Here’s why Citi says crypto prices have been weak recently

Introduction & Market Context

Orla Mining Ltd (TSX:OLA) delivered a record gold production quarter in Q1 2025, according to the company’s latest corporate presentation. The multi-asset gold producer reported significant operational growth following the completion of its Musselwhite mine acquisition, though financial results were impacted by one-time costs associated with the transaction.

The company’s shares have performed strongly in 2025, with the stock price reaching $15.48 as of May 9, 2025, representing a 4.03% increase and approaching its 52-week high of $16.53. This performance reflects investor optimism about Orla’s expanded production profile and growth strategy across its North American portfolio.

Quarterly Performance Highlights

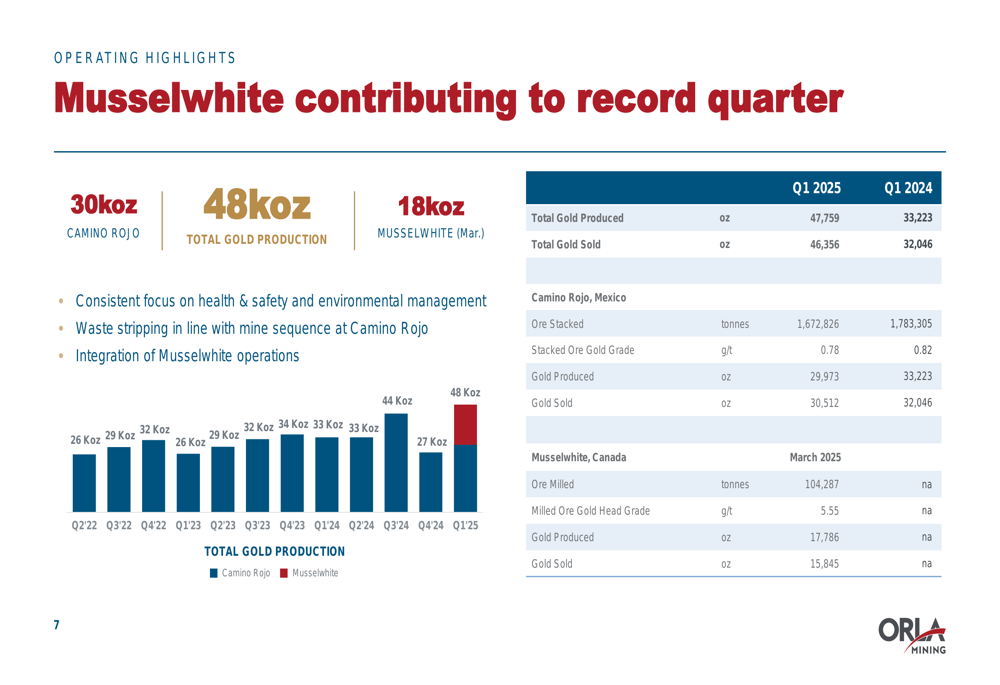

Orla Mining achieved total gold production of 47,759 ounces in Q1 2025, representing a 44% increase compared to 33,223 ounces in Q1 2024. This growth was driven by the addition of the Musselwhite mine in Canada, which contributed 17,786 ounces, while the company’s Camino Rojo operation in Mexico produced 29,973 ounces.

As shown in the following production chart:

