Street Calls of the Week

Introduction & Market Context

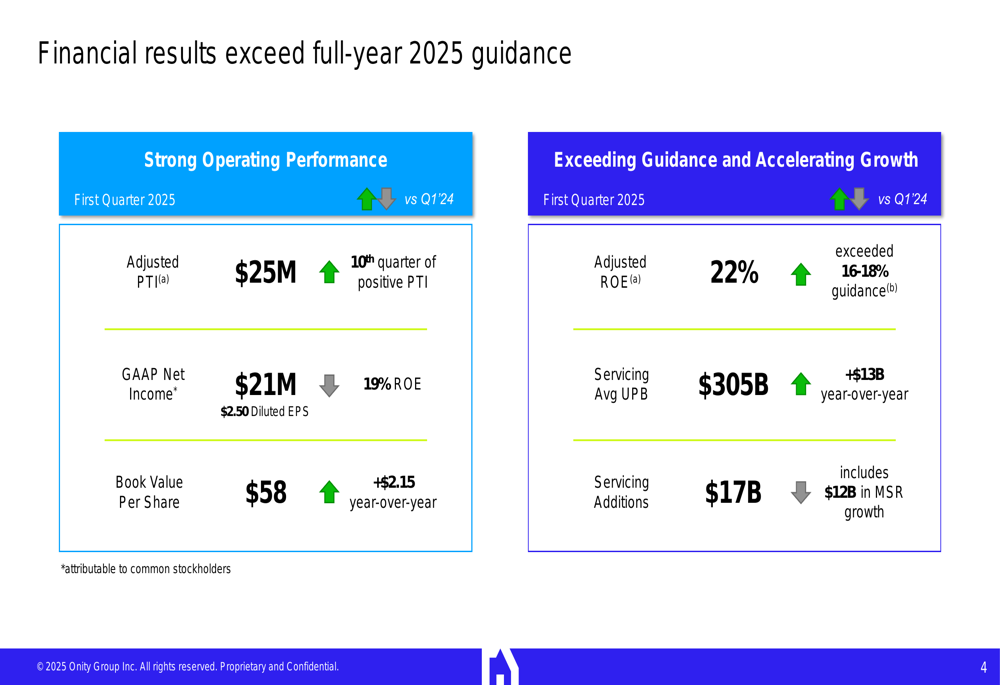

Onity Group Inc (NYSE:ONIT) presented its first quarter 2025 business update on April 30, 2025, highlighting strong financial performance that exceeded the company’s full-year guidance. The mortgage servicer and originator reported an adjusted return on equity (ROE) of 22%, significantly outpacing its previously announced 16-18% guidance for 2025.

The company’s presentation comes amid continued interest rate volatility and economic uncertainty, with Onity emphasizing its balanced business model designed to perform well in both high and low interest rate environments. This approach appears to be paying dividends, as the company’s stock has recovered from its post-Q4 2024 earnings drop, trading at $35.53 as of April 29, 2025, up from its 52-week low of $22.40.

Quarterly Performance Highlights

Onity reported its tenth consecutive quarter of positive adjusted pre-tax income (PTI), reaching $25 million for Q1 2025. The company achieved GAAP net income of $21 million, translating to $2.50 diluted earnings per share and a 19% return on equity.

As shown in the following financial results slide, Onity’s performance exceeded expectations across multiple metrics:

Book value per share increased to $58, representing a $2.15 gain year-over-year. The company’s servicing portfolio average unpaid principal balance (UPB) grew to $305 billion, up $13 billion from the same period last year. Servicing additions totaled $17 billion, including $12 billion in mortgage servicing rights (MSR) growth.

