HK-listed gold stocks jump as US economic fears boost bullion prices

Introduction & Market Context

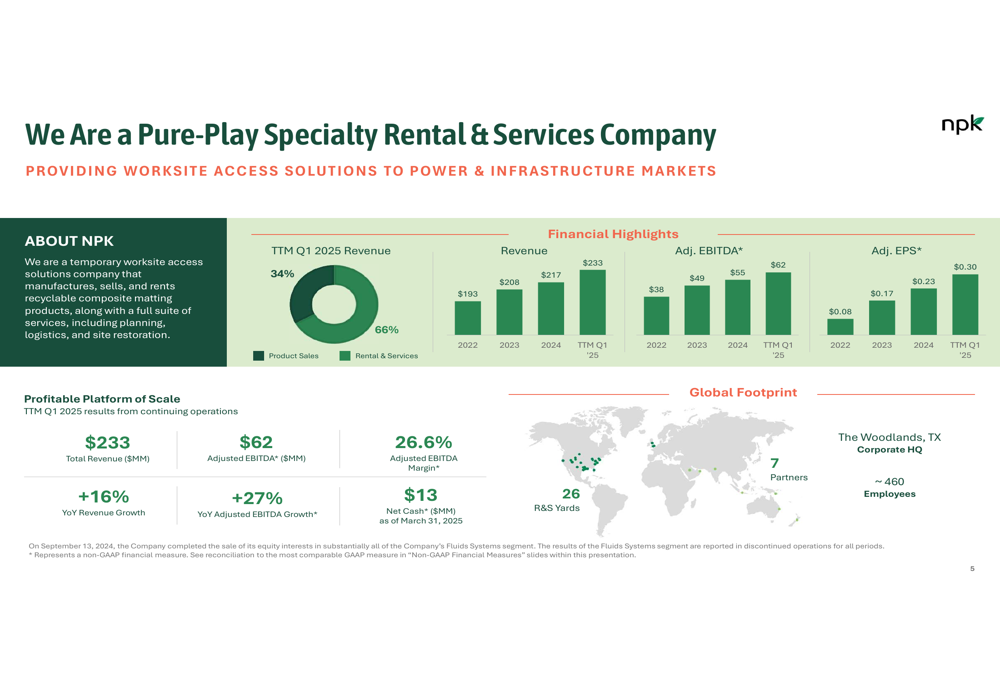

NPK International Inc. delivered a strong first quarter of 2025, showcasing accelerated revenue growth and expanded margins in its May 2025 investor presentation. As a pure-play specialty rental and services company, NPK provides worksite access solutions primarily to power and infrastructure markets, capitalizing on significant infrastructure investment trends.

The company has established itself as a leader in the composite matting industry with its flagship DURA-BASE® product, introduced in 1998 as the market’s first engineered thermoplastic worksite access matting. This innovative solution continues to drive NPK’s competitive advantage in temporary worksite access solutions.

As shown in the following overview of NPK’s business model and financial highlights:

NPK’s vertically integrated business model spans engineering and design, precision manufacturing, logistics planning, and specialty rental services. This comprehensive approach allows the company to serve diverse end markets including power transmission, oil and gas, infrastructure construction, rail, and pipeline sectors.

The following slide illustrates how this integrated model supports specialty end-markets:

Quarterly Performance Highlights

NPK reported impressive financial results for Q1 2025, with revenues from specialty rental and related services increasing to $43 million and adjusted EBITDA margin improving to 30.4%. The company’s TTM Q1 2025 performance showed total revenue of $233 million, representing 16% year-over-year growth, while adjusted EBITDA reached $62 million, up 27% year-over-year.

According to the earnings report, NPK’s Q1 2025 revenue surged by 32% to 65 million CAD, while adjusted EBITDA saw a 59% increase to 19.7 million CAD. The company also reported an improved gross margin and a rise in adjusted earnings per share from continuing operations to $0.12.

