Gold ticks up but remains pressured by Fed rate caution, easing trade fears

Introduction & Market Context

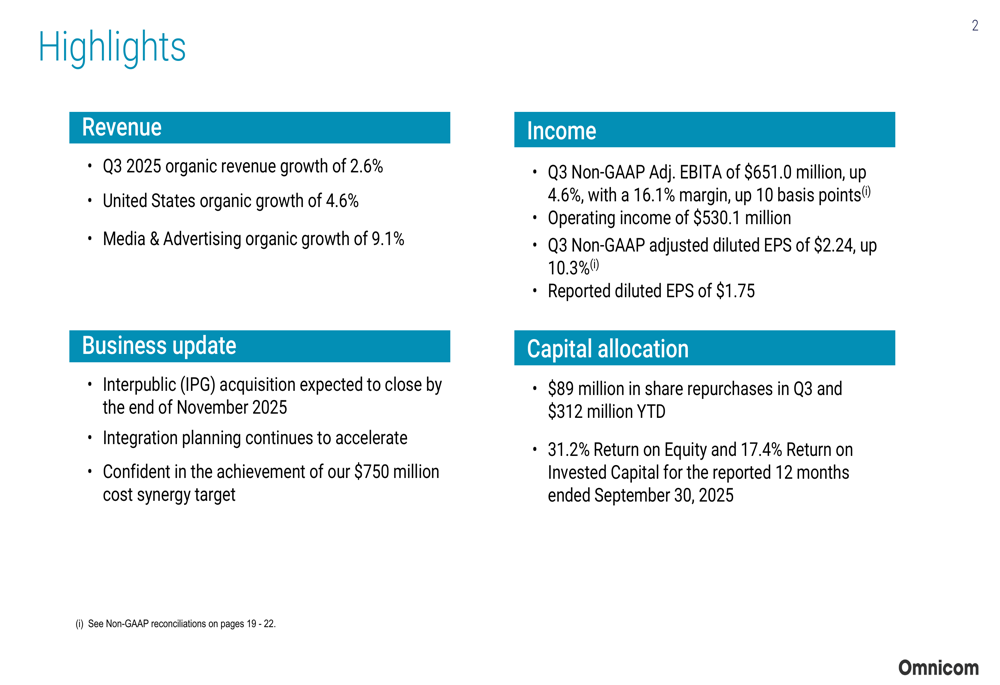

Omnicom Group Inc (NYSE:OMC) released its third quarter 2025 results on October 21, showing organic revenue growth of 2.6% amid varying performance across business segments and regions. The advertising and marketing services giant reported earnings per share of $2.24 on a non-GAAP adjusted basis, exceeding analysts’ expectations of $2.16, while revenue reached $4.04 billion against projections of $4.02 billion.

Following the earnings announcement, Omnicom’s stock closed at $78.19, up 0.67%, with an additional 0.4% gain in aftermarket trading. The company’s shares remain well below their 52-week high of $107, suggesting potential upside according to analyst targets ranging from $80 to $115.