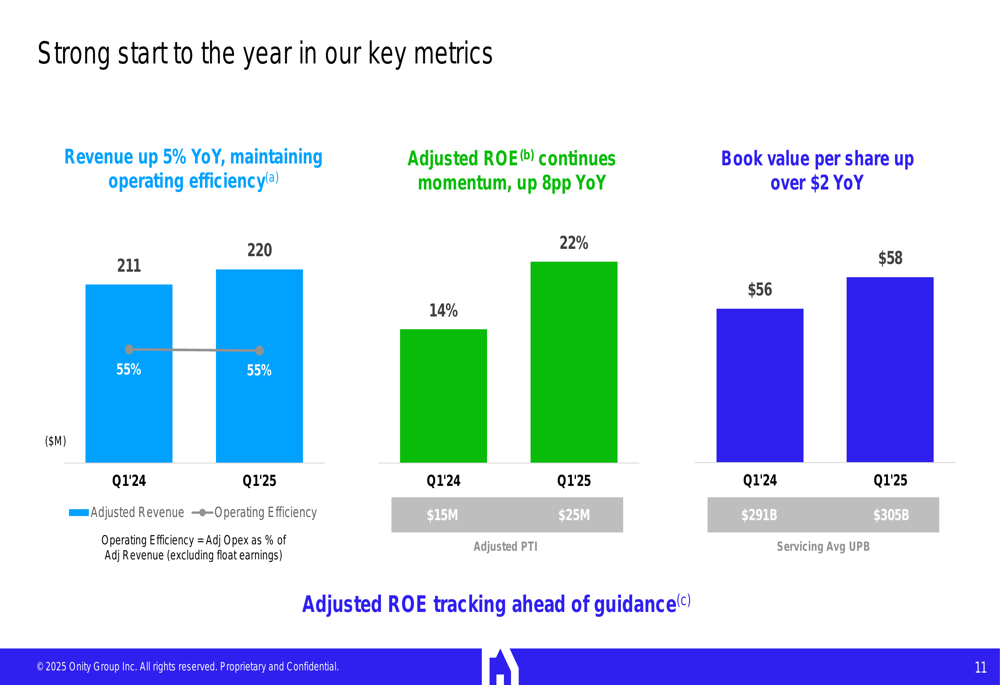

Revenue increased 5% year-over-year to $220 million while maintaining operating efficiency, as illustrated in this key metrics slide:

Particularly notable was the improvement in adjusted ROE, which jumped 8 percentage points from 14% in Q1 2024 to 22% in Q1 2025, significantly exceeding the company’s full-year guidance range of 16-18%.

Strategic Initiatives

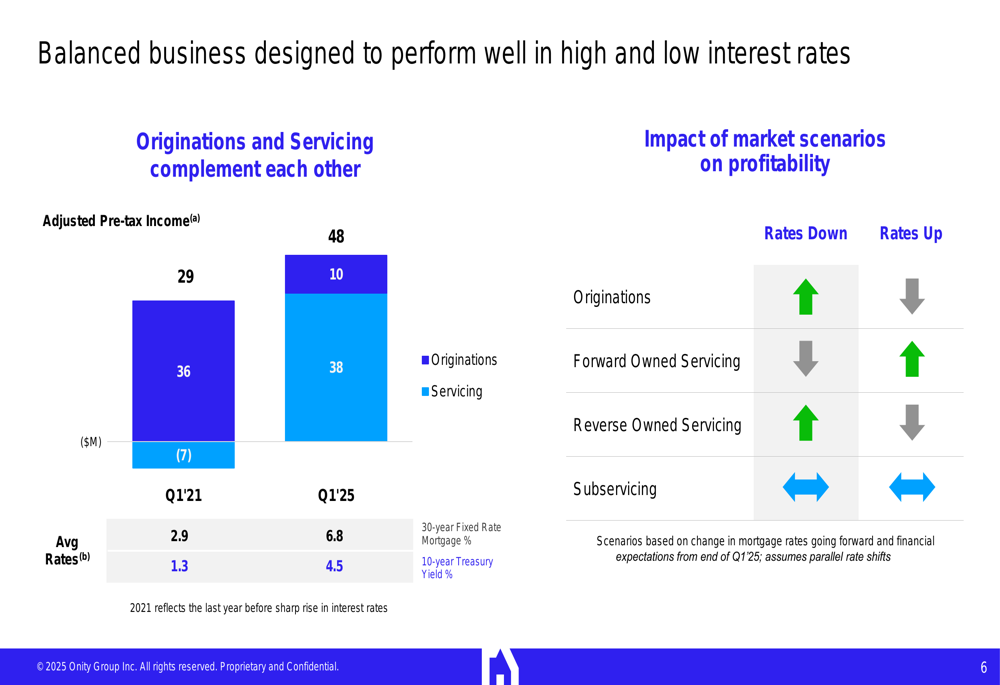

Onity’s presentation emphasized its balanced business approach, designed to perform well regardless of interest rate movements. This strategy appears to be working effectively, as demonstrated by the complementary performance of its originations and servicing segments.

The following slide illustrates how the company has maintained strong adjusted pre-tax income across different interest rate environments:

In Q1 2025, with average rates at 6.8%, originations contributed $38 million to adjusted pre-tax income, while servicing added $10 million. This balanced performance contrasts with Q1 2021 (when rates were at 2.9%), when originations generated $36 million but servicing posted a $7 million loss.

