Microvast Holdings announces departure of chief financial officer

Onsemi (NASDAQ:ON) reported first-quarter 2025 results showing significant year-over-year revenue declines but highlighted strong free cash flow generation and robust growth in its AI Data Center segment. The company’s presentation, released on May 5, 2025, revealed a strategic focus on high-growth markets amid broader semiconductor industry challenges.

Quarterly Performance Highlights

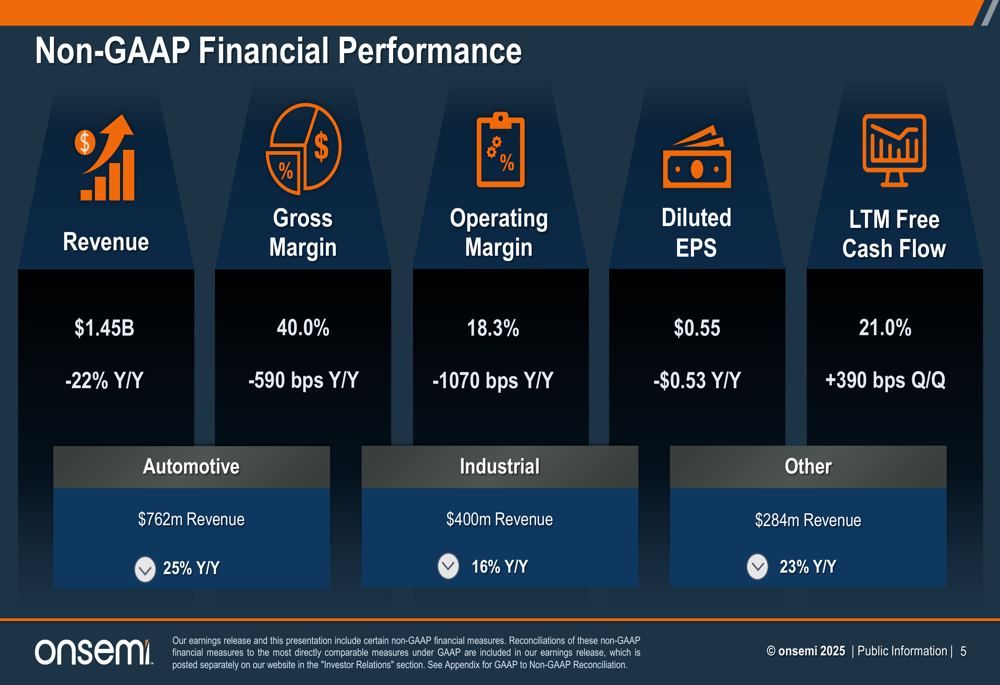

Onsemi reported Q1 2025 revenue of $1.45 billion, representing a 22% year-over-year decline. Despite this drop, the company maintained a non-GAAP gross margin of 40.0%, which management emphasized compares favorably to the approximately 30% margins achieved during previous industry downturns.

As shown in the following financial performance breakdown, automotive remained the largest segment at $762 million but declined 25% year-over-year, while the industrial segment generated $400 million, down 16% from the previous year:

The company’s operating margin contracted to 18.3%, down 1070 basis points year-over-year, while diluted EPS came in at $0.55, a decrease of $0.53 compared to Q1 2024.

