Microvast Holdings announces departure of chief financial officer

Introduction & Market Context

Omnicell , Inc. (NASDAQ:OMCL) released its Q1 2025 investor presentation on May 6, highlighting significant year-over-year improvements in financial performance and continued progress in its strategic transformation toward recurring revenue streams. The medication management technology provider reported strong quarterly results amid its ongoing shift toward a SaaS-based business model and expansion of expert services.

The company’s shares were trading down 2.15% at $30.49 at the previous market close, with premarket activity showing additional pressure with an 8.86% decline to $27.79. Despite this market reaction, the presentation emphasized Omnicell’s strengthening financial position and strategic initiatives.

Q1 2025 Financial Performance

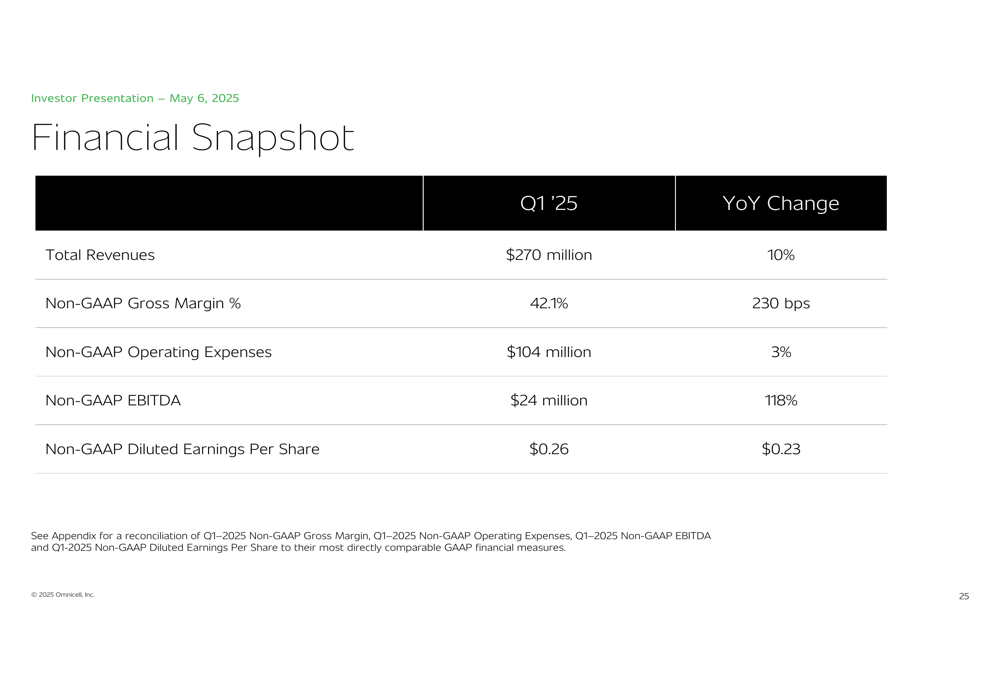

Omnicell reported total revenues of $270 million for Q1 2025, representing a 10% year-over-year increase. The company demonstrated significant improvement in profitability metrics, with non-GAAP EBITDA reaching $24 million, a remarkable 118% increase compared to the same period last year. Non-GAAP diluted earnings per share came in at $0.26, up $0.23 year-over-year.

As shown in the following financial snapshot from the presentation, gross margin improvements were a key driver of enhanced profitability:

The company’s non-GAAP gross margin expanded to 42.1%, a 230 basis point improvement year-over-year, while non-GAAP operating expenses as a percentage of revenue decreased from 41.3% to 38.7%. This operational leverage helped drive the substantial EBITDA growth.

A detailed reconciliation of GAAP to non-GAAP metrics shows the company’s transformation from a GAAP net loss of $7 million to a non-GAAP EBITDA of $23.6 million:

Strategic Shift to Recurring Revenue

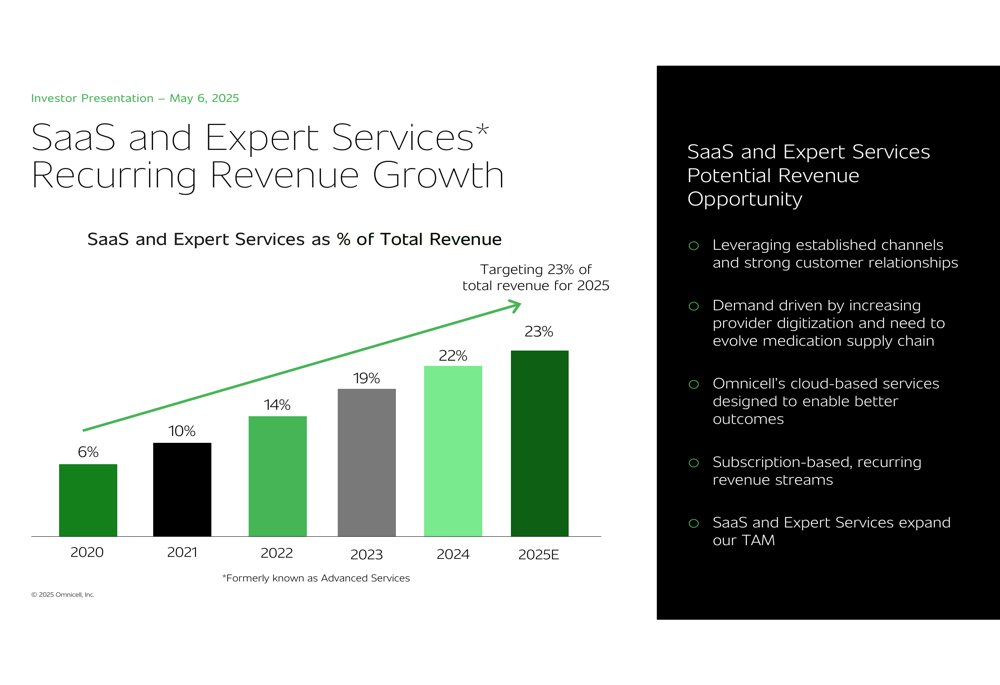

A central theme of Omnicell’s presentation was the company’s strategic transformation toward recurring revenue streams, particularly through SaaS and Expert Services. This segment now represents 23% of total revenue, up from just 6% in 2020, demonstrating the company’s successful execution of this strategic pivot.

The following chart illustrates this multi-year progression:

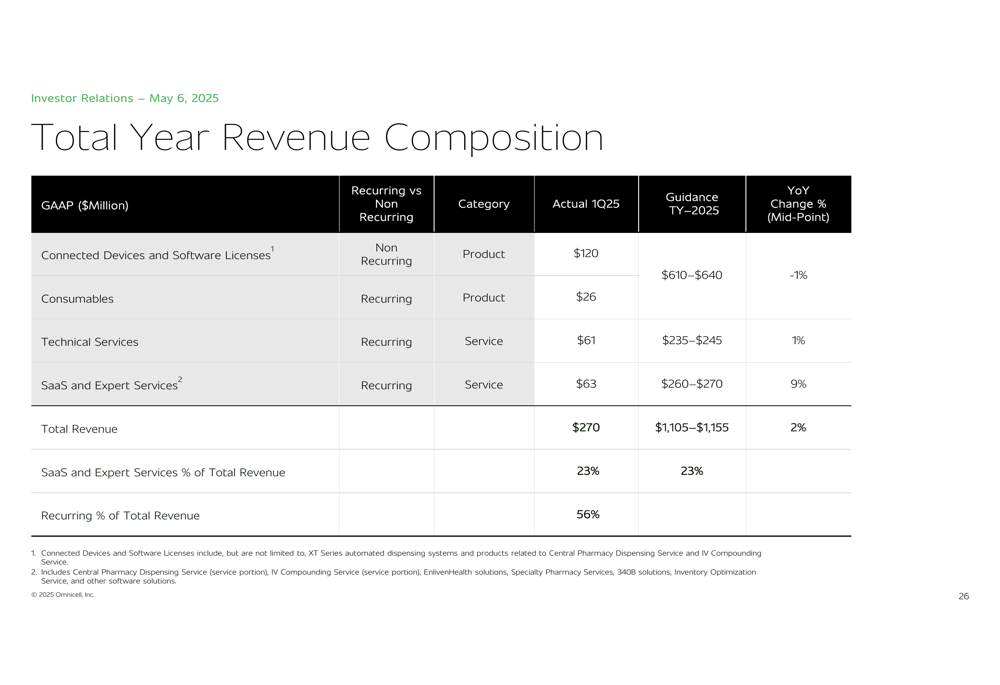

The presentation revealed that recurring revenue now accounts for 56% of Omnicell’s total revenue, including SaaS and Expert Services (23%), Technical Services (23%), and Consumables (10%). This shift provides the company with greater revenue predictability and stability.

