United Homes Group stock plunges after Nikki Haley, directors resign

Introduction & Market Context

Openlane Inc. (NYSE:KAR) released its second quarter 2025 earnings presentation on August 6, showing robust financial performance across key metrics and prompting management to raise its full-year guidance. The digital automotive marketplace operator continues to benefit from its dual-segment business model connecting vehicle buyers and sellers.

The company’s stock responded positively to the results, trading up 3.91% in premarket at $26.02, building on its previous close of $25.04. This marks a significant recovery from its 52-week low of $15.44 and approaches its 52-week high of $26.04.

In a letter to stockholders included in the presentation, CEO Peter Kelly highlighted the company’s strategic investments and increasing market recognition of the Openlane brand as key drivers of growth.

Quarterly Performance Highlights

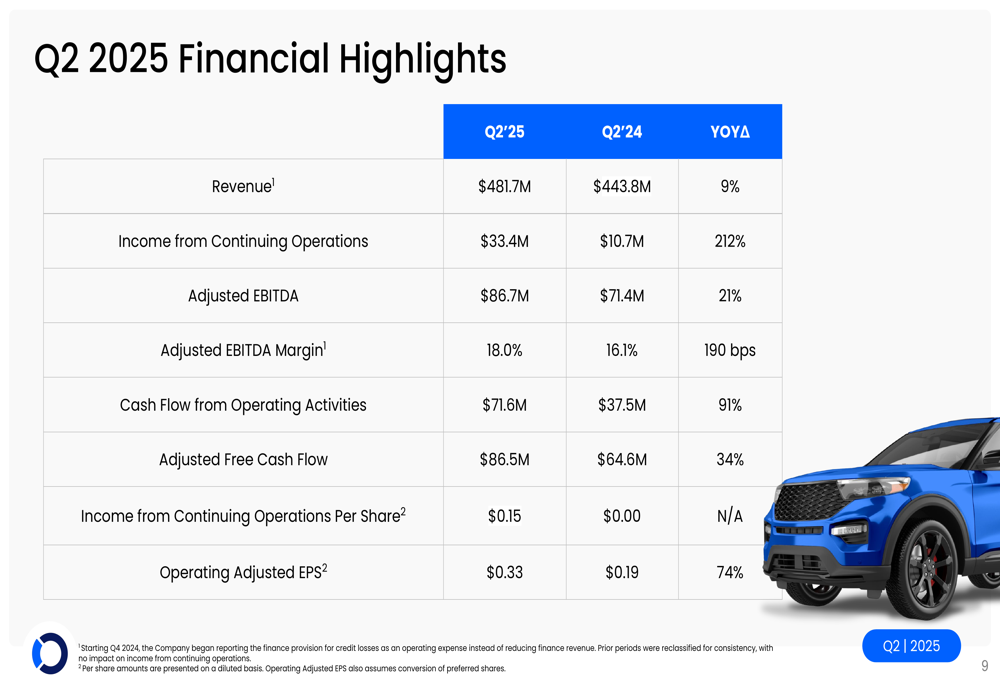

Openlane reported impressive financial results for Q2 2025, with consolidated revenue reaching $481.7 million, a 9% increase compared to the same period last year. More notably, income from continuing operations surged 212% year-over-year to $33.4 million.

The company’s profitability metrics showed substantial improvement, with adjusted EBITDA of $86.7 million representing a 21% year-over-year increase, while adjusted EBITDA margin expanded by 190 basis points to reach 18.0%.

As shown in the following financial highlights chart:

Cash generation also strengthened considerably, with cash flow from operating activities increasing 91% to $71.6 million and adjusted free cash flow rising 34% to $86.5 million. Operating adjusted earnings per share grew 74% to $0.33, compared to $0.19 in Q2 2024.

