e.l.f. Beauty stock plummets 20% as revenue and guidance fall short of expectations

Introduction & Market Context

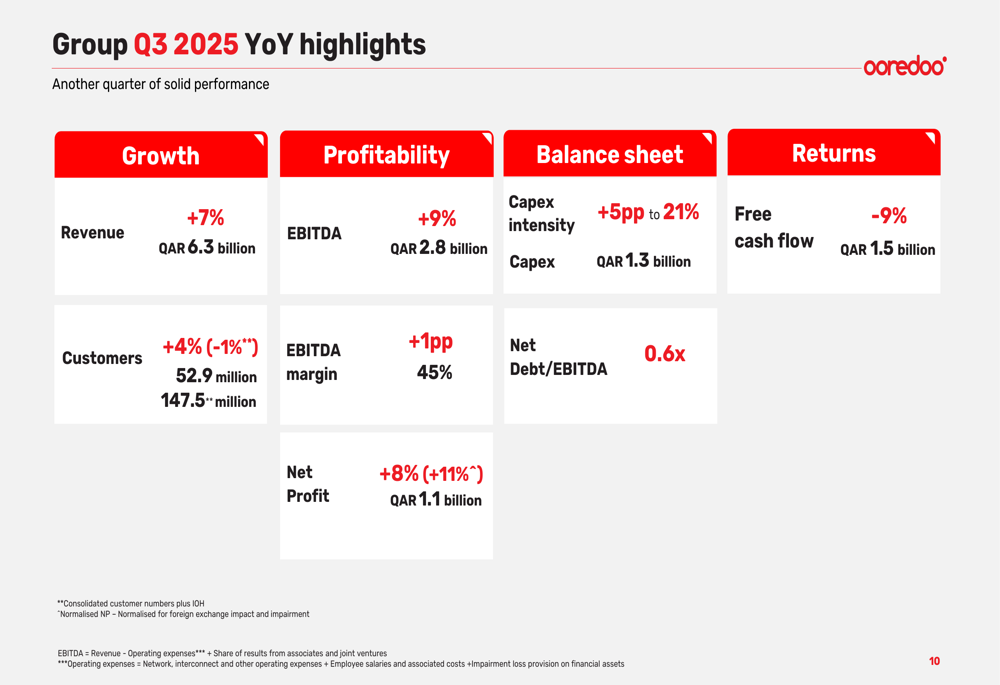

Ooredoo Group (DSM:ORDS) reported strong third-quarter results on October 30, 2025, with revenue growth accelerating to 7% year-over-year, reaching QAR 6.3 billion. The telecommunications company’s stock responded positively to the earnings announcement, rising 3.51% to close at QAR 13.55, approaching its 52-week high of QAR 14.37.

