Moody’s downgrades Senegal to Caa1 amid rising debt concerns

Introduction & Market Context

The ODP Corporation (NASDAQ:ODP) presented its second quarter 2025 financial results on August 6, 2025, highlighting improved year-over-year trends across business segments despite ongoing revenue challenges. The office supplies and business services provider reported that while overall sales declined compared to the same period last year, the company has made meaningful progress on its strategic initiatives and significantly improved its cash flow generation.

ODP shares have faced significant pressure over the past year, with the stock declining 73.74% over the 12 months preceding the Q1 earnings report. Recent trading shows the stock at $17.55, down 3.04% in the most recent session, though still above its 52-week low of $11.85.

Quarterly Performance Highlights

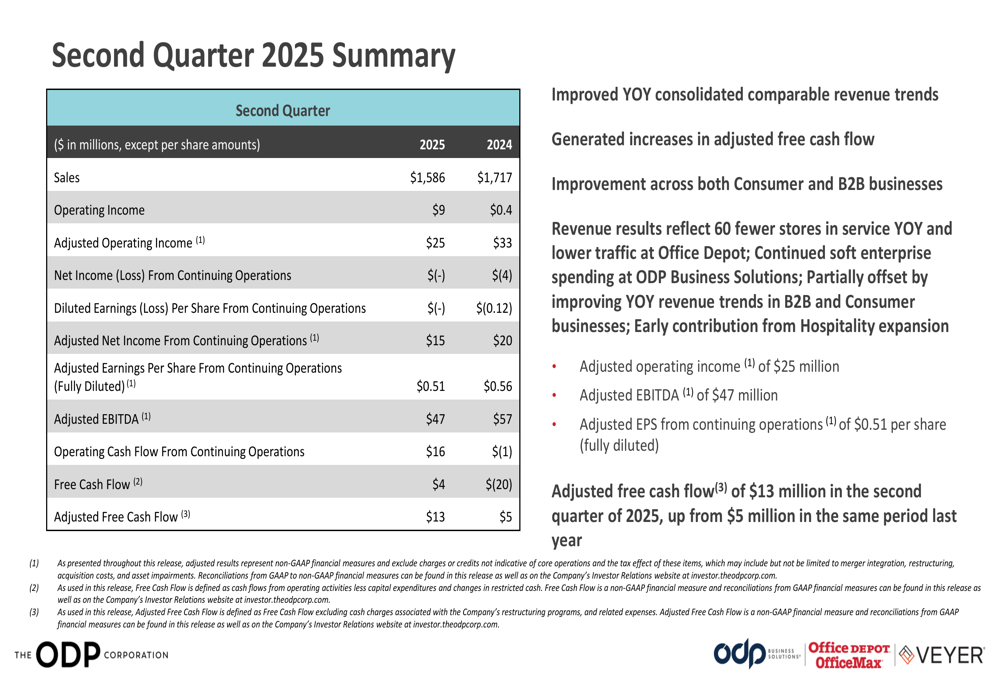

ODP reported second quarter 2025 sales of $1,586 million, down from $1,717 million in the same period of 2024. Despite the revenue decline, the company showed notable improvements in profitability metrics, with operating income rising to $9 million compared to just $0.4 million in the prior year period.

As shown in the comprehensive financial summary below, adjusted metrics showed mixed results with year-over-year declines in some areas but significant improvements in cash flow:

Particularly noteworthy was the company’s adjusted free cash flow, which more than doubled year-over-year to $13 million from $5 million in Q2 2024. This improvement came despite ongoing macroeconomic challenges and soft enterprise demand that continued to impact the business.