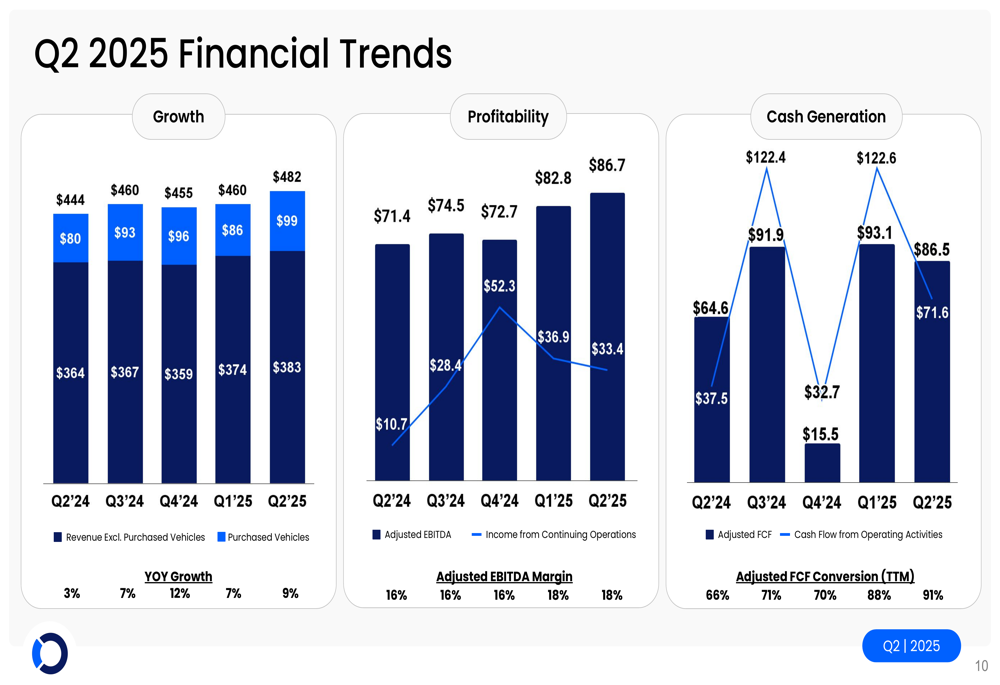

The quarterly financial trends illustrate consistent improvement across growth, profitability, and cash generation metrics:

Segment Performance

Openlane operates through two complementary business segments: the Marketplace segment (Openlane) and the Finance segment (AFC). Both segments contributed to the company’s strong quarterly performance.

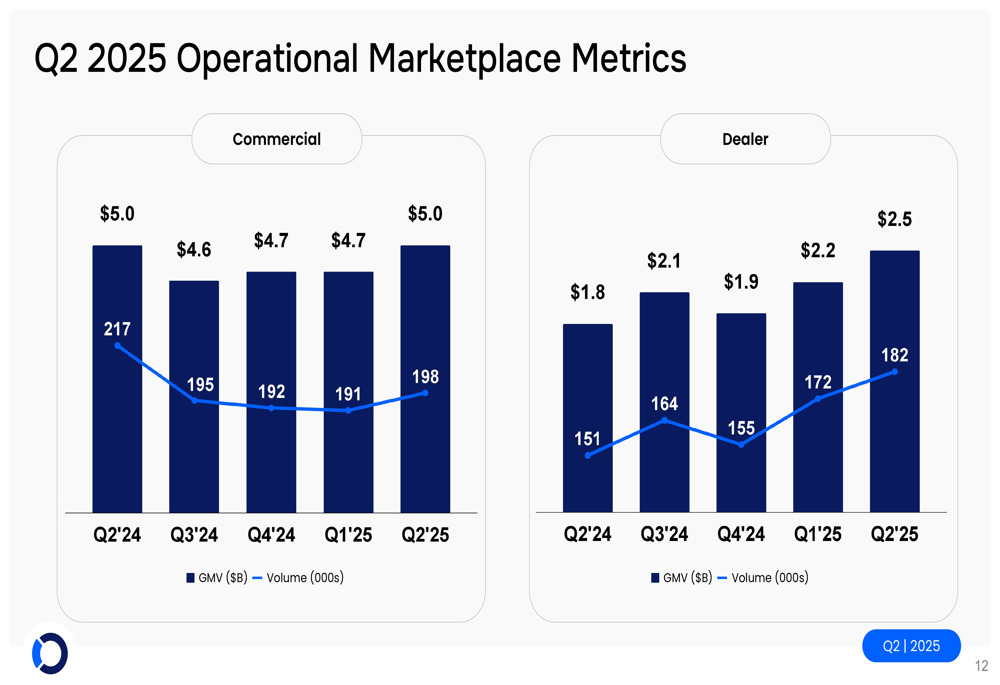

The Marketplace segment, which connects automotive manufacturers, dealers, rental companies, and fleet operators through a digital platform, showed solid growth. Commercial segment gross merchandise value (GMV) increased to $5.0 billion with 198,000 vehicles sold, while the Dealer segment saw more substantial growth with GMV rising to $2.5 billion and volume reaching 182,000 vehicles.

