Moody’s downgrades Senegal to Caa1 amid rising debt concerns

Introduction & Market Context

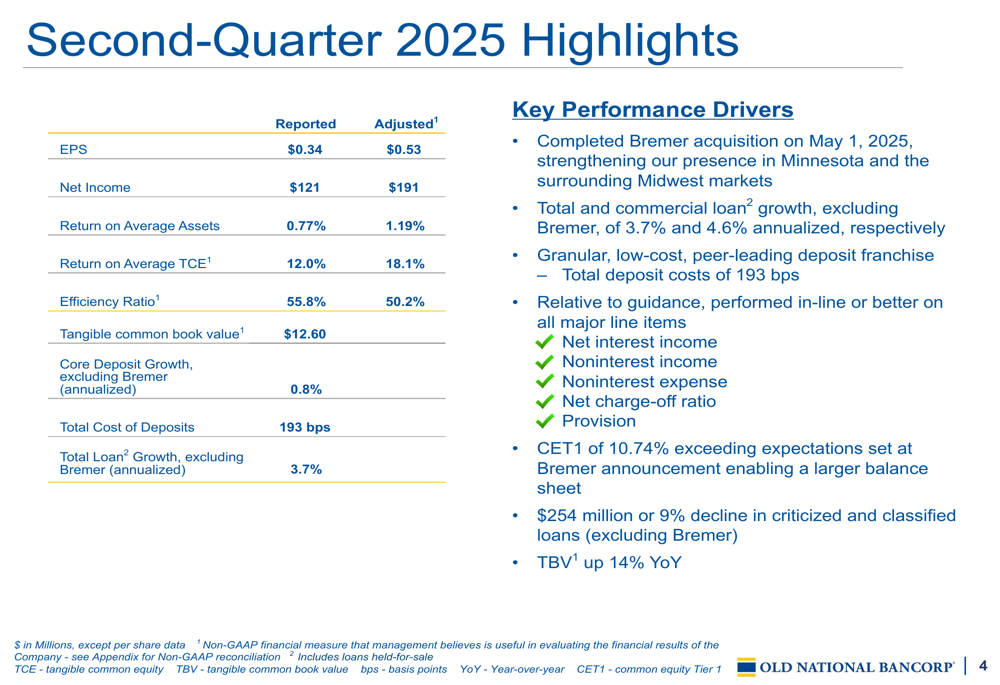

Old National Bancorp (NASDAQ:ONB) released its second quarter 2025 financial results on July 22, showcasing significant growth across key metrics, largely driven by the recently completed Bremer Bank acquisition. The regional bank reported adjusted earnings per share of $0.53, representing an 18% increase from the previous quarter and a 15% year-over-year improvement.

The company’s stock closed at $22.65 on July 21, down 1.01% ahead of the earnings release, but has shown resilience with a price well above its 52-week low of $16.83. Following a strong first quarter that beat analyst expectations, investors have been closely watching how the Bremer integration would impact second quarter performance.

Quarterly Performance Highlights

Old National delivered impressive results across its key financial metrics for Q2 2025. Adjusted net income reached $191 million, up 32% quarter-over-quarter and 33% year-over-year, while adjusted return on average assets improved to 1.19%.

As shown in the following comprehensive overview of the quarter’s performance:

The bank’s efficiency ratio improved to 50.2% on an adjusted basis, demonstrating effective cost management despite the integration of Bremer operations. Tangible common book value increased to $12.60, representing a solid 14% year-over-year growth.

