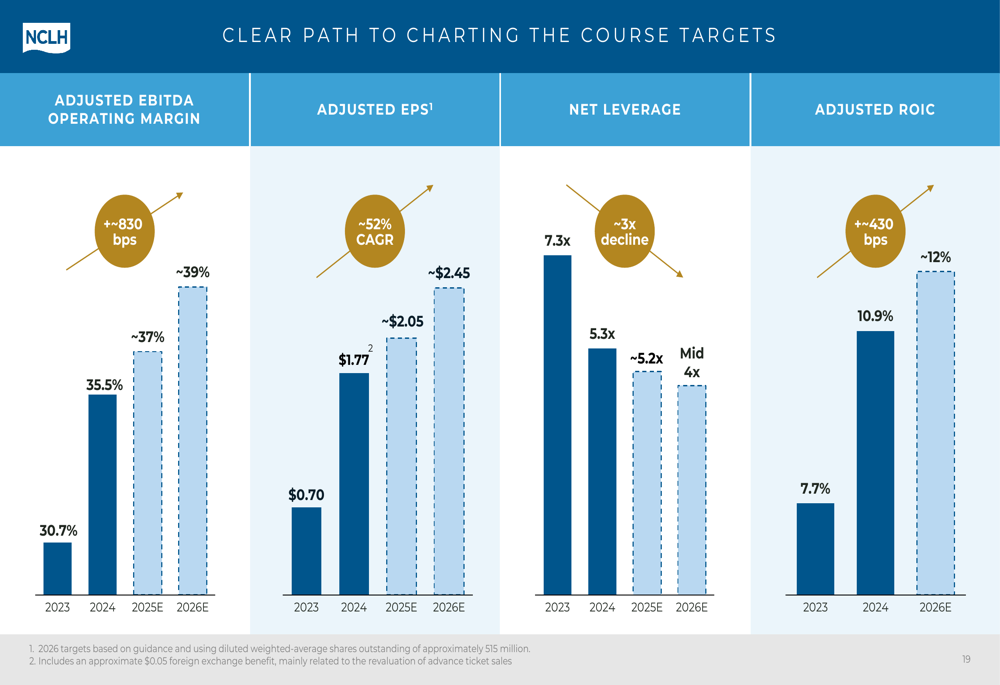

For the full year 2025, Norwegian anticipates net yield growth of approximately 2.5%, adjusted EBITDA of around $2.72 billion, and adjusted EPS of approximately $2.05. The company remains on track to achieve its 2026 targets, including an adjusted operational EBITDA margin of approximately 39%, adjusted EPS of around $2.45 (representing over 30% CAGR from 2024), and net leverage in the mid-4x range.

The company’s clear path toward these targets is illustrated in the following chart:

Detailed Financial Analysis

Norwegian Cruise Line Holdings continues to make progress on its deleveraging strategy, with net leverage decreasing from 7.3x in Q4 2023 to 5.3x in Q2 2025. The company expects to end 2025 with net leverage of approximately 5.2x before reaching its mid-4x target in 2026.

This deleveraging trajectory is shown in the following chart:

The company’s cash generation engine is fueled by robust advance ticket sales, which reached $4.0 billion in Q2 2025, up approximately 1% compared to Q2 2024 and 76% higher than 2019 levels. This growth is driven by strong pricing, optimized deployment mix, enhanced pre-sold onboard revenue, and capacity expansion.

Norwegian is also focused on delivering sub-inflationary cost growth, with adjusted net cruise cost excluding fuel per capacity day expected to increase by just 0.6% in 2025. The company anticipates delivering more than $200 million in cumulative total savings by the end of 2025 and has expressed confidence in achieving its $300+ million target through 2026.

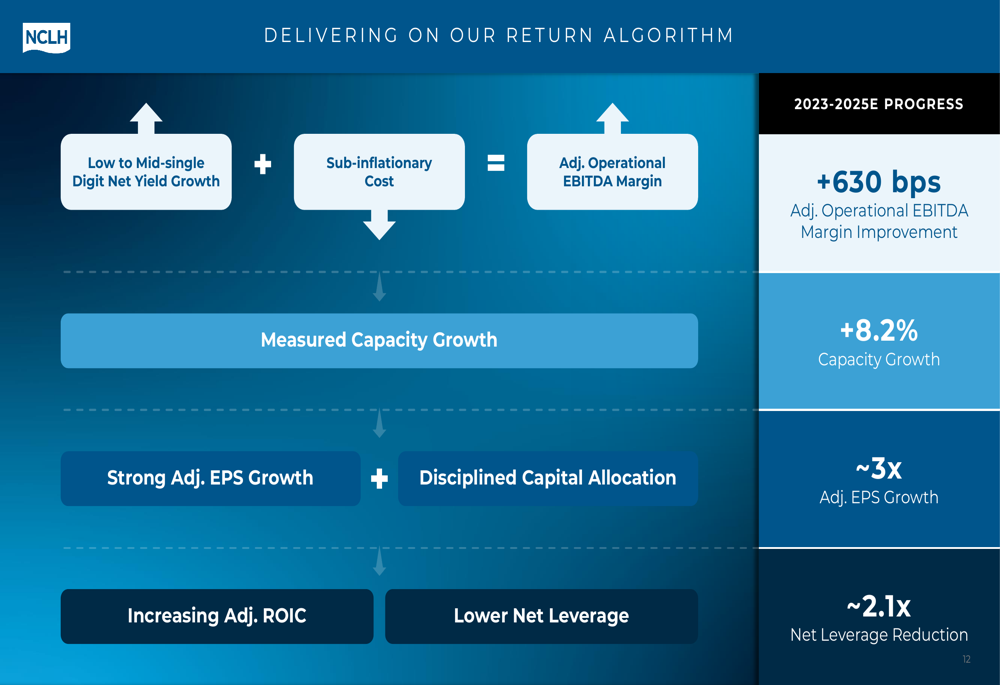

The company’s return algorithm combines low to mid-single digit net yield growth with sub-inflationary cost growth to drive margin expansion, as illustrated in this flowchart:

With its strong Q2 performance, Norwegian Cruise Line Holdings appears to be successfully navigating the challenges it faced earlier in the year while making steady progress toward its long-term financial targets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.