Microvast Holdings announces departure of chief financial officer

Orthofix Medical (TASE:BLWV) Inc (NASDAQ:OFIX) presented its first quarter 2025 earnings results on May 6, highlighting revenue growth across all business segments and improved profitability metrics, despite a significant premarket stock decline of nearly 24%.

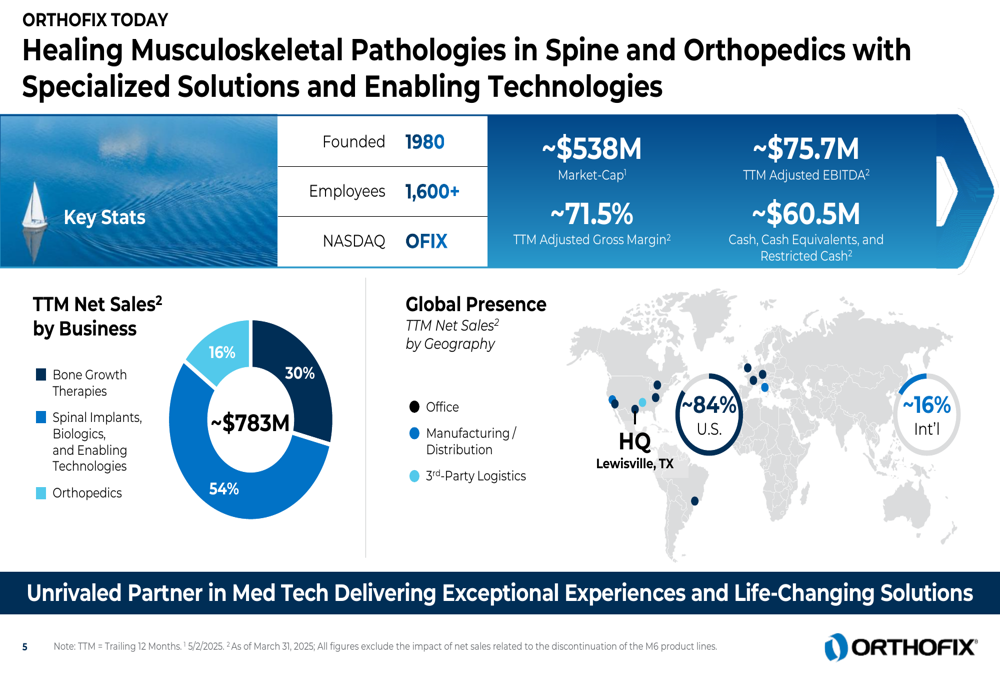

Executive Summary

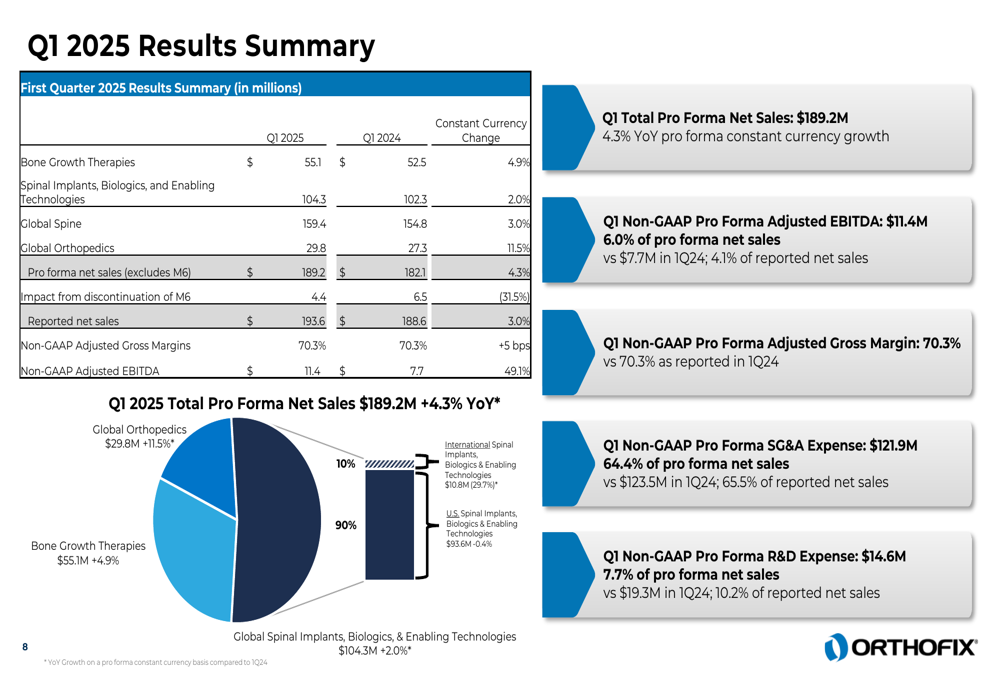

Orthofix reported pro forma net sales of $189.2 million for Q1 2025, representing 6% growth year-over-year on a same sales day constant currency basis. The company achieved non-GAAP pro forma adjusted EBITDA of $11.4 million, a $3.8 million increase from the prior year, with margin expansion of approximately 200 basis points.