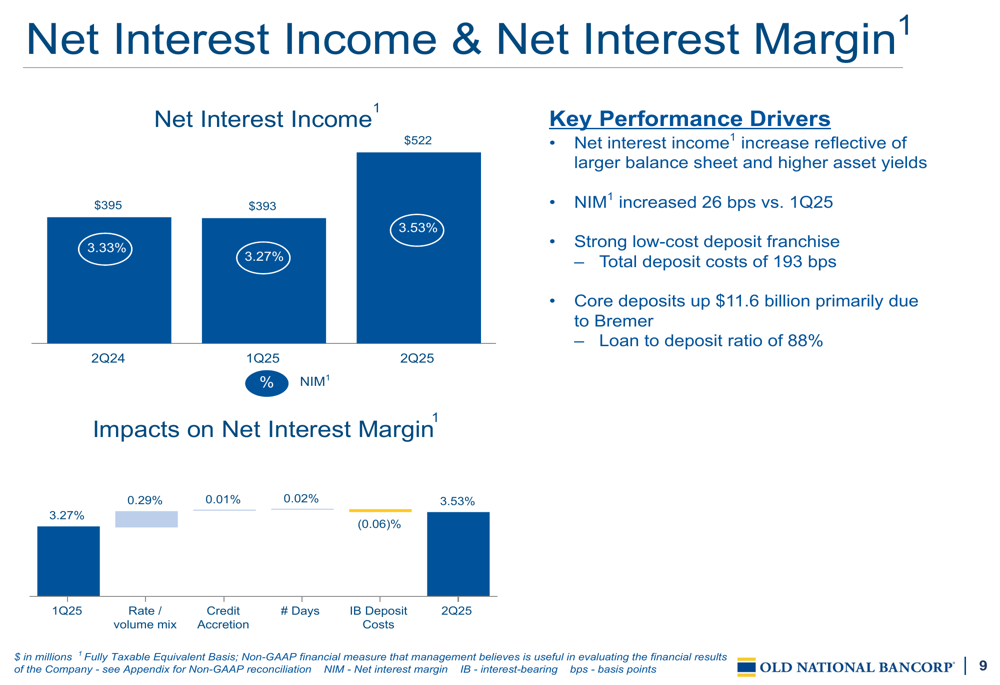

Net interest income grew substantially to $522 million, up 33% from the previous quarter and 32% year-over-year. This growth was accompanied by an expansion in net interest margin to 3.53%, a 26 basis point improvement from Q1 2025.

The following chart illustrates this positive trend in net interest income and margin:

Bremer Acquisition Impact

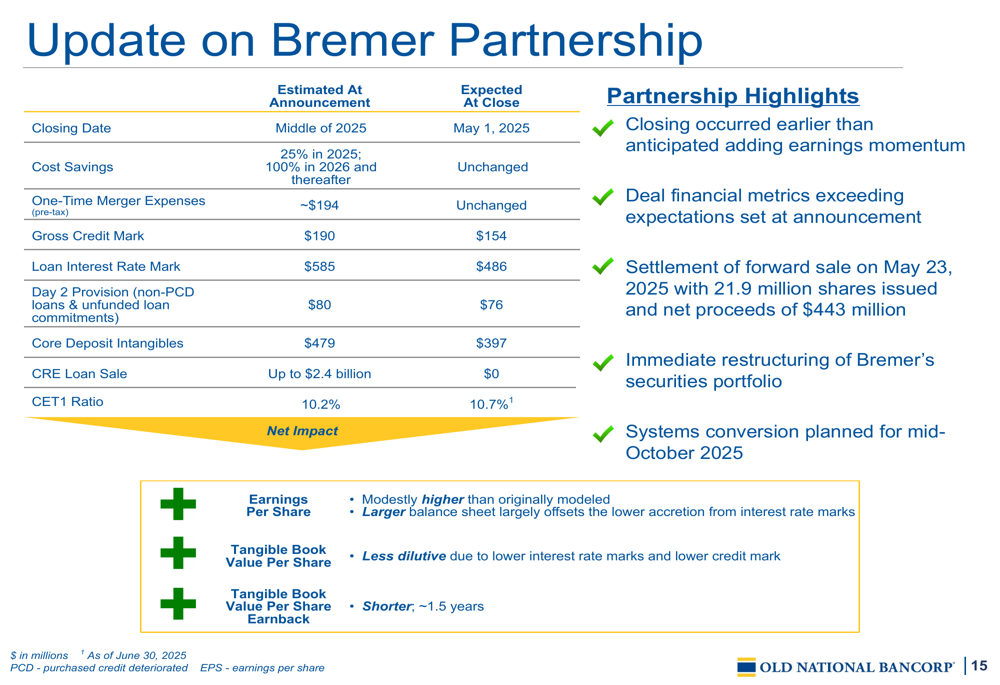

The Bremer Bank acquisition, which closed during the second quarter, has significantly transformed Old National’s balance sheet and market presence. The company highlighted that the partnership is already exceeding expectations set at the announcement.

As illustrated in the update on the Bremer partnership:

The acquisition has contributed substantially to the growth in loans and deposits, with system conversions planned for mid-October. Management expressed confidence that the integration is proceeding smoothly and will continue to add to earnings momentum.