Segment Performance Analysis

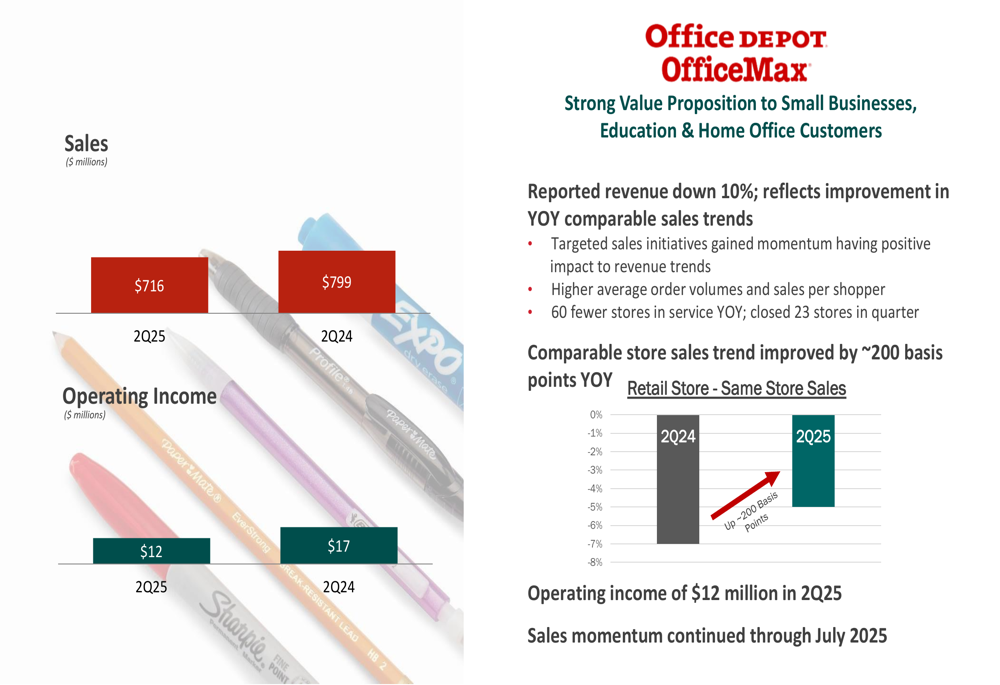

ODP’s retail division, comprising Office Depot and OfficeMax stores, reported a 10% revenue decline, reflecting both the closure of 60 stores year-over-year (including 23 in Q2 alone) and broader market challenges. However, the company highlighted that comparable store sales trends improved by approximately 200 basis points year-over-year, indicating better performance in the remaining store base.

The retail segment performance details show improving trends despite the overall revenue decline:

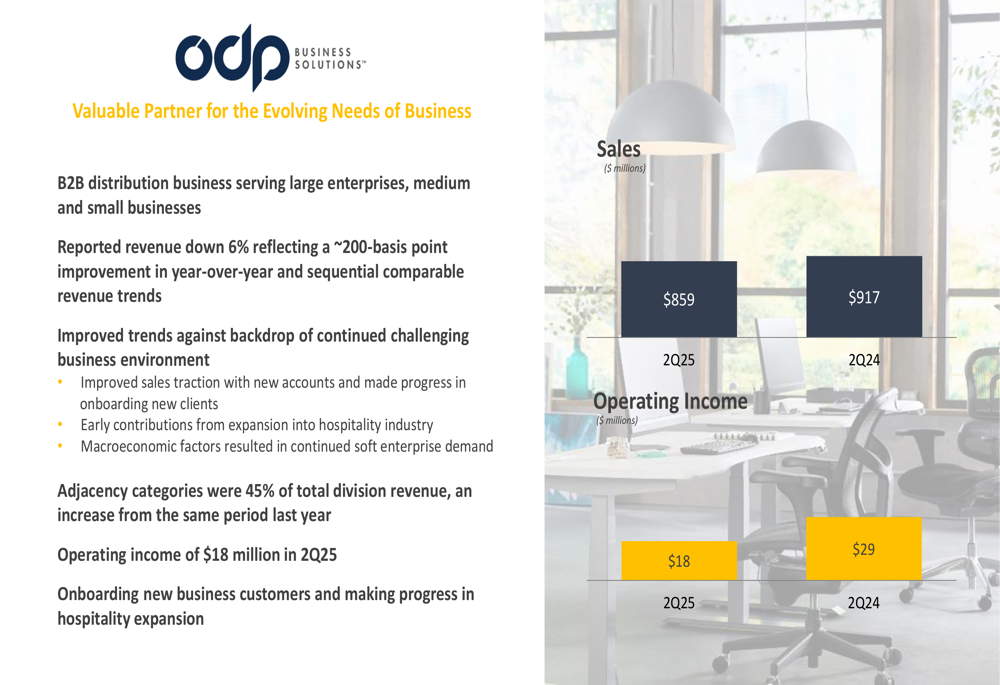

The ODP Business Solutions division, which serves large enterprises and small to medium-sized businesses, reported a 6% revenue decline to $859 million. However, this represented a 200 basis point improvement in year-over-year trends. The division generated $18 million in operating income, down from $29 million in the prior year period.