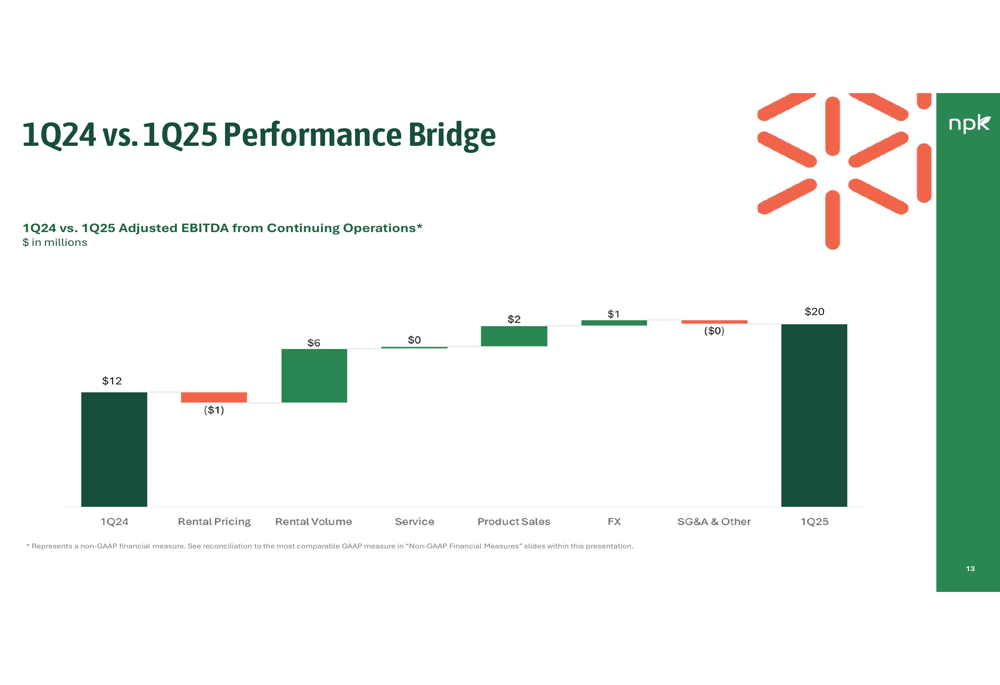

The following bridge analysis highlights the key drivers of NPK’s performance improvement from Q1 2024 to Q1 2025:

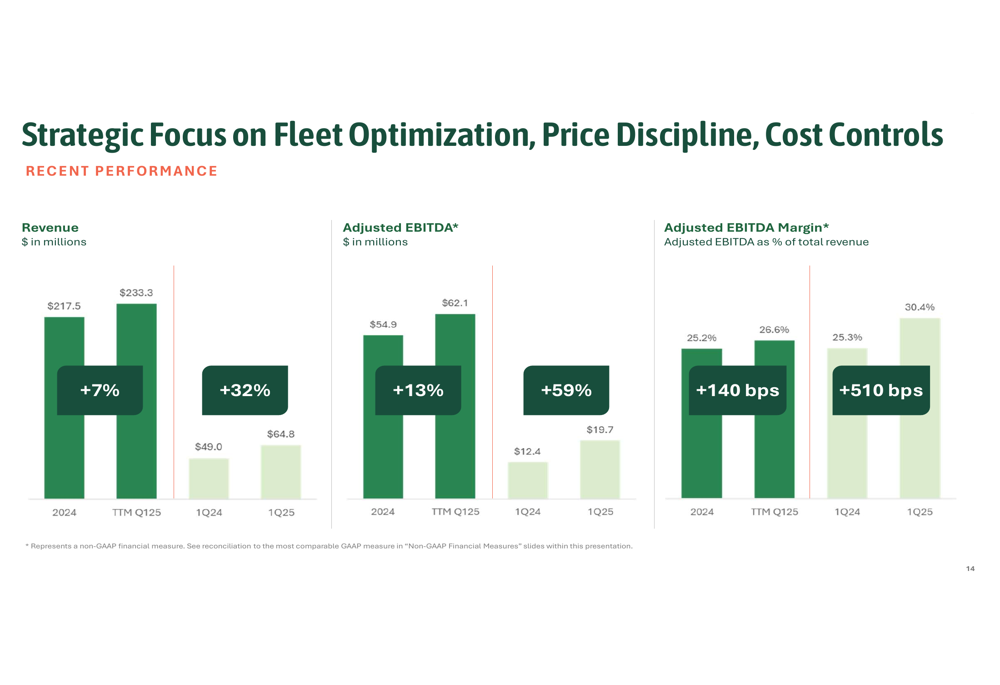

The company’s strategic focus on fleet optimization, price discipline, and cost controls has yielded significant improvements in key performance indicators. Revenue increased from $217.5 million in 2024 to $233.3 million in TTM Q1 2025 (up 7%), while adjusted EBITDA grew from $54.9 million to $62.1 million (up 13%). Most notably, adjusted EBITDA margin expanded by 510 basis points to 30.4%.

The following slide illustrates these performance improvements:

Strategic Focus and Growth Opportunities

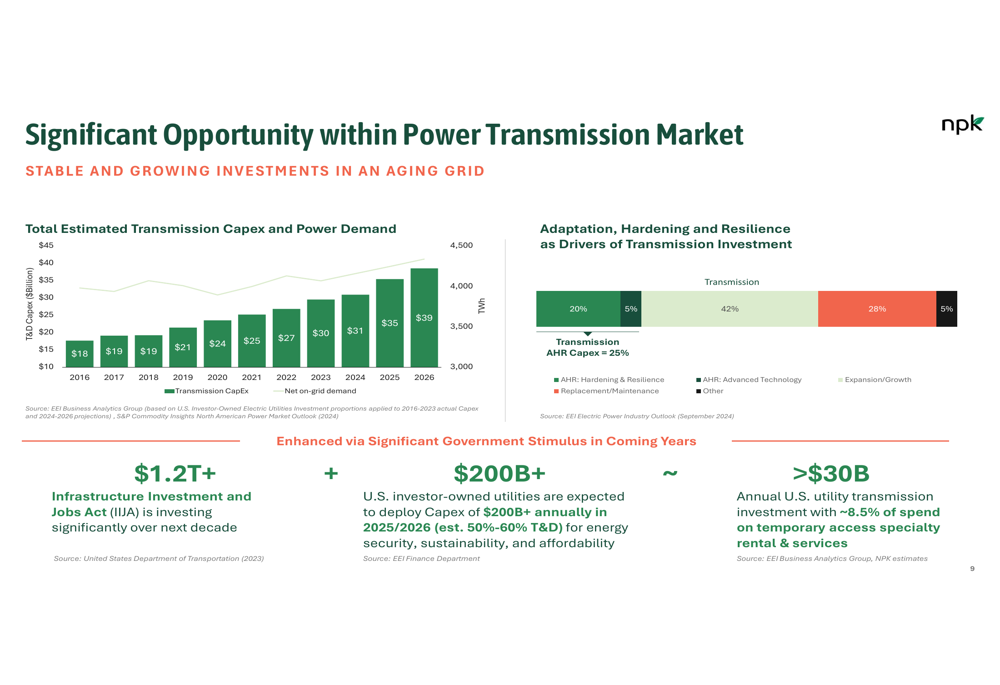

NPK is capitalizing on significant opportunities in the power transmission market, which is experiencing stable and growing investments in aging grid infrastructure. The $1.2+ trillion Infrastructure Investment and Jobs Act (IIJA) is driving substantial investments over the next decade, while U.S. investor-owned utilities are expected to deploy capital expenditures of $200+ billion annually in 2025/2026.