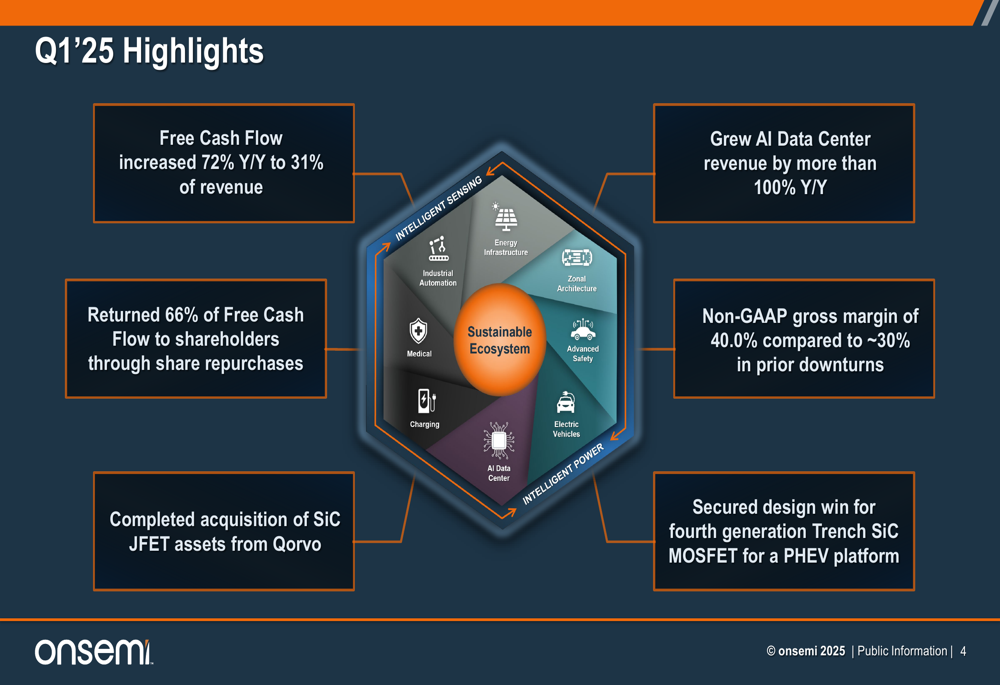

Despite revenue challenges, Onsemi highlighted several positive developments in its quarterly presentation. Free cash flow increased 72% year-over-year to 31% of revenue, with 66% of this cash returned to shareholders through share repurchases. The company also completed its acquisition of Qorvo (NASDAQ:QRVO)’s Silicon Carbide JFET Technology Portfolio, strengthening its position in wide bandgap semiconductors.

The following slide summarizes the key highlights from the quarter, including the strong performance in AI Data Center revenue, which grew more than 100% year-over-year:

Strategic Initiatives

Onsemi continues to position itself as a leader in the Silicon Carbide (SiC) market, targeting 35-40% market share. The company secured a design win for its fourth-generation Trench SiC MOSFET for a plug-in hybrid electric vehicle platform during the quarter, demonstrating continued traction in automotive applications.

The company’s presentation emphasized its focus on what it calls a "sustainable ecosystem" encompassing energy infrastructure, industrial automation, medical applications, advanced safety, AI data centers, electric vehicles, and charging infrastructure. This diversified approach aims to capture growth across multiple sectors.