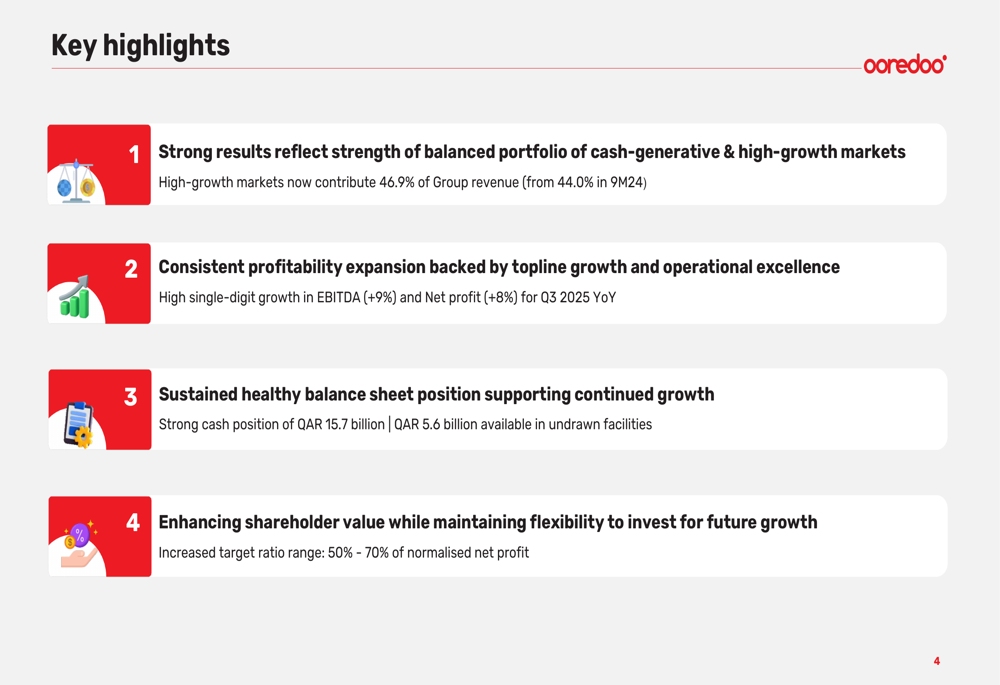

The Qatar-based telecom operator highlighted its balanced portfolio of cash-generative and high-growth markets, with high-growth markets now contributing 46.9% of Group revenue, up from 44.0% in the same period last year.

As shown in the following key highlights from the presentation, Ooredoo maintained consistent profitability expansion backed by topline growth and operational excellence:

Quarterly Performance Highlights

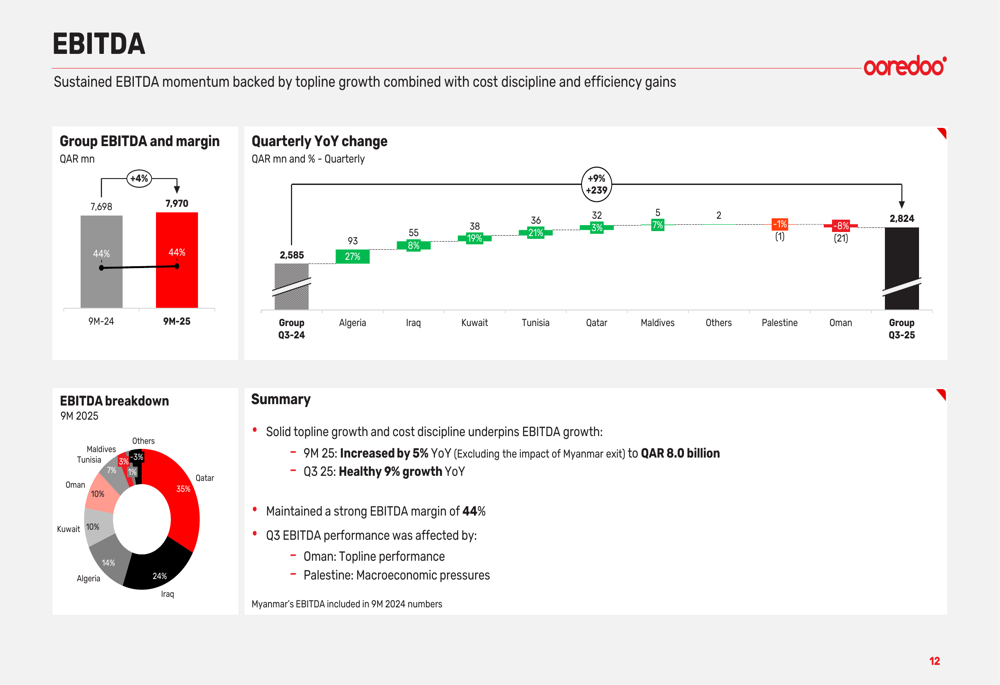

Ooredoo’s third-quarter performance showed significant improvement compared to the same period last year, with EBITDA growing 9% to QAR 2.8 billion and net profit increasing 8% to QAR 1.1 billion. The EBITDA margin improved by 1 percentage point to 45%.