The detailed revenue composition for Q1 2025 and full-year guidance shows the balance between recurring and non-recurring revenue streams:

Innovation Roadmap and Product Strategy

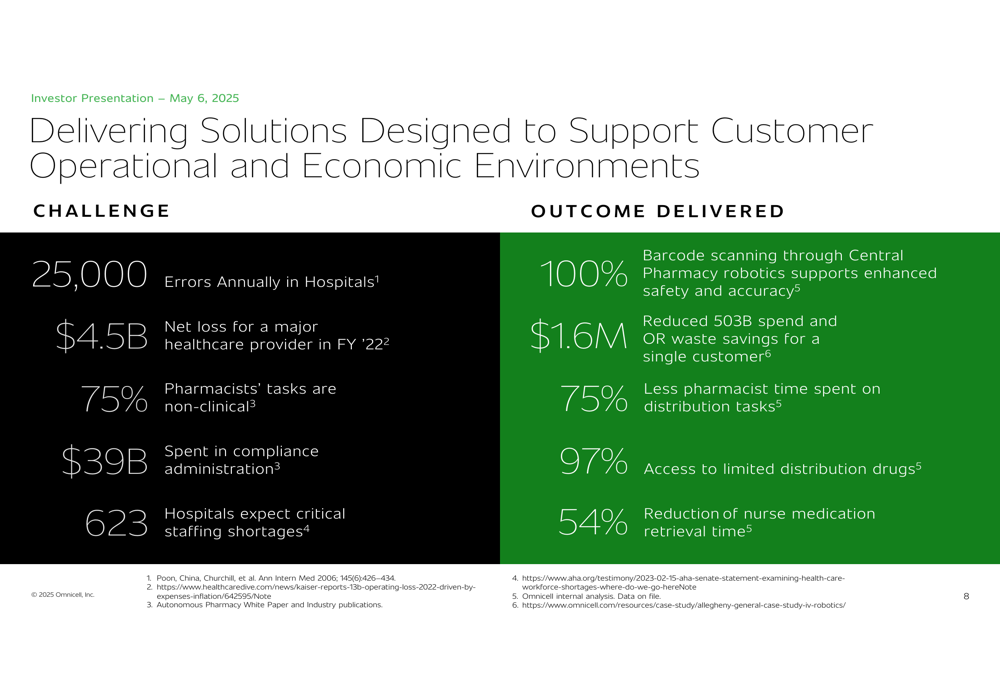

Omnicell’s presentation emphasized its vision of the "Autonomous Pharmacy," which aims to replace manual, error-prone activities with automated processes designed to be safer and more efficient. Key goals include zero medication errors, zero medication waste, 100% regulatory compliance, and allowing pharmacists to focus entirely on clinical activities.

The company highlighted how its solutions address critical healthcare challenges:

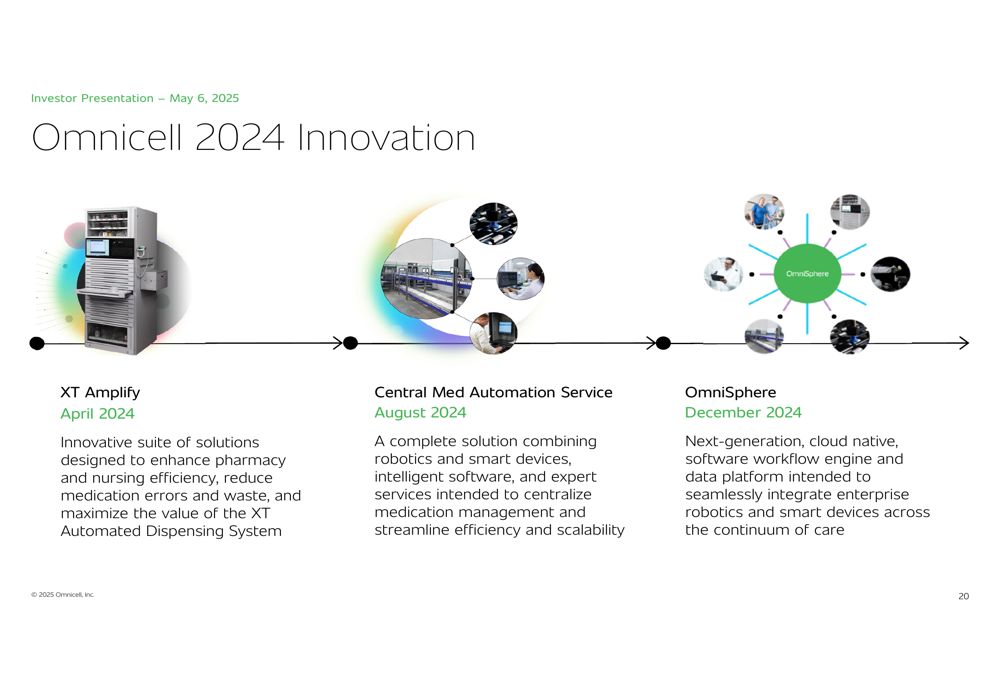

For 2024, Omnicell outlined three major innovations that will drive its growth strategy:

The company’s XT Amplify platform, launched in April 2024, offers solutions including XTExtend, MedChill, SupplyXpert, ServerScale, and CarePlus. The Central Med Automation Service, scheduled for August 2024, combines robotics, software, and expert services, while OmniSphere, planned for December 2024, will provide a next-generation cloud-native software workflow engine and data platform.

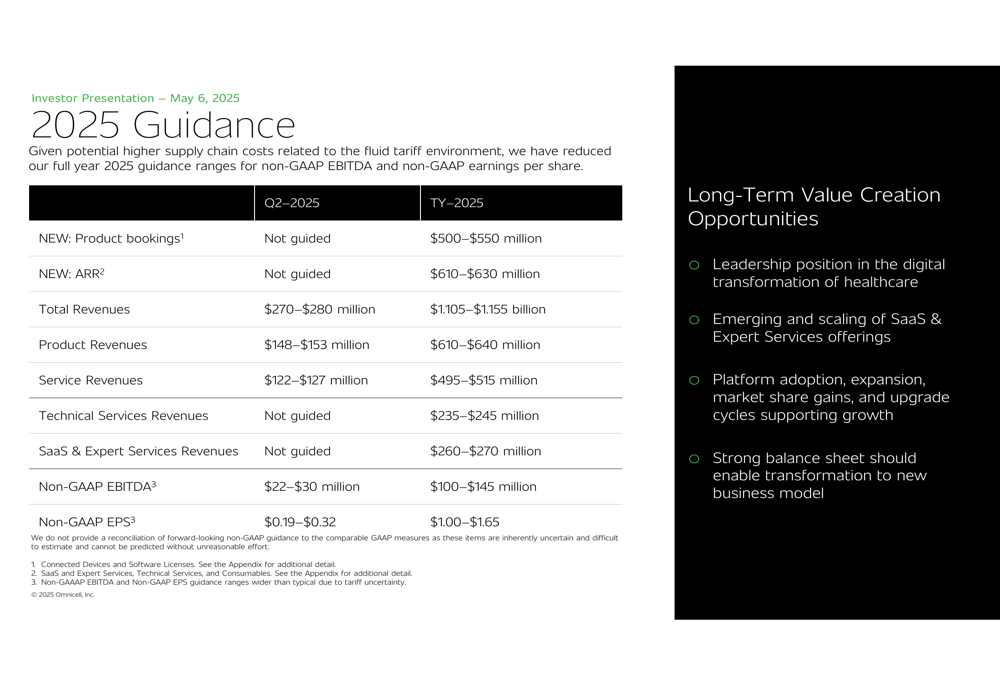

2025 Financial Outlook

Omnicell provided detailed financial guidance for Q2 2025 and the full year, projecting total revenues of $1.105-$1.155 billion for 2025, representing approximately 2% year-over-year growth at the midpoint:

The company introduced new metrics for 2025, including Product Bookings (projected at $500-$550 million) and Annual Recurring Revenue (ARR) (projected at $610-$630 million). For Q2 2025, Omnicell expects revenues between $270-$280 million and non-GAAP EPS between $0.19-$0.32.

Non-GAAP EBITDA for the full year is expected to range from $100-$145 million, with non-GAAP EPS projected between $1.00-$1.65. The wide guidance ranges suggest some uncertainty in the market environment, though the company emphasized its strong position with more than half of the top 300 U.S. health systems as customers.

Competitive Positioning

Omnicell highlighted several factors that it believes position the company for long-term success in the medication management market:

The company emphasized its proven track record of innovation, scaling of SaaS and Expert Services, and continued investment in new products and solutions. With a product backlog of $647 million and Annual Recurring Revenue of $580 million as of December 31, 2024, Omnicell believes it has a strong foundation for sustainable growth.

The presentation positioned Omnicell as having the right solutions and business model to address medication management challenges in healthcare, with a particular focus on leveraging its established customer relationships to drive adoption of its expanding portfolio of products and services.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.