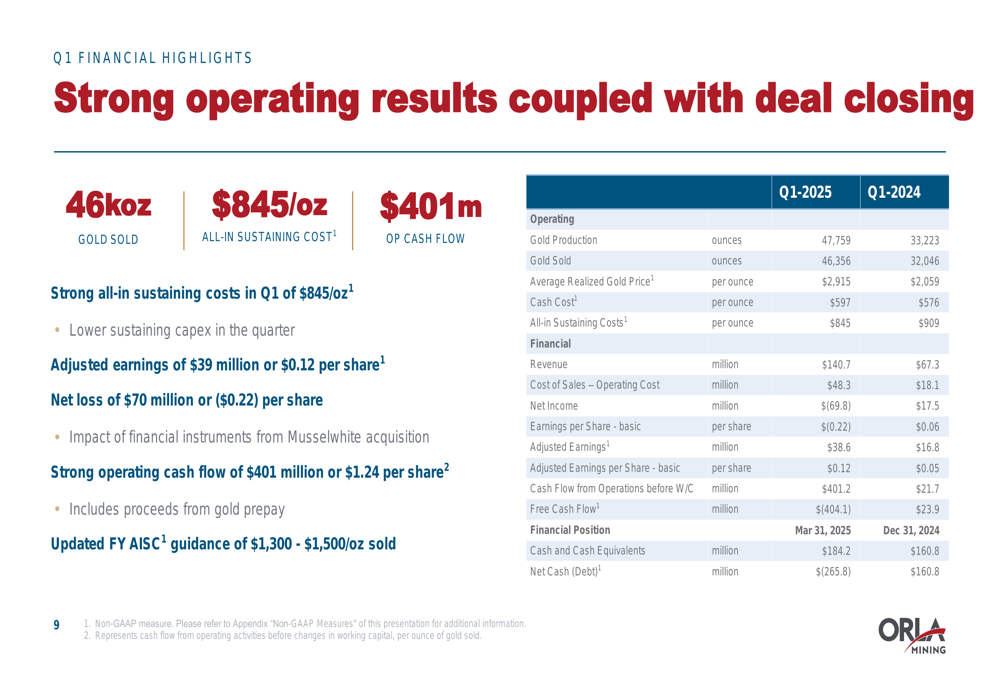

The company sold 46,356 ounces of gold during the quarter at an average realized price of $2,915 per ounce, generating revenue of $140.7 million. All-in sustaining costs (AISC) were reported at $845 per ounce, demonstrating strong cost control despite the integration of a new asset.

Detailed Financial Analysis

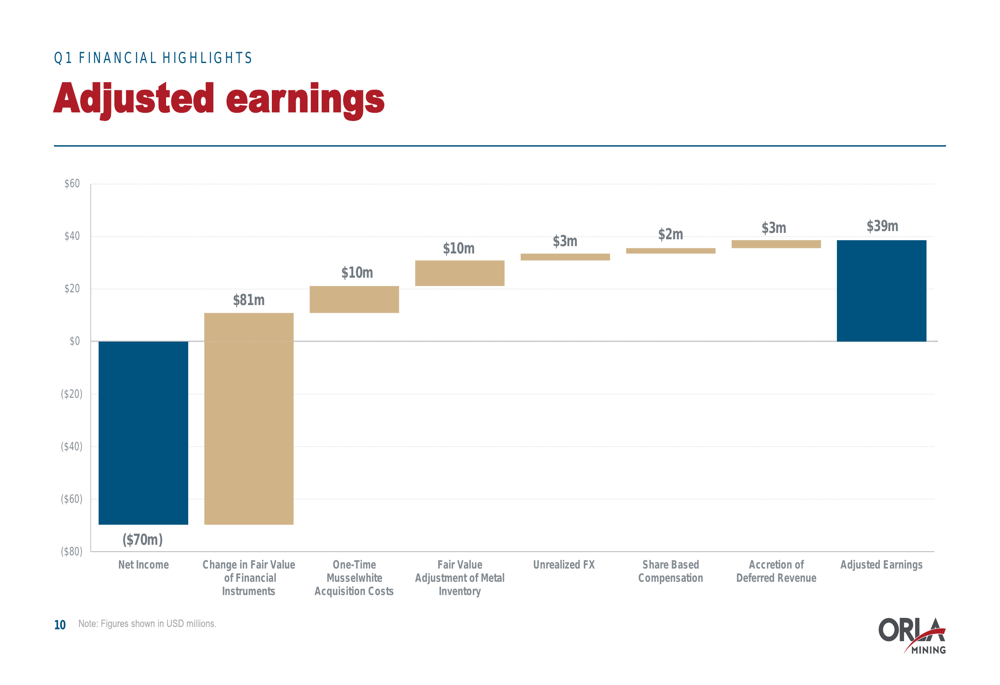

Despite strong operational performance, Orla reported a net loss of $69.8 million ($0.22 per share) for Q1 2025. However, after adjusting for acquisition-related items, the company posted adjusted earnings of $38.6 million ($0.12 per share). Operating cash flow before working capital changes was robust at $401.2 million, though free cash flow was negative at $404.1 million due to acquisition costs.