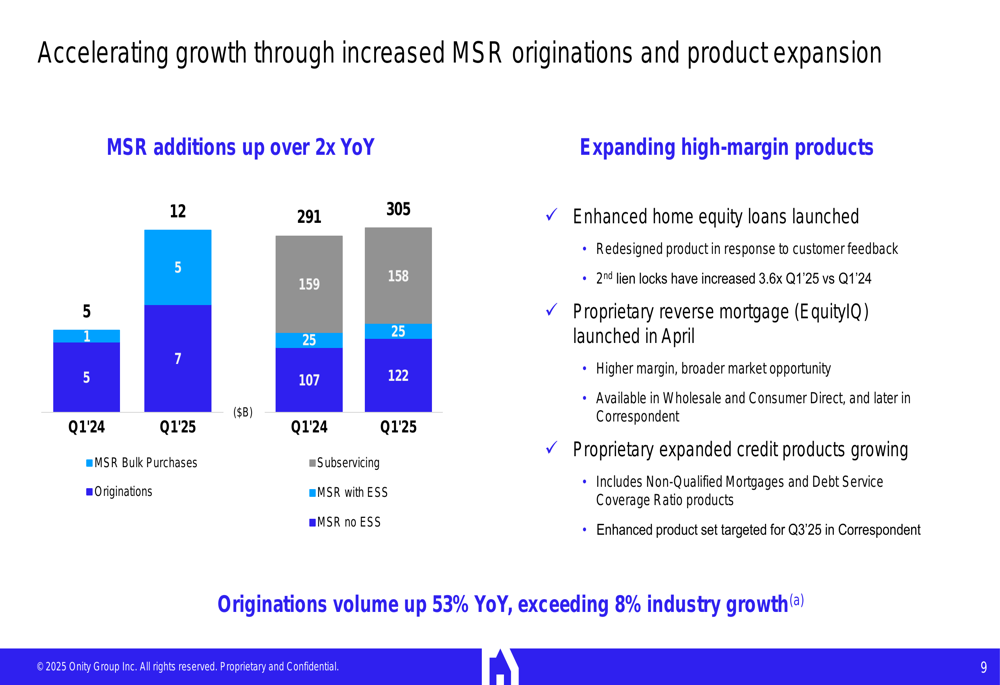

The company is also accelerating growth through increased MSR originations and product expansion, as shown in this growth strategy slide:

MSR additions more than doubled year-over-year, while originations volume increased 53% compared to the industry growth of 8%. Onity has also expanded its high-margin product offerings, including home equity loans and a proprietary reverse mortgage product (EquityIQ) launched in April.

Competitive Industry Position

Onity highlighted its competitive advantages in servicing performance, showcasing awards and efficiency metrics that position it favorably against industry peers.