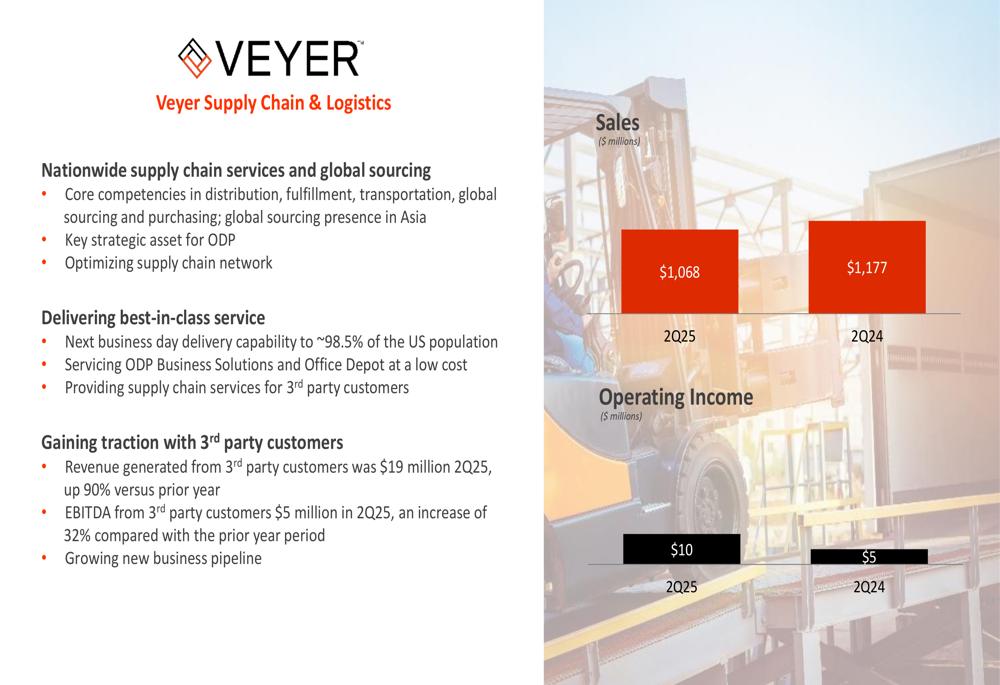

Veyer, the company’s supply chain and logistics segment, showed promising growth in its third-party business, with revenue from external customers increasing 90% year-over-year to $19 million. EBITDA from third-party customers grew 32% to $5 million, demonstrating the potential of this business unit as a standalone growth driver.

Strategic Initiatives & Expansion

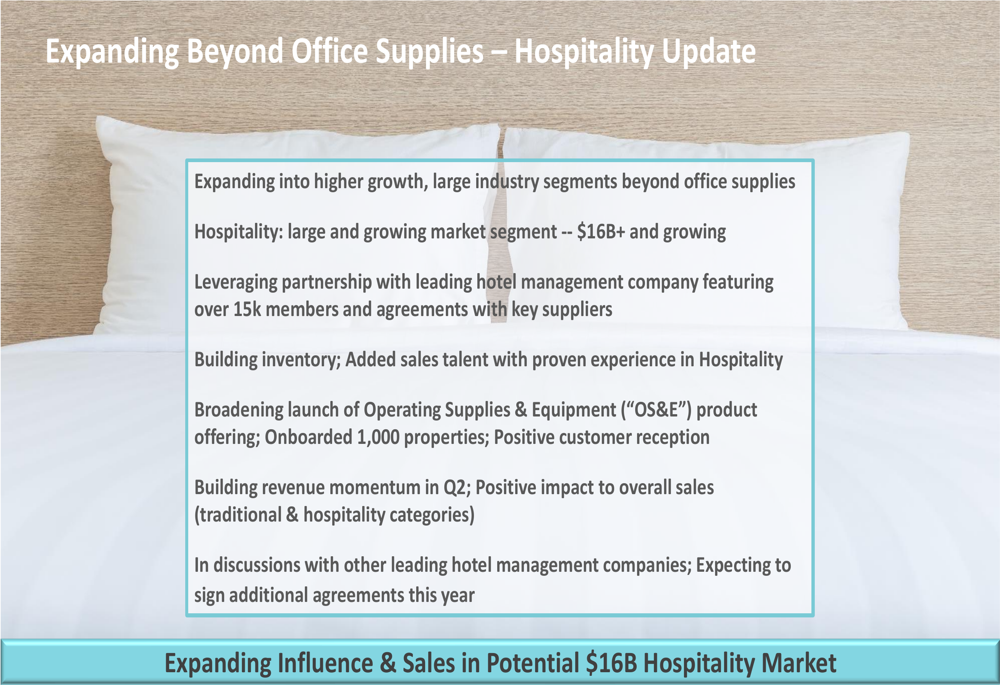

A key focus of ODP’s presentation was its strategic expansion into the hospitality sector, which represents a potential $16+ billion market opportunity. The company reported progress in building inventory, adding sales talent, and onboarding approximately 1,000 properties in the Operating Supplies & Equipment (OS&E) segment.