For the nine-month period ended September 30, 2025, Ooredoo reported:

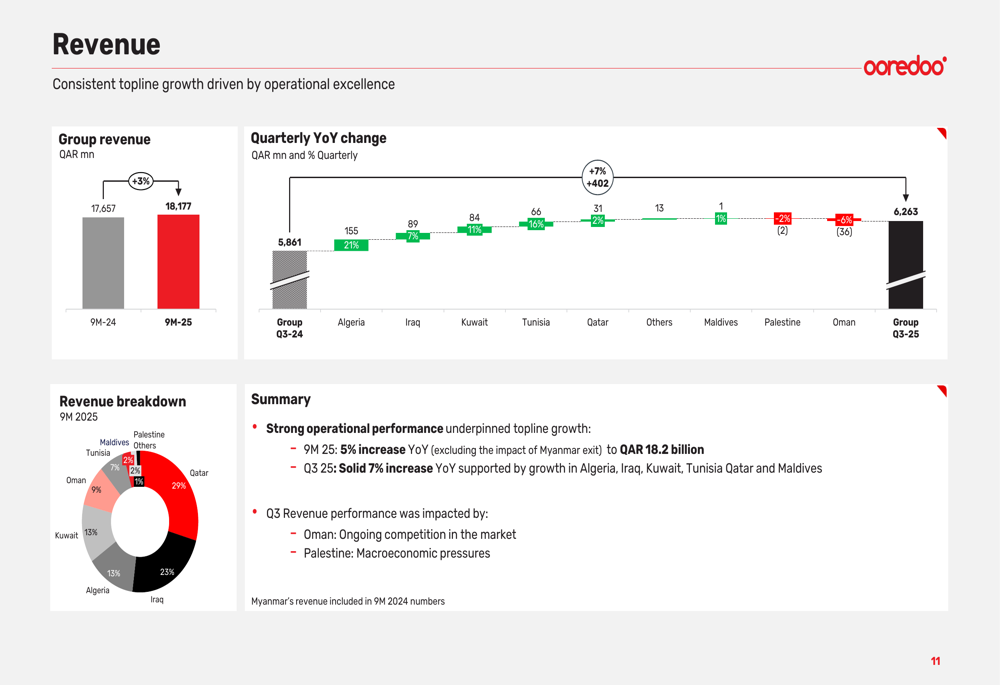

- Revenue of QAR 18.2 billion, up 3% year-over-year (5% excluding the impact of Myanmar exit)

- EBITDA of QAR 8.0 billion, up 4% (5% excluding Myanmar), with a stable margin of 44%

- Net profit of QAR 3.1 billion, up 6%

- Customer base of 52.9 million, increasing 4% year-over-year

The detailed quarterly performance metrics are illustrated in the following slide:

The company’s revenue growth was driven by strong performance in several key markets, particularly Algeria (up 16%), Iraq (up 8%), and Kuwait (up 4%). However, Oman experienced a 4% revenue decline due to ongoing competitive pressures.

The revenue breakdown by region shows Qatar remains the largest contributor at 29%, followed by Algeria at 23%, while Kuwait and Iraq each represent 13% of total revenue:

Strategic Initiatives

Ooredoo highlighted two key strategic initiatives driving future growth: data center expansion through Syntys and fintech services development.

Syntys, the group’s data center business, is accelerating the development of AI-ready, hyperscale data centers across the MENA region. For the nine months of 2025, Syntys generated QAR 115.1 million in revenue and QAR 38.0 million in EBITDA. The company currently operates 13 active data centers across three countries with 20 MW IT capacity and has 4.5 MW under construction.