"We are focused on three strategic priorities to drive market share gains in our spine business and build a fast-growing orthopedics business specifically focused on limb reconstruction," said Massimo Calafiore, President and Chief Executive Officer, in the presentation.

As shown in the following comprehensive financial highlights, the company saw growth across all its major segments:

Despite these positive results, Orthofix’s stock dropped significantly in premarket trading, with shares down 23.86% to $10.31, suggesting investors may have had higher expectations or concerns about other aspects of the company’s performance.

Quarterly Performance Highlights

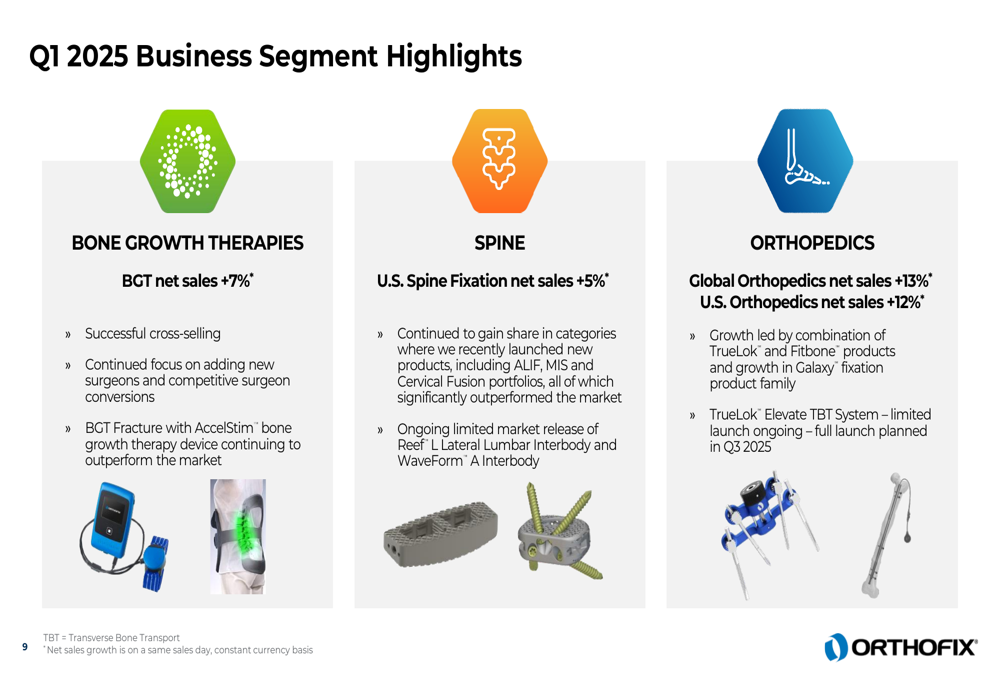

Orthofix’s growth was led by its U.S. Orthopedics business, which achieved 10% year-over-year net sales growth (12% on a same sales day basis). The Bone Growth Therapies segment saw 5% growth (7% on a same sales day basis), while U.S. Spine Fixation grew by 4% (5% on a same sales day basis).