Deposit and Loan Growth

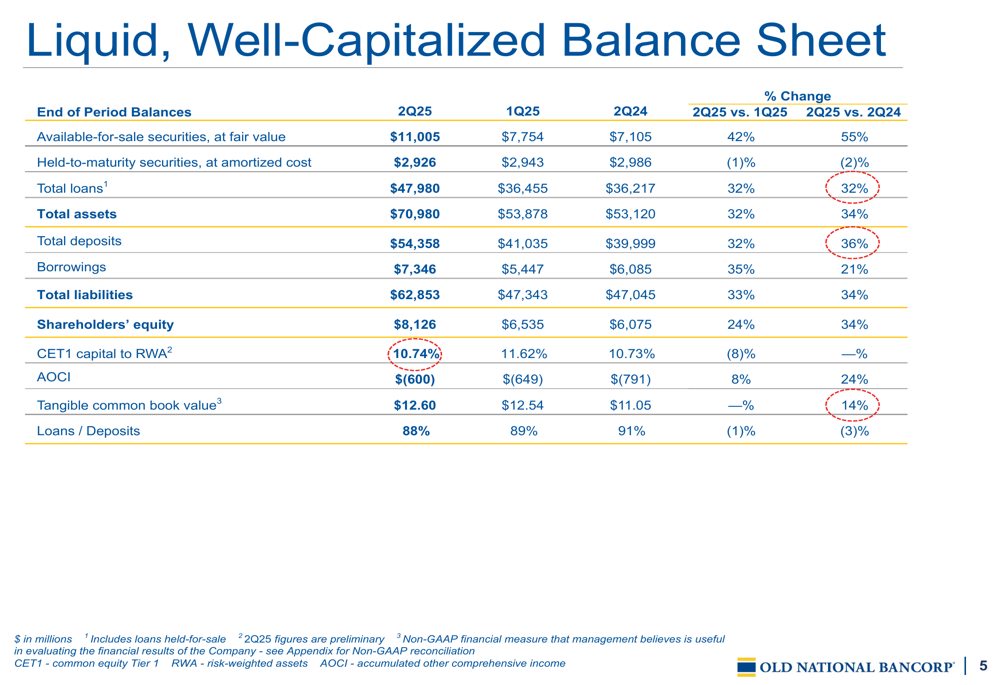

Old National’s balance sheet showed remarkable expansion in Q2 2025, with total assets reaching $70.98 billion, up 32% from the previous quarter and 34% year-over-year. This growth was primarily driven by the Bremer acquisition but also reflected organic business development.

The bank’s liquid, well-capitalized balance sheet is detailed in the following slide:

Total (EPA:TTEF) loans increased to $47.98 billion, up 32% from both the previous quarter and year-over-year. The loan portfolio remains well-diversified, with commercial and industrial loans comprising 31% and commercial real estate loans accounting for 45% of the total portfolio.

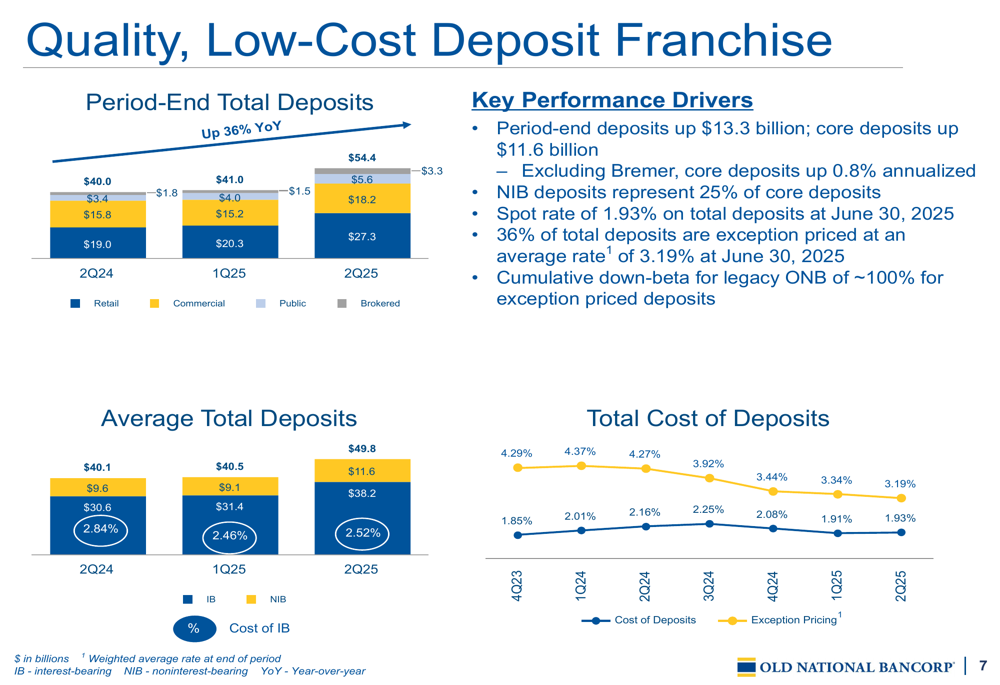

The deposit franchise also showed impressive growth, with total deposits reaching $54.36 billion, up 32% quarter-over-quarter and 36% year-over-year. The bank maintained a favorable loan-to-deposit ratio of 88%.