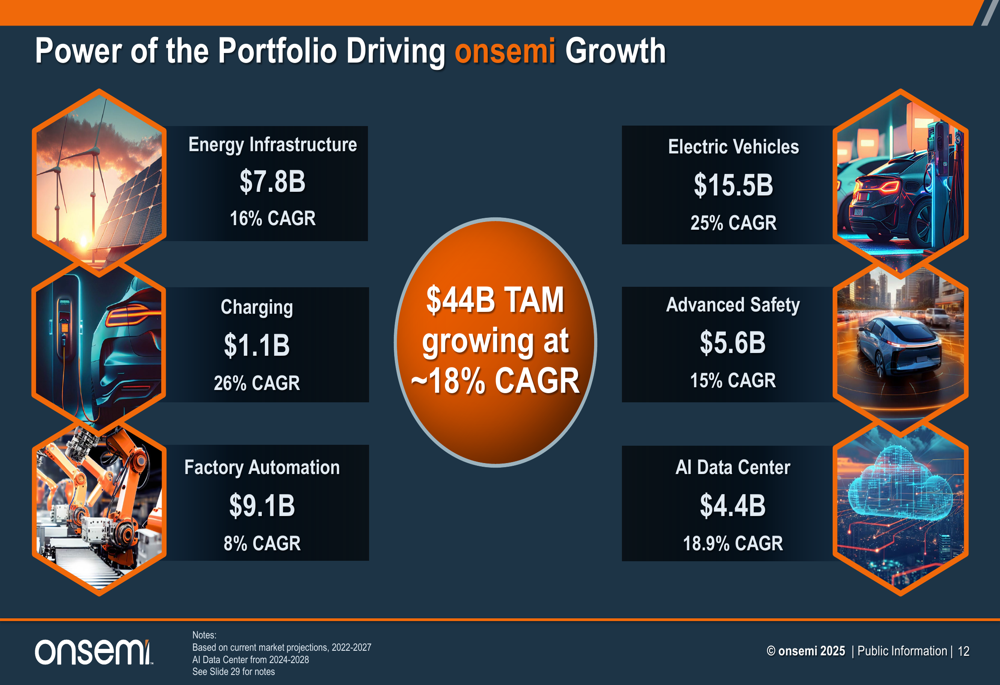

As illustrated in the following market opportunity breakdown, Onsemi is targeting a total addressable market of $44 billion growing at approximately 18% CAGR, with electric vehicles representing the largest opportunity at $15.5 billion:

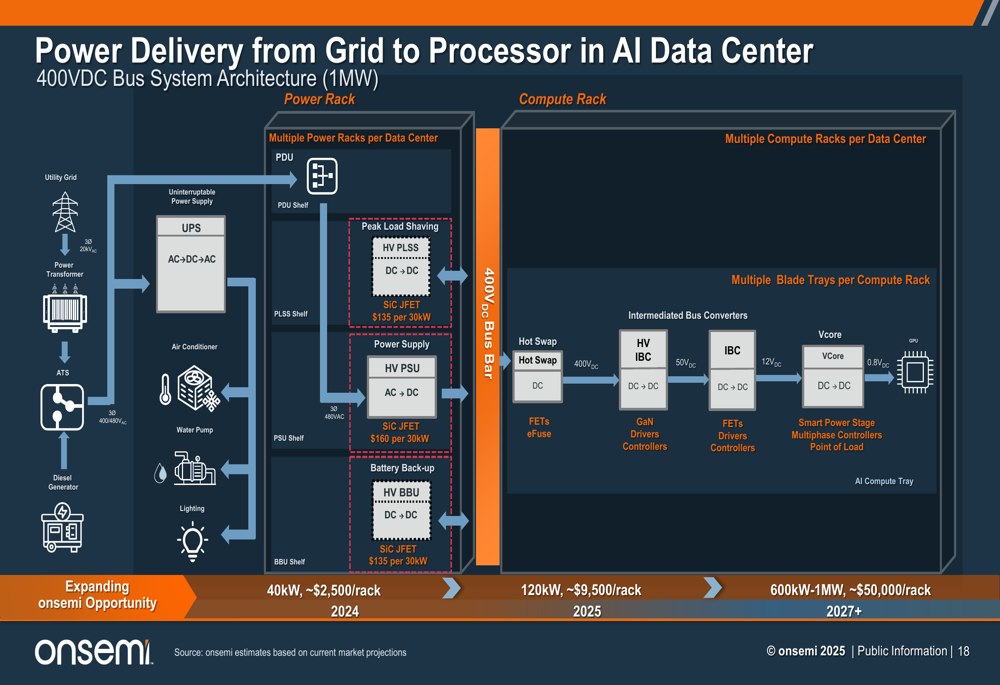

The AI Data Center segment emerged as a particular bright spot, with revenue more than doubling year-over-year. Onsemi is expanding its presence in power delivery systems for AI data centers, as shown in the following technical diagram:

The company also highlighted its diversified customer base, noting that its top 20 customers represent approximately 40% of revenue, with each purchasing around 600 products on average. Onsemi now serves over 600 silicon carbide customers, demonstrating broad market adoption of its SiC technology.