The company maintained its gross margin at 70.3%, unchanged from Q1 2024, while reducing both SG&A and R&D expenses as a percentage of sales. Free cash flow remained negative at $(25.1) million but showed continued year-over-year improvement.

The following chart provides a detailed breakdown of Q1 2025 results by business segment:

The company’s business segment highlights reveal specific growth drivers across its portfolio:

This performance builds on momentum from the previous quarter. In Q3 2024, Orthofix had reported a 7% year-over-year increase in net sales, with particularly strong performance in U.S. spine fixation (18% growth) and U.S. Orthopedics (15% growth).

Strategic Initiatives

Orthofix continues to position itself as a comprehensive provider of solutions across spine, orthopedics, and enabling technologies. The company is leveraging its competitive advantages to drive growth and market share gains.

The following slide outlines the company’s clear competitive advantages:

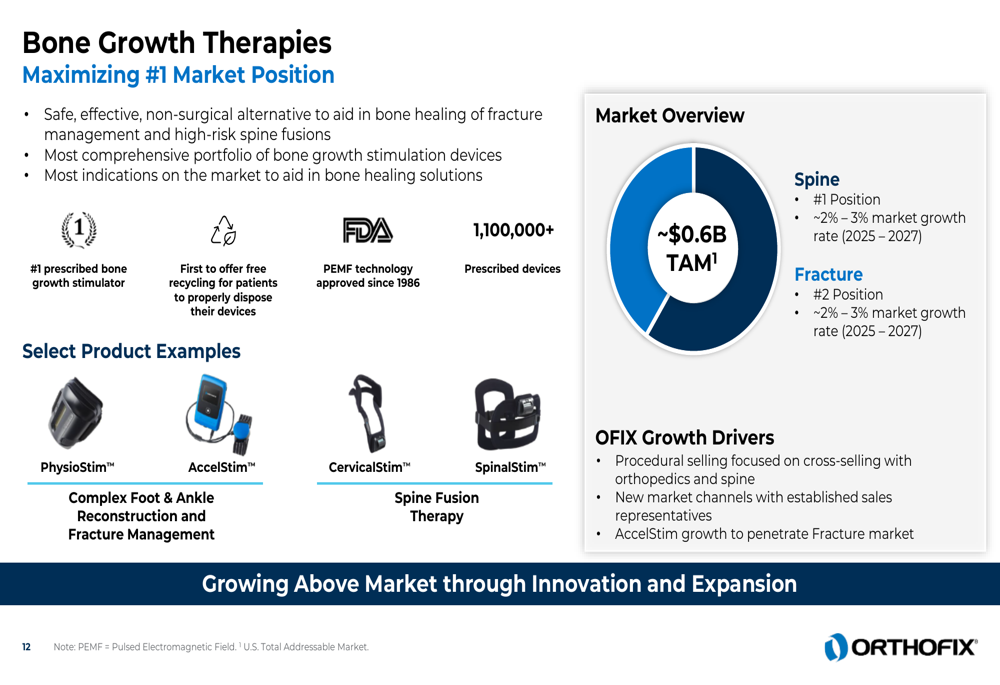

A key focus area for Orthofix is its Bone Growth Therapies business, where the company maintains the #1 market position in spine applications and the #2 position in fracture management. This segment represents a total addressable market of approximately $0.6 billion with projected market growth of 2-3% from 2025-2027.