Strategic partnerships with Iron Mountain (minority equity stake) and NVIDIA (cloud partner) are enhancing Syntys’s capabilities, as illustrated in the following slide:

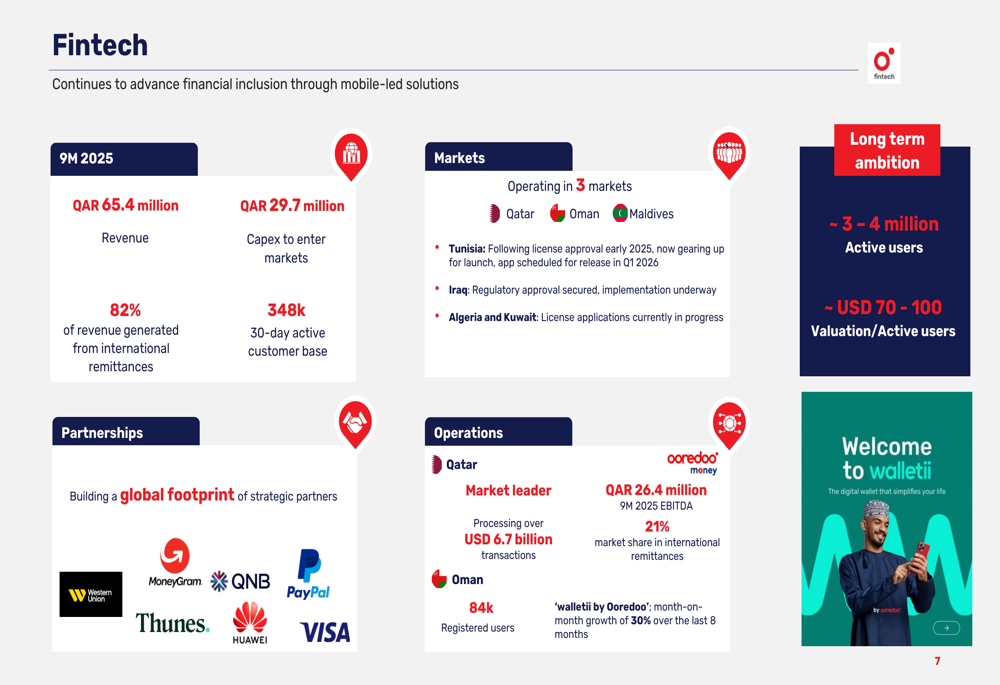

In fintech, Ooredoo reported revenue of QAR 65.4 million for 9M 2025, with 82% generated from international remittances. The company has a 30-day active customer base of 348,000 across its operating markets of Qatar, Oman, and Maldives. In Qatar, Ooredoo has established itself as a market leader with a 21% market share in international remittances, processing over USD 6.7 billion in transactions.

The company’s fintech expansion strategy includes recent regulatory approvals in Tunisia and Iraq, with license applications in progress for Algeria and Kuwait:

Regional Performance

Ooredoo’s performance varied across its operating regions:

Qatar: Revenue increased 1% year-over-year to QAR 5,335 million, with a stable EBITDA of QAR 2,799 million and a strong EBITDA margin of 52%. Normalizing for the impact of the AFC tournament in 2024 and data center carve-out, revenue grew 2% and EBITDA grew 2%.

Kuwait: Strong performance with revenue up 4% to QAR 2,421 million and EBITDA surging 27% to QAR 770 million. The EBITDA margin improved by 6 percentage points to 32%.

Iraq: Revenue grew 8% to QAR 4,141 million, with EBITDA up 5% to QAR 1,920 million. The customer base increased 6% to 19.8 million. Capex more than doubled (+113%) to QAR 885 million as the company invested in network expansion.

Algeria: Impressive performance with revenue up 16% to QAR 2,437 million and EBITDA up 23% to QAR 1,119 million. The EBITDA margin improved by 3 percentage points to 46%.

Oman: Faced competitive challenges with revenue declining 4% to QAR 1,721 million and EBITDA down 7% to QAR 769 million. However, the company maintained a resilient EBITDA margin of 45%.