The operational metrics for the Marketplace segment demonstrate this growth trajectory:

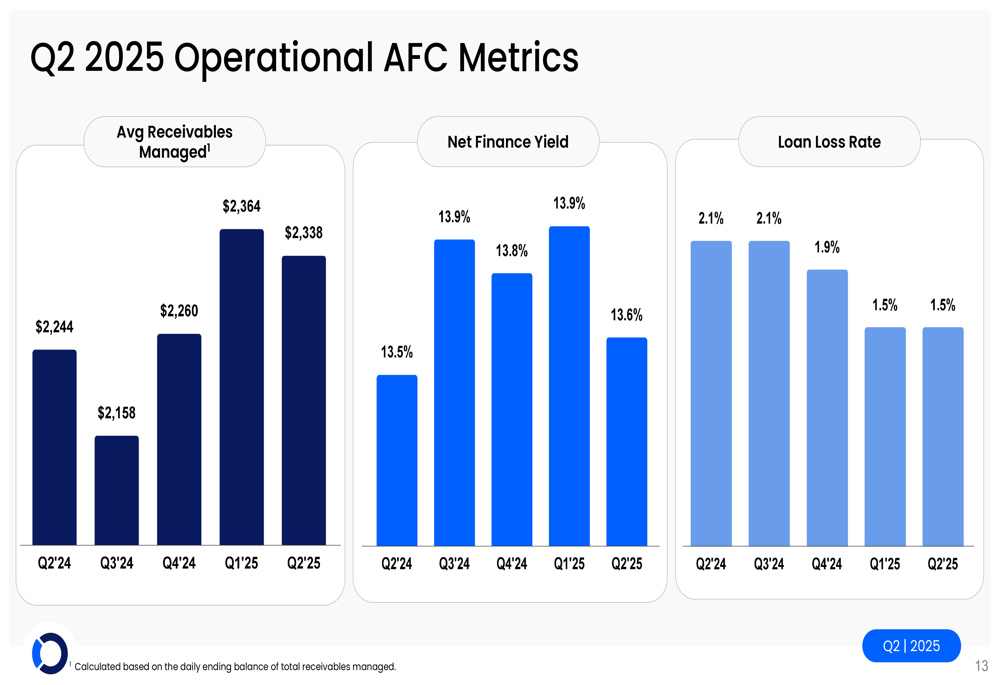

The Finance segment, operated through Automotive Finance Corporation (AFC), provides floorplan financing to independent dealers. This segment reported average managed receivables of $2,338 million, with a net finance yield between 13.5% and 13.9%, while maintaining a controlled loan loss rate between 1.5% and 2.1%.

The following chart details the operational metrics for the AFC segment:

The company emphasized the synergistic relationship between its two segments, with dealer recruitment, bundled products and services, and dealer credit driving transactions across both platforms. This integration allows Openlane to capture more value from each customer relationship while generating cash for continued innovation.