The following financial summary highlights key metrics from the quarter:

The significant difference between reported net income and adjusted earnings is primarily due to one-time costs and fair value adjustments related to the Musselwhite acquisition. The company provided a detailed breakdown of these adjustments:

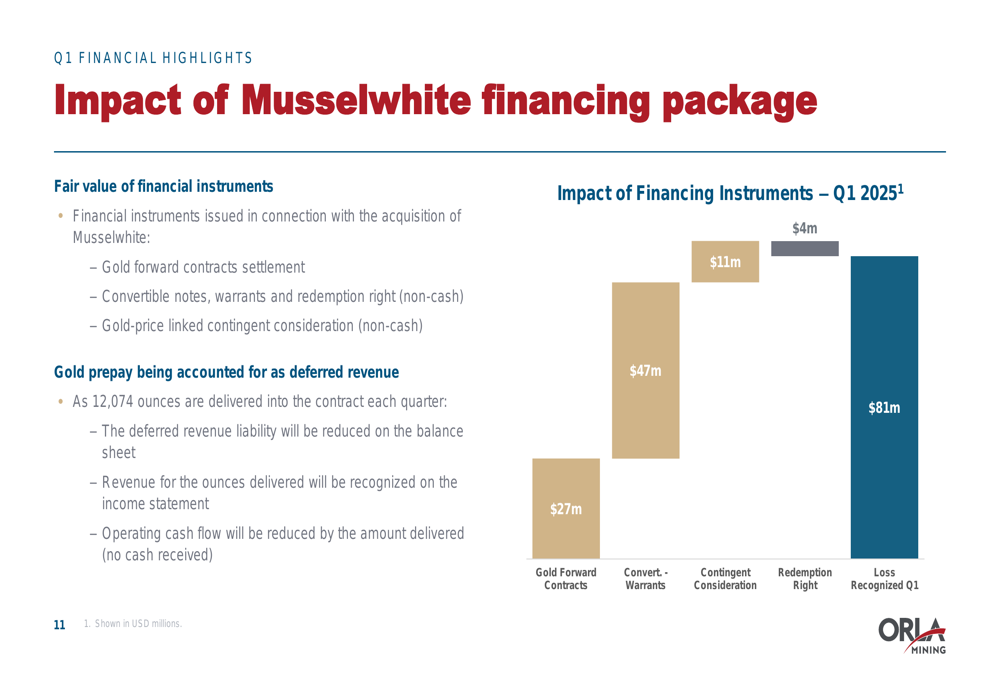

The Musselwhite financing package had a substantial impact on Q1 results, with an $81 million loss recognized from various financial instruments issued in connection with the acquisition:

Strategic Initiatives

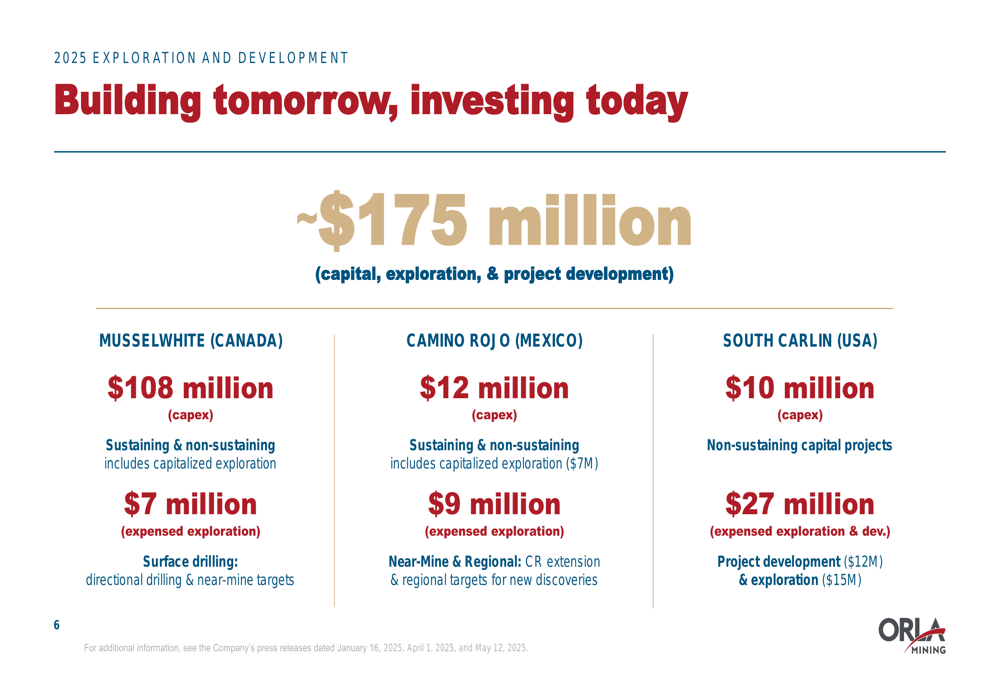

Orla Mining has outlined an ambitious exploration and development program for 2025, with approximately $175 million allocated across its portfolio. This investment is divided between the Musselwhite mine in Canada ($115 million), Camino Rojo in Mexico ($21 million), and the South Carlin Complex in the USA ($37 million).

The following breakdown illustrates the company’s capital allocation strategy:

At Musselwhite, the company plans to reactivate exploration with 55,000 meters of drilling and a $25 million budget. Key objectives include expanding reserves and resources, defining extensions of the deposit, and discovering near-mine mineralization with open-pit potential.

For Camino Rojo, Orla expects to release an initial underground sulphide resource estimate in Q2 2025, which will include portions of the Zone 22 discovery. The company is advancing a 15,000-meter infill drilling program to build upon the initial resource.

The South Railroad project in Nevada is progressing through permitting, with a Notice of Intent expected by mid-2025 and a Record of Decision targeted for mid-2026, followed by construction.

