Moody’s upgrades Agnico Eagle’s rating to A3 on debt reduction

Introduction & Market Context

Orion Energy Systems Inc . (NASDAQ:OESX), a provider of LED lighting, maintenance services, and EV charging solutions, recently reported its Q1 fiscal 2026 earnings, beating EPS expectations despite revenue shortfalls. The company’s stock surged 24.56% following the announcement, reflecting investor optimism about its improving profitability metrics despite ongoing revenue challenges.

The company’s August 2025 presentation highlights its three-segment business strategy amid a growing market for energy-efficient lighting solutions and EV infrastructure. According to the presentation, the global LED lighting market is projected to grow from approximately $20 billion in 2020 to over $50 billion by 2030, representing a 10.2% CAGR.

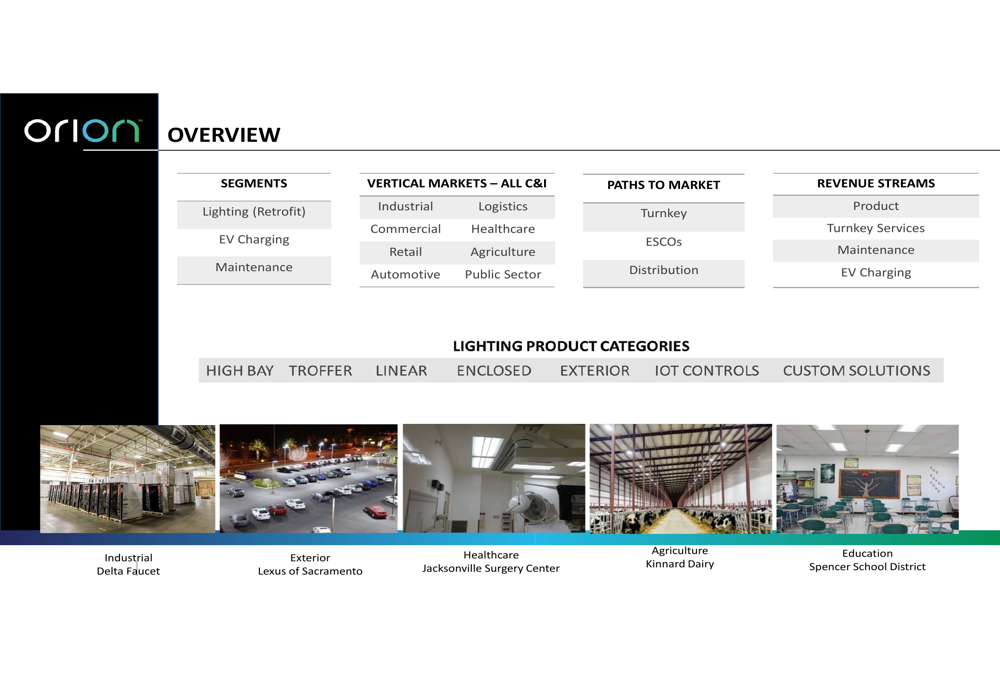

As shown in the following overview of Orion’s business segments, markets, and revenue streams:

Executive Summary

Orion Energy Systems operates across three primary business segments: LED Lighting & Controls, Lighting Maintenance, and EV Charging. Led by CEO Sally Washlow, CFO Per Brodin, and President & COO Scott Green, the company positions itself as a comprehensive solution provider for energy efficiency and sustainability initiatives.

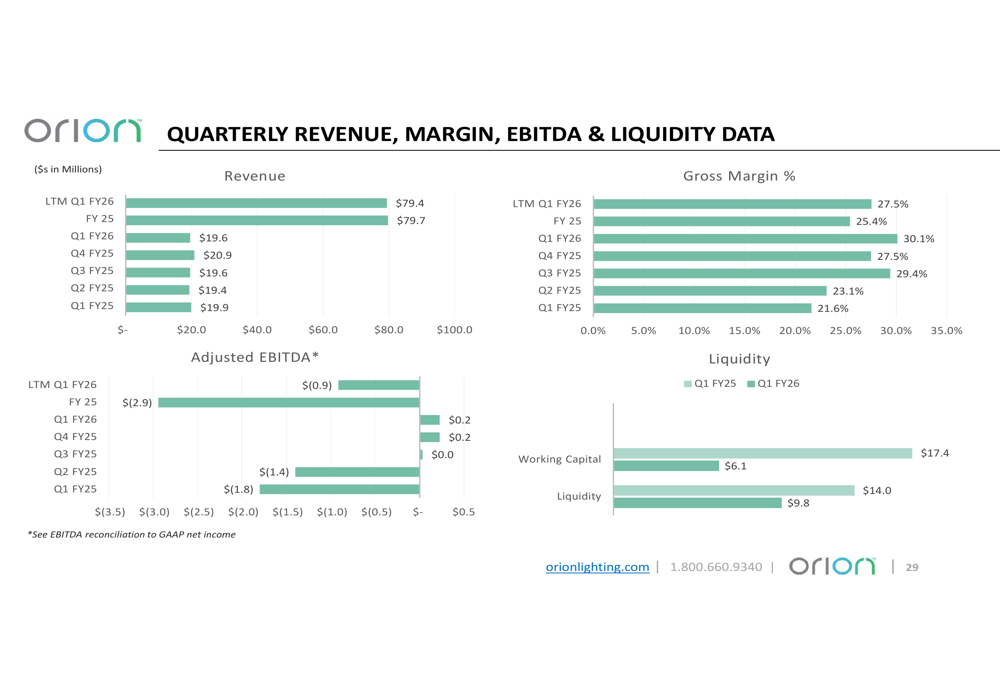

The company’s Q1 FY2026 results showed an EPS of -$0.04, surpassing the forecasted -$0.06, while revenue came in at $19.6 million against expectations of $21.22 million. Despite the revenue miss, Orion demonstrated significant improvement in profitability metrics, with gross margin increasing to 30.1% from 21.6% year-over-year and adjusted EBITDA turning positive at $200,000 compared to a negative $1.8 million in the prior year.