The EBITDA breakdown by region shows Qatar as the largest contributor at 35%, followed by Iraq and Algeria each at 24%:

Balance Sheet & Shareholder Returns

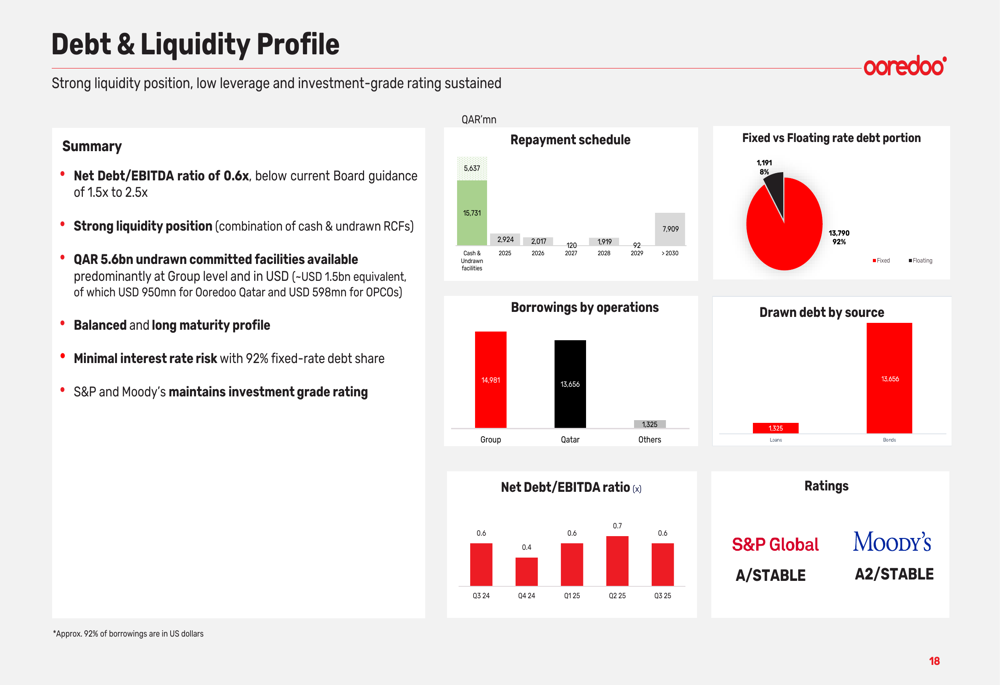

Ooredoo maintained a strong balance sheet position with a Net Debt/EBITDA ratio of 0.6x, well below the current Board guidance of 1.5x to 2.5x. The company has a strong liquidity position with QAR 15.7 billion in cash and QAR 5.6 billion in undrawn facilities.

The debt profile is well-managed with 92% fixed-rate debt, minimizing interest rate risk:

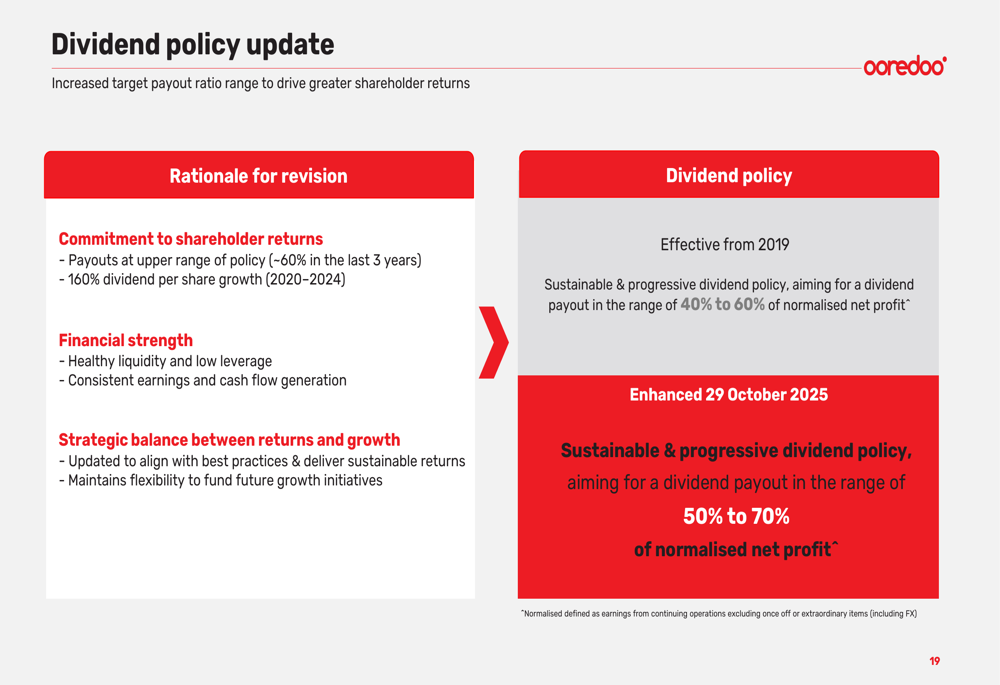

In a significant development for shareholders, Ooredoo announced an enhancement to its dividend policy, increasing the target payout ratio range from 40-60% to 50-70% of normalized net profit. This update reflects the company’s financial strength and commitment to shareholder returns, having delivered 160% dividend per share growth between 2020 and 2024:

Forward-Looking Statements

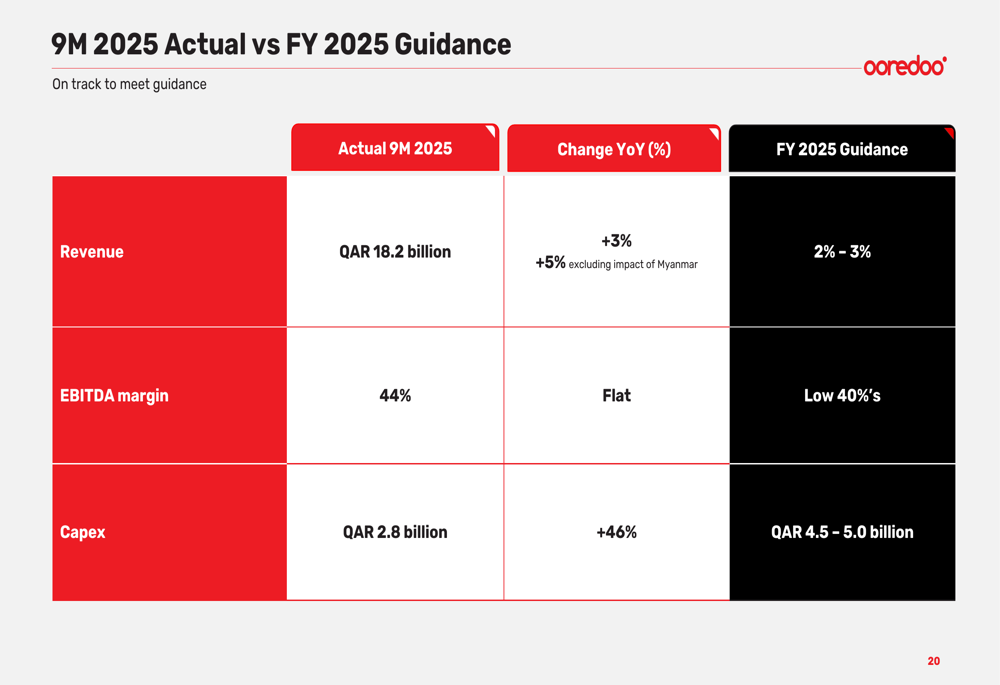

Ooredoo’s performance for the first nine months of 2025 is tracking ahead of its full-year guidance. The company had projected 2-3% revenue growth for FY 2025, while actual 9M 2025 revenue growth stands at 3% (5% excluding Myanmar). Similarly, the EBITDA margin of 44% is at the higher end of the guided "low 40’s" range.

The company plans to invest between QAR 4.5-5.0 billion in capex for the full year, having spent QAR 2.8 billion in the first nine months:

Group CEO Aziz Aluthman Fakhroo emphasized the company’s focus on profitability and strategic priorities, stating, "We remain committed to driving strong and sustainable profitability while advancing our strategic priorities."

Looking ahead, Ooredoo has scheduled a Capital Markets Day on November 3rd to outline strategic priorities and future growth plans, which will provide investors with more insights into the company’s long-term strategy and objectives.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.