Forward-Looking Statements

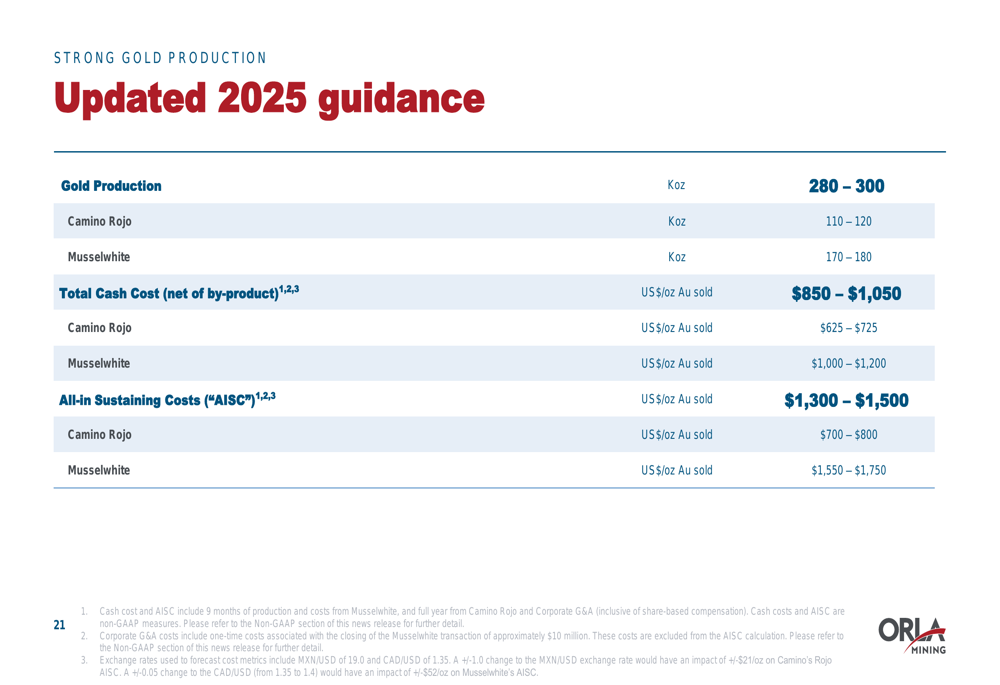

Orla Mining has updated its guidance for 2025, projecting total gold production of 280,000-300,000 ounces with all-in sustaining costs of $1,300-$1,500 per ounce. This represents a significant increase from previous production levels, driven by the full-year contribution from Musselwhite.

The detailed production and cost guidance by asset is shown below:

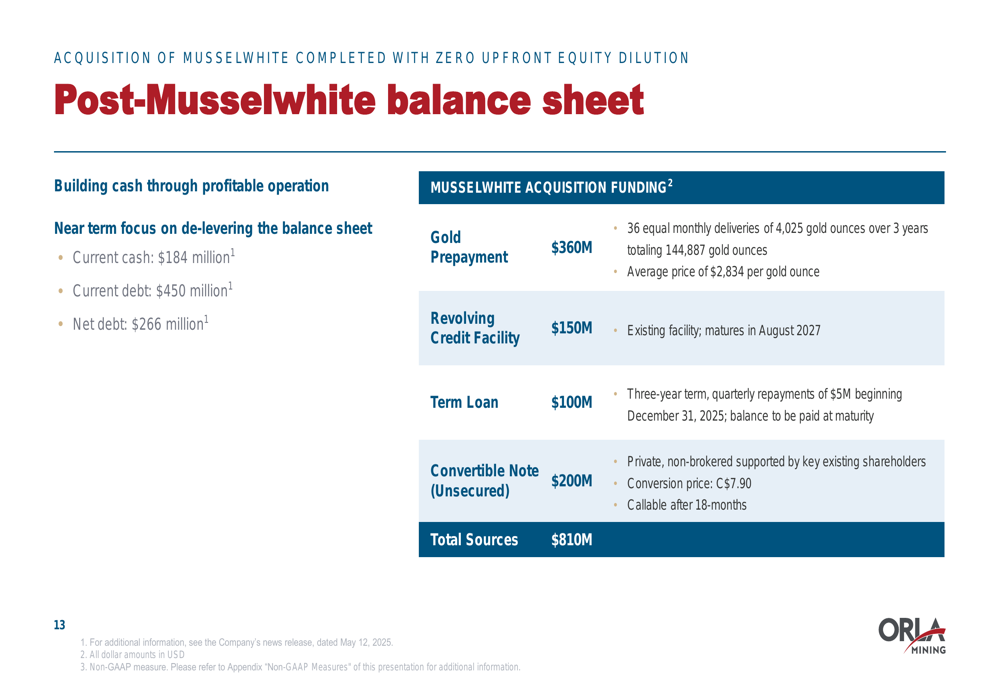

Following the Musselwhite acquisition, Orla’s balance sheet now shows $184 million in cash and $450 million in debt, resulting in a net debt position of $266 million. Management has indicated that deleveraging the balance sheet is a near-term priority, alongside continuing to build cash through profitable operations.

The company’s funding structure includes:

Competitive Industry Position

With the addition of Musselwhite, Orla Mining has transformed into a mid-tier gold producer with a diversified asset base across North America. The company now operates two producing mines (Camino Rojo and Musselwhite) with a third development project (South Railroad) advancing toward construction.

The company has identified several catalysts for 2025, including the completion of Musselwhite integration, resource updates at both South Railroad and Camino Rojo Sulphides, permitting milestones in Mexico and Nevada, and study work for the Camino Rojo underground project.

Orla’s strategy focuses on creating value through proven operational expertise, quality partners, and high-potential projects across politically stable jurisdictions in North America. This approach positions the company competitively within the mid-tier gold producer segment, with significant organic growth potential from its existing asset portfolio.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.