The hospitality expansion strategy was highlighted as follows:

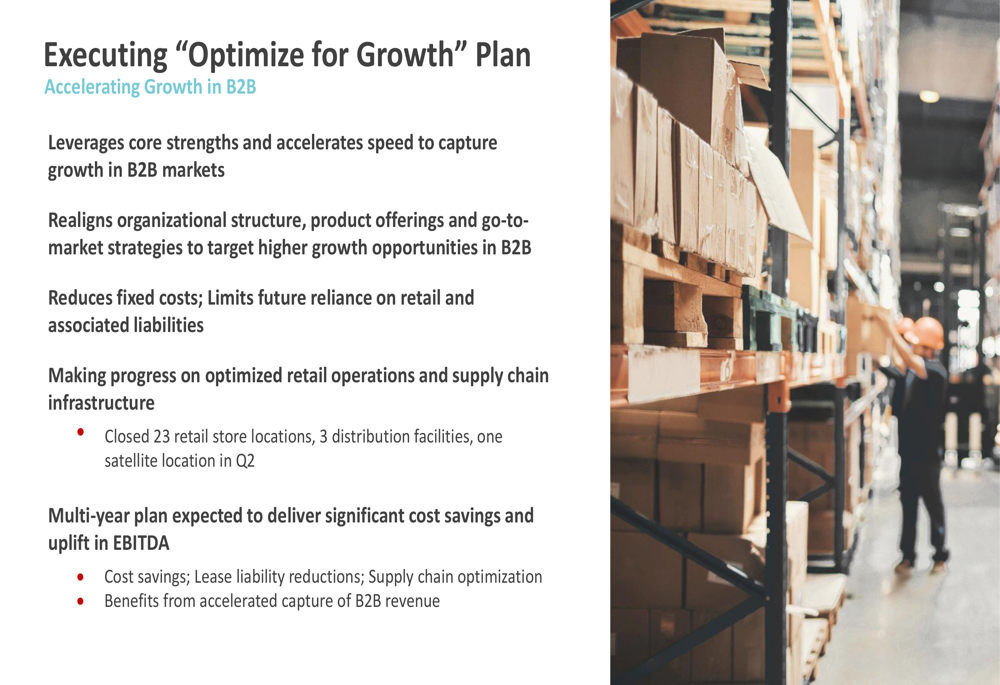

Simultaneously, ODP is executing its "Optimize for Growth" plan, which involves realigning the organizational structure, reducing fixed costs, and limiting reliance on retail operations. In Q2, the company closed 23 retail locations, 3 distribution facilities, and one satellite location as part of this multi-year plan.