As shown in the following chart detailing the power transmission market opportunity:

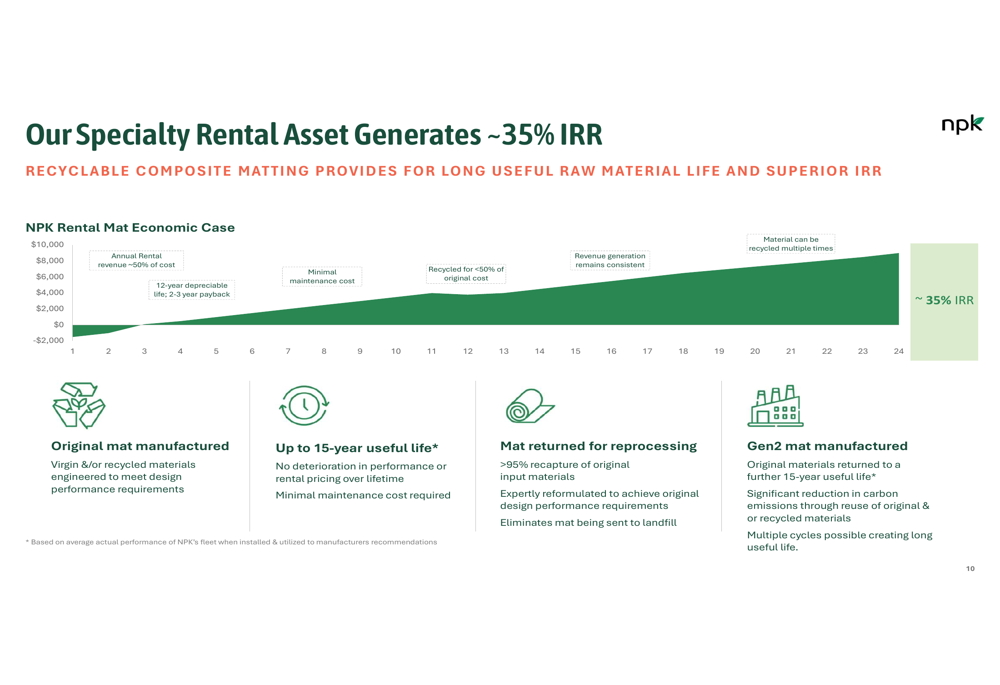

The company’s rental assets generate approximately 35% IRR, supported by recyclable composite matting that provides long useful raw material life. NPK’s mats have up to a 15-year useful life with minimal maintenance costs and can be reprocessed with over 95% recapture of original input materials.

The following slide demonstrates the economic case for NPK’s rental mat business:

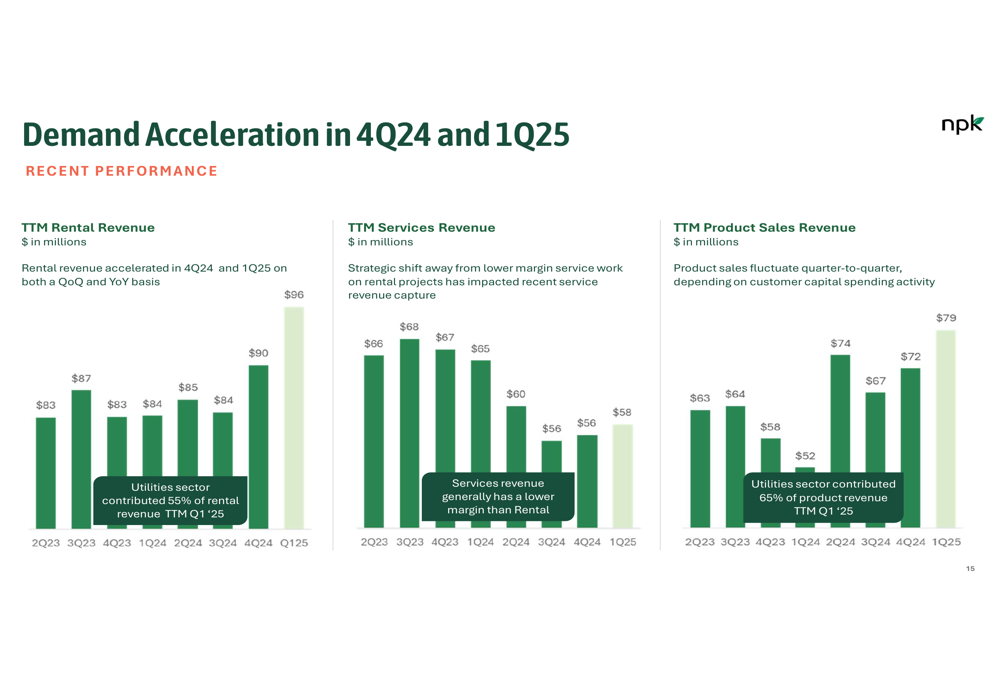

Recent quarters have shown acceleration in demand, particularly in rental revenue, which has grown from $90 million in Q4 2024 to $96 million in Q1 2025. Product sales revenue has also shown strong growth, increasing from $67 million in Q4 2024 to $79 million in Q1 2025.

The following chart illustrates this demand acceleration:

Financial Outlook and Guidance

Based on strong Q1 performance and positive market trends, NPK has increased its full-year 2025 guidance. The company now expects consolidated revenues in the range of $240-$252 million, representing 13% growth compared to 2024. Consolidated adjusted EBITDA is projected to be between $64-$72 million, indicating 24% growth.

Matthew Lanigan, CEO of NPK International, emphasized the company’s strong market position and growth potential in the earnings call: "We are the lightest composite fleet operator in the country," highlighting the company’s competitive edge. He also noted, "We’re pretty early innings on a revised kind of outlook for the industry," suggesting optimism about future industry trends.

NPK ended Q1 2025 with a strong balance sheet, including total cash of $21 million, total debt of $8 million, and available liquidity under its ABL credit facility of $66 million. The company also holds significant U.S. federal NOL and other tax credit carryforwards, as well as an administrative headquarters building in Katy, TX with an approximate net book value of $23 million.

Capital Allocation Strategy

NPK maintains a disciplined capital allocation strategy focused on maintaining modest leverage, organic investment to expand the rental fleet, evaluating accretive inorganic growth opportunities, and returning capital to shareholders through programmatic share repurchases.

The company resumed its programmatic return of capital in Q1 2025, using $11 million to repurchase 2% of outstanding shares. The remaining share repurchase authorization was increased to $100 million on April 30, 2025, demonstrating management’s confidence in the company’s future prospects.