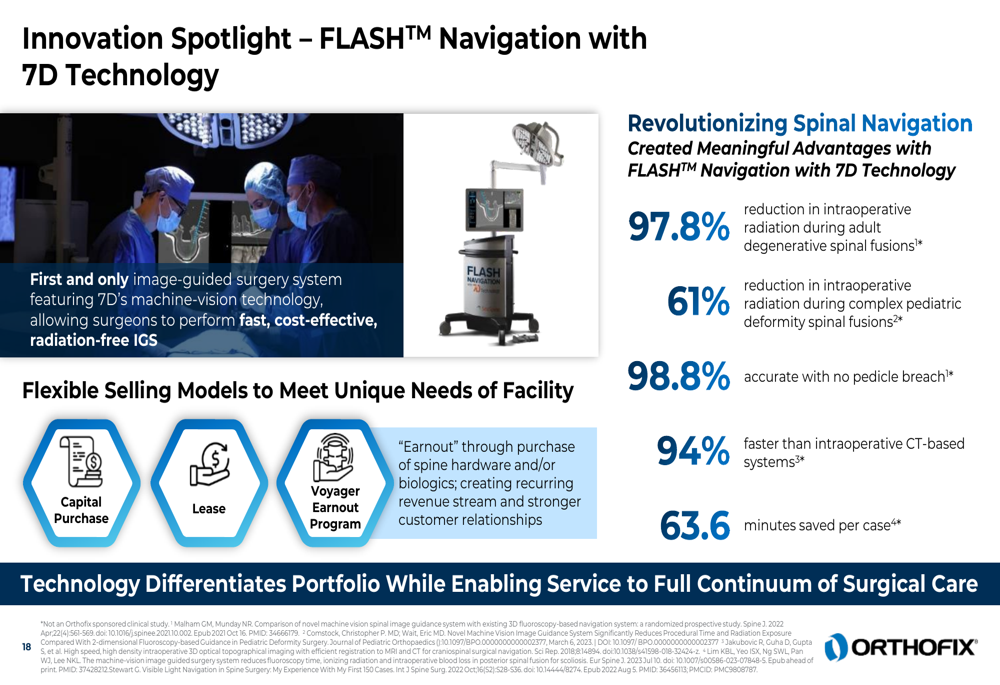

Innovation remains central to Orthofix’s strategy, particularly in enabling technologies. The company’s FLASH™ Navigation with 7D Technology is positioned as a significant differentiator, offering radiation-free image-guided surgery with substantial clinical and operational benefits:

The company is also pursuing cross-portfolio commercial opportunities, leveraging synergies between its various product lines to maximize value and drive growth:

Forward-Looking Statements

Orthofix maintained its full-year 2025 guidance, projecting net sales of $808-816 million, adjusted EBITDA of $82-86 million, and positive free cash flow for the year. This guidance excludes sales from the discontinued M6 product lines and assumes a $5 million negative impact from U.S. funded non-governmental organization business compared to 2024.

This guidance aligns with the company’s longer-term targets announced during its Q3 2024 earnings call, which included a 6-7% compound annual growth rate in net sales from 2025 to 2027 and mid-teens adjusted EBITDA margins by 2027.

Detailed Financial Analysis

Orthofix’s current financial position shows a company in transition, working to improve profitability while maintaining growth. The company’s snapshot reveals a market capitalization of approximately $538 million, trailing twelve-month net sales of around $783 million, and adjusted EBITDA of $75.7 million.

The company’s balance sheet as of March 31, 2025, showed cash, cash equivalents, and restricted cash of approximately $60.5 million. Free cash flow, while still negative at $(25.1) million for Q1 2025, showed year-over-year improvement, suggesting progress toward the company’s goal of positive free cash flow for the full year.

The significant premarket stock decline following the earnings release contrasts with the company’s generally positive presentation. This may reflect investor concerns about the pace of improvement in profitability metrics or cash flow generation, despite the revenue growth across segments.

Looking ahead, Orthofix’s focus on high-growth areas like limb reconstruction and enabling technologies, combined with its efforts to improve operational efficiency, will be critical to achieving its long-term financial targets and rebuilding investor confidence.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.