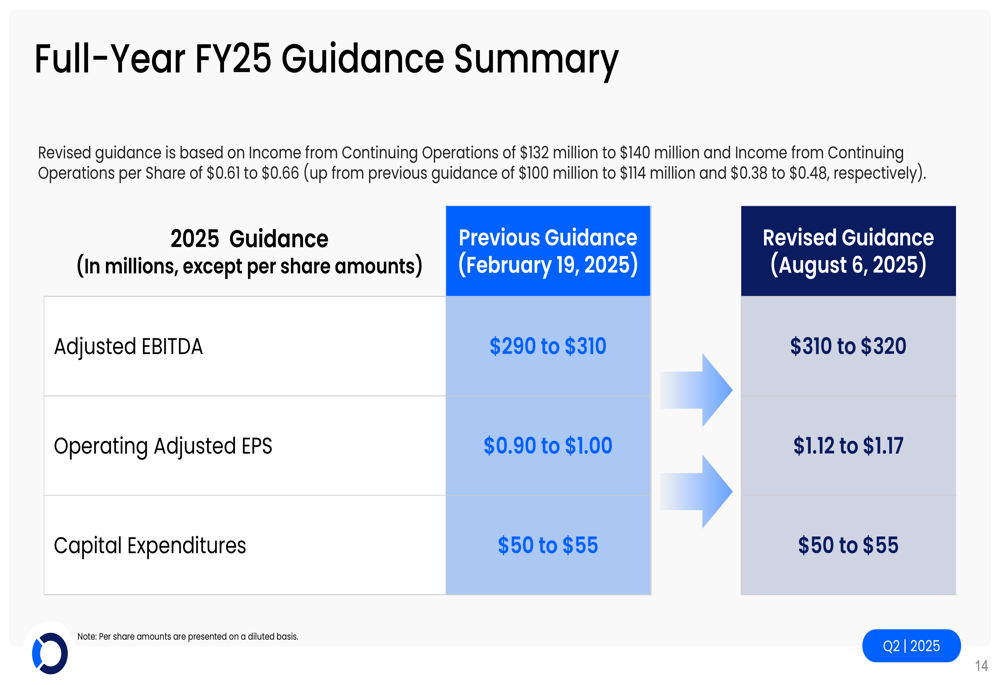

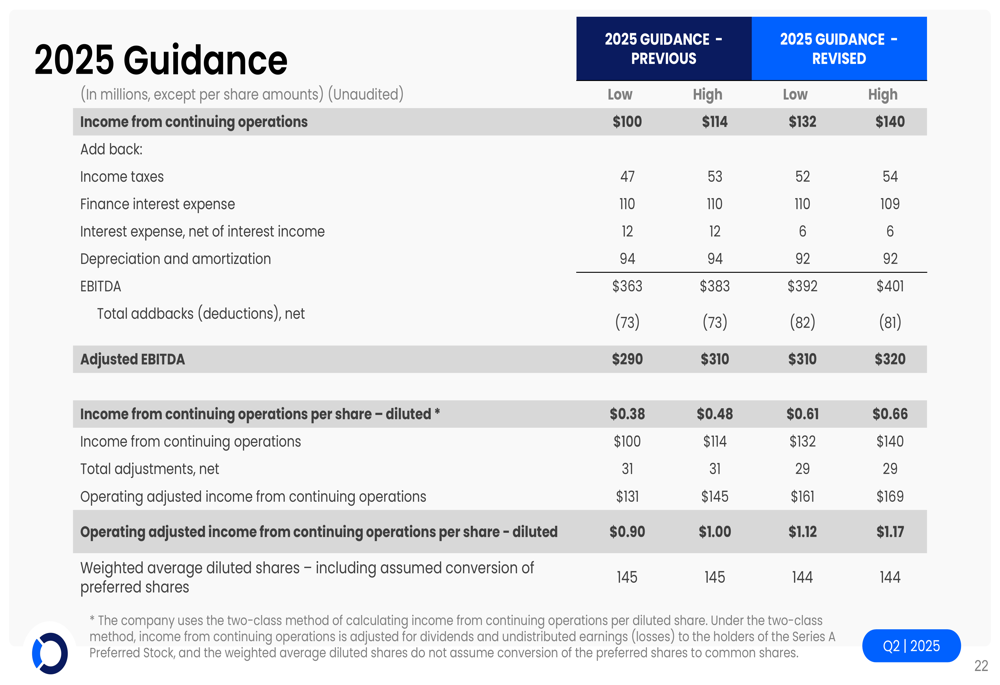

Revised Guidance and Outlook

Based on the strong first-half performance, Openlane raised its full-year 2025 guidance. The company now expects adjusted EBITDA of $310-$320 million, up from the previous guidance of $290-$310 million provided in February. Operating adjusted EPS guidance was also increased significantly from $0.90-$1.00 to $1.12-$1.17, while capital expenditure guidance remained unchanged at $50-$55 million.

The revised guidance is illustrated in the following chart:

The detailed breakdown of the 2025 guidance shows income from continuing operations is now projected at $132-$140 million, up from the previous $100-$114 million, with corresponding adjustments to income taxes and other financial metrics:

In the presentation, management noted that despite potential tariff headwinds, the company remains confident in its ability to deliver on the improved outlook. This confidence stems from the continued strength in both business segments and the company’s ability to leverage its digital marketplace and financing capabilities.

Market Reaction and Analyst Perspectives

The market’s initial reaction to Openlane’s Q2 results appears positive, with the stock trading up 3.91% in premarket. This contrasts with the reaction to Q1 results, when the stock dipped slightly despite beating earnings expectations.

The Q2 performance builds on the momentum established in Q1 2025, when the company reported an EPS of $0.31 (exceeding forecasts of $0.22) and revenue of $460 million. The consecutive quarters of strong performance suggest Openlane is executing effectively on its strategic initiatives.

Prior to the Q2 results, analysts maintained a moderate buy consensus on Openlane with price targets ranging from $20 to $26. The company’s current trading level near the top of that range, combined with the raised guidance, may prompt analysts to revisit their valuations and price targets.

The company’s new $250 million share repurchase authorization announced during the Q1 earnings call, valid through 2026, provides additional support for the stock as management demonstrates confidence in Openlane’s long-term value proposition and cash generation capabilities.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.