Balance Sheet & Cash Flow

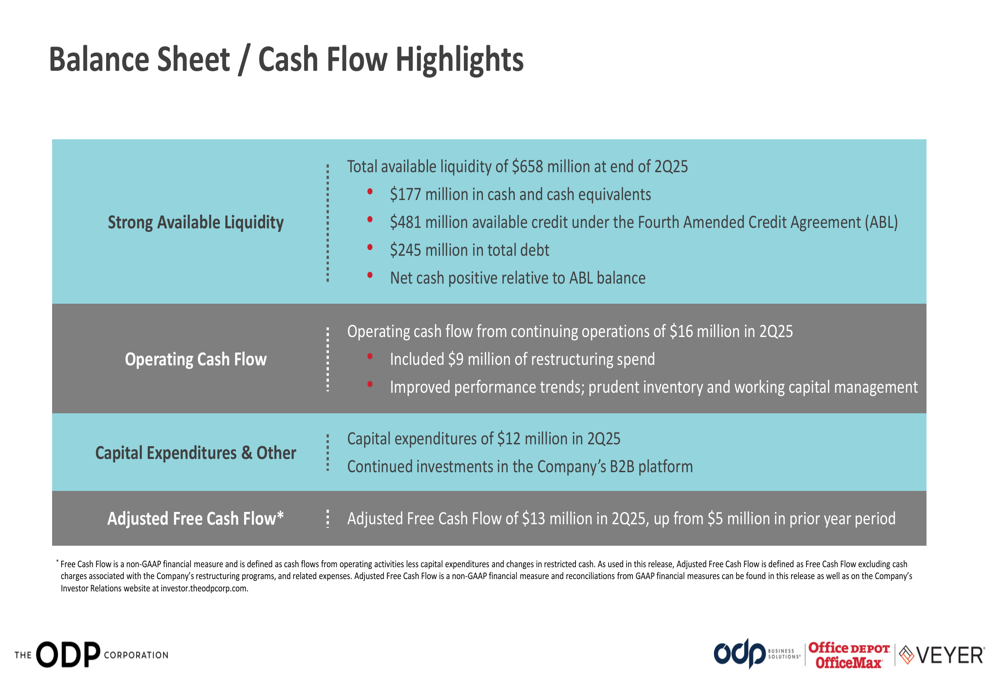

ODP maintained a strong liquidity position at the end of Q2 2025, with total available liquidity of $658 million. This included $177 million in cash and cash equivalents and $481 million available under the company’s credit agreement. Total (EPA:TTEF) debt stood at $245 million, leaving the company in a net cash positive position.

The balance sheet and cash flow highlights demonstrate the company’s financial stability:

Operating cash flow from continuing operations improved significantly to $16 million in Q2 2025, compared to a $1 million outflow in the same period last year. This improvement was attributed to better performance trends and prudent inventory and working capital management, despite including $9 million in restructuring expenses.

Forward Outlook

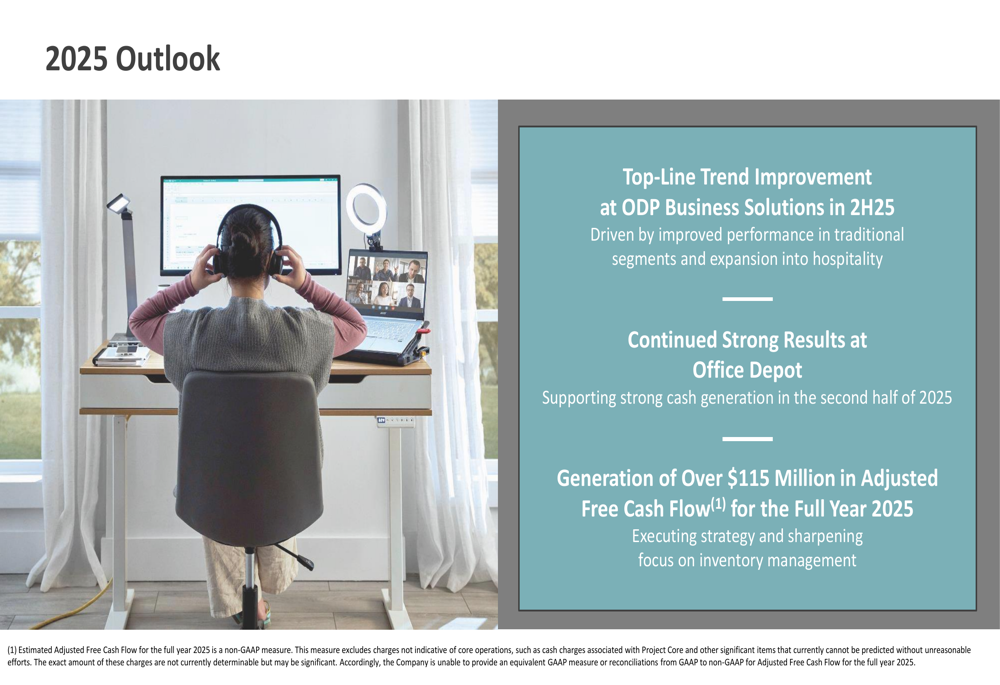

Looking ahead, ODP expects continued improvement in top-line trends for its Business Solutions division in the second half of 2025, driven by better performance in traditional segments and the expansion into hospitality. The company also anticipates strong results from Office Depot to support cash generation.

For the full year 2025, ODP projects adjusted free cash flow generation of over $115 million, a significant figure relative to the company’s current market capitalization of approximately $479 million based on recent trading.

CEO Gerry Smith emphasized the company’s progress on its strategic initiatives: "We are executing and making meaningful progress on our strategy, leveraging our core strengths and capturing opportunities in both traditional and new markets."

The key takeaways presented by management highlight both the progress made in Q2 and expectations for continued improvement:

While ODP faces ongoing challenges in its traditional markets, the company’s improved cash flow generation, strategic expansion into hospitality, and optimization initiatives suggest a pathway to stabilization and potential growth in the coming quarters, despite the overall revenue declines experienced in recent periods.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.