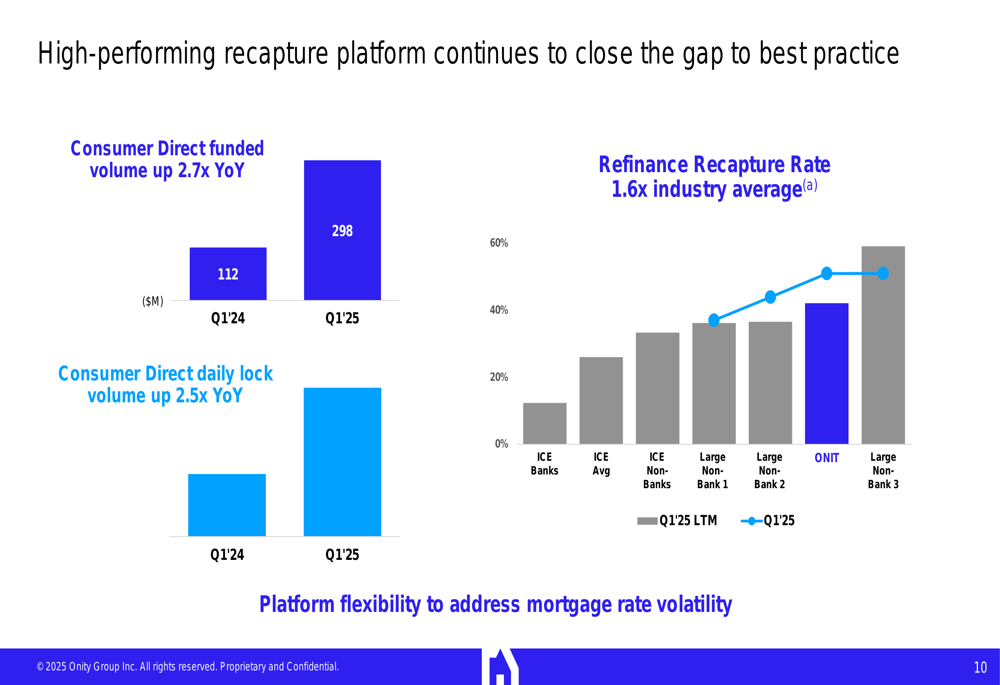

The company’s recapture platform is performing exceptionally well, with consumer direct funded volume up 2.7x year-over-year and a refinance recapture rate of 41%, which is 1.6x the industry average:

This performance demonstrates Onity’s ability to retain customers when refinancing opportunities arise, a critical capability in a volatile interest rate environment.

The company also emphasized its top-tier servicing performance through various industry recognitions and cost advantages:

Onity has received all possible GSE awards for the last four years and maintains a competitive cost structure, with performing loans serviced at 18%+ lower costs and non-performing loans at 52%+ lower costs compared to industry benchmarks.

Forward-Looking Statements

Looking ahead, Onity outlined its expectations for navigating economic uncertainty, including continued interest rate volatility, increased industry M&A activity, and a higher probability of recession.

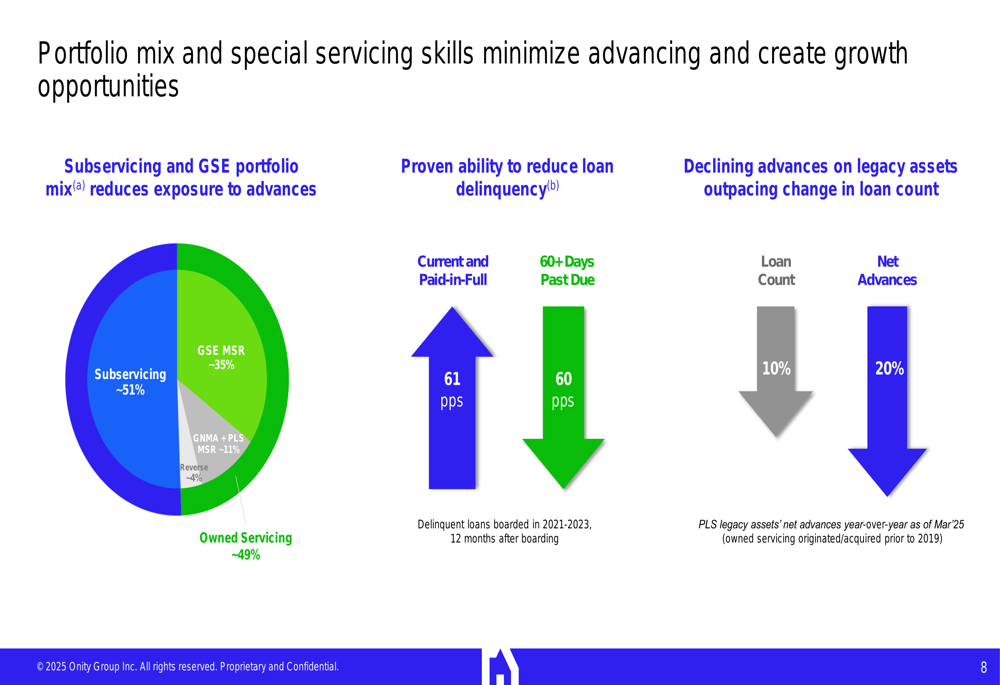

The company’s portfolio mix and special servicing capabilities are designed to minimize advancing requirements and create growth opportunities:

Subservicing and GSE loans comprise approximately 86% of Onity’s servicing portfolio, reducing exposure to advances. The company has demonstrated an ability to reduce loan delinquency and decrease advances on legacy assets at a rate outpacing the change in loan count.

Onity expects originations industry volume to increase by 17% in fiscal year 2025 compared to 2024, with unpredictable surges in refinancing activity. The company’s high-performing recapture platform positions it to capitalize on these opportunities while maintaining flexibility to address mortgage rate volatility.

Given the strong first quarter performance exceeding full-year guidance, investors will be watching closely to see if Onity revises its 2025 outlook upward in subsequent quarters. The company’s balanced approach and demonstrated ability to perform in various interest rate environments suggest it is well-positioned for continued success despite economic uncertainties.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.