Business Strategy

Orion’s business strategy centers on its three core segments, with a strong emphasis on cross-selling opportunities. The company has completed over 25,000 lighting projects, provides maintenance services at more than 8,000 customer locations throughout the US and Caribbean, and is expanding its EV charging capabilities following the October 2022 acquisition of Voltrek.

The company maintains a 266,000 square foot manufacturing facility in Manitowoc, Wisconsin, which provides advantages in lead times (10-15 business days) and compliance with Buy American Act (BAA) and Build America, Buy America Act (BABA) regulations. This positioning is particularly advantageous for securing government contracts and projects with federal funding.

Orion boasts an impressive client roster across all three business segments, as evidenced by their lighting customer base:

Similarly, the company has established strong relationships in the maintenance sector with major retail brands:

Following its acquisition of Voltrek, Orion has expanded into the EV charging market with notable institutional clients:

Financial Performance

While Orion’s presentation emphasizes growth opportunities, the company’s recent financial performance reveals both challenges and improvements. Revenue for Q1 FY2026 slightly declined to $19.6 million from $19.9 million in the same quarter last year, but profitability metrics showed substantial improvement.

The company’s quarterly financial data shows the trajectory of revenue, margins, EBITDA, and liquidity:

Notably, Orion’s gross profit margin increased significantly to 30.1% in Q1 FY2026, up from 21.6% in the prior year period. This improvement reflects enhanced operational efficiency and cost management strategies. The company also reduced its net loss to $1.2 million from $3.8 million year-over-year, demonstrating progress toward profitability.

Growth Opportunities

Orion identifies several growth drivers in its presentation, particularly in the EV charging segment. The National Renewable Energy Laboratory (NREL) estimates that by 2030, the U.S. will need 28 million EV charging ports to support an anticipated 33 million electric vehicles, representing a substantial market opportunity.

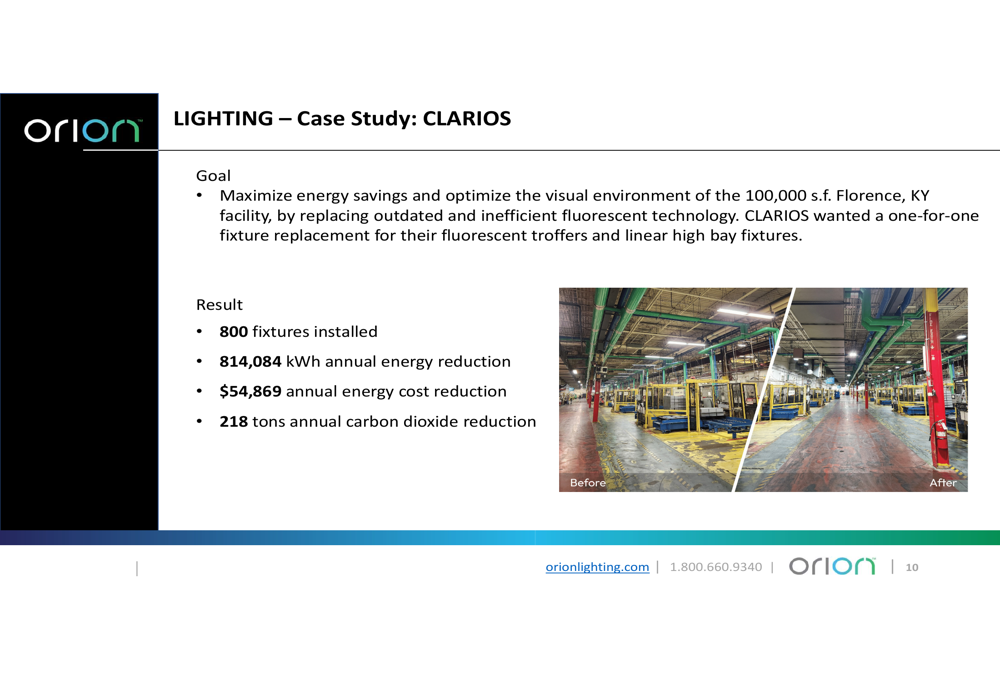

The company’s case studies highlight the tangible benefits of its solutions. For instance, a lighting project for Clarios resulted in significant energy and cost savings:

In the EV charging segment, Orion is positioning itself to capitalize on fleet electrification trends, particularly for Level 3 DC fast charging installations. The company has partnerships with leading equipment suppliers including ChargePoint (NYSE:CHPT) and ABB (ST:ABB), enhancing its competitive position in this growing market.

Challenges and Outlook

Despite the positive narrative in its presentation, Orion faces several challenges. The company’s revenue has declined by 11.99% over the last twelve months according to InvestingPro data, and its stock has traded near 52-week lows despite recent gains. The EV charging market, while promising, faces funding uncertainties that could impact growth projections.

Nevertheless, Orion maintains its revenue target of $84 million for FY2026, projecting 5% growth over the fiscal year. The company expects to achieve positive adjusted EBITDA for the full fiscal year, continuing the improvement trend seen in Q1.

CEO Sally Washlow expressed confidence during the earnings call, stating, "We see no better growth opportunity in this sector than Orion," while CFO Per Brodin added, "We expect our overall gross margin to remain strong in FY2026," underscoring the company’s focus on maintaining profitability despite revenue challenges.

As Orion continues to execute its three-segment strategy, investors will be watching closely to see if the company can translate its operational improvements and diverse business model into sustained revenue growth and consistent profitability.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.