The following slide illustrates the company’s diverse customer relationships across multiple industries:

Forward-Looking Statements

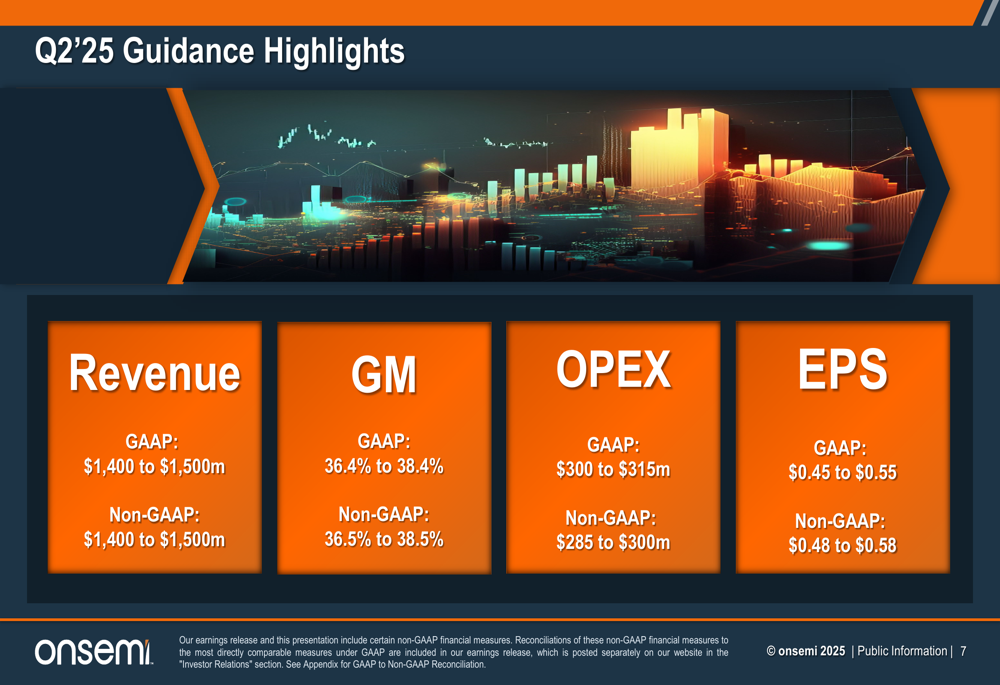

For the second quarter of 2025, Onsemi provided guidance that suggests continued challenges. The company expects Q2 revenue between $1.40 billion and $1.50 billion, with non-GAAP gross margins declining to between 36.5% and 38.5%.

The following guidance summary shows the company’s expectations for Q2 2025:

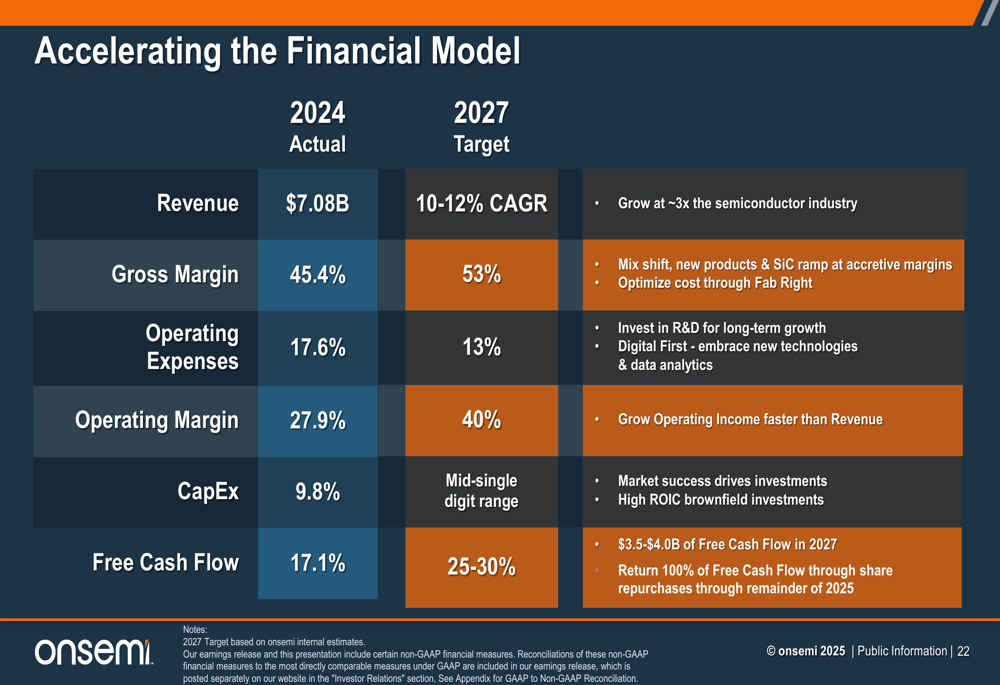

Despite near-term headwinds, Onsemi maintained an optimistic long-term outlook. The company reaffirmed its 2027 targets, including 10-12% compound annual revenue growth, 53% gross margin, 40% operating margin, and 25-30% free cash flow.