The quality of the deposit base is highlighted in the following chart:

The bank’s total cost of deposits was 193 basis points, reflecting a strong low-cost deposit franchise. Management noted that 36% of deposits are exception priced, contributing to the bank’s ability to manage funding costs effectively.

Credit Quality and Capital Position

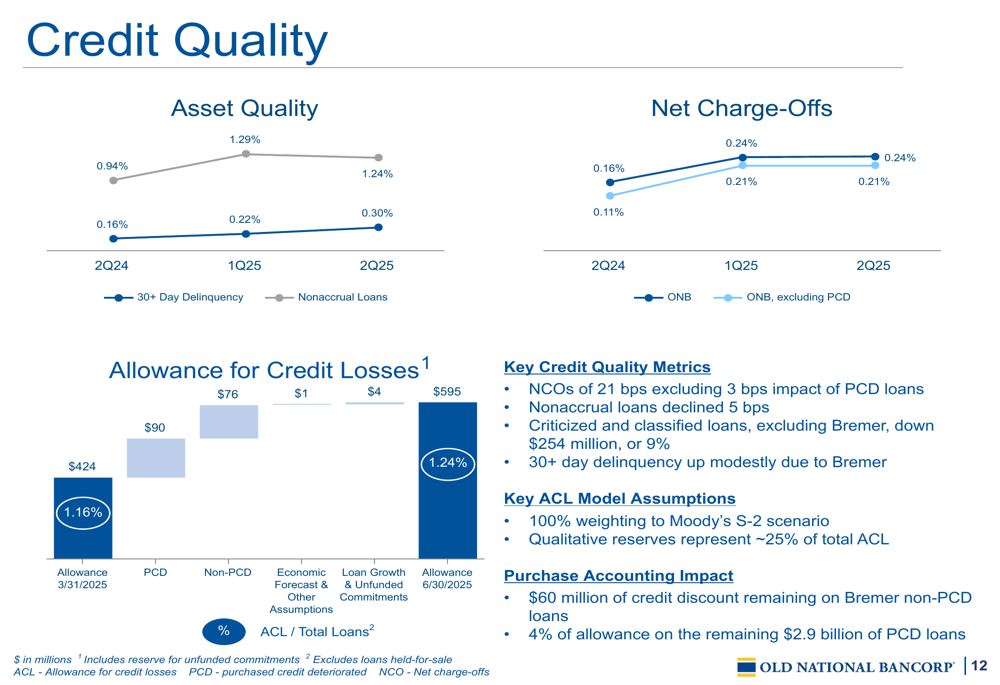

Old National maintained strong credit quality metrics in the second quarter, with a $254 million decline in criticized loans. The bank’s conservative approach to lending, particularly in commercial real estate, has positioned it well compared to peers.

The following slide illustrates the bank’s credit quality metrics:

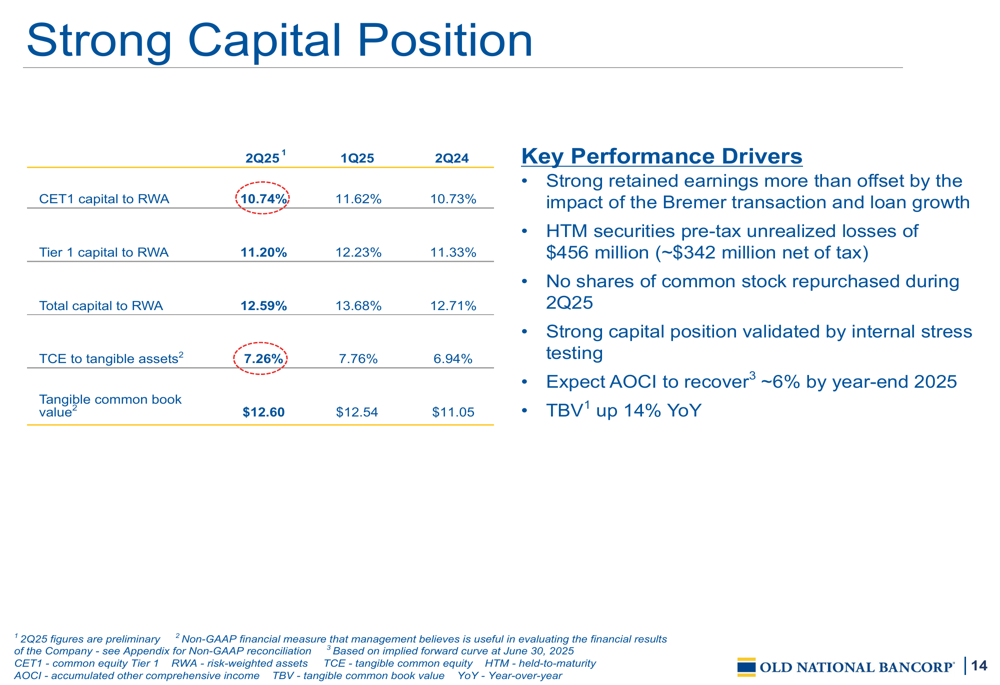

The bank’s capital position remains robust, with a Common Equity Tier 1 (CET1) ratio of 10.74%. This strong capital base provides flexibility for future growth opportunities while maintaining a conservative risk profile.

As shown in the capital position summary:

Management noted that retained earnings more than offset the capital impact of the Bremer transaction, demonstrating the bank’s ability to quickly rebuild capital following a significant acquisition.

Forward Outlook

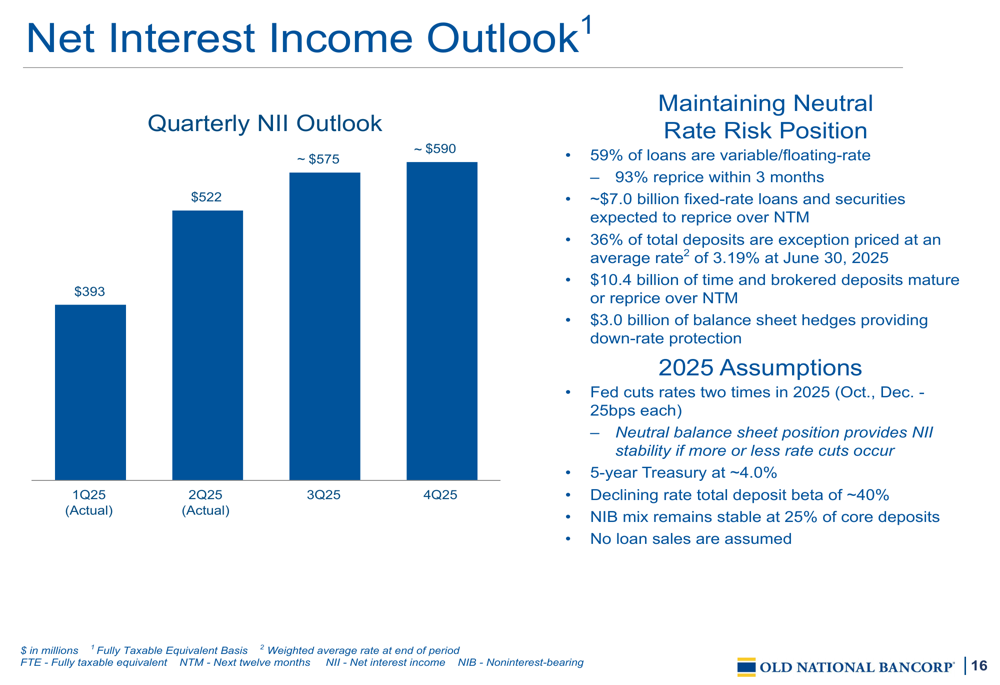

Old National provided an optimistic outlook for the remainder of 2025, projecting continued growth in key metrics. For the third quarter, the bank expects net interest income of approximately $575 million and noninterest income of around $120 million.

The following chart illustrates the projected growth in net interest income:

For the full year 2025, Old National forecasts net interest income between $2,065 million and $2,095 million. End-of-period loans are expected to grow by 2-4% in the third quarter, reflecting continued momentum in lending activities.

Management emphasized that the Bremer partnership is expected to continue driving growth, with the full benefits of the acquisition to be realized following the system conversions in mid-October.

Conclusion

Old National Bancorp’s second quarter 2025 results demonstrate the positive impact of the Bremer acquisition and the bank’s ability to execute on its growth strategy. With strong performance across key metrics, a robust capital position, and an optimistic outlook for the remainder of the year, the bank appears well-positioned to continue its growth trajectory.

While the integration of Bremer operations presents both opportunities and challenges, management’s confidence in exceeding the initially projected benefits suggests the acquisition will be a significant driver of long-term value for shareholders.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.