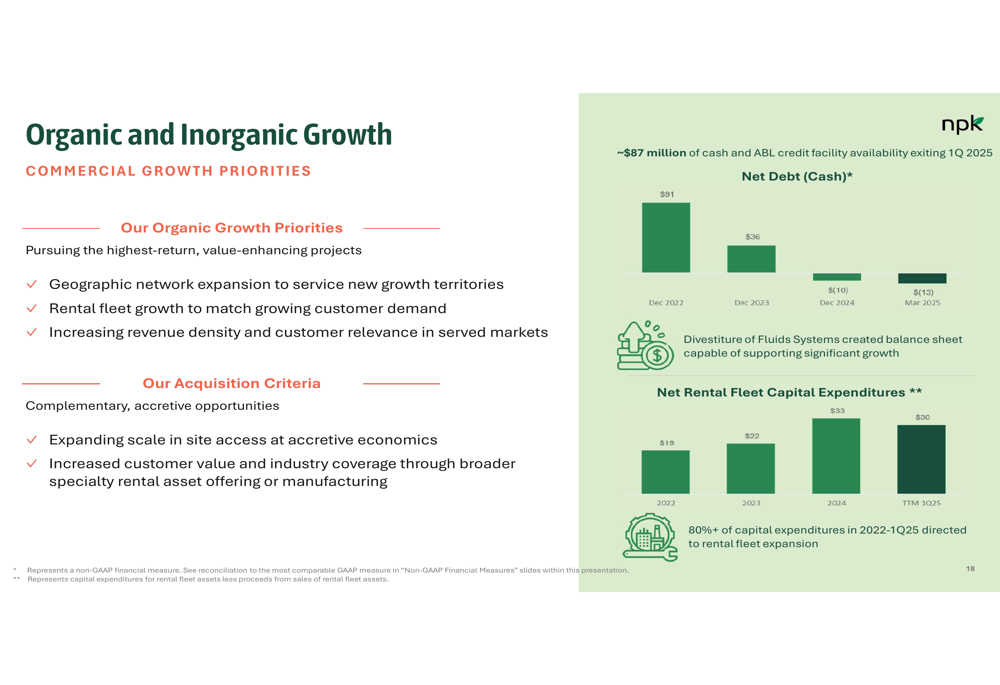

NPK’s organic growth priorities include geographic network expansion, rental fleet growth, and increasing revenue density. For potential acquisitions, the company is targeting complementary, accretive opportunities that expand scale and increase customer value.

The following slide outlines the company’s approach to organic and inorganic growth:

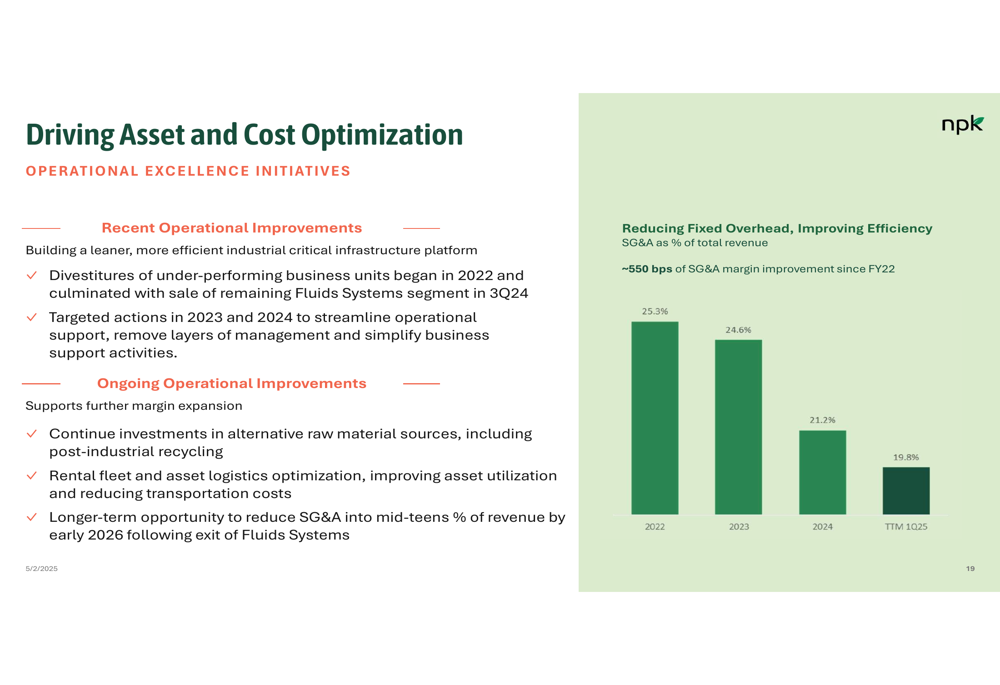

NPK has also made significant progress in driving asset and cost optimization. SG&A as a percentage of total revenue has decreased from 25.3% in 2022 to 19.8% in TTM Q1 2025, representing approximately 550 basis points of improvement. The company continues to execute actions intended to streamline the organization and its cost structure.

The following slide highlights these operational improvements:

With its strong Q1 2025 performance, increased full-year guidance, and disciplined capital allocation strategy, NPK International is well-positioned to capitalize on growing infrastructure investments while delivering value to shareholders through both organic growth and strategic capital returns.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.