The comparison between 2024 actual results and 2027 targets demonstrates management’s confidence in the company’s long-term trajectory:

Market Context and Strategic Positioning

Onsemi’s Q1 2025 results come amid ongoing challenges in the semiconductor industry. The previous quarter’s earnings call had highlighted muted demand, particularly in North America and Europe, with ongoing inventory digestion across the supply chain.

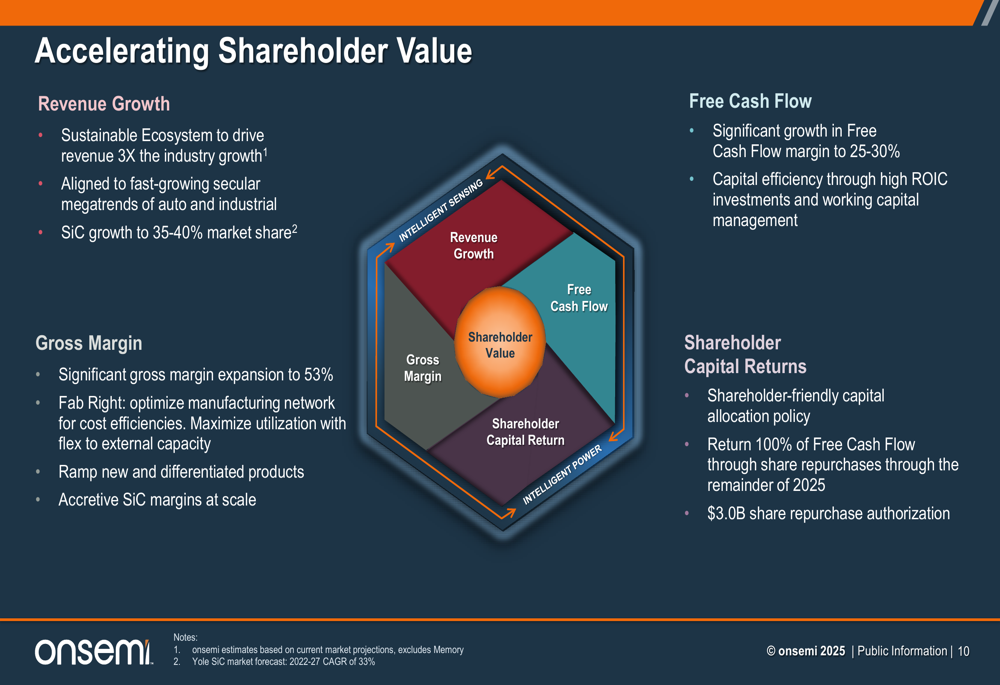

The company’s strategy focuses on accelerating shareholder value through four key pillars: revenue growth, gross margin expansion, free cash flow generation, and shareholder capital returns. Management emphasized its commitment to returning 100% of free cash flow to shareholders through its $3.0 billion share repurchase authorization.

As illustrated in the following strategic framework, these elements are designed to work together to drive long-term shareholder value:

Onsemi also highlighted its sustainability initiatives, noting that it achieved approximately 16% reduction in Scope 1 and 2 emissions versus its 2022 baseline. The company had its near-term science-based targets validated in December 2024 and maintains a goal of achieving net zero emissions by 2040.

While Onsemi faces significant near-term challenges with declining revenue and margins, its presentation emphasized resilience through the downturn and strategic positioning for long-term growth in high-value markets like silicon carbide power devices and AI data center infrastructure. Investors will be watching closely to see if the company can maintain its gross margin performance and free cash flow generation as it navigates the current industry environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.