Quarterly Performance Highlights

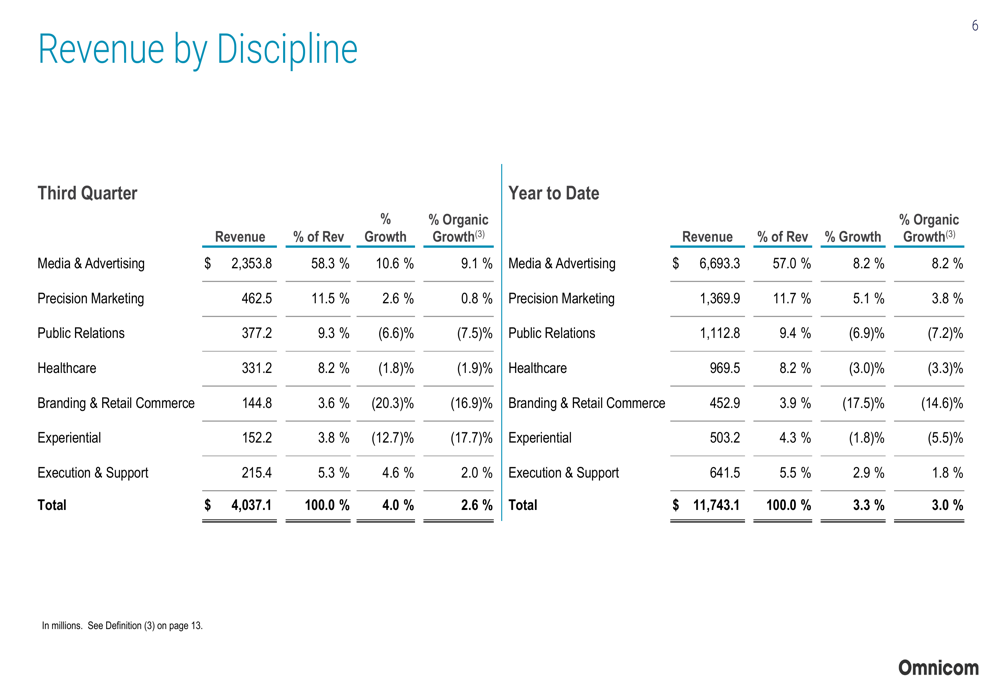

Omnicom delivered mixed results across its business segments in the third quarter, with Media & Advertising emerging as the standout performer. The company achieved 2.6% organic revenue growth overall, with particularly strong performance in the United States at 4.6%.

As shown in the following breakdown of revenue by discipline, Media & Advertising led the way with impressive 9.1% organic growth, while several other segments experienced significant declines:

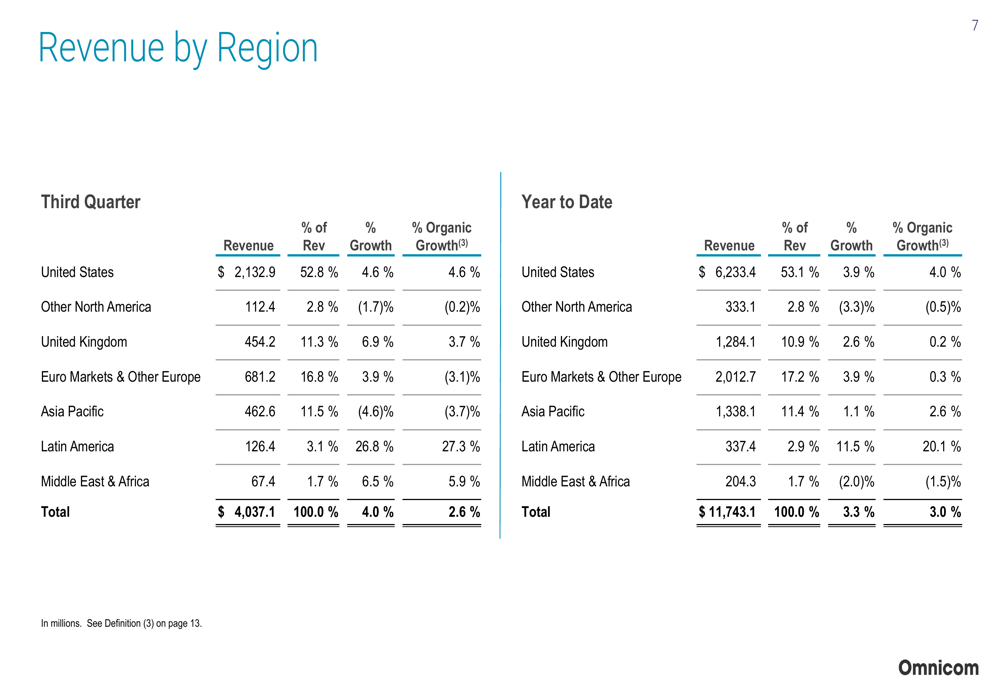

Geographically, performance varied substantially across regions. Latin America showed exceptional growth at 27.3%, while the United States remained solid with 4.6% organic growth. However, Euro Markets & Other Europe declined by 3.1%, and Asia Pacific fell by 3.7%.

The following regional breakdown illustrates these geographic disparities:

Detailed Financial Analysis

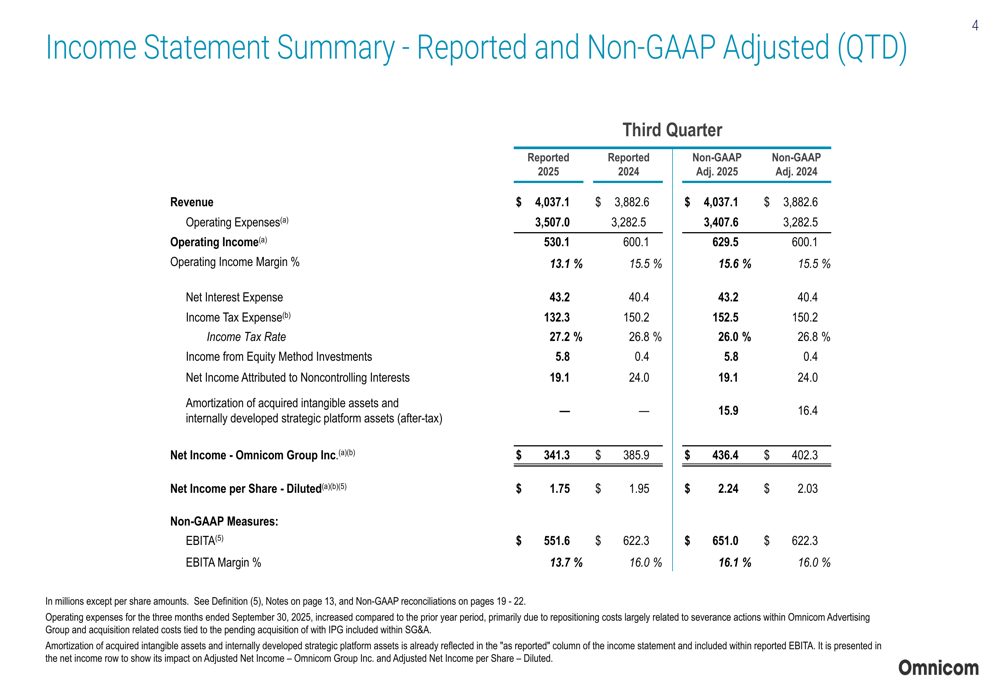

Omnicom reported third-quarter revenue of $4.04 billion, representing a 4.0% increase from the same period in 2024. The company’s non-GAAP adjusted EBITA reached $651.0 million, up 4.6% year-over-year, with a margin of 16.1%, representing a 10 basis point improvement.

The following highlights summarize Omnicom’s key financial metrics for the quarter:

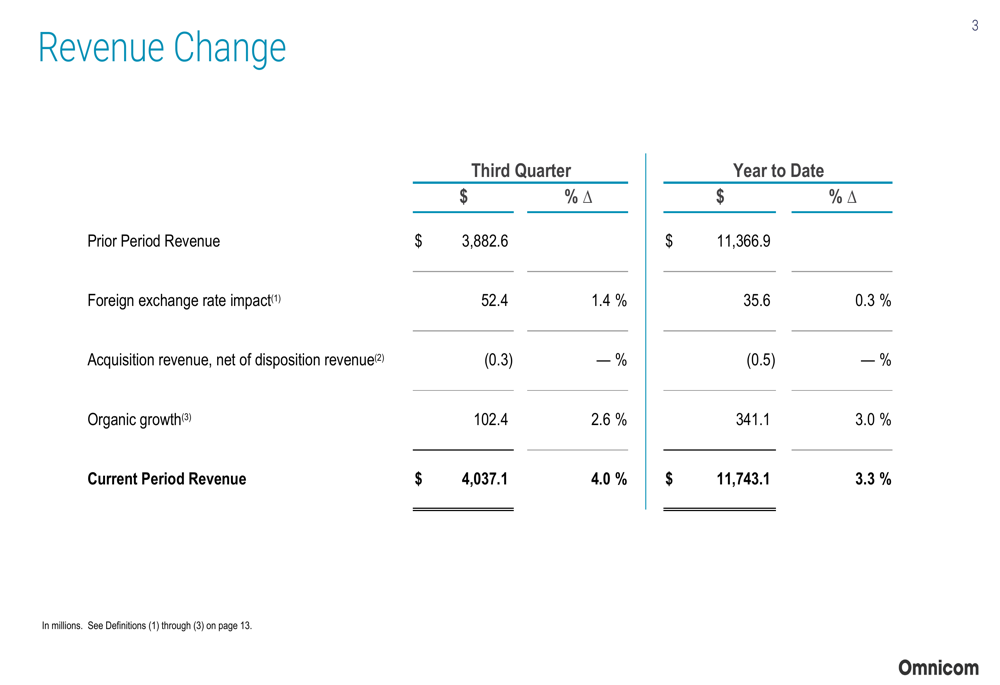

A closer examination of the revenue change analysis reveals that organic growth contributed $102.4 million to the quarterly revenue increase, while favorable foreign exchange rates added $52.4 million:

The company’s income statement shows reported operating income of $530.1 million, with non-GAAP adjusted operating income of $629.5 million after accounting for repositioning costs of $38.6 million and acquisition-related costs of $60.8 million:

Omnicom’s expense structure showed notable shifts compared to the previous year. Salary and related costs decreased as a percentage of revenue (44.1% vs. 47.6% in 2024), while third-party service costs increased (23.7% vs. 20.2%). This reflects the company’s changing business mix and ongoing operational adjustments.

Strategic Initiatives

The most significant strategic development for Omnicom is its pending acquisition of Interpublic Group (IPG), which is expected to close by the end of November 2025. The company reported that integration planning is accelerating, and management expressed confidence in achieving the targeted $750 million in cost synergies.

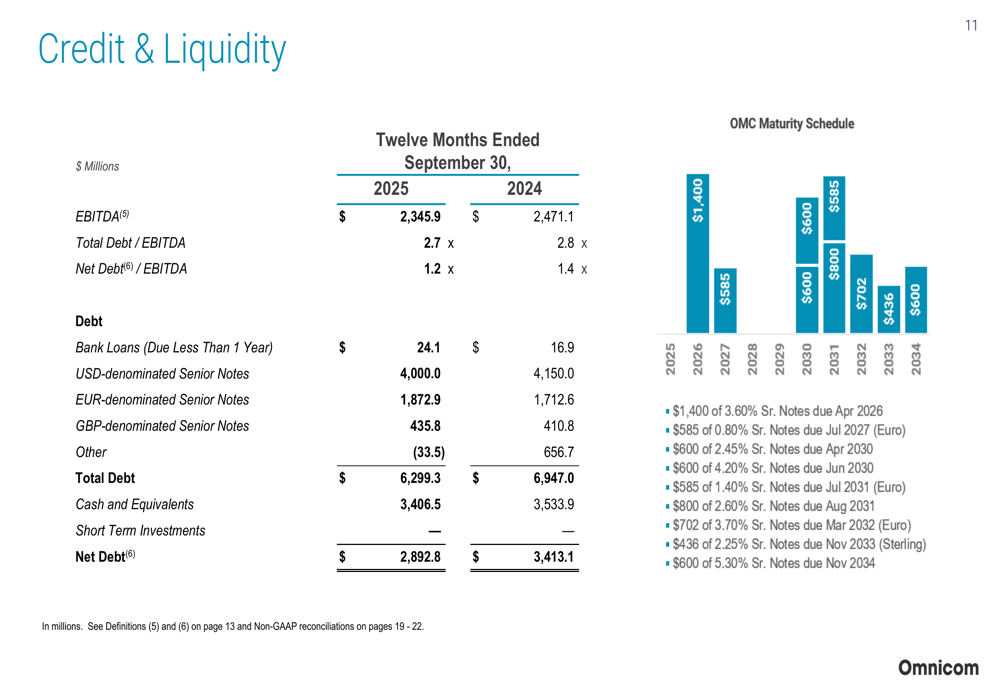

Omnicom’s debt position remains manageable as it prepares for this major acquisition. The company’s total debt to EBITDA ratio improved slightly to 2.7x from 2.8x in the prior year, while its net debt to EBITDA ratio improved to 1.2x from 1.4x.

The following slide provides a comprehensive view of Omnicom’s credit and liquidity position, including its debt maturity schedule:

Despite the company’s strong revenue performance, its profitability metrics have declined year-over-year. Return on Invested Capital fell to 17.4% from 20.2% in 2024, while Return on Equity dropped to 31.2% from 40.6%. These declines may reflect the costs associated with the company’s strategic repositioning and pending acquisition.

Free cash flow for the nine months ended September 30, 2025, reached $1,323.6 million, down from $1,402.1 million in the same period of 2024. The company continued its share repurchase program, buying back $89 million in shares during Q3 and $312 million year-to-date.

Forward-Looking Statements

Omnicom is maintaining its original organic growth guidance of 2.5-4.5% for the full year, consistent with its third-quarter performance of 2.6% organic growth. The company anticipates potential project work in Q4 2025 valued between $200 million and $250 million.

The successful integration of Interpublic Group will be crucial for Omnicom’s future performance. Management has confirmed synergy expectations for 2026, emphasizing the strategic fit between the two companies.

Key risks and challenges facing Omnicom include:

- Integration risks associated with the Interpublic Group merger

- Continued weakness in several business segments, particularly Public Relations, Healthcare, and Experiential

- Regional challenges in Europe and Asia Pacific

- Declining profitability metrics despite revenue growth

- Macroeconomic pressures that could impact client budgets

Despite these challenges, Omnicom’s strong performance in Media & Advertising, which accounts for 58.3% of total revenue, provides a solid foundation for future growth. The company’s improved debt ratios also position it well for the upcoming